]]>

]]>

… on Monday, about 350,000 T.P.S. recipients from Haiti and several other countries will lose their work permits in the first wave of fallout from the Supreme Court ruling. About 190,000 Salvadoran beneficiaries could be next to lose their status when it expires in September.

“For particular places and particular industries, tens of thousands of workers no longer able to legally work is going to be a very big hit,” said Alexander Arnon, the director of policy analysis at the Penn Wharton Budget Model, a nonpartisan research organization that has analyzed the economic impacts of T.P.S. workers.

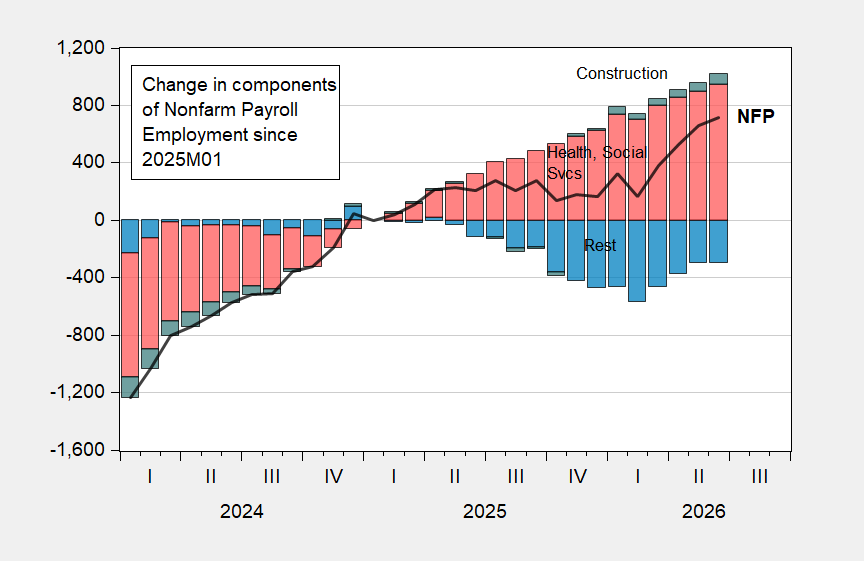

This is on top of the crackdown on migrants the administration has been pursuing. Heavily affected by these measures would be health care/social services and construction. The former has been a main constituent of employment growth over the last year.

Figure 1: Change since 2025M01 in total nonfarm payroll (NFP) employment (bold black line), hoealth care and social services employment (salmon bar), construction (green bar), rest of NFP (blue bar), all in 000’s, s.a. Source: BLS and author’s calculations.

]]>

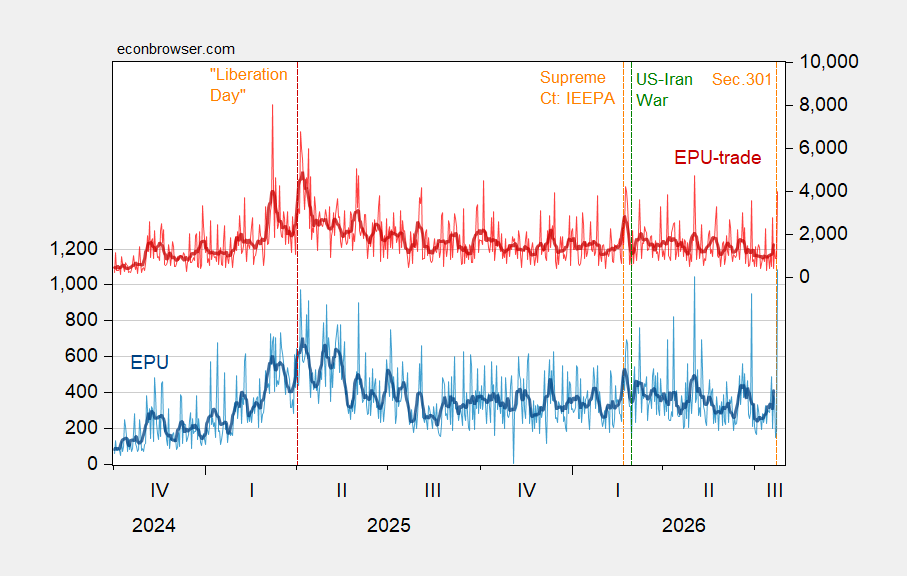

Figure 1: Economic Policy Uncertainty (blue, left scale), 7 day centered moving average (bold dark blue, left scale), EPU-Trade Category (pink, right scale), 7 day centered moving average (bold red, right scale). Source: Policyuncertainty.com accessed 7/25/2026.

Hence, even if the new Section 301 tariffs merely maintain the effective tariff rates under Section 122, trade policy uncertainty seems heightened (note the Section 338 tariffs threatened against Canada are only a few days before the new Section 301 tariffs).

]]>

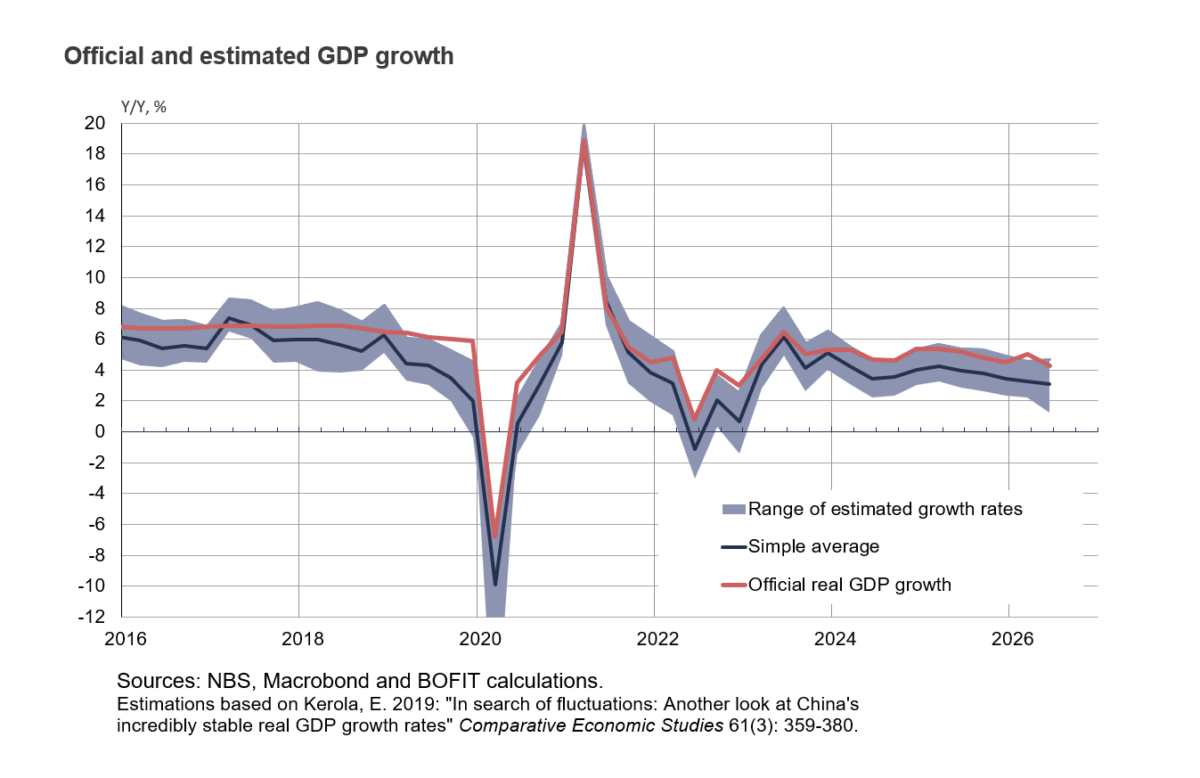

From the analysis:

Official figures show the Chinese economy grew by 4.3 % y-o-y in the second quarter of this year (up 3.6 % q-o-q annually adjusted), missing China’s official 4.5–5 % target range for the year. Weak household demand and lower fixed investment reduced growth from 5 % y-o-y in the first quarter (up 5.3 % q-o-q). BOFIT’s alternative GDP calculations indicate Q2 growth slowed to 3.1 % y-o-y (3.2 % in 1Q). Our estimated alternative GDP growth rate band also widened considerably (1.2–4.7 %). The IMF’s updated World Economic Outlook released earlier this month raised its Chinese GDP growth forecast for 2026 by 0.2 percentage points to 4.6 %, and by 0.1 percentage points to 4.1 % for 2027.

China CAT from the SF Fed which incorporates import data provides estimates only through Q4; it too suggests official above alternative estimates of GDP growth.

]]>

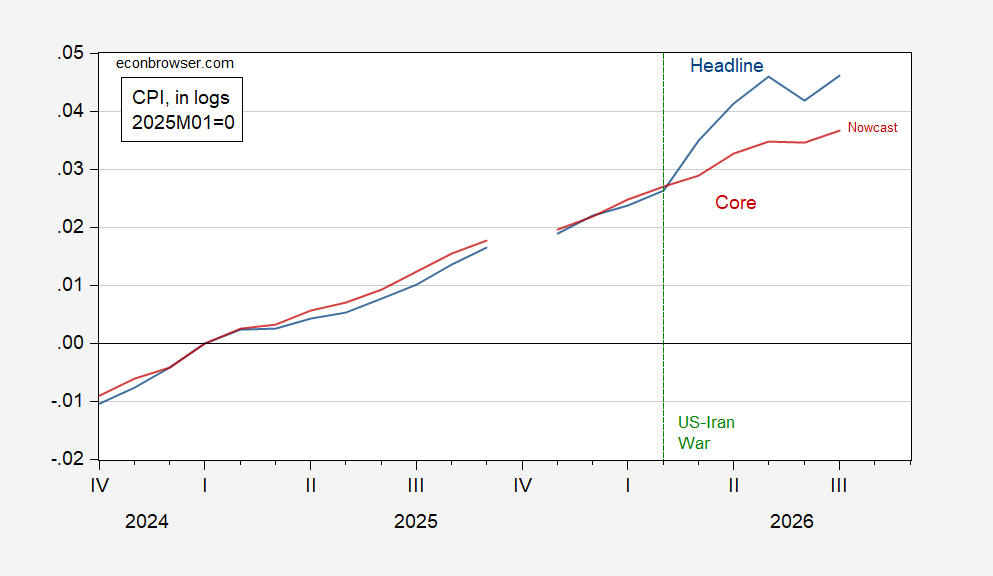

Figure 1: CPI (blue), core CPI (red), both in logs 2025M01=0. July is July 23 m/m nowcast. Source: BLS, Cleveland Fed, and author’s calculations.

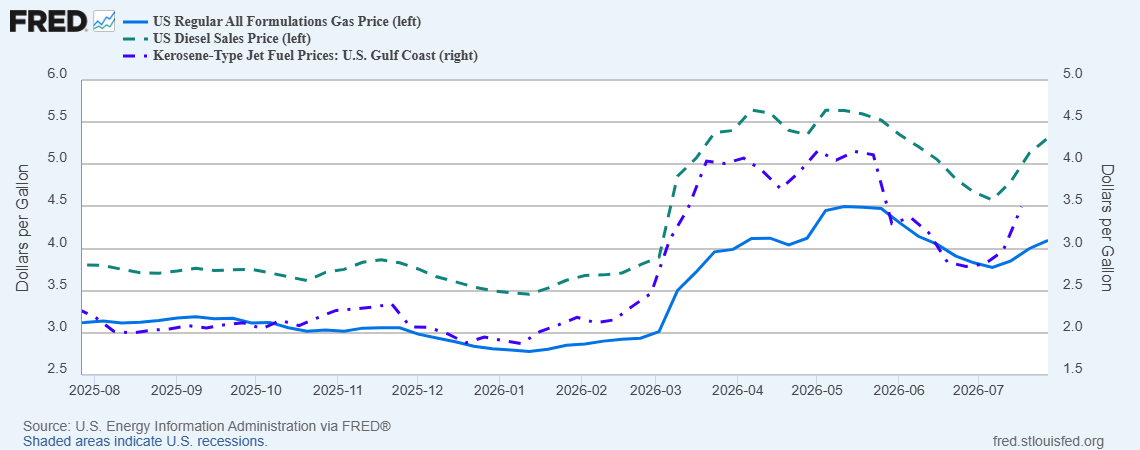

These nowcasts incorporate EIA’s gasoline price data through 7/22, as well as oil prices.

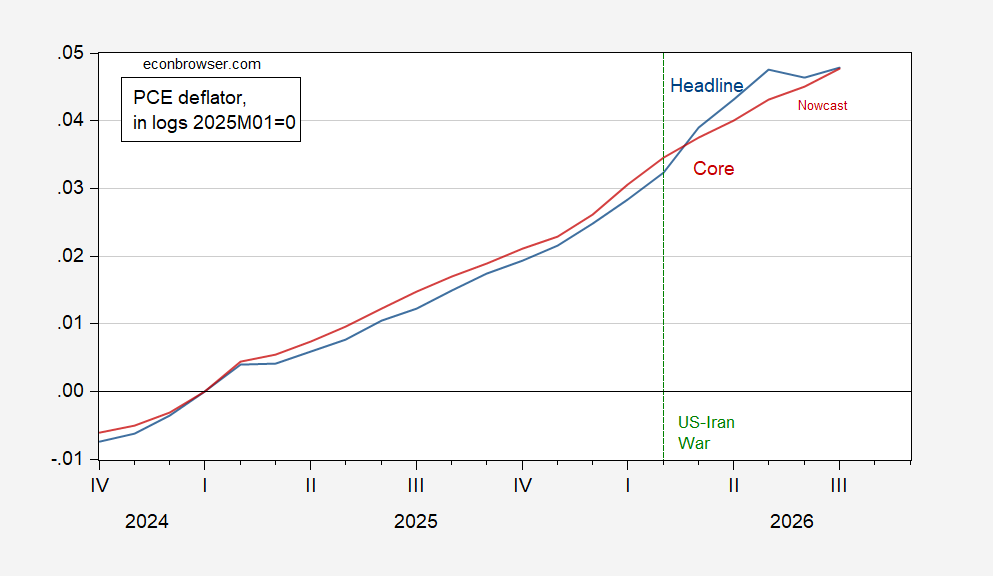

In terms of the Fed’s preferred measure:

Figure 2: PCE deflator (blue), core PCE deflator (red), both in logs 2025M01=0. June and July are July 23 y/y nowcast. Source: BLS, Cleveland Fed, and author’s calculations.

Nowcasts are only nowcasts. However, with gasoline prices rising without apparent stop (see graph below), it seems unlikely that these nowcasts will prove to be overshooting.

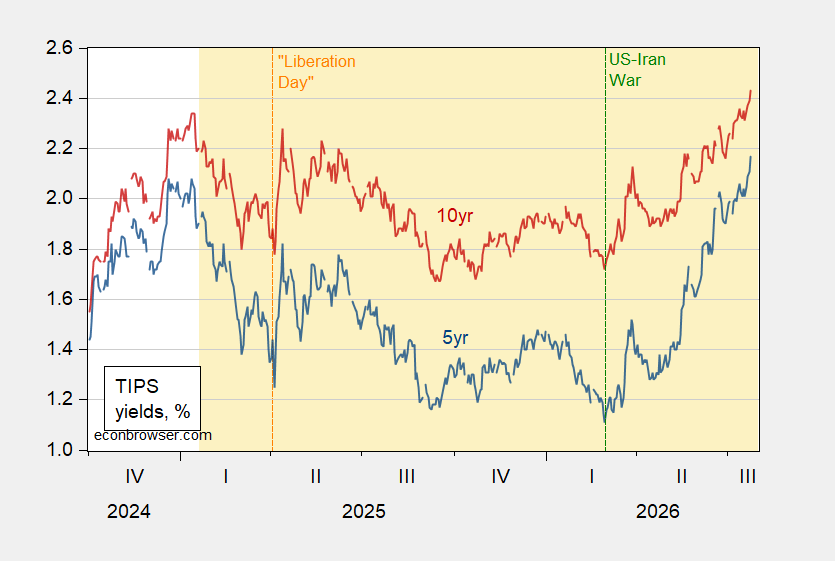

Figure 1: TIPS 5 year yield (blue), 10 year yield (red), both in %. Source: Treasury.

]]>

Fifty years ago this month, I was one of a team of five MIT graduate students who were in Lisbon working for the Central Bank of Portugal. Paul Krugman, another member of that team has reminisced, on the occasion of the semicentennial of the 1976 mission. So, I will contribute my own reflections on that summer in light of where we are today, geopolitically.

Two years before, Portugal had ended a 48-year military dictatorship[1] in its “Carnation Revolution” of 1974. It had then swung from right-wing to left-wing — the government had taken over some parts of the economy, as marchers in the street chanted, “muerte à CIA,” a slogan that we saw still visible painted on the walls (as Paul notes). But the country had turned back from an attempted left-wing coup in November 1975, setting the stage for a new beginning.

At the time of our arrival in June 1976, Portugal was about to hold its first democratic elections in living memory. The favored candidate for president was António Ramalho Eanes, an army general who had led the forces countering the attempted coup in 1975 and had already become a reassuring figure of stability and guarantor of democracy. But it was going to be the job of the new Prime Minister and cabinet to run the country, and that government wasn’t formed until July 23rd.

The economy was in crisis. In particular, the budget deficit was ballooning, and the balance of payments was in severe difficulty, so that the central bank would soon run out of foreign exchange reserves. The Governor of the Banco de Portugal, Jose da Silva Lopes, wanted to have a plan of action all ready to go when the new government took office. To advise him, he had called upon some MIT Economics Department professors, who in turn sent us five Ph.D. students for the summer, into our first experience with international advising.

I remember on the plane over the Atlantic thinking, “I’m not sure that we have learned anything in our classes that can be of help to a real economy.” But we were to discover that we had.

Paul was the “brains” of the team, unsurprisingly. Miguel Beleza, a Portuguese classmate of ours who was later to become finance minister, knew “the ropes” of the country. Andy Abel was the one who managed to process our work through a refrigerator-sized computer that the central bank had been given but hadn’t figured out how to use. Ray Hill was the “adult” whom we put forward to speak for us on occasions when we 24-year-olds might be viewed as too young. (I think he was all of 29.) As for my role, maybe I was the one who would suggest, after an intense six-day workweek, that it was time to knock off and go to the beach. It was a memorable summer.

Portugal’s democracy began to put down roots that year and is going strong 50 years later. The escudo was devalued in February 1977, which was one of the things we had recommended. The country has become increasingly integrated into Europe, having joined the European Union in 1986 (a sign of its progress in democratizing). It progressed well enough to be a founding member of the euro in 1999 (a sign of the new-found stability of its currency). Today, it has been ranked the 4th freest country in the world and the 7th safest, which helps explain its popularity as a destination for visitors and investors. No more power failures. Some Americans have fled to Portugal, seeking a better lifestyle. It hosts several important NATO facilities. So, basically a success story, from the western viewpoint.

True, Portugal’s income has failed to converge with that of other Western European economies. That is an issue in domestic politics. But the critics tend to come from the right, attacking the (center-left) Socialists who have been in power for much of the last 30 years, rather than from the left attacking the basic market system.

The wages of the MIT team that summer were paid out of a grant to Portugal from USAID. But it took time for the wheels of USAID bureaucracy to turn: the money hadn’t shown up after the first month. Governor Silva Lopes rang a little bell in his office and had an assistant take us down to the basement to count out stacks of currency with which we could pay our hotel bills. I sometimes tell this story to my students as an example of “seigniorage”: a government prints money and gets to spend it directly.

More small anecdotes from the summer of 1976:

A Soviet trade mission occupied the floor above our offices. We would see them in the elevator and took care not to be trapped in it with them during the city’s daily power outages.

It seemed like there were only a few dozen Americans in Lisbon that summer, so soon after the attempted coup. That was evident from attendance of the community at the quiet bicentennial celebration on July 4 convened by the US Ambassador, Frank Carlucci . Meanwhile, Carlucci was apparently struggling to persuade the Secretary of State, Henry Kissinger, that Portugal was not necessarily lost to the Communists and the US should engage with the Socialist candidate for Prime Minister (Mario Soares).

By an astounding coincidence, my college roommate Alberto Mora was one of the few Americans in the country, working on political affairs in the US embassy at the time. He came by our office one day, on our way to lunch. I took him up the fire escape to see the fine view of Lisbon from the roof. It didn’t particularly bother me that the Soviet trade mission looked out on the roof patio. Foolishly, it did not occur to me that if he was caught lurking on the terrace adjoining the Soviet mission, it could cause an international incident. Alberto was not pleased when a door opened and a thuggish looking Russian came ambling toward us, as I belatedly whispered to him about the trade mission people. The Russian asked in broken Portuguese what we were doing there on the roof, and my friend answered, “oh, we are just here from the floor below, working with the Banco de Portugal.” Thanks to his State Department language training, his Portuguese was good enough to fool the Russian and we were able to beat a hasty retreat. (As for me, I can’t tell Portuguese apart from Russian.) I had been thoughtless indeed. Alberto and his family had emigrated to the US from Cuba in 1960. The Russians would have thought “CIA for sure.” He wasn’t, for the record.

Eventually, we wrote a report recommending something like a 15 % devaluation. We distributed copies to the senior economists in the Bank, hoping to mollify any resentment of our presence. When we told the Governor, he was alarmed, afraid of a leak. We reminded him that he had told us not to worry that the Soviets might eavesdrop on our work. His reply: “I am not worried about the Soviets; I am worried about the markets.” That night, we surreptitiously went back into their offices, recovered the copies of our memo off their desks, and replaced it with a version that used “measures to improve the trade balance” as a euphemism for devaluation.

We kept the USAID provenance of our pay secret, because locals might have concluded that we were really working for the CIA. In my thinking at the time, the US government was not a particularly helpful factor in the cause of launching Portugal’s democracy on a solid path. It was well-known that the US had supported the previous authoritarian government. I think I was even a bit resentful that we had to hide the thin USAID connection because of a history of ill-considered CIA meddling in other countries’ politics. (This was in the aftermath of a CIA-supported coup that overthrew a democratic government in Chile in 1973.

At the time, the MIT Five in Lisbon in 1976 were fledgling technocrats, setting off on our careers. In retrospect, we can be viewed as one small cog in the prosecution of the Cold War. One could only have dreamed that the US and Western Europe would peacefully prevail within 15 years in that contest.

We would never have even conceived it possible that one day the US might unilaterally abandon its role as leader of the rule-based, democratically oriented, market-based world order. But it has happened.

Among many other outrages, Donald Trump has hit the EU with illegal tariffs, dismantled US AID, and discombobulated NATO (ranting at the summit meeting last week because the Europeans have demurred from supporting his reckless attack on Iran). He ignores what he is told by the CIA and other intelligence agencies, angry at them for having reported accurately on Russian attempts to interfere with the US election in 2016 and on Russia’s imminent invasion of Ukraine in 2022. Almost single-handedly, he has torn down the open, democratically based, market-oriented structure that previous generations of western leaders worked so long and hard to build.

[1] Since 1926; Salazar, since 1933.

This post written by Jeffrey Frankel.

]]>

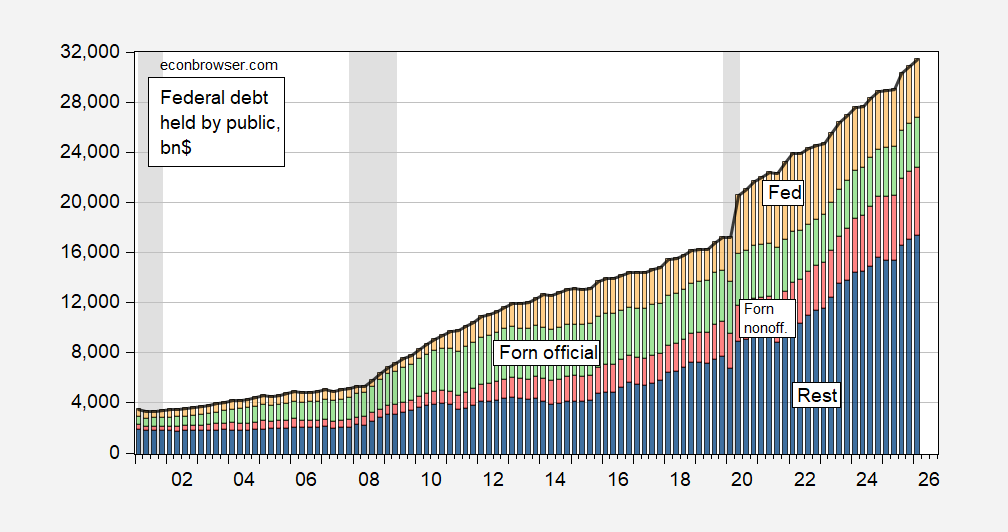

Figure 1: Total Federal debt held by public (black line), held by Fed (yellow bar), held by foreign official sector (green bar), held by foreign non-official (red bar), held by rest (blue bar), all in bn.$. NBER defined peak-to-trough recession dates shaded gray. Source: Treasury via FRED, TIC for 2026Q1 foreign holdings, and NBER.

Note the green bars over time. Normalized by GDP:

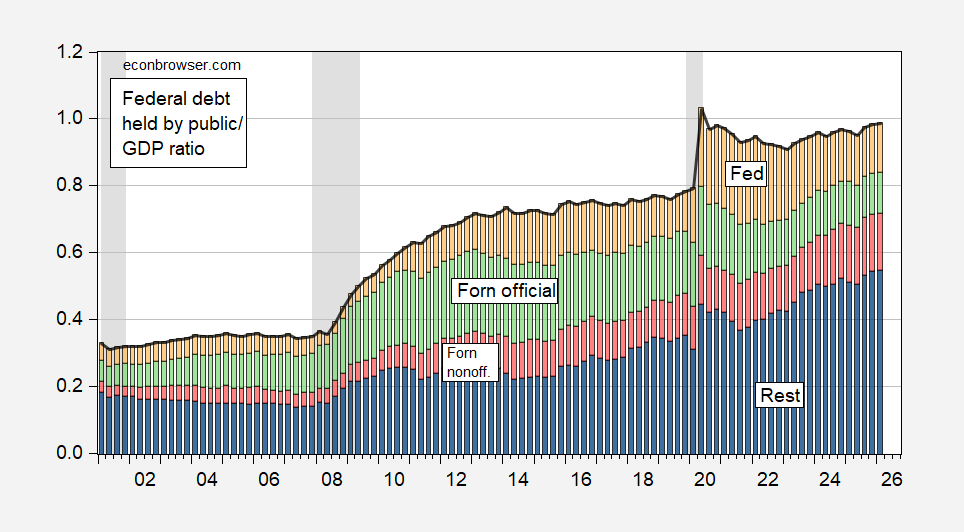

Figure 2: Total Federal debt held by public (black line), held by Fed (yellow bar), held by foreign official sector (green bar), held by foreign non-official (red bar), held by rest (blue bar), all normalized by GDP. NBER defined peak-to-trough recession dates shaded gray. Source: Treasury via FRED, TIC for 2026Q1 foreign holdings, BEA, and NBER.

]]>

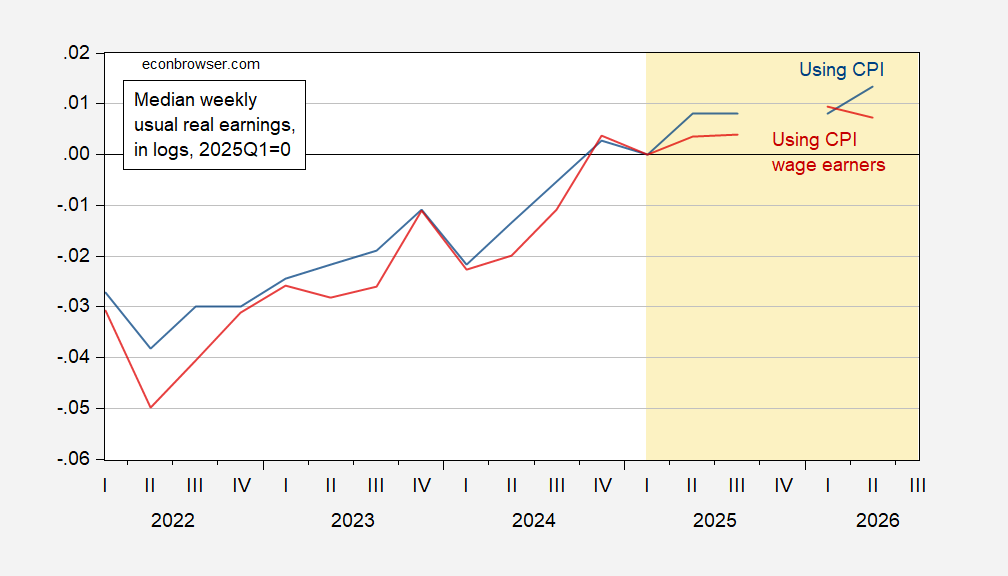

FIgure 1: Median weekly usual real earnings, deflated using CPI (blue), using CPI for wage earners and clerical workers (red), both in logs 2025Q1=0. Source: BLS and author’s calculations.

]]>