How did we get into this mess, and how do we get out of it?

First, a little background:

Both Freddie and Fannie were initially created by the U.S. Congress with the goal of expanding the residential mortgage market. They are for this reason referred to as “government-sponsored enterprises”, or GSEs, even though both eventually were converted into private companies for which there is today no explicit government guarantee of their debt….

After a homeowner has borrowed money to buy a home, the original lender likely resold that loan to Fannie or Freddie. The GSE in turn collected some of those mortgages in a pool which was sold in the form of mortgage-backed securities (MBS) to private investors, for which the GSEs collect a fee in exchange for guaranteeing payment on the MBS. Other mortgages purchased by the GSE are held directly by the GSE for its own investment portfolio. The GSEs obtained the funds for these investments primarily with money borrowed directly from private investors, which instruments are referred to as “agency debt”.

The table below provides a simplified balance sheet for Freddie Mac. Most of the nearly $800 billion in assets held by Freddie as of the end of 2007 consisted of mortgage loans or securities based on mortgages. The company acquired the resources to buy these assets primarily by borrowing, with outstanding debt as of the end of 2007 of $738.6 billion. The key item on the liabilities side of the balance sheet is stockholders’ equity, which represents the capital raised by Freddie through direct sales of stock and cumulative retained earnings. This equity provides a cushion against possible losses on any of its assets, in that the first $26.7 billion in losses would come out of the company’s original capital, with creditors losing nothing. That cushion, however, would only cover losses that were less than 26.7/794.4 = 3.4% of the assets.

| Assets | Liabilities | ||

|---|---|---|---|

| mortgages | 80.0 | debt | 738.6 |

| securities | 629.8 | other liabilities | 29.1 |

| other assets | 84.6 | stockholder equity | 26.7 |

| total assets | 794.4 | total liabilities | 794.4 |

Fannie’s 2007 stockholders’ equity came to 5.0% of assets.

| Assets | Liabilities | ||

|---|---|---|---|

| mortgages | 403.5 | debt | 796.3 |

| securities | 406.6 | other liabilities | 42.2 |

| other assets | 72.5 | stockholder equity | 44.0 |

| total assets | 882.6 | total liabilities | 882.6 |

These balance sheets leave out the mortgage-backed securities that the enterprises created and sold directly to outside investors, for which the enterprises have issued off-balance-sheet guarantees for payment. The OFHEO 2008 Annual Report to Congress states that Freddie had sold $1,381.9 billion in MBS and Fannie $2,118.9 billion. If you add together the mortgages retained outright by Fannie and Freddie (either as whole loans or MBS) plus the MBS that they have sold to others and offer a guarantee for payment, the OFHEO calculates a total “book of business” for the two enterprises of $4,934.4 billion as of the end of 2007, slightly less than the total publicly held debt of the U.S. government. Fannie and Freddie’s combined stockholders’ equity amounts to 1.4% of their total book of business.

Fannie and Freddie borrowed the funds with which this empire was leveraged at terms nearly as favorable as those for the Treasury itself. Unquestionably a key reason that investors have received agency debt so warmly over the years, and treated the guarantees as credible, was the assumption that Fannie or Freddie were too big for the federal government to allow to fail. This creates an unambiguous concern of moral hazard. When investors assume that the government will cover their losses, the result is a higher volume of funds flowing into the GSEs than is socially desirable. The upside goes to the lender, the downside is supposedly picked up by the government, and the result is the enterprise is expanded to a greater level of risk than makes economic sense.

|

The GSEs’ book of business represented 25% of outstanding residential mortgage debt in 1990 but comes to 41.4% today. It is hard to avoid the conclusion that these moral hazard distortions were one factor that contributed to the rapid expansion of mortgage debt over the last decade and attendant excessive price appreciation and risk taking. Granted, the real excesses, such as the subprime loans that everybody was initially discussing, came from MBS created by private institutions rather than the GSEs. But the stock market seems to be declaring pretty loud and clear this week that risks associated with enterprise assets are significant.

|

|

So where do we go from here? If we indeed reach a point where one or both of the GSEs can no longer honor its commitments, the Treasury’s contingency plan might follow the Bear Stearns philosophy of leaving shareholders nothing but protecting creditors and counterparties fully. But if the U.S. Treasury ends up assuming a significant burden, this would at a minimum raise the logistical question of how taxes are going to be raised to cover the costs. One strategy that holds some appeal would be to let the burden of the tax fall entirely on the creditors and counterparties themselves– in other words, no government bailout at all– as argued by Nouriel Roubini:

notice that the hit that bondholders will take will be limited in the absence of their bailout. With a debt/liabilities of about $5 trillion and expected insolvency– as of now and in the worst scenario of $200 to $300 billion– the necessary haircut is relatively modest: either a reduction in the face value of the claims of the order of 5% (if the mid-point hole is $250 billion) or– for unchanged face value– a very modest reduction in the interest rate on their debt after it has been forcibly restructured.

So what’s wrong with that idea? The overriding concern in dealing with the current mess is that the process of rapid and radical deleveraging would so impede the flow of new credit that the housing price declines, foreclosures, and bankruptcies significantly overshoot the values that we’d expect in a properly functioning credit market. In addition, I would worry about possible serious repercussions of a flight of foreign capital if there is a sudden perception that agency debt entails heavy risks.

The principle of “make those who caused the problem pay” has a lot of visceral appeal. But the principle of “don’t impose severe and gratuitous extra costs on those who had no role in causing the problem”– in other words, don’t make the housing depression much more severe just to teach somebody a lesson– has to be the basis for our policy decisions.

My recommendation would therefore be for a managed bailout in which the stockholders, creditors and taxpayers jointly share the bill.

And now we can haggle about the price.

Technorati Tags: macroeconomics,

economics,

housing,

Fannie Mae,

Freddie Mac

GSE,

credit crunch

I think the first thing to do is to recapitalize both companies by issuing new stock for cash and essentially diluting or freezing out the current shareholders. This should be done by way of a rights offering that would allow current shareholders to “pay to play”. The Federal government should underwrite the offering by agreeing to purchase unsold shares, but for each unsold share it purchases, it should receive a warrant allowing it to acquire more shares cheaply.

The second step should be the ritual of human sacrifice. Any of the top managers or directors who have been on-board for more than a year or two should be fired “for cause” and without unvested benefits or severance.

The third step is to institute new underwriting rules (actually go back to the old ones), a 20% down payment, PITI

But a bailout does impose gratuitous extra costs on those who had no role in causing the problem. Many taxpayers will bear these costs, while only some taxpayers will reap the benefits of the bailout. Homeowners and mortgage-holders will benefit from a bailout, but taxpayers who don’t own a home will likely be charged more in taxes than they benefit (particularly non homeowners who may buy a home in the near future)

I think what you mean to say is that you’d rather the gratuitous extra costs be imposed on as many people as possible, thus reducing the cost per person.

That is a mistake. The government has been pandering to homeowners for years by making mortgage interest tax deductible and by creating and implicitly guaranteeing the mortgage GSE’s. Those were mistakes, particularly the GSE’s. Now you want to compound the mistake by further pandering to home owners and mortgage holders? For shame.

The best policy is to let the GSE’s sink or swim. If they sink, then some constructive action might be taken. I read a suggestion somewhere that the goverment might help capitalize eight or so mortgage bundling entities, impose some strict regulations to prevent excessive risk-taking, and then let them sink or swim. I think that idea has a lot of merit. Free market survival of the fittest is what makes capitalism work so well. Bailouts are what makes investors and businesses take excessive risks. Let’s encourage the former, not the latter.

So, we clearly have a short-term big mess, and it is likely that many people who didn’t help create it will help pay for it, and maybe necessarily so.

Still, can you say more about:

The mechanisms by which this happened.

The position that we’d like to get to, with appropriate mechanisms for controlling the risk-cascade/free-money effects.

And then see if the short-term actions properly head towards the long-term goal.

The innocents is this mess are not those referenced continuously by Hamilton and the rest of the “community of university-based economists,” Thoma, deLong and their ilk.

The innocents are those who hold the currency of the United States of America, mistakenly thinking that it represents a store of vlaue.

The United States of America has evolved into a complicated con game with Paulson, Bernanke and those cited above the con men as their intellectual enablers,

and this is seen with crystal clarity outside of the USA.

http://blogs.ft.com/maverecon/2008/07/time-for-comrade-paulson-the-pull-the-plug-on-the-fannie-and-freddie-charade/

“In addition, I would worry about possible serious repercussions of a flight of foreign capital if there is a sudden perception that agency debt entails heavy risks.”

IMHO this will not be a consequence of Roubini’s plan,*once* it is implemented. Entities have trouble raising capital *before* restructurings when investors think they may lose their money. *After* the restructuring takes place, investors are *more* willing to put their money in, because the entity is stronger financially.

So, the best plan is: (1) haircut for bondholders, sufficient to raise 300-400 billion Usd; followed by, (2) guarantee by the U.S. of the debt, and (3) gradual winding down of GSEs.

Any discussion of what intervention is needed should either Fannie or Freddie fail must include a discussion of the impact on the banking system directly. Any lose to debt creditors will cause severe to catastrophic damage to the banking system.

The evaluation of capital adequacy of a banking institution is based on the idea of risk-based capital. For most banking institutions, a significant portion of securities held in the bank asset and liability portfolio are Fannie and Freddie mortgage backed securities and debentures. These are preferred securities because of their treatment under risk-based capital guidelines, their liquidity, their acceptance as collateral by the Federal Reserve, the ready ability to finance them in the repurchase agreement market, and the additional yield when compared to comparable US Treasury securities,

These securities are the marketable, or liquid portion of the banks balance sheets. Loses and re-categorization to a higher risk-based capital haircut will have a dramatic, detrimental, immediate effect on the capital adequacy of the banking system, increasing the pace of bank failure exponentially. Without liquidity, the banking system would be subject to the phenomenon of bank runs.

The implications of a Freddie and Fannie generated collapse of the banking system are far more costly than the bailout of the GSEs. Confidence must be restored in them. It is not a choice. So stockholders must pay the price, and so too, must the tax payer.

I think Fat Man’s suggestions above are pretty much on target. But he forgot to mention firing other people in the Federal Govt. who are not part of FNM or FRE but are actually paid to provide oversight of those agencies.

The stock price of the GSEs is largely irrelevant.

As long as the GSEs can borrow money at reasonable rates and their MBS trades well, they can keep the secondary market functioning. The Fed opened its discount window to Wall Street for the first time in history, and didn’t wipe out their shareholders or even take any equity. So, why shouldn’t the feds extend the same rights to the GSEs, when OFHEO just said that they’re “well capitalized?” Why do more than is necessary? (Is that because so many poliicians depend on Wall Street for campaign donations and post-government jobs?)

If the feds announce that it will not let the GSEs fail and opens its discount window, that is likely to be enough to stabilize the secondary market. If the government has to step in further, with real tax dollars, then the government should take more drastic dilutive measures, such as getting equity conversion rights or warrants.

Assuring borrowing rights for the GSEs would give confidence to future investors that the GSEs need for gathering additional capital. So, ironically perhaps, strengthening the federal backing would reduce any bailout costs. Plus, the GSEs will be hugely profitable in the future, so the government should make money on the deal in taxes and pure return.

Down the road, in perhaps ten years, the government should evaluate the need for the GSEs and consider total privatization. Of course, as we’ve seen, we can’t let Wall Street run things without significant regulatory restrictions and oversight, or they just maximize short-term bonus-driven goals and leave the US economy reeling. In fact, Wall Street’s excesses, which were caused in part by the anti-regulatory fervor of laissez faire free market ideologues, have materially contributed to the losses at the GSEs. Now they want to punish the GSEs, who they also required to make risky loans to expand homeownership.

Over time, the government should also evaluate other aspects of its arguably excessive bias toward subsidizing home ownership, which has the perverse effect of making housing unaffordable.

Here’s my solution solution to the GSE problems-

The government buys a huge package of non-performing loans from the GSE’s (out of their portfolios or out of MBS pools that they guaranteed)- and sets up a new Home Owners’ Loan Corporation to restructure the loans to keep as many people as possible in their homes. (FDR’s HOLC ended up owning 20% of the nation’s mortgages) By combining a Continental Illinois style rescue package with a New Deal program it should be an easy sell politically….

“My recommendation would therefore be for a managed bailout in which the stockholders, creditors and taxpayers jointly share the bill.”

I doubt we can all fit in the Russian or Chinese

embassies to work this out…could the DC Nationals

offer their stadium ?

Prof. Hamilton —

Does it really make sense to compare the “total book of business” to the national debt? The debt is an actual liability; the “book of business” is the total amount of insured bonds, right?

For an insurance company, we do not consider the total theoretical exposure as a liability. I mean, imagine adding up the value of all of the property insured by (say) State Farm… If we counted that as a liability, every insurer in history would be insolvent.

This is certainly a big problem, but I do not think it is helpful to anyone to focus on numbers that make it look even larger than it is. Or am I confused?

James:

You say that “The overriding concern in dealing with the current mess is that the process of rapid and radical deleveraging would so impede the flow of new credit that the housing price declines, foreclosures, and bankruptcies significantly overshoot the values that we’d expect in a properly functioning credit market.”

What, pray tell, is the appropriate value of housing? A historic analysis of price/rent, case shiller, etc. shows that housing still has about 30%-50% to fall before it turns to historic norms. Given the glut of housing due to overbuilding in the past 7 years, one might expect the new appropriate price to be lower than historic norms as the increase in supply is larger than the increase in demand.

We are nowhere near the historic level, or the sub-historic level that the market would dictate. By working to keep prices above their historic norms, you’re working to keep pricing unaffordable. Why?

If a property insurer was fundamentally confused about the risk profile of what they were insuring, they could become insolvent and go out of business. If the incidence rate of major home fires was comparable to the current rates of foreclosure (and the price to replace was that much different in percentage than the coverage value) then the property insurers would be going bankrupt. The difference is that the property insurers’ assumptions that the rate couldn’t be that high were correct while the mortgage insurers’ assumptions about foreclosure rates and home prices were wrong. That’s the core of the problem. Lots and lots of people put on suits and got paid for their expertise but they didn’t actually understand the risk conditions of their business.

On July 11, Freddie Mac made an announcement (or threat, if you prefer) that their 10 Billion per month runoff in the retained portfolio would free up $250 million per month if not reinvested. The same, roughly, could be said of Fannie Mae. So, by doing nothing, they free up capita at $500 MM per month. Problem – who buys the newly originated conforming loans?? Answer – create a shiny new clean GSE with explicit guarantee to write the new business, with a sunset provision.

10 minutes ago on the NYT:

http://www.nytimes.com/2008/07/14/washington/14fannieweb.html?_r=1&hp&oref=slogin

The Treasury announcement seems to me to not go nearly far enough — see the Treasury website for so-called “details”. Apparently the instant market reaction (stock futures and USD/Yen) is positive, but I’m not sure we’ll know anything until about 10:30 am tomorrow. For the FRE debt auction ends at 9:45 am and the first hour of stock market trading will be sorting and sifting and thinking the issues through.

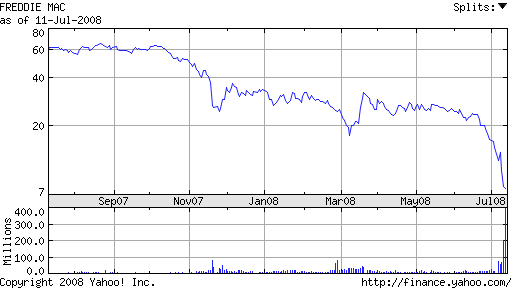

On the odd panicky reaction of FRE and FNM stock last week, here’s the way I’d think about it: because both GSE’s are wildly leveraged there’s little room to take hits from rising bad debt problems. On an honest mark-to-mark it basis (which both companies report), FRE’s liabilities are about as large as its assets, leaving a net worth of approximately zero, and FNM is in not much better shape. That’s using current values of the housing stock, and futures are predicting a steady decline in home prices for the next 12-18 months. So essentially neither company has meaningful equity value on a current basis, and looking ahead for 3-4 quarters all you can see is worsening losses and erosion of net worth meaningfully into negative territory.

Note that normal companies in such a fix would be shrinking their balance sheets as fast as possible, cutting dividends to zero and raising equity.

In this case, the government has been encouraging FNM and FRE to expand their balance sheets as fast as possible even as their net worth has shrunk.

In my opinion, the stock market collapse of both company’s shares last week was the market saying, “enough of this financial madness, already, we’re not going to accept the charade that these companies are ‘well-capitalized’ when in fact they are not”.

Stay tuned — market verdict around 10:30 am to noon on Monday (EDT).

So, in essence, you’re just telling young people to bend over. The property bubble has been a massive transfer of wealth to the baby-boomers, and now the Federal government is stepping in with future tax payers’ dollars to make sure that the transfer sticks.

Fannie Mae is one of the Ponzi schemes created during the FDR New Deal, 1938. Nearly all of those in the FDR “brain trust” were not smart enough to understand that the success that they reasoned would come from such agencies was actually based on the pyramid. Since the Great, Depression Fannie Mae has been expanding because, as with any Ponzi scheme, expansion is the only way to remain solvent.

There is a phrase that is often used with Fannie Mae and Freddie Mac, They are too big to fail, but there is an underlying assumption built into this phrase. The assumption is that the government is bigger. What happens when these entities grow to where they rival the federal government in size? What will the government do? Right now they can throw cash at the problem (can you say inflation) and keep the Ponzi scheme alive for a little longer, but that does not solve the problem. Fannie Mae and Freddie Mac will return as an even more difficult problem and this will continue until they either fail or the federal government admits its mistake and puts them out of our misery.

But the too big to fail problem is very serious. The correction will be nearly as painful as enduring all of the other failures of the central planning fiasco called the New Deal.

When I look at the balance sheets of these 2 organizations I see nothing related to off balance sheet potential liabilities. Since they have guaranteed these mortgage pools why isn’t there some liability like a one percent failure rate on these pools on freddie or fannie’s balance sheet. They have the liability but no balance sheet reference. The government claims that they are well capitalized is true if one does not consider these guarantees but they are insolvent if some of these pools go bad. Any explanation would be appreciaited????

Can’t Say They Were’nt Warned

I guess we take another step toward nationalizing the secondary mortgage market this morning. Only Congress would vote to expand the scope and authority of an entity the same quarter it votes to bail it out. Everyday Economist links to…

This has all the earmarks of a panicked last minute rescue, mostly on the taxpayers, rather than a thoughtful rescue that spreads things around as you suggest.

your Roubini estimate of $2-300 billion is outdated, he has upped it. In my view the $5 trillion assets might actually be worth roughly $4.5 trillion, or maybe $4 trillion if house prices keep going down. thats a half trillion to 1 trillion loss, dwarfing the 80s S&L crisis for example

Guests question above is the right one. Think of Fannie/Freddie as $ trillion SuperSIVs with no capital and bad assets, AND mortgage pool insurers with no reserves.

By no capital, I mean about 1 1/2% against $1.6 trillion of unmarked mortgage assets on their books. By insurers with no reserves I also cant find reserves of more than 0.1% on their balance sheets. They have been taking the insurance premiums, $ 7 bio/yr? and using them as hand to mouth earnings, rather than putting 50% or more aside as a respectable insurer would.

Fannie/Freddie paper and insurance will need to be guaranteed. I suggest only with fees and haircuts. One proposal is to sell puts in the paper, think of that as another insurance premium. Make it out of the money or, in insurance terms, a holder deduction first.

This bailout of Freddie and Fannie counterproductive. Another congressional initiative, the Mortgage Bailout, will tax Freddie and Fannie to the tune of $530 million/ YEAR. So Congress wants to bail out an institution and tax it as well? Whats going on? Call your senators/representatives and tell them: Back off the Mortgage Bailout Bill and Back off Bailing out Fannie and Freddie Mac!

http://www.freedomworks.org/newsroom/press_template.php?press_id=2585

Blue Dog House Contact info:

1-866-887-5841

http://www.freedomworks.org/newsroom/press_template.php?press_id=2580

Bankrupt – A person, firm, or corporation that has been declared insolvent.

Bankruptcy – The condition of being unable to pay debts.

Recent Ufo Report: Unapproachable Financial Obligation.

Interesting that the government would bail out Fannie and Freddie but are not interested in bailing out Social Security. The beneficiaries of the bailout include foreign debt holders, pension funds etc. The losers are the American taxpayer and the USD…. let free markets run their course, if Fannie and Freddie are not profitable busineses, let them go broke. This is the way free enterprise is supposed to work.

I question whether the U.S. needs outfits like Fannie Mae and Freddie Mac. Why is it necessary for the government to make such an issue of house ownership?

Seems to me that many people–especially low income people–would be better off renting so they’d be more mobile and could relocate for higher paying jobs.

The American obsession with house ownership is ridiculous and the last few frenzied years of rising prices along with dishonest borrowers and incompetent lenders has finally blown up.

Maybe it would be best to wind down the mortgage intermediaries and let lenders deal with borrowers on a basis that makes sense.

Both Freddie and Fannie are in good shape. Both have sufficient liquidity. This is much ado about nothing. The price declines in their respective stocks is the underlying reason for all the attention. But the naked short sellers have had their day (today). And now that Paulson has floated this ridiculous (politically expedient) plan, I should think that Freddie and Fannie Bonds will be quickly snapped up (as most now believe that the bonds are “no-brainers” now that the Federal Government – under Paulson’s plan – would back both Freddie and Fannie).

I agree with “Josh Stern”, the stock price is irrelevant – yet the stock price gets the publicity. Once the short sellers move elsewhere and both Freddie and Fannie make nice price recoveries – the media will have to generate another “crisis” somewhere else.

This is the opinion of Robert Sheridan, CEO of Sheridan & Partners, a Chicago real estate & development company. Their site is http://www.sheridanpartners.com/market.php

Not All Financial Woes Are Created Equal

The failure of Indymac Bank according to The New York Times the largest lender to fail in more than two decades can be laid squarely at the feet of the lax (or nearly non-existent) underwriting that is part of (a big part of) the sub-prime mess. The chickens simply came home to roost.

The troubles of Fannie Mae and Freddie Mac are quite different. Freddie and Fannie underwrote loans carefully; their difficulties are a result of the unprecedented decline of home values.

In 2006, going against the conventional wisdom that single-family home prices never decline (they might stop rising for awhile, but they never decline), we predicted that single-family prices could decrease 10 to 20 percent. Painfully, that forecast turned out to be very correct but also optimistic. Were in a cycle now in which housing declines already are greater than at any time since the Great Depression of the 30s. And were not at the bottom yet.

If you dont want to be disappointed by housing performance in the near term, disregard forecasts that the bottom is just around the corner unless that corner is in Timbuktu. The bottom is NOT coming soon. And when it does arrive, it will not be obvious, like the bottom in the chart of the DJIA. The housing bottom will become apparent only in the rear-view mirror, when you realize that prices have stopped falling. Dont expect a sharp rebound.

We will stay at the bottom for quite a while. How long that lasts will vary, as always, market-by-market.

First we fire all the incompetent and corrupt Bush appointees, regulators and executives responsible for this mess and fine them into bankruptcy.

Great post. I agree that all three parties — shareholders, creditors and tax-payers — should bear the cost.

If the assets turn out to be insufficient to cover liabilities, shareholders should be the first one’s to be wiped out. No need for any pity-payment, like the Bear Stearns $10/share; what was that all about?

Creditors should be the next ones hit. I don’t think the government should bear the first slice of any shortfall. One can haggle over the amount. I would think that the government should not intervene until creditors are looking at 90% or less.

The only reason the tax-payer may legitimately be on the hook is because of the whole “government sponsored” nature of these entities, with a declaration of non-support coupled with a wink-wink, nudge-nudge notion that the government would look out for them after all. I think we can assume that a whole lot of tax-payers have got slightly cheaper mortgages as a result, and it’s time to pay the piper.

What I think is really important is to to make the government support absolutely clear. make a clear statement at what level the tax-payer will start to share losses, and at what level the tax-payer will guarantee against losses. An example would be:

* First losses to shareholders

* Next 10% borne by creditors

* Next 20% borne 50% by creditors and 50% by tax-payers

* Bottom 70% borne by tax-payers

Also, this should apply to existing commitments only. At the most, for another quarter or two of new commitments. These agencies should be put into a run-off mode, and whittled down, with the private sector stepping in.

Perhaps this might mean rates go up by 1%. Well, if that’s the real cost that the market sets, then that is what it is. Fooling ourselves by creating a fuzzy-cloud organization that has to be bailed out later, is simply a form of governmental wealth redistribution.

That’s what *ought* to happen. OTOH, it is an election year, so we should probably expect worse. Already, the agencies have taken a larger step into the Jumbo market. It’s reasonable to expect that the government — current and new-in-2009 — will make more guarantees than required.

So, we should expect that the previously informal arrangement will be formalized even more, and the moral hazard will be stepped up a notch or two.