Bitcoin is a digital currency for which no government, bank, or corporation takes responsibility. Like many others, I was curious to learn how it works and why it seems to be succeeding.

Instead of having a sum (in dollars) in an account with a bank, you could have a sum (in Bitcoins) that you hold in an account that is kept track of by a network of individuals with a public record of where all the sums reside. The mechanics of being able to transfer an entry from one Bitcoin account to another are based on advances in cryptology that use open-architecture algorithms to convert one string of data into another. You can see one in operation here. You enter one string of characters, and out comes another string. Although the formulas by which the output is calculated are totally open and public, it is essentially infeasible to do the operation in reverse. If you only know the string that came out as a result of the operations, about the only way you can guess what went in is by trying every possible input string, a very time-consuming process even for the fastest computers. On the other hand, if you tell me the input you used and I already know the output, I can readily verify whether the input string was indeed as you reported.

The output of a Bitcoin transaction is based on combining some private code associated with your holdings, which only you know, with the full history of previous transactions, which everyone knows. If you supply the correct private code, other users can verify that you indeed were the owner of that sum because your code together with the public history correctly solves a known math problem. In this way, your participation is required to transfer your sum to a new owner, with security of the system maintained by the difficulty of anyone simply guessing the code.

OK, so let’s grant for the time being that the technology exists for you to securely order the transfer of some of your Bitcoin holdings to somebody else without any government or bank needing to be involved. Why does the stuff have value in the first place? The answer is that it would be very helpful to many buyers and sellers of real goods and services if they were able to pay for transactions in this way. We can think of any form of money as an asset that provides liquidity services, which refers to the tangible benefit to its holder coming from the ability of the asset to facilitate certain transactions. The value of money, that is, the value of real stuff you’d be willing to give up to hold money, can be thought of as the present value of the stream of these future liquidity services.

Bitcoin has two potential advantages over credit cards for providing such liquidity services. First, the supporting network only needs to verify that the private code is valid, which is less costly than verifying that you are indeed the rightful owner of a credit card and are ultimately going to deliver good funds. With a conventional credit card, the merchant needs to pay the card company a significant fee for the transaction which in an economic sense results from that high cost of verifying everybody’s compliance. That’s why many merchants are embracing Bitcoin. Your Bitcoin gets deposited into the account of a third party that the merchant specifies. That third party then gives the merchant dollars, confident they will be able to get dollars in turn from somebody else who will want the Bitcoins to pay for some other transaction.

Second, Bitcoins are relatively more anonymous than credit cards. In this respect, they enjoy some of the same advantages as cash. It’s striking that of the $1.2 trillion currency in circulation, three-quarters is held in the form of $100 bills, which many of us never carry. The use of Bitcoin for illicit transactions may have been part of what helped it initially develop into something that had a dollar value. But people like Charlie Shrem can tell you the internet isn’t nearly as anonymous as it seems. Marc Andreessen explains:

Much like email, which is quite traceable, Bitcoin is pseudonymous, not anonymous. Further, every transaction in the Bitcoin network is tracked and logged forever in the Bitcoin blockchain, or permanent record, available for all to see. As a result, Bitcoin is considerably easier for law enforcement to trace than cash, gold or diamonds.

Yet another group helping to establish Bitcoin’s value are people who have an ideological passion for a system of exchange that is independent of any government or bank, perhaps some of the same individuals who want to hold their wealth in the form of gold, despite the volatile value of both. And like gold, the fact that Bitcoin has been appreciating in value relative to the U.S. dollar brings in some who assume the trend has to continue. Much of the current value of a Bitcoin, just like much of the current value of an ounce of gold, could well turn out to be a speculative bubble.

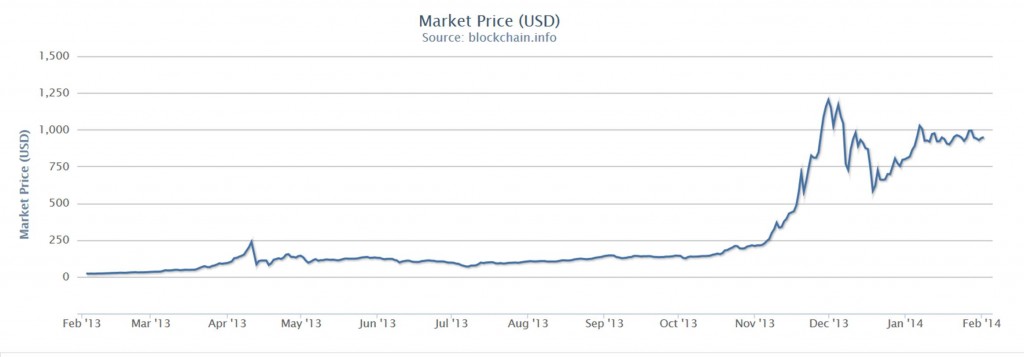

At a current price of $944 per Bitcoin and 12.3 million Bitcoins in circulation that gives a total market value of $11.7 B. That’s a little more than the $10.3 B worth of U.S. one-dollar bills that were in circulation as of the end of 2012.

Will it keep up? The value of the liquidity services that something like Bitcoin could provide is certainly quite tangible. Bitcoin’s functionality relies on the security of the underlying cryptology, and I am no one to judge whether better algorithms might develop for hacking the code or usurping the network on which the system depends. Another detail I am unclear about is whether a peer-to-peer network can continue to be relied on to provide verification to merchants at minimal cost. Currently the system creates new Bitcoins that are credited to entities on the network who successfully solve sets of new verification problems, giving individuals an incentive to maintain and update the system of accounts as well as ensure that the number of Bitcoins grows at a fixed rate over time. But the system is set up so that the maximum number of Bitcoins could not exceed 21 million, a ceiling that we are already more than halfway toward. Could a variant of the system continue to survive after we reach peak Bitcoin?

Hard to know where this is all going to lead. But one thing is clear– we have added a very interesting new chapter in the history of money.

I think there is also the question of how things are affected by the existence and adoption of other cryptocurrencies. While bitcoin supporters can probably find reasons to label the alternative cryptocurrencies (aka altcoins, e.g., litecoin, peercoin) as inferior, it may not remain that way. This may have an effect on the speculative value of bitcoin (and speculation very much plays a role in the price dynamics of bitcoin). For all we know, bitcoin could be the Friendster of cyrptocurrencies.

Nylund: I thought the same thing about Amazon years ago. What I’ve learned is that there can be a huge first-mover advantage in these network/reputation equilbria. And $10 B is a pretty big first move.

Amazon has large economies of scale in its operations (warehouses and delivery). I have no idea if Bitcoin has something similar, but a simple appeal to Amazon is not immediately convincing.

Bitcoin isn’t friendster or facebook, but rather it’s more like TCP/IP. It is the protocol upon which those sites operate.

At the moment, there are more than a few protocols, but bitcoin has a huge head start, and as things move forward it will most likely become entrenched to the point that no alternative is necessary or desired.

After all, we only have ONE internet; that’s the whole point of THE internet. Bitcoin will most likely serve as the backbone of other types of applications that will be built on top of it.

It’s the layers above where all the cool stuff is going to be happening over the next few years. Bitcoin is just the foundation, a slab of concrete.

i think i prefer beanie babies and cabbage patch dolls

The obstacle to bitcoin becoming a mainstream payment medium is that it involves exchange rate costs and risks that may not be economically more attractive than debit cards to non-enthusiasts.

For an ordinary person with dollar income to pay with bitcoin, there are five cost factors

1 the cost of transmitting dollars to the bitcoin exchange (often by traditional payment card)

2 the cost of converting dollars into bitcoin (transaction fee and/or market spread)

3 the cost of converting bitcoin into dollars (transaction fee and/or market spread)

4 the risk that bitcoin’s dollar value will fall in the meantime

For merchants, accepting bitcoin could be a very good deal, especially if they don’t have to pay any of cost factor 3 (I don’t know how it works, personally). But for consumers this is a terrible bargain compared to debit and credit cards, where all costs are born by the merchant, who are even overcharged so that a small portion can be kicked back to the consumer. Hence bitcoin adoption relies on a small hard core of enthusiasts who are usually also investing in bitcoins.

I don’t really see how bitcoin payments can go further. If, say, banks got into the business, offering to convert dollars to bitcoins and transmit them to a bitcoin payment service provider on behalf of bank clients at the moment of a purchase, cost factor 1 could be eliminated, but the remaining costs would made transparent and I think customers would be quickly disillusioned.

Oops, four cost factors (I consolidated two and forgot to edit, sorry).

One potential problem with bitcoin is that it is inherently deflationary. There is a hard limit on the number of bitcoins (21 million), regardless of growth of the economy, and also occasionally some bitcoins are lost. This means that the real value of bitcoins should increase. This could lead to a deflationary spiral in which bitcoin speculators withdraw coins from circulation in anticipation of further appreciation. There is the potential for a speculative bubble which reduces liquidity since no one wants to trade a currency that might increase in value tomorrow.

A second problem with bitcoin relates to the supposed low transaction fees. The problem is that only a small subset of items can be purchased with bitcoin. You can’t pay your rent with bitcoin and you can’t pay taxes with bitcoin. Eventually you need government currency and the exchange rates between bitcoin and government currency is quite expensive. So, for example, for an American to purchase an item from an Australian, you first have to pay a 3% exchange fee to convert U.S. dollars to bitcoin and then the merchant on the other end has to pay a 3% fee to convert bitcoin to AU dollars. The round trip cost is higher than just using a credit card.

Exchange fees are closer to 0.5%. And someday, bitcoin users may not need to exchange into fiat to buy groceries or pay rent.

Until your landlord or your grocery store accept bitcoins

I guess any medium of exchange beyond straight barter requires some leap of faith. Gold was given value because of it’s scarcity [at one time] and because it could be fashioned into pretty baubles. Same for diamonds. Beyond that, you had to have faith that a bank, city, state, or government was going to be able to back up their coins or currency in some way that wasn’t harmfully inflationary [printing more currency without any conceivable foundation]. Credit cards introduced middlemen, but not new currencies. Bitcoins seem to break the paradigm by being created by ??? and managed by ??? and having a value of ???.

Lot’s of questions, but the answers aren’t that satisfying.

FYI, transaction fees goes to the miners, and is what will keep the system running when the last coins are mined.

Why did Shiller say Bitcoin is a bubble? I could not find his reasoning but he said he is certain that bitcoin is a bubble. Any idea?

Here is one of many links: http://rt.com/business/bitcoin-shiller-bubble-davos-127/

Natanael makes an important point. After the 21 million limit to bitcoins is reached, bitcoin transactions will incur a small fee, to pay the people who ensure the integrity of the system (called “miners” because they’re currently paid in newly created bitcoins, until that 21 million is reached). Those future transaction fees will be on top of the four cost factors I mentioned. You could say there’s a current equivalent cost in the form of downward pressure on bitcoin value from “mining” issuance.

PA misses the point. Even if landlords and grocers accepted bitcoin, they would still be converting to dollars. The conversion cost could be paid by consumers through a commission or spread, or swallowed by merchants and passed on to all consumers through higher dollar prices. Unless you’re imagining a world where bitcoin replaces dollars, the conversion costs and exchange rate risk will still be there born at least partly by the consumer, and it’s very unlikely bitcoin payment will be competitive with debit cards.

The enthusiast hard core is willing to bear conversion costs and FX risk mainly because they are bitcoin investors, and they believe capital gains on bitcoin will usually compensate. So far that has worked – in other words, the fx risk has been a good bet. Continuing that depends on constantly recruiting more enthusiast-investors. Once that pool stops growing, the fx risk will be balanced at best and the underlying costs will be apparent and annoying.

It is an interesting study in deflation that one Bitcoin could buy one blazer in April of 2013. Today one Bitcoin can buy 5 blazers. Should those users of Bitcoin be pounding their chests because of the huge deflation in Bitcoin? The truth of inflation and deflation becomes much clearer if you consider that Bitcoin has become more valuable (as it should) as it has deflated and its use in international trade has increased. Bitcoin should make all of the “monetary experts” question their theories.

Bitcoin is very volatile, and you can’t get a credit card. So to use it I have to maintain a store of a volatile collectible that has only a virtual existence so offers none of the potential utility or alternate uses of gold or diamonds (the latter backed by a cartel that tries to preserve value, because small gem-quality diamonds aren’t that scarce).

Credit cards allow us to delink our cash balances and our current consumption. Even if for reasons that aren’t apparent the value of bitcoin were to stabilize, the purported transaction advantages are a function of its use by generally well-heeled individuals who have needs different from mere academics, much less the hoi polloi whose average income is even lower and cash flow constraints likely binding. Likewise, without the existence of bank credit markets in bitcoins, there’s no way to use it for standard commercial purposes.

So once the fad fades, well, the equilibrium price of bitcoin is zero. Better to buy beanie babies – your kids or grandkids can at least play with them. In the end they too failed to hold their value as a trendy collectible with exchange markets (eBay). But they still do have an intrinsic value.

“Why does the stuff have value in the first place?” Because people are losing faith in fiat money.

“The value of money, that is, the value of real stuff you’d be willing to give up to hold money …” This is a backward way of looking at things. Ordinary people do not think this way. I have no immediate objection to the second part of the sentence, however: “ … the present value of the stream of these future liquidity services.”

This takes us to money being a store of value. This function of money has two parts. The one is the predominant common function – money being a medium of exchange. Time is always involved here. You must have the cash money from a previous time period (no matter how short) to consummate the exchange. The second aspect of store of value is conceptually more complex. That’s because it inherently involves uncertainty. Suppose you knew with certainty the entire future of exchange transactions you were going to engage in. If your flow of receipts (income) exactly matched the sequence of all future exchanges, there would be no reason to store value for the purpose of these exchanges. However, in general in the real world the flow will be lumpy. Hence a need for store of value even if the future were certain. I do not know what to call this, but it is conceptually separable.

That leaves the uncertainty aspect of store of value. A bargain can appear at any moment out of the clear blue, as well as an unanticipated need. For this, we would want to hold money. For speculative and precautionary reasons. I have not yet admitted credit to this world. Let me now do so. Still, the only reasons to hold money would be for (a) the lumpiness of exchange and (b) the opportunity and unanticipated needs reasons. Here enters the possibility of debt default. There’d be no reason to protect against debt default, if you had no debt. As for individuals who do have debt, by definition they are not holding that portion of their assets in money. So the demand for money as a store of value is seemingly diminished. Yet, another new aspect of money demand arises in the process. For the precaution debtors must take. The net of these two – the diminution of money demand as value flows from cash to collateral, and the new precautionary demand debtors must have because they now have the possibility of a liquidity crisis – will on net reduce the money demand of debtors. However this is not the whole story, since non-debtors’ demand for money may now be affected by the existence of debt. And will be at the point when these creditors perceive a credit bubble is underway. Time to prepare a tarp of speculative balances to catch the soon ripening and falling fruit.

Is any of this a reason for bitcoin to exist? Said another way, does bitcoin provide some value over and above these core reasons people have for holding ordinary money? From what’s indicated in the post, anonymity would not be a reason. Perhaps the miniscule transaction time it takes to acquire ordinary money (going to the bank or ATM) might be lessened. But (I judge) this time-saving hardly has much relative value. Perhaps it is safer to keep money in this digital form rather than risk theft of cash. But that’s debatable as digital theft is also possible. Furthermore, the current level of acceptability of bitcoin for transactions militates against it. Something has to drive the acceptability of bitcoin to a critical mass where it is roughly as acceptable for transactions and store of value as ordinary money. This something is the crux. Which takes us full circle back to the first paragraph – loss of faith in government fiat money. This in turn raises a question: Why would a government ever give up the monopoly it has on its fiat money to another fiat money like bitcoin?

Parenthetical note. A core assumption of the model developed in the Santos paper is: “There exists but a single consumption good at all times … .” Given that the primary function of money is as a medium of exchange, how realistic is that? Why would you even need money in such a world?

The money supply doesn’t increase at a fixed rate . While I can’t claim to understand the Bitcon mining procedure, the wikipedia page states: “The total supply is capped at 21 million, and every few years or so the creation rate is halved. This means new bitcoins will continue to be released for more than a hundred years.”.

Every time a Bitcoin is mined it becomes harder to discover the next one! Thus it is increasingly hard to min profitably as your profit is more than eaten up by the power consumption required to mine. This is why some malware is trying to install Bitcoin mining software on your computer – you pick up the electricity bill, they get the profit!

Have You noticed that behavior of bitcoin is on 45 times shorter time scale copying that of gold over centuries (in USD since USD inception)? So it acts like a kind of ew gold relative to USD, but with much shorter life span.

How would You explain current stability of bitcoin price? It should have dropped by now more if that was a mere bubble, 1200 USD price. Its obviously not a speculative bubble only. There is some other value in it that has been recognized by market and valued at 900+-15% USD.

JDH,

Some comments on a very interesting topic.

“Bitcoin has two potential advantages over credit cards for providing such liquidity services. First, the supporting network only needs to verify that the private code is valid, which is less costly than verifying that you are indeed the rightful owner of a credit card and are ultimately going to deliver good funds. With a conventional credit card, the merchant needs to pay the card company a significant fee for the transaction which in an economic sense results from that high cost of verifying everybody’s compliance.”

At this point, transactions costs may be obscured by the seniorage that bitcoin miners earn to verify transactions in the system. Every proposed transaction contains a transaction fee, which bitcoin miners earn if they successfully verify the transaction block (more about that in a minute.) But the system is also set up so that if a bitcoin miner verifies a transaction block, the miner receives the transaction fees for all transactions as well as seniorage. This is how the money supply grows. For the first 210,000 blocks, miners receive 50 bitcoins for each block verified and the money supply grows 50 bitcoins every time that happens. For the next 210,000 blocks verified, miners receive 25 bitcoins for each block verified and the money supply grows 25 bitcoins per block. 25 bitcoins is the current seniorage rate, which halves after the next 210,000 blocks have been verified. So, right now transactions fees can be relatively low, but as time goes on they will have to comprise a bigger percentage of the overall payment to bitcoin miners. Still, when you consider how the system is set up, it’s not hard to see that transactions fees should be much lower than in more conventional payments schemes. It’s just too easy to set it up. For example, in Tokyo “The Pink Cow,” which is a tex-mex restaurant in Roppongi, has set up a bitcoin payment system. They just have an ipad that displays a barcode that you can photograph with a smartphone and then pay with bitcoins. All the complex and expensive payment methods have been bypassed.

“Second, Bitcoins are relatively more anonymous than credit cards. In this respect, they enjoy some of the same advantages as cash.”

I’d say not really on this point. Bitcoin is pseudonymus, since the identity of the owner of bitcoins is established using public-private key cryptography, and a public key may be linked to a pseudonym. But there are a couple of points to consider. First, national authorities are requiring the bitcoin exchanges to collect personal data from people who purchase bitcoins. And, unlike cash, the bitcoin block chain contains a complete record of every bitcoin transaction from the genesis block. Thus, every time bitcoins change hands, there is a complete record. That’s one reason that many privacy advocates aren’t happy with bitcoin. Cash doesn’t remember who spent it.

“Bitcoin’s functionality relies on the security of the underlying cryptology”

Yes, ultimately it does depend on the security of public-private key cryptography, as does all modern cryptography. But the security depends also on the incentives that are built into the system. How does the system prevent someone from double spending bitcoins? How does the system prevent someone from counterfeiting bitcoins? It all depends on the incentives provided to the bitcoin miners, whose role is to verify transactions. If a miner wants to verify a block and thus earn fees plus seniorage, his compute node must successfully solve a “proof of work” problem, which requires computational expenditure. When a proposed block is being verified, all miners are attempting to solve the proof of work problem. The first to do so verifies the block and inserts the block into the block chain. One rule of the bitcoin protocol is that the block chain the system will accept is the one that has the most proof of work associated with it cumulatively from the genesis block. Now consider a counterfeiter. A counterfeiter would have fork the current block and insert a block with some false transactions. However, in order to do that, the counterfeiter will have to solve proof of work problems. Meanwhile, the other miners are working on other blocks and inserting them into the current block chain. As long as the counterfeiter is small, his computational power will be overwhelmed by the collective compute power of the other miners and he’ll never catch up and be able to insert his false block as legitimate. And, if he does possess enough computational power, the idea is that the transaction fees and seniorage will be a more efficient use of computational resources than the rewards to cheating or counterfeiting. So, you need most miners to be honest or for the incentives to work if they aren’t.

Will this really be true? What if miners collude? There are a number of interesting economic incentive questions here.

“giving individuals an incentive to maintain and update the system of accounts as well as ensure that the number of Bitcoins grows at a fixed rate over time. ”

Bitcoins do not grow at a fixed rate over time. Let me comment more on how the money supply process works. As I mentioned, bitcoin miners serve as decentralized central banks in that they earn bitcoins for verifying transaction blocks, which increases the money supply. This process is very tightly controlled in the bitcoin system. Each bitcoin miner must solve a proof of work problem to verify a block. Here’s how it works in more detail. For each block the system proposes a challenge string. A solution is another string such that when the solution string and challenge string are put through a crypto hash function, a certain number of the leading elements of the resulting string are zeros. Since the hash function is strongly one way, there is no way to solve this other than by trial and error. But, this process results in a probability distribution that governs the chance that any particular miner will solve the problem. It’s set up so that on average it takes about 10 minutes to solve a proof of work problem and those solutions are necessarily distributed randomly among the miners. The system self adjusts the difficulty of the proof of work problems so that 2016 blocks are verified in 2 weeks time. In 4 years about 210,000 blocks are verified then. During the first 4 years, the seniorage paid to miners is 50 bitcoins per block, and so the money supply will increase by 210,000 X 50 = 10.5 million bitcoins. During the second 4 year period, the money supply will increase by 210,000 X 25 = 5.25 million bitcoins. During the third 4 year period, the money supply increases by 210,000 X 12.5 bitcoins = 2.625 million. That process continues, with the seniorage payment halving every 4 years. It will finally stop when bitcoins can’t be earned any more. The smallest unit of account is the “satoshi,” which is one 100 millionth of a bitcoin. So, if you follow that process, the money supply process will stop in a little over 130 years from now with a maximum number of bitcoins of 21 million.

The interesting thing about this money supply process is that while the reward to creating bitcoins keeps cutting in half, so does the additional number of bitcoins. So the reward goes down as most of the bitcoin that is going to be created has already been created. The money supply process will continue as long as fees are sufficient for miners to keep verifying transaction blocks.

This is certainly a rule-based monetary policy but not the rule that John Taylor wants followed.

Sorry, I meant to say that the whole money supply process would take a little over 130 years to complete starting from inception, 2009, not from today. So, the system would reach 21 million bitcoins around 2140. In 20 years from 2009, however, most bitcoins would have been created, about 20.3 million by that point. Once that threshold is reached at the 20 year mark, the payment for mining bitcoins would then be 1.56 bitcoins per block over the following 4 years, which would yield an additional 328K bitcoins added to the money supply by 24 years out.

I think that there is also one important issue. What happens if some big goverment, for example US, will make BC illegal? It can be a big shoch for this industry. The story was when US made internet poker illegal.

Warren Coats has a fairly detailed recent blog post (1/25/2014) on Bitcoin and why he doesn’t think it will be truly “money”. Covers some of the same ground but more details on the liquidity and peer-to-peer verification aspects. This was linked to by another blog, but I can’t remember which one for a HT.

http://wcoats.wordpress.com/2014/01/25/cryptocurrencies-the-bitcoin-phenomena/

Update: HT to Free Banking.

http://www.freebanking.org/2014/01/26/warren-coats-on-bitcoin/

Please don’t quote the price of Magic the Gathering Online eXchange (aka MtGox). It is a dying web site from which you can no longer get bitcoins nor dollars.