Some people observed 9/11 by lighting candles, others by killing more Americans.

Yesterday a mob stormed the U.S. Consulate in Benghazi, Libya, killing the U.S. ambassador to Libya and three other Americans. Among other implications, this raises the possibility that the stability that seemed to have returned to that country may be short-lived.

As of May, the EIA estimates that the world was producing 75.3 million barrels a day of crude oil (not including natural gas liquids, biofuels, or refinery processing gain). That’s up a million barrels a day from where it had been last October. However, all of the gains since October came from the return of Libyan production after the unrest seen there last year.

|

A crowd of 2,000 had also gathered at the U.S. embassy in Cairo, Egypt, though no one was killed there. The U.S. embassy in Algeria today issued warnings to Americans there. Last Friday, Canada closed its embassy in Tehran, Iran.

In other news, while some have speculated that Venezuela’s leader Huge Chavez may be terminally ill, on Monday he warned of a possible civil war if his policies are opposed. In Nigeria, Islamist groups are conducting open warfare on churches and police stations. In Iraq, 75 people were killed and 300 wounded in a wave of attacks on Sunday, and the fugitive vice president was sentenced to death by hanging.

Below I provide data on the importance of the countries just mentioned for world oil production. The table leaves out Egypt, which by itself only produces a little over a half million barrels a day, though another 2 mb/d travel through the Suez Canal and SUMED pipeline.

| Country | Oil production | % of world total |

|---|---|---|

| Libya | 1.4 mb/d | 1.9% |

| Algeria | 1.5 mb/d | 2.1% |

| Venezuela | 2.2 mb/d | 3.0% |

| Nigeria | 2.5 mb/d | 3.4% |

| Iraq | 2.9 mb/d | 3.9% |

| Iran | 3.5 mb/d | 4.7% |

| Saudi Arabia | 9.8 mb/d | 13.1% |

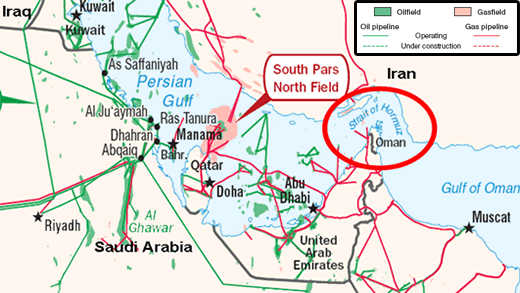

The table also includes Saudi Arabia, for which I did not highlight a specific recent news development. But note that even if all remains calm in the kingdom, most Saudi oil is currently getting to market as part of the 17 mb/d going through the Strait of Hormuz.

|

Closely related: Here’s a simple tool for projecting how much the price of a barrel of oil might change assuming you know how much the supply might be disrupted, and here’s a variation of that tool that will let you estimate how much markets believe the supply of oil passing through the Strait of Hormuz may be affected, assuming you know how much of an additional “premium” is built into the current price.

Is anyone else curious why oil did not take a jump today? If world events have such a great impact on the price of oil shouldn’t the killing of an American Ambassador in a major oil producing country cause a rise?

Jim: That’s a great (and terribly sad) opening line.

Ricardo,

Do you expect a strong response from the current administration against Libya that would in any way affect Libyan oil production?

Note the Libyan attack was a battle between the attacking Libyans and the Libyans defending the US property and people. According to the latest stories, the Libyan security detail not only fought back but local people – referred to as militia but who knows – joined them in the battle. So it wasn’t as simple as portrayed and, frankly, less one-sided than the invasion of US property in Egypt, which has the security people to stop whatever it wants in Cairo.

To be fair, Iran is down nearly 1 mbpd from August last year. So the numbers are a bit better than they look.

Also, the removal of Chavez should be taken as a bullish sign for the Venezuelan oil industry.

In Argentina, the nationalized YPF is looking the increase production by 7% per annum. But lo! They have no money, no investors. At some point, reality will break Cristina, but it could be a few years. In any event, the longer term is bullish there.

Petrobras is facing up to reality with reduced production schedules. I think we’ll see some improvement there, but no miracles.

Expect Russia to improve its oil governance, but with a lag, and it may be only sufficient to hold production levels there.

I think big money pre-salt finds in Africa will encourage more offshore development there–again, these are long lead time items, although Exxon’s Kozimba satellites in Angola just came on line (and not too soon for a company which had repeatedly blown its production forecasts!).

Iraq is a wildcard. Global forecasts depend heavily on Iraq for incremental production. The collapse of governance there could be a serious blow, but doesn’t seem in the cards right now. But if you’re looking for downside risk, that one be one country to track.

I’ve run the numbers on Saudi. They have a good bit of firepower left, I think. However, their national expenditures have been rising in the double digits, and our forecasts suggest oil prices will rise by only around 7% from here out. Thus, Saudi will face a choice between limited expenditure growth or higher production levels. Risks there may become unmanageable, but by the numbers, only after 2020.

Of course, the biggest downside risk is the US. The US contributed half of global production growth in the last year, and a good bit of incremental growth is slated for us. Should the shales turn into a flash-in-the-pan, then the future will look a good bit less optimistic.

But the point is taken: Oil comes from politically volatile regions of the world. There’s always something.

Oh, and by the way, according to the EIA, peak oil–crude oil and lease condensates–on a full year basis remains 2004, with 74.4 mbpd. The next best year is 2011, with 74.1 mbpd. (This is consistent with Ken Deffeyes’ forecasts at the time.)

I might also add that, according to Barclays Capital, global upstream spend in 2004 was less than $300 bn. In 2012, it will exceed $600 bn.

What has that extra $300 bn / year bought us, exactly? Not much, it seems.

Regarding US Shale Plays to the rescue, there have been several very interesting articles and studies released recently. Two studies are especially interesting, one by the USGS, and another, an SPE (Society of Petroleum Engineers) paper on the Eagle Ford Shale Play.

http://energypolicyforum.com/?p=505

USGS Releases Damning EUR’s For Shale

By Deborah Rogers

http://energypolicyforum.com/?p=526

Shale Oil Reserves Questioned Too

By Deborah Rogers

http://www.energybulletin.net/stories/2012-09-12/magic-shales

The Magic of Shales

By Deborah Rogers

http://online.wsj.com/article/SB10000872396390443589304577635783532976456.html?mod=WSJ_article_comments#articleTabs%3Darticle

The Shale Revolution: What Could Go Wrong?

Excerpt:

So why is John Hofmeister, the former chief of U.S. operations for Shell, sounding an alarm? “Unless something seriously changes in the next five years,” he said in an interview, “we’ll be standing in gas lines because there won’t be enough oil to go around.”

The reason is that there’s still disagreement over the factors governing the growth of production from the new fields. Among those factors: the direction of global supply and demand, how price will help or hinder exploration, whether new regulation will impede development, and how long it will take to build the infrastructure needed to get more oil to market.

Mr. Hofmeister said he believes forecasts also understate the “decline” rate of shale fields. The hydrocarbons tend to flow robustly in the first months of drilling, then decline before plateauing at lower levels. To sustain growth, companies will need to drill many wells at a rate “beyond the capacity of the industry as currently defined,” he says. “Those who ballyhoo oil shale and say that this will take care of us—no, it won’t.”

Regarding global supplies, following is my “Trends that can’t continue” chart, showing the decline in the ratio of Global Net Exports of oil* to Chindia’s Net Imports (GNE/CNI) versus the increase in total global public debt:

http://i1095.photobucket.com/albums/i475/westexas/GNE-CNI_total-debt_PS1.png

*Top 33 net exporters in 2005, BP + Minor EIA data, total petroleum liquids

At the 2005 to 2011 rate of decline in the GNE/CNI ratio, the Chindia region alone would theoretically consume 100% of GNE in only 18 years, which of course won’t happen, and there are already signs of weakening demand in the Chindia region.

But we can do some “What-if” Scenarios.

Available Net Exports (ANE), or GNE less the Chindia region’s net exports, were 35 mbpd in 2011, or 12.7 Gb/year (versus 40 mbpd and 14.6 Gb/year in 2005).

Here are two post-2011 Available CNE (Cumulative Net Exports) estimates for two rates of decline in the GNE/CNI ratio:

8.7%*/year: 110 Gb

4.3%/year: 235 Gb

*2005 to 2011 rate of decline

To put these numbers in perspective, note that Available CNE for 2006 to 2011 inclusive were about 81 Gb. As I have frequently pointed out, in my opinion we are only maintaining something resembling Business As Usual because of a sky-high rate of depletion in post-2005 Global and Available CNE.

Steven, in the case of Iraq you have huge political divisions.

You basically have a Shiite PM who has grabbed all the major intelligence/enforcement ministries for his own people, and the country has a solid 35 % Sunni minority who were used to being in power(when Saddam ruled the roost).

Not only that, most of the oil is in Sunni areas.

Second, Iraq faces plenty of bottlenecks. They need tons of infrastructure to put in place and they won’t get to 5-6 mb/d until 2016/17 at the earliest.

Third; Brazil is a huge disappointment. They have been around 2 mb/d for many years now.

Petrobras came out recently and basically admitted that they don’t expect production to increase much the next two years as there are already significant declines from their Campos field(which is where 85% of their oil produced comes from, mind you, so how bright do you think that place is?).

They’re already in a position where all the delays and costunderestimation means that just staying still will be a challenge.

Venezuela? Whoever is after Chavez won’t be different. The lure of a piggybank to give out to the people is just too big.

The only point I’d agree with you is on Saudi. They are capable to inch up to about 12.5 mb/d in production and keep it there for a decade or two. However, it isn’t “spare capacity”. They’re going almost flat out as of now. If they want to get to 12.5 mb/d it would take a year or two to get there, but they can do it.

U.S. shale oil is a bubble. It will render about 2 mb/d to 2.5 mb/d at the maximum. The decline rates are astronomical – 40%!

You have a year left for ramping up production. Entering 2014, you’ll see a marked slowdown and then the challenge is to keep it at those levels from mid-decade onwards with huge decline rates.

NGPL is 9 mb/d. It could get to 12 mb/d by 2020 with some luck.

But all of these things are not going to replace 4.5 mb/d(3.5 mb/d just current capacity and then 1 mb/d in new demand each year) every year going forward.

The CEO of CoreLabs says we got 2-3 years left before the peak and he has access to most of the new plays in the world; and they are the biggest at Brazilian plays.

I personally think we got more. I think we can stretch it perhaps 4-5 years. And I think the decline will be milder than most assumed(I am leaning towards 1% per year), so we’ll manage but it will be very difficult for most people.

Still, anyone who does the basic math can see that we’re already peaking, but the peaking itself is a multi-year event which is drawn out with stops and starts.

But we’re getting there.

The only way we’ll be sitting in gas lines again is if we have Nixonian price controls. Otherwise the price of a scarce resource simply adjusts.

B Turnbull,

I have come to expect nothing from this administration. I am so angry at how Obama has handled this situation with the murder of our ambassador I could spit. Going to Las Vegas to party with his friends and raise money was sick and derilection of duty. He is supposed to be the Commander-in-Chief but he is more like the way he describes himself in his youth. Willful incompetence.

Yes, Skeptic. I largely agree.

Iraq looks to do +0.5 mbpd / year, which gets you to 5-6 mbpd in the 2016/2017 range. So we’re in agreement there. But that’s still a pretty good performance.

I agree on Saudi.

I disagree on Venezuela. Nothing has been done under Chavez. I think his successor will look to improve performance. You’d be surprized how conservative nominally left wing governments can be. My uncle is now on fiscal policy council in Peru. That’s like inviting Ron Paul to address a labor rally, but there you have it. A successor may look around to see how Venezuela’s situation can be improved. It doesn’t take a genius to see that the easiest method is to increase oil production.

So I’ll take the long position on that one. But again, we’re talking about major investments in upgraders, for which the time lag is significant. In terms of volumes, maybe an incremental 1.5 mbpd by 2020 or so. Nice, but little impact on the overall picture.

I wasn’t disappointed in Petrobras, because my view was already modest. I was publicly skeptical when they were still flavor of the month. But Petrobras is saying 2.5 mbpd for 2015, and I think that’s acceptable. Petrobras is at 4.2 mbpd for 2020 (reduced from 5), we’re at 3.5. Some of the banks are a bit below that. That’s not terrible, but I think growth in production will be consumed domestically, so I don’t think Petrobras developments will improve Jeffrey’s net export market.

I don’t have an independent view on US shales. At the low end, we have 2 mbpd total shale/tight oil production, at the high end, 5 mbpd. O&G Journal puts sustainable Bakken production at 1.5 mbpd, and I thought the reasoning looked pretty good in the article. The Eagle Ford is on pace to outproduce this, and then there’s the Permian. Then we have the Mississippian, the Utica and the Monterey. One major producer is looking at the layer beneath the Monterey–I don’t even know what it’s called. So, notwithstanding high decline rates, there are a number of basins not yet in play.

I don’t have a clear sense of the balance over time. In June, people were talking 2 mbpd. In August, they were saying 5 mbpd.

And this is just US shales.

I do, however, agree that all the talk of peak oil being dead is pre-mature. Overall, we have been unable to move the needle for more than seven years.

Steven Kopits,

Thanks for the analysis. Very good.

Patrick R. Sullivan,

Thanks for the words of sanity.

Re: Gas Lines

I agree.

However, the primary point that Hofmeister was making was in regard to US shale plays, which was as follows:

Mr. Hofmeister said he believes forecasts also understate the “decline” rate of shale fields. The hydrocarbons tend to flow robustly in the first months of drilling, then decline before plateauing at lower levels. To sustain growth, companies will need to drill many wells at a rate “beyond the capacity of the industry as currently defined,” he says. “Those who ballyhoo oil shale and say that this will take care of us—no, it won’t.”

Steven,

The latest numbers on Bakken are out.

As I thought, production is already decreasing in speed. The increase in July this year over last year is over 50 %, an impressive number.

But the increase in April and May this year over last year was over 70 %. So in just a few months, 20 % growth has been lost. I think we’ll get under 30 % by early next year and then get to about 10 % by the end of next year in production growth.

And then, by 2014, as I’ve written above, we’ll start to see the flatlining. Eagle Ford is catching up to Bakken but I don’t expect a major deviation from Bakken’s production growth. I think Eagle Ford can have a higher maximum production, perhaps 1.2 mb/d.

All in all, I expect around 2 mb/d to 2.5 mb/d total tight oil from the U.S. over the long term as the older parts of Bakken starts to drag on the newer and the production growth is slowing and the easiest/lowest hanging fruit will by then already been picked since long ago.

I think your estimate of Brazilan production at 3.5 mb/d is probably optimistic but it’s still within the realistic range.

Canada to me seems to be the only country which has the potentional to largely fulfill the projections it has made(about 4.5 mb/d to 4.7 mb/d).

Venezuela’s problem isn’t dependent on a single leader. It’s a culture in Latin American countries where you take the oil company and use it as a piggy bank. This has been the fate of Pemex and the Venezuelan counterpart.

Even Petrobras, which sold itself to the world as more professional, is falling into the same trap as it’s used as a tool by politicians to increase domestic employment at the expense of genuine international expertise. The result if the flatlining we’ve seen.

Venezuela isn’t going to have an oil revolution because it’s more backwards than either Brazil or Mexico and how do you think it will play if a bunch of International oil companies come in, with their own workers and experts, and start drilling?

Whoever is PM will be massacred in the Congress and his own party will stage a mutiny and kick him out.

B Turnbull,

I looked back at my response to your question about the actions of this administration and I believe that your question deserves a more direct response. I apologize to you for not addressing your valid question. I was just so angry at the incompetence of this administration I had to vent.

To address your question directly, what is happening in North Africa and other Islamic states is a direct reaction of the Islamic radicals to the Democrat Convention. In each state from Egypt to Australia the crowds are chanting “Obama, Obama we are all Osama.” They are not chanting against some stupid Egyptian criminal making a very bad YouTube video that no one had heard of until it was brought out as an excuse for the rioting. If you listen to the rioters themselves they tell you who is causing them to riot. It is one thing to take credit for directing a military action against an enemy but it is totally different when night after night in speech after speech Obama is raised up as the killer of Osama bin Laden. How do you expect his followers to react? It was just one more stupidity to come out of this fiasco of a convention.

That said I do not believe there will be direct action by this administation that would interrupt oil flow – they seem paralyzed by events and totally over their head in this crisis – but their mishandling of foreign policy has created political unrest to the point of very serious radical threats to disrupt the flow or oil not the least the terrorist threat to close the Strait of Hormuz.

http://online.wsj.com/article/SB10000872396390444023704577650052651105074.html?mod=WSJ_Opinion_BelowLEFTSecond

Noonan: The Age of the Would-Be Princips

An idiot with a video camera has the terrifying power to change the world.

Excerpt:

Whatever the exact impact of the anti-Muhammad hate film that went viral, we have entered an age of would-be Princips.

Gavrilo Princip of course was the assassin who killed the Archduke Franz Ferdinand and his wife on June 28, 1914. He was 20, largely friendless and small in stature. He pulled the trigger that killed the archduke which led to the ultimatums that brought the war that misshaped the 20th century. From his act sprang nine million dead, Lenin at the Finland Station, the fall of Russia, the rise of communism, World War II, the Cold War . . .

Maybe all those things would have happened anyway, one way or another. We’ll never know. All we know is how it did begin, with one young man and a gun.

Now in the age of technology, with everything disseminated everywhere instantly, it isn’t one man with a gun but one man with a camera, or a laptop, or a phone.

Interesting reference to “peaked production” in Saudi Arabia in the following column.

In any case, we can argue about what Saudi Arabia may produce in the future, but what the post-2005 data show so far is that their annual production, for six straight years, has not materially exceeded their 2005 annual production rate (2011 annual crude oil production was slightly below 2005 annual level, 2011 total petroleum liquids production was slightly about 2005).

And because of rising internal consumption, Saudi net oil exports have been well below their 2005 level for six straight years, now going on seven straight years, even as annual global crude oil prices doubled from $55 in 2005 to $111 in 2011.

If we see some serious disruptions to Saudi oil exports, because of domestic unrest, things could get very “interesting” very quickly in oil importing countries.

http://www.washingtonpost.com/opinions/next-up-in-the-middle-east-mess-saudi-arabias-succession-fight/2012/09/14/b316e7ec-fd44-11e1-a31e-804fccb658f9_story.html

Next up in the Middle East mess? Saudi Arabia’s succession fight

Excerpt:

From afar, the kingdom of Saudi Arabia appears immune from the turmoil and uncertainty engulfing nations such as Syria, Egypt and Libya. But rather than being an oasis of stability in the Middle East, Saudi Arabia is nearing its own crisis point. . .

The three historic pillars of Saudi stability are cracking. Massive oil revenue, which has bought public passivity, is threatened by peaked production and sharply increased domestic energy consumption. A supportive Wahhabi Islamic establishment that bestowed legitimacy on the House of Saud is increasingly fractious and is losing public credibility. And now, the royal family is in danger of division as it is forced to confront generational succession.

The statement that a “mob stormed the embassy” in Benghazi and killed the ambassador is factually incorrect. It was an organized paramilitary squad of some sort, using powerful weapons.

The author of the column linked above on Saudi Arabia is Karen Elliot House, and she is the author of a book on Saudi Arabia coming out next week:

http://www.amazon.com/On-Saudi-Arabia-People-Religion/dp/0307272168/ref=cm_cd_pdp_t?_encoding=UTF8&cdPage=1&newContentID=Tx2W5GDKGRKTJE8&noLL=1#CustomerDiscussions

On Saudi Arabia: Its People, Past, Religion, Fault Lines – and Future

Karen Elliott House (Author)

Excerpt from Amazon:

From the Pulitzer Prize–winning reporter who has spent the last thirty years writing about Saudi Arabia—as diplomatic correspondent, foreign editor, and then publisher of The Wall Street Journal—an important and timely book that explores all facets of life in this shrouded Kingdom: its tribal past, its complicated present, its precarious future.

Through observation, anecdote, extensive interviews, and analysis Karen Elliot House navigates the maze in which Saudi citizens find themselves trapped and reveals the mysterious nation that is the world’s largest exporter of oil, critical to global stability, and a source of Islamic terrorists.

In her probing and sharp-eyed portrait, we see Saudi Arabia, one of the last absolute monarchies in the world, considered to be the final bulwark against revolution in the region, as threatened by multiple fissures and forces, its levers of power controlled by a handful of elderly Al Saud princes with an average age of 77 years and an extended family of some 7,000 princes. Yet at least 60 percent of the increasingly restive population they rule is under the age of 20.

“the stability that seemed to have returned to that country may be short-lived.” Difficult to be more wrong than that!

Since Qaddafi is gone from Libya so is stability and it is not anywhere close to returning to the country in spite of the overwhelming wishes of the population.

To understand why, it is essential to realize that Libya is the opposite of Egypt. Egypt is a cauldron with a huge bulging population and no resources. A great culture on the verge of the abyss. Libya has a sliver of land with a tiny population and plenty of resources in the desert. But the area never really became a country before the Italians said it was one just before WW2 and even after that the tribal system remained the main structure of the country, beside Qaddafi of course.

It is consequently quite normal that after the fall of Qaddafi, the country returned to this earlier level of organization with all the dysfunctional aspects it implies. The tribes of Benghazi who won the civil war now control very weakly the country from Tripoli with much resentments from the other parties and little means to exert their power except through force, which is still limited and invites even more resentment.

The attack in Benghazi was therefore not a slap to America but a slap to the Libyan government. This is essential to understand because it means that there is very little America can do except help the current government strengthen its power. Anything else will help those who committed the aggression and weaken the government.

In the short term, it does not really matter in Libya. Oil is relatively well protected and out of reach. But thanks to over 10 years of American intervention in the region, quite a few countries are ready to explode and at this stage almost anything can be used as a match.

It would be extremely surprising that nothing does in the coming months and when this happens, it is millions of barrels which will be taken away from the global market. If it last 2 months, the world can live with it. The price of oil will just shoot to 150$ faster than we expected. But if it last any longer, then we have a problem.

There is a huge frustration building up in the Middle East against the US, against Israel, against their government, against poverty. Some is legitimate, some is not but clearly these people want us to share their frustration and eventually they will find a way. This way is likely to be the oil market.

Thanks for the post.

As a layman, I also believe the ‘sweetness’ (is it a term?) also plays a role in oil prices, doesn’t it?

What about possible excess capacity in safe oil producing countries, existing storage, etc.? Is it possible to roughly estimate what would happen with the unsafe oil producing part of the world going ‘crazy’ in near term?