Here I offer some thoughts on last week’s numbers for employment, auto sales, and commodity prices.

On Friday the Bureau of Labor Statistics reported that 20,000 fewer Americans were working in January compared with December on a seasonally adjusted basis but that the unemployment rate nevertheless fell from 10.0% in December to 9.7% in January. The discrepancy comes from the fact that the BLS gets employment counts in two different ways. The first is by asking establishments how many people they employed last month, and this establishment survey provides the basis for the reported 20,000 decline in nonfarm payrolls. But a second method is to go to individual residential addresses and ask the occupants how many people living there were working last month. According to the BLS household survey, the number of Americans working increased by a seasonally adjusted 541,000 workers in January over December, though updated population controls make that December-to-January comparison for the household survey problematic. Usually what we hear featured in the press are employment numbers coming from the establishment survey and an unemployment rate coming from the household survey. The wildly diverging fundamental numbers for employment itself in the two surveys account for the reported improvement in the unemployment rate coinciding with no progress yet on jobs. Mark Thoma, Phil Izzo, and of course Bill McBride

([1],

[2])

survey the takes of various analysts on what to make of the conflicting numbers.

Normally the establishment survey is regarded as the more reliable, though Tim Kane has argued that the household survey sometimes does a better job of recognizing turning points. We might look to some other labor market indicators to try to referee the current dispute. Automatic Data Processing constructs its own estimate based on the 22 million Americans whose payrolls it helps prepare, and their guess was that the economy shed 22,000 private sector jobs in January on a seasonally adjusted basis. Since BLS estimates that 8,000 government jobs were lost in January, ADP’s estimate is about 10,000 more pessimistic than the BLS payroll figure. The Institute for Supply Management’s survey of nonmanufacturing establishments found more managers reporting declines in employment than reported increases in employment in January. By contrast, their survey of manufacturing establishments found more managers reporting increases in employment than declines. Fair to say that the signals are mixed, but things may not be as bad as the BLS nonfarm payroll numbers suggest.

Earlier in the week we received reports on January auto sales that could also be described as no better than lukewarm. Americans purchased 6% more light vehicles last month than they had in January 2009. That might sound encouraging, unless you’ve forgotten that January 2009 was the worst month for car sales out of the last 6 years (on a seasonally unadjusted basis). Last week’s good news was that January 2010 was only the third worst month out of the last 6 years, beating both January and February 2009. Nonetheless, that’s the same basic arithmetic that gives rise to some hope for 2010 reported growth rates– things were so awful last year that even a very bad month counts as an improvement.

|

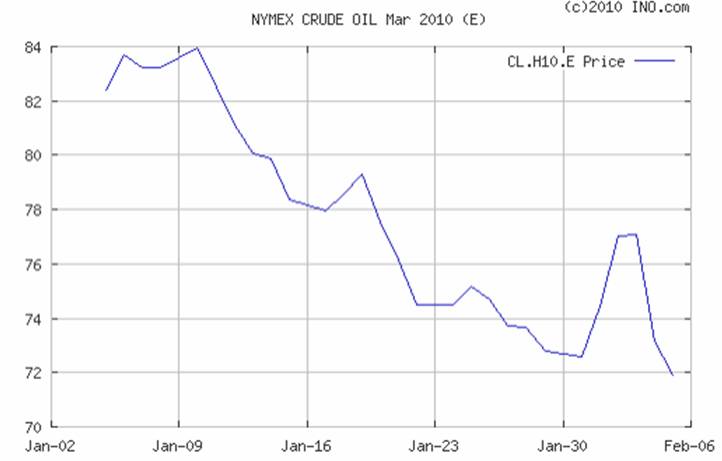

I also continue to follow with interest what’s been happening to commodity prices, with both oil and copper now off 15% from their values of just a few weeks ago. I’m persuaded that speculation in China has been a big part of the story on both the way up and now on the way down. Greg Merrill calls attention to the estimate by the International Copper Study Group that China’s apparent usage of copper grew by 43% in the first 10 months of 2009, while copper usage by the rest of the world fell by 18% over the same period. If stockpiling in China has indeed come to an end, that would explain the sharp fall in prices, and could portend more to come.

|

|

Finally, I have to pass along a story that Mike Shedlock highlighted from Bloomberg:

Non-performing loans in China have risen into the “trillions of renminbi” because of poor lending practices, an insolvency lawyer said.

“We work really closely with SASAC, the state-owned enterprise regulator in China, and there are literally trillions and trillions of renminbi of, frankly, defaulting loans already in China that no one is doing anything about,” Neil McDonald, a Hong Kong-based business restructuring and insolvency partner with Lovells LLP, said at an Asia-Pacific Loan Market Association conference yesterday. “At some point there’s going to be a reckoning for that.”

China’s government is tightening controls, including banks’ reserve ratios, to prevent record lending from fueling inflation. The Shanghai office of the China Banking Regulatory Commission warned yesterday that a 10 percent fall in property values would treble the number of delinquent loans in the city. Liu Mingkang, chairman of the CBRC, said Jan. 4 that loans were channeled into stock and property speculation last year, which China has been taking measures to stop.

My bottom line: the scales tipped last week in the direction of near-term deflationary pressures, despite the strong 2009:Q4 U.S. GDP report and falling unemployment rate.

I have a couple of questions regarding China. Right now there are a lot of concern over China’s asset bubbles. It is also clear that China is a prime driver for the global recovery.

1. Given China’s growth rate is consistently higher than 8% a year, strategically, it seems very logical to stockpile on commodity when the price is relatively low. Why should China hold pieces of US treasury paper can be inflated away instead of holding commodities that it needs for it’s growth? As such, how does one distinguish between speculation vs. strategic stockpiling while the prices are relative low? Granted some stockpiling is not centrally planned but that just proves that market and price works in China too right?

2. China’s current housing bubble is very different in nature than the US sub-prime bubble. In China, there is no sub-prime mortgages.

– All first time home buyers must put down 20% down. For buyers of 2nd home and beyond, they must put down 40% payment.

– The average down payment for home purchase is 50%

– The Chinese are famous for their frugal ways (savings rate is nearly 40%).

– Rental price in China are dirt cheap relative home price.

Over leverage is primary cause of pain during an asset bubble. From data on Chinese home buyers, they are not the one’s taking on excess leverage. Which economic players (the central gov, the local gov, the banks, the developers, and the home buyers) are taking on excessive leverage in China? Also, how/why is the excessive leverage taken on?

3. On the non-performing loans, a trillion of RMB is 140 billion dollar. Assuming a recovery rate of 70%, the lost is about $40 billion dollars. Today, China’s economy is slightly less than 5 trillion dollar. I know the article mentioned multiple trillions of RMB of none performing loan. I just want some reference point to consider the big numbers.

The question is at what point, are there any academic study, that the ratio of none performing loan relative to GDP becomes a problem? How close is China to that danger?

Can the Chinese use the 2 trillion foreign reserve to help directly or indirectly with the excess non-performing loan problem and how?

I heard The Party complain last year that they thought speculators were driving up the price of whatever China was buying, and of course I also heard ,incessantly, that the world should borrow in the ZIRP currency of their choice and buy commodities, especially the ones China likes. So this enigma is solved to my satisfaction.

As far as the China real estate boom, I heard a lot of the bad loans are with developers, who are getting stuck with unsold inventory. The idea was to create jobs, not homeowner and office space owners, remember.

But back to the USofA. In case we think we have left no rock unturned looking for problems, here’s another to play out in parallel with the expected CRE refinance problem, ongoing residential defaults (even higher than last year), a few state insolvencies (CA at the top of the list) and a $1.6 Trillion (and counting) USG deficit…..

tada!…. LBOs are still a $800 Billion problem!!!!!!!

http://www.zerohedge.com/article/lbo-refi-wave-approaches-800-billion-junk-debt-maturing-2014-adds-multi-trillion-fixed-incom

One other thing pushing things toward deflation is the increase concern over deficits, by the market in Europe, and by the electorate here.

Silly Things, buying a commodity because you expect the price to rise is always speculation. It isn’t a big deal that players in China are speculating in copper, per se. But if the apparent recovery in demand for copper, et al., over the last year was due to a large extent to speculation, than the inflationists may have been misreading things and seeing their expectations of inflation providing the justification for their expectations.

You’re correct about the differences between our housing bubble and the bubble in China. But last year net new loans were over $1.5T, and that leverage exists somewhere. That would be equivalent to net new lending here of $5T in one year. It’s really hard to imagine that wouldn’t result in some pretty extreme leverage ratios.

Cedric,

Since the home prices and residential mortgages both sky rocketed in 09 in China, the developers are not getting stuck with unsold inventory with such strong demand. On the other hand, the developers could have started too many building projects last year. Since it typically takes a year or more to build large multi story buildings (typical residential housing in major Chinese cities), there could be a glut of supply coming soon…

I think the question is how much leverage have the developers taking on? I’ve read that the developers themselves are concerned (one can’t help it given all the noise in the media) and view their operation like that of a factory. They wanted to churn out buildings quickly and sell them as fast as possible. They don’t want to hang on to inventory and risk price collapse either. Understandably they also want to keep selling when the customers are still clamoring for their product. Anyway, this all seem quite obvious and reasonable. So the question is, with that kind of mindset, how much leverage have the developer took on?

Here is my take on “$800 Billion In Junk Debt Maturing By 2014” from the zerohedge. The article mentioned these things need to be refi between 2012-2014. In other words, starting 2012, each year about $270 billion needs refi. Let’s make a conservatively estimate that only 70% can be refi, that left $80bn in trouble. Of that let’s say recovery is also 70%. That means the creditor needs to take a hit of $24 billion. Why is that a problem for a 14 trillion dollar economy?

I know zerohedge also mention a multi-trillion fix income refi cliff and yada yada. Media outlet likes to throw up big number for dramatic affect. There is no substance and it is just a cheap shtick to get readers attention. The fact is our economy, never mind the world economy, deals with trillion dollar of xyz year in year out.

Bob_in_MA,

1. Isn’t deficit spending inflationary?

With regards to commodity there are 2 questions:

2. Should China continue it’s stockpiling, especially if we take a long view that all countries should? Also consider this question for other rapidly growing economies.

3. Is the global demand for commodity sustainable? Actually, we should keep in mind it isn’t just China growing strongly in 2009. India for example grew 7%. China and India accounts for close to 40% of global population. Many other emerging markets also rocked pretty hard by the end of 2009.

According to J. Chanos, China is currently building 70 billion sq ft of hi rises. 30 billion of that is commercial. That is enough commercial sq ft for every man, woman, & child in China to have a 5’x5′ cubicle. Currently vacancy rates in China probably exceed 20%.

In spite of the PBoC reserves, the banks in China carry tons of bad loans. I asseverate that China is going to hit the wall….for reasons consistent with Austrian Business Cycle Theory.

The reserves of PBoC are not unlike the reserves held by Japan in 1989 & the US in 1929. If the Chinese are such fabulous savers, why has it been necessary for the PBoC to create out of thin air roughly 1/2 of the Yuan with which they buy $s & Euros?

You certainly can’t do such a thing without distorting relative prices & thereby misdirecting resources.

Bryce, you can check yourself the data

http://www.pbc.gov.cn/english/diaochatongji/tongjishuju/

If you look at PBC’s balance sheet data you will see that in the past two years the large accumulation of foreign assets has continued to be financed largely by deposits of (state) banks with the PBC. These deposits are SAVINGS and have nothing to do with an inflationary monetary policy. You are relying on standard ideas of monetary theory that are irrelevant to understand what has been going on in China since 1994.

James, to understand the current levels of commodity prices, I’d appreciate it greatly if you can provide us with a benchmark, like the average prices for 1950-2000 adjusted by any price index you prefer. It’s my view that most commodity prices are today (after the recent decline) at least twice as high as those averages.

sillythings,

Big Spender. Also remember LBOs are companies, not mortgages, and it works different.

Here’s some media indicating that private investors may not want to “deal with” all the trillions, and what happens as a result.

Personally, I have some concerns about being a citizen of a country where all mortgages, car loans, student loans and credit cards are co-signed by the taxpayer.

“….zombies start to eat one another.”

http://www.nakedcapitalism.com/2010/02/bank-securitization-woes-only-beginning.html?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+NakedCapitalism+%28naked+capitalism%29

A lot of people seem to expect a Chinese housing bubble to look like an American housing bubble. It’s not that buyers are over-leveraging and driving up demand, and then developers are extrapolating that demand as a basis for new projects. Instead state owned enterprises are moving out of their core businesses and taking massive loans to build massive housing projects. The fact that there will not be demand for these houses (at projected prices) doesn’t really matter because they initiated the projects in accordance with political directives.

I’d prefer to have hundreds of billions of dollars worth of copper piled up than the same amount of US dollars and treasuries.

Thank you E. Barandiarain. I had relied on Brad Setzer for that generalizaion from ~9 months ago. Going to the site, I find “Savings Deposits” as ~52% of sources; I’m not knowledgeable enough to understand well the other sources. There isn’t a category labelled “printed Yuan”.

I’m sure you are right that many forces are at work in China other than “monetary policy”, but that doesn’t do away with the negative effects of lending money that no one ever saved.

JDH wrote:

My bottom line: the scales tipped last week in the direction of near-term deflationary pressures, despite the strong 2009:Q4 U.S. GDP report and falling unemployment rate.

Professor,

From this paragraph it appears that you agree with Ben Bernanke that a growing economy generates inflation. Please look again at the 1970s and 1980s. This idea that growth causes inflation is nothing be a myth and the exact opposite is true. A growing economy will regulate inflation, but inflation will stop an economy from growing. This whole idea of controlling inflation by driving the economy into a contraction is insane but it seems to be part and parcel of the FED SOP.

Crude oil Jan-02 to Feb-06 looks like an inverse hockey stick !

This is the final hint that global cooling has set in, give me a $100m research grant. Otherwise, I will fake my emails, until you believe my truth.

E. Barandiaran,

For precious metals, I do maintain a graph of long term prices, CPI-adjusted, and updated monthly.

http://www.clearonmoney.com/dw/doku.php?id=public:historical_prices_of_precious_metals

If you find other such resources, I’d like to know about it.

Jim Fickett

ClearOnMoney.com

Just to add onto what Jim provided, this is another good resource for information on precious metals and gold and silver mining companies that have benefited significantly over the past decade from the rise in the gold price and silver price:

http://www.goldalert.com/gold-stocks.php

two quick comments

“Silly things” is not so silly about lack of china bubble. lines up with Barclays and an analyst who used to work for me (runs Larry Kleins China Model). The bubble is only a housing price and building surge on restrictions coming off. the tightening is taking that back, counteracting. China will still hit near 10% GDP growth this year, anyone want to bet?

Jobs taking a while, but the NEXT benchmark will probably show a more solid move to a payroll plus late last year, as indicated by recent withholding data incorporated in monthly wage and salary. Then it will be consistent with all other NBER benchmarks showing recession trough last fall.

Before we get too excited about the unemployment number for January 2010 we need to consider that the -85,000 reported loss for December 2009 was adjusted downward by 76% to -150,000.

Imagine trying to run a business on the reporting of actuals off by 76%. A pink slip would be on your desk when you walked in the door tomorrow. And people talk about not trusting the market and needing the government to manage it. Give me a break!!!

Jim Fickett: Several months ago I found a web site (in Australia as I recall) with a downloadable spreadsheet of gold prices from The Bank of England. Annual data went back to 1800. Monthly data from COMEX went back to 1968. Sorry, I don’t have the web site address any more, but try Google. Its out there.

But Ricardo we are not running a business here…we are counting the hairs on a dog’s back, sampling a tiny patch and making corrections as the beast moves and we get more “settled” data; we skip over the details of those hairs (the chance that they will survive for more than a quarter, the chance that they will spawn new jobs or swallow others, and of course the actual remuneration rather than the unstated conditions set by the employer).

We take it with a grain of salt…not especially trusting government, but waiting for those revisions and hoping the numbers are not being managed for our continuing consumption.

What is happening in China and Europe and on commodity markets is very much related to financial markets’ uncertainty over the Fed’s next moves, particularly the looming end of the MBS/GSE-debt purchase program, coming at the end of March.

There is trepidation that the supply of freshly made dollars that the Fed has been using to purchase MBSs and GSE debt could be suddenly turned off. The recent Fed statement seemed contradictory; on one hand, it said the purchases would end by the end of March as planned; on the other hand, it said rates would remain low for “an extended period”, which is understood to mean at least six months. The purchases are the tool that the Fed is currently using to keep rates so low. So will it use some other tool, or what?

Likewise, the government has been keeping its plans for the GSEs very close to its chest. What is currently underway is a joint effort by the Fed and government to shrink the GSEs’ balance sheets. Having the Fed as a big buyer in the MBS market enables the GSEs to unload their MBS holdings and retire their debts, which collectively came down by >$500b last year. On top of that, the Fed has been buying some GSE debt, leaving practically none for the private market. The category of GSE debt has been eliminated from the market, pushing the kind of investors who would buy GSE debt toward Treasuries and other high-quality bonds.

So what happens when the Fed stops purchasing MBSs? Will the GSEs continue to try to unload MBSs off their balance sheets and retire debt, without the Fed as an MBS buyer? Will GSE debt come back to the market?

No one’s sure, but no one wants to be unprepared. If more debt product will be available amid less demand, a flight to quality must ensue. The bonds of small, uncompetitive Eurozone countries with giant deficits that they couldn’t possibly have funded if they weren’t in the Eurozone, suddenly don’t look so safe.

Because the yuan is pegged to the dollar, yuan liquidity is mechanically linked to dollar liquidity. So the Chinese financial system, and especially its more leveraged and speculative parts, are highly vulnerable to any change in Fed policy.

I keep reading that the minimum down payment on a home purchase in China is 20% for a first home, 40% for a second, and that the average is 50%. I also read that home prices are now 80 times annual income, making the corresponding multiples to annual income, respectively, 16x, 32x and 40x.

It puzzles me that any very large number of people can have accumulated the savings needed to make down payments of such magnitude, especially given that the rapid growth of incomes means also that they were much lower in the not-too-distant past. I wonder whether the amounts are not actually being borrowed, but in some indirect manner (e.g., siphoned off from loans to companies that will end up as bad loans, but will not be counted as loans for real estate purchase).

Hi Jm,

Hahah, the popular media that you’ve read most likely fell for the oldest and most often made mistake in the book. The average home price multiple of income quoted is wrong and by a lot. All real estate is local. Most media probability misunderstood the concept of average and completely neglect the concept of variance. Remember China still have a few of hundred million very poor farmers (larger than the US population).

Here is an analysis of the local housing market in Beijing (one of the hottest in China).

http://www.nuwireinvestor.com/articles/why-the-china-property-bubble-doesnt-exist-54504.aspx

Warning, he is bullish biased. I don’t share his over all view that property bubble doesn’t exist in China. However, I do visit China annually and the housing price and income number seemed about right.

I think it is very likely that there is a real estate bubble in China. What I really wanted to know is the following:

Which economic players (the central gov, the local gov, the banks, the developers, and the home buyers) are taking on excessive leverage in China?

In the last 10 years, we’ve went through 2 recession. One of them, the tech bubble, was not due to over leverage in the over all economy and it was painless. On the other hand, the current and very painful recession is due to massive over leverage across the entire economy.

Therefore, I wanted to know who in China is over leveraged. So far, I still don’t know. I sincerely appreciate any help in sorting this out.

an interesting bit about a new tightening measure being developed by the Fed to drain reserves (eventually), from Bernanke’s comments today:

“As a second means of draining reserves, the Federal Reserve is also developing plans to offer to depository institutions term deposits, which are roughly analogous to certificates of deposit that the institutions offer to their customers. The Federal Reserve would likely auction large blocks of such deposits, thus converting a portion of depository institutions reserve balances into deposits that could not be used to meet their very short-term liquidity needs and could not be counted as reserves. A proposal describing a term deposit facility was recently published in the Federal Register, and we are currently analyzing the public comments that have been received. After a revised proposal is reviewed by the Board, we expect to be able to conduct test transactions this spring and to have the facility available if necessary shortly thereafter. Reverse repos and the deposit facility would together allow the Federal Reserve to drain hundreds of billions of dollars of reserves from the banking system quite quickly, should it choose to do so.”

Interpreting the near-term implications of Bernanke’s statement is like reading tea-leaves, but I understand it this way:

The Fed plans to stop expanding the supply of reserves at the end of March. No further asset purchases are planned after the current program to purchase GSE MBSs and debt is completed by the end of March.

The Fed plans to allow the federal funds rate and other market rates to climb upward after March (as they naturally will without the downward pressure that the Fed is currently exerting by continuously creating new reserves).

Later, the Fed will increase the discount rate, allowing the federal funds rate and other market rates to climb further. (No bank would borrow on the fed funds market above the discount rate.)

Even later, the Fed will begin increasing the rate it pays on reserves.

Around the same time as that or later, the Fed will begin using reverse repos and deposit certificate auctions to drain reserves. (Tests of these will be done in the short-term, but on an insignificant scale.)

Of course, Bernanke’s plans presume a sustained recovery, which I doubt.