98 thoughts on “Big oil companies spending more and producing less”

Tom

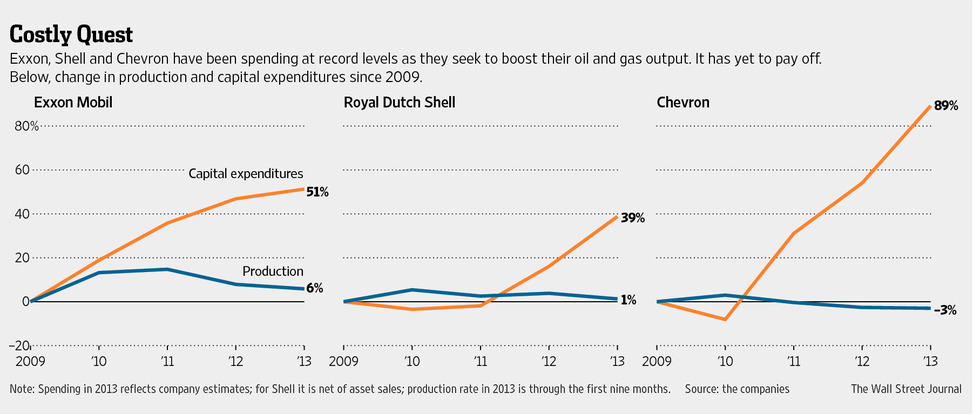

Chevron is explained by the Gorgon project (Shell probably has a similar project). If the capital expenditures are primarily (small) flows to maintain current fields or maintain exploratory operations, then a lumpy field project would distort these proportional figures. For example, Gorgon was never expected to produce until 2014 whereas the capital expenditures are all upfront (if they missed production deadlines, that would be another story). In addition, Gorgon is a “megaproject”, and (judging from the reporting) a much bigger expenditure than the typical oil field development. But there is no comparison between the cost per expected lifetime production of this project versus past projects, i.e. there may be a correspondingly higher lifetime production value capitalized at a single point in time (although I doubt it). A longer horizon would highlight the lumpiness of the capital expenditures and compare it to the declining production (which you’ve highlighted in other posts).

I agree with the general sentiment that oil and gas low-hanging fruit are depleted, but I find these graphs to be a little misleading.

Lyle

Note that Chevron also has another LNG product off northwest Australia Wheatstone. So there are two big projects underway at once.

The big issue is how much nuclear will be used in Japan in the future? That is a significant determination of the viability of these projects.

Note that Gorgon was first discovered in 1981, so it has not been a fast process to develop the field due to it being essentially in the middle of

nowhere.

Steven Kopits

Really, you’re going to leave it at that?

James_HamiltonPost author

Steve: I’m pressed for time this afternoon, and plan to write on another topic this weekend. Just hoping you’d pick up the ball here in the comments!

Steven Kopits

Touche!

2slugbaits

So are we saying that they would have gotten a better return if they had invested in solar or wind? ;->

that affects PV and offshore wind, the crucial question for utilities is whether or how onshore wind is affected: Onshore wind already produces cheaper than new coal, NG or nuclear power plants.

Or from a German POV, nobody plans to build new coal power capacity even when 2022 additional 8 GW nuclaer capacity will be gone. All added capacity until 2015 is legacy from the time before 2005, when almost everybody expected increasing demand until 2030. Therfore, each added GW onshore wind capacity eats away FLH of conventional power plants and erodes their economic base in a energy only market.

From discussion on other boards, the problem of oil companies is that they have no technological advantage when investing in wind or most other REs, they would be in the same situation as McDonald or Münchener Rück. 🙂

Steven Kopits

Can you give me one example of a wind power plant build without subsidies, PTCs, ITCs, or feed in tariffs? I keep hearing that wind is cost competitive, in which case, all public support should be discontinued.

Are you really saying that you don’t think that Climate Change is a real problem? That’s the only justification I can see for such a question. After all, there’s plenty of coal in the world, and if we don’t care about it’s pollution (especially CO2), then we should just burn as much as we want, right?

On the other hand, if Climate Change really is serious, then it’s cost should be internalized into carbon, or non-carbon energy sources should be subsidized.

baffling

kopits, as soon as the oil industry pays back its shipping and military subsidy, they we can talk about removing the PTC from wind, solar, etc. we provide subsidy to industries who are not yet mature-you cannot make that claim about oil and yet they do get significant, even if indirect, subsidies.

Steven Kopits

What shipping subsidy? Product, crude and chemical tankers change hands at market rates. Here’s page on the various Baltic indices which measure, among other things, dirty and clean tanker rates. http://en.wikipedia.org/wiki/Baltic_Exchange

If anything, the Jones Act substantially raises the cost of shipping for US producers.

As for military costs, these are primarily related to the Persian Gulf. I have addressed those elsewhere.

Steven Kopits

As for military protection in the Persian Gulf (Strait of Hormuz):

Some 17 mbpd of crude, and I believe another 2.5 mbpd of product, move through the Strait daily. That’s more than 20% of global oil production.

Of this, equity oil for the oil majors (BP, Exxon, etc) is probably around 2 mbpd, depending on how you want to count. The rest is Saudis (9 mbpd); Kuwaitis, Iranians, Emirates, and Iraq. So the military presence in the Gulf overwhelmingly serves to protect the oil flows of the Gulf’s national oil companies.

Further, on the consuming side, only 11% of Gulf exports find their way to the US. Nearly 90% of Gulf exports flow to Europe, India, China, Japan and other countries.

If you want to get huffy about the matter, criticize the US government for subsidizing Gulf oil exporting countries and the consumers of the other major global economies. US producers and consumers are the least of it.

criticize the US government for subsidizing Gulf oil exporting countries and the consumers of the other major global economies.

I agree completely! I think there’s a pretty good case that the US has gone overboard in it’s interventions over the years in defense of the “stability” of the international oil market, starting with Roosevelt’s guarantee of the Saudi family’s control over the Arabian peninsula, and continuing with it’s intervention in Iran in 1954 which ended so badly in 1979. Unintended consequences…

On the other hand, criticism of US foreign policy is a distraction. For better or worse, the US has chosen to spend a great deal of blood and treasure guaranteeing the security of oil exports for both itself and many other countries. That cost wouldn’t exist if the US eliminated most of it’s oil consumption: the US supply would be secure, it would have surplus to sell to allies, the world market would be oversupplied, and the strategies the US used to eliminate it’s oil consumption would be used everywhere else.

My focus is simply recognizing this very large cost, and accounting for it.

baffling

kopits,

“What shipping subsidy? Product, crude and chemical tankers change hands at market rates.”

and how much would it cost to insure those tankers if they were not protected from terrorists and pirates?

the oil industry does include the nationals. and oil prices around the world are subsidized by the protections provided to all oil in transit. as well as security to the landlocked oil in Iraq, Saudi, Kuwait, etc. I lump them all together. Persian gulf issues affect supply and price here in the states. if those countries and their shipments were not protected, you think oil prices would be lower? I make no distinction between oil nationals and public corporations-they are still all the oil industry. oil is like money, fungible.

Steven Kopits

Slugs –

Efficient markets theory tells us that, on average, all investments should bring their risk-weighted return on average.

The shares of the oil majors have not done too badly, but they haven’t really been all that spectacular, either, in the last couple of years. It is precisely this lack of dynamism which is compelling investors to prefer cash over growth, in turn leading to divestments and capital discipline from the operators.

Wind turbine manufacturers have done less well, particularly post-2008. However, both Gamesa and Vestas have recovered from near-death experiences and have seen significant share price gains in the last two years, comfortably out-performing the oil majors. They remain well off of historical highs. Over the life of the investments, the oil majors have done much better.

The wildcard here is public policy and climate change.

As long as oil, gas and coal companies (and their industrial/commercial partners) manage to use disinformation and insider influence to prevent the proper recognition of the costs of climate change, wind and solar companies will be at a disadvantage.

Heck, if climate change weren’t a problem, we could burn all the coal we wanted, and there’s an enormous amount available – for instance, there’s billions of tons of it in Alaska, which apparently now needs an alternative to oil.

Ulenspiegel

@Steven Kopits

SK wrote: “Wind turbine manufacturers have done less well, particularly post-2008. However, both Gamesa and Vestas have recovered from near-death experiences and have seen significant share price gains in the last two years, comfortably out-performing the oil majors.”

Near death is a little bit overblown, at least in case of Vestas. In addition, Enercon -which does not sell stocks and is the largest onshore producer in Europe- has done very well in 2008-2012 with a completely different strategy than Vestas: They increased vertical integration and were and are able to sell their products with very high price tag. IMHO you miss some critical aspects of the problem.

SK wrote:”Over the life of the investments, the oil majors have done much better.”

But here the irony is that oil companies depend on depleting resources, their wind power competitors not. Therefore, could “done much better over life time” be a little bit artificial comparison when we consider the expected remaining liftime of the companies. 🙂

Steven Kopits

Ulen –

Vestas’ share price fell from 700 to 30. Thus, I should have said “a near death experience for its owners” to clarify the matter.

What are Enercon’s profits? Sales growth?

I think there is no one who has argued more cogently about peak oil than I have. However, peaking oil doesn’t make subsidized energy competitive in and of itself.

If you are arguing that renewables are now competitive and all subsidies and public support for renewables should be discontinued, well, just say it.

Ulenspiegel

According to data I can find for 2011: sales volume 4 billion EUR, profit >470 million EUR.

As Enercon has defended its market share in 2012 and 2013, years with increasing numbers of installed turbines , I do not see any problem for them. A good indicator for their situation was/is the high demand for qualified workers, even in 2012 when Vestas was cutting the workforce they hired.

It is not clear for me, where Vestas got their problems, the major difference is that Enercon does not sell offshore wind turbines but concentrates on the onshore market and is able to provide better service than their competitors. They rule in central Europe, Siemens and GE look really pale in comparison.

Onshore wind power in northern Germany produces for 5-8 cent/kWh, this is below the costs of NEW CAPACITY of nuclear, hard coal and (of course) NG. This fact is not disputed by the large utilities. The FIT for wind power is around 8-9 cent/kWh in 2013.

The FITs will be reduced for onshore wind and direct marketing (last years it was around 50% for new capacity) will become mandatory, therefore, they are on track.

And one can add that each kW PV that is used to cover own consumption is already highly competitive in Germany: production costs 10-15 cent/ kWh, consumers pay the utility 25-30 cent/kwh , small industry etc. ca. 15-20 cent/kWh.

baffling

kopits,

“If you are arguing that renewables are now competitive and all subsidies and public support for renewables should be discontinued, well, just say it.”

I argue that oil is mature and should not receive any subsidy at all! pay fairly for your mineral rights and defense of shipping lanes, overseas labor, etc.

2slugbaits

Steven Kopits,

I think you’re talking about returns for the oil industry in the aggregate. I was just referring to those particular capital investments shown on the WSJ chart. Those look like losers to me. My secondary, but less obvious point, was that people who like to point to failed “green” projects should keep in mind that plenty of dirty carbon projects fail as well.

Steven Kopits

Of course, there are failures in the fossil fuel industry. For example, Shell just wrote down a bunch of onshore US assets. The difference is whether these are paid for by the owners (the shareholders), who have voluntarily invested in the company, or taxpayers, who have been coerced into investing in the company.

Overall, oil projects remain profitable, but that profitability is eroding. So it’s not that the high capex investments have failed, it’s that they’re increasingly failing to reach their hurdle rates, even if they are profitable in an accounting sense.

taxpayers, who have been coerced into investing in the company

Or, people who’s clean air is being stolen from them by the burning of carbon fuels.

Or, taxpayers coerced into paying trillions for oil wars.

baffling

kopits,

the highway system has been built from taxpayer money-including gas tax-to facilitate a mode of transportation primarily based on oil! so we the people have also paid a price for so called “failed” fossil fuel assets as well, albeit in a less direct sense. it is disingenuous to say fossil fuel failures are paid for by investors and green failures are paid for by taxpayers.

Joe Clarkson

Does anyone have the data to extend the trend-lines in the posted graphs back in time? It would be interesting to see the longer term relationship between capex and production, especially whether huge increases in capex relative to production is a periodic occurrence or is a recent phenomenon only. I tried to find the information on line, but couldn’t find any sources except for proprietary reports.

Jeffrey J. Brown

Here are some numbers I put together, based on Steven Kopits’ excellent work*.

The cumulative increase in global crude oil (Crude + Condensate) production, in the seven year period from 1998 to 2005, in excess of what we would have produced at the 1998 production rate of 67.0 mbpd (million barrels per day, EIA), was 6.3 Gb (billion barrels).

Steven Kopits estimated that cumulative global upstream (oil exploration and production) capital costs were $1.5 Trillion in the seven year period from 1998 to 2005.

Of course, the total upstream capital expenditures were used to both offset declines from existing production and to show a net increase in production, but I am primarily interested in the difference between the 1998 to 2005 increase in global crude oil production versus the 2005 to 2012 increase in global crude oil production.

The cumulative increase in global crude oil production, in the seven year period from 2005 to 2012, in excess of what we would have produced at the 2005 production rate of 73.6 mbpd (million barrels per day, EIA), was 0.3 Gb.

Steven Kopits estimated that cumulative global upstream capital costs were $3.5 Trillion in the seven year period from 2005 to 2012.

Note that cumulative upstream capital costs increased by 133% from the 1998 to 2005 time period to the 2005 to 2012 time period, but the corresponding increase in cumulative production (relative to 1998 and 2005 respectively) fell by 95%.

Therefore the global upstream capital costs necessary to offset production declines from existing wells and to add one new barrel of cumulative production in the 2005 to 2012 time period was 39 times what was necessary to offset production declines from existing wells and to add one new barrel of cumulative production in the 1998 to 2005 time period–in terms of capital costs per barrel of new cumulative production (relative to 1998 and 2005).

In terms of barrels per day (bpd), the industry had to spend 58 times as much money from 2005 to 2012 as they did from 1998 to 2005, in order to add one new bpd of average incremental production (relative to 1998 and 2005), in terms of capital cost per average bpd increase in production.

And note that annual Brent crude oil prices rose at an average rate of about 15%/year from 1998 to 2012.

A critically important point to remember is that the post-2005 decline in US petroleum consumption, and the post-2008 increase in US crude oil production, caused US demand for net oil imports to decline, but this had no impact on the global supply of net oil exports.

We have seen a material post-2005 decline in Global Net Exports of oil (GNE**), with developing countries, led by China, so far at least, consuming an increasing share of a post-2005 declining volume of GNE.

The reality facing the US and most other developed net oil importing countries is that they are gradually being priced out of the global market for exported oil, via price rationing, at least relative to 2005 consumption levels.

At the 2005 to 2012 rate of decline in the ratio of GNE to Chindia’s Net Imports (GNI), the GNE/CNI ratio would approach 1.0 in only 16 years, which implies that the Chindia region alone would theoretically consume 100% of Global Net Exports of oil. What I define as Available Net Exports of oil, or GNE less CNI, fell from 41 mbpd in 2005 to 35 mbpd in 2012.

For more information, you can search for: Export Capacity Index.

*Data Source: Barclays Capital

**GNE = Combined net exports from (2005) Top 33 net oil exporters, total petroleum liquids + other liquids (EIA)

With respect to price rationing, it seems reasonable to assume that within the US, it is generally the least-productive uses of liquid fuels that go first. If someone out in the exurbs works one day per week from home rather than driving, the loss of production is minimal but the decrease in their personal fuel use may be substantial. A suburbanite who takes a minute to order an errand list to reduce the distance traveled probably gets that minute back, and then some. I would guess that there’s quite a bit of low-hanging fruit in the US where miles traveled (and correspondingly, fuel used) can be reduced at no economic cost. The value of the marginal gallon of gas is increasing rapidly in the developing countries right now; the rate of increase is bound to decline in the future. The interesting question, IMO, is if and at what allocations things stabilize. Has anyone done any modeling around that question?

The average MPG of US light vehicles on the road is about 22. The cost of increasing MPG to 44 (or reducing fuel consumption by 50%) through natural attrition is very low. Given that light vehicles account for about 55% of US oil consumption, it’s pretty clear that the US has a lot of low hanging fruit.

There’s a lot of industrial/commercial low hanging fruit as well: movement of freight from long-haul trucks to rail; aerodynamic improvements to trucks; conversion of large-volume long-haul freight routes to CNG & LNG; use of hybrid and PHEV trucks for local delivery; conversion away from oil petrochemical feedstocks;, etc., etc.

I’d say an equilibrium consumption level in the US, even with just current tech, is roughly 50% of current levels. And, of course, with economies of scale and engineering progress the cost of hybrids, PHEVs etc will continue to fall quickly.

Steven Kopits

“If someone out in the exurbs works one day per week from home rather than driving, the loss of production is minimal but the decrease in their personal fuel use may be substantial.”

I would guess most people work within 25 miles of home, or two gallons worth of gasoline, which costs around $7 in total. So you’re saying going into the office is not worth $7?

“With respect to price rationing, it seems reasonable to assume that within the US, it is generally the least-productive uses of liquid fuels that go first.”

The least productive uses are, in descending order (change from 2005 to 2012):

– residual fuel oil, down 65%

– Heating oil (!): down 46%

– Distillate for power: down 45%

– Asphalt: down 40%

– Pet coke: down 35%

– Jet fuel: down 14%

– Gasoline: down 4%

– Diesel: down 0%

The consumer has spoken. They’d rather go without heat than without their cars. Mobility is critical, and except for NY, DC, and maybe parts of SF, mobility involves a car.

“The value of the marginal gallon of gas is increasing rapidly in the developing countries right now”

Marginal value decreases with increasing quantity.

“The interesting question, IMO, is if and at what allocations things stabilize. Has anyone done any modeling around that question?”

Of course. For the US, carrying capacity is around 4.25% of GDP for crude oil consumption. For China, it’s probably around 6% now.

So you’re saying going into the office is not worth $7?

He referred to “working from home”, not being idle.

They’d rather go without heat than without their cars.

Steven, this is a good example of an oddly static, highly unrealistic analysis. As a practical matter, no one is going without heat: instead, they’re insulating their homes, or switching to natural gas or heat pumps.

For the US, carrying capacity is around 4.25% of GDP for crude oil consumption

Again, this is an oddly static kind of analysis. The fact is that above around $60/bbl, consumers start to find better and cheaper alternatives. In the short term that may include modest sacrifice, like slowing down the container ship or catching a ride into work with a neighbor, or ordering things online, but it doesn’t take long to find truly better and cheaper alternatives like hybrids. And, some people discover that ordering things online is actually better and cheaper.

baffling

kopits,

“I would guess most people work within 25 miles of home, or two gallons worth of gasoline, which costs around $7 in total. So you’re saying going into the office is not worth $7?”

I can still “work”, but now I have an extra hour plus which is not stuck on the road consuming gasoline. I can work an extra hour, go to the gym, or simply take a nap-my preference. but I now am more productive and have an additional $7 plus extra work $$ in my pocket to spend. and I have reduced the “demand” of gasoline, so my future tank refill will be slightly less than otherwise.

“The consumer has spoken. They’d rather go without heat than without their cars.”

You really think people are going without heat in favor of their car? Or could it be that our home heating systems are getting more efficient, and alternative sources (gas) are being used. Up north I hear gas consumption was at record levels during the past cold spell.

Several years ago, I used to put on 20-30k miles a year on my car. Now I am lucky to put on 10k a year (although gas mileage is about half of my old camry stick shift). Even so, I will probably pull the trigger on a hybrid or EV in the next couple of years.

The reality facing the US and most other developed net oil importing countries is that they are gradually being priced out of the global market for exported oil, via price rationing, at least relative to 2005 consumption levels.

You make that sound like a bad thing. If people are moving to cheaper or better alternatives, that’s all to the good.

Many young people are choosing social media to meet each other, instead of cruising in cars. Some are choosing to live in urban areas rather than contribute to climate change (and liking the location better). Some people are buying hybrids to save money, and Teslas to have fun (while still saving a lot of money).

Oil is dirty, expensive and risky. It’s time to move away from it ASAP.

Steven Kopits

No, Nick. If people were moving to cheaper alternatives, then VMT would be rising on trend. It’s one car in six off trend, even allowing for the recession. But still, tell me again what’s cheaper and better than oil for a person making, say, $50,000 per year (median household income)?

2slugbaits

Steven Kopits,

I have to say that I’m a little puzzled by this. The problem is that too many cities…especially Sunbelt cities like Atlanta, Dallas and Houston, but also northern cities like Seattle, have been organized around the mobility of the private car. So we shouldn’t be surprised that cars are the most cheapest form of transportation for median income folks. But simply making that observation doesn’t answer the larger policy question of where do we go from here? The answer isn’t to continue to make driving as cheap as possible come hell or high water; and I think we can take that “hell or high water” comment quite literally given climate change concerns. There are two big policy issues. The first is that while driving might be the cheapest form of transportation for the median worker, it rarely is for those workers in the lowest quintiles. They depend on subsidized public transportation. Expanding public transportation would open up job opportunities for many low income workers. The second policy issue is that depending on private cars is temporally inconsistent behavior over the long run. It’s an economic model that we know will fail within the lifetimes of many of today’s young workers. The problem is that for many workers (particularly those that vote and are in their peak earning years), that day of reckoning is outside their lifetime horizon, so they have very little incentive to change the private car commuting to work model. But every year we put off doing what needs to be done because comfortable people don’t want to face uncomfortable truths, that just increases the costs down the line. When it comes to matters of consumption smoothing across generations, the evidence is pretty clear that aggregate private decisions are a big fail. Our addiction to dirty carbon is pretty strong evidence that people do not follow some optimal control theory style Euler equation across an infinite horizon. They just don’t. So we need a benevolent government bureaucrat to force us to do the right thing.

If people were moving to cheaper alternatives, then VMT would be rising on trend.

Steven, you’re not really reading my comments and thinking them through. In this instance, I didn’t say young people were switching to hybrids (though some are), I said they’re switching from cruising in cars to using Facebook, or choosing shorter commutes.

what’s cheaper and better than oil for a person making, say, $50,000

The US fleet average is currently 22MPG, with the median light vehicle at about 6 years old. So, for that average person, trading in for a used hybrid of about the same age, getting 45MPG, would be an enormous improvement.

Jeffrey J. Brown

And some US natural gas numbers.

As best that I can tell, the Marcellus produced about 8 BCF/day in 2013.

Citi Research estimates that the 2013 decline rate from overall existing US natural gas production was about 24%/year (all sources, dry gas wells, wet gas, associated gas). This would be the estimated percentage decline from 2012 to 2013, if no new wells were completed in 2013.

Using the (processed) dry gas metric, the EIA shows that the US produced about 66 BCF/day in 2013. Based on the Citi Research estimate, we need about 16 BCF/day of new production every year, in order to maintain a processed dry natural gas production rate of 66 BCF/day.

Or, in order to maintain 66 BCF/day, we would need to put on line the productive equivalent of the 2013 production from the Marcellus every 6 months. So, over a 10 year time period, we would to put on line twenty (20) times the productive equivalent of the 2013 production from the Marcellus–just to maintain 66 BCF/day for 10 years.

Some industry watchers expect natural-gas storage to be significantly lower than average at the end of the winter, prompting concern that inventories still may be low by next winter.

Storage levels could fall below 1.2 trillion cubic feet by the end of March, said Anthony Yuen, energy strategist at Citigroup, C +0.25% meaning that producers would need to supply more than 2.5 trillion additional cubic feet to bring storage back to October 2013 levels.

If storage levels aren’t replenished by next winter, natural-gas supplies could be “uncomfortably low” in some areas of the country, sending benchmark futures prices higher, Mr. Yuen said.

Refilling storage caverns could be difficult if producers don’t ramp up drilling, Mr. Yuen said. “There has been a lot of talk about, when some price levels have been reached, that maybe producers will come back in” to produce more, he said. “But the market has not really seen that.”

Steven Kopits

Some sources on production and wells.

The EIA recently inaugurated its “Drilling and Productivity Report”, a monthly review of rigs, oil and gas production at the key shale plays. Credit for this goes to Adam Sieminski, EIA Administrator. This has rapidly become a go-to source.

According to this report, Marcellus gas production increased by a whopping 4 bcf/day in the 12 months to December. For purposes of comparison, that’s about 6% of total US production, or the equivalent of total Argentina’s gas consumption.

Based on EIA data through November, the industry has been able to keep us on a natural gas production plateau of about 66 BCF/day.

The problem of course, based on the Citi Research report, is that in order to continue to offset declines, we need 4 BCF/day of new production every 90 days, or 16 BCF/day per year. To put 16 BCF/day per year on line, we would have to replace the 2012 productive equivalent of Denmark + the UK + Norway’s gas production–every single year.

So, at a 24%/year decline rate from existing wells, in order to maintain 66 BCF/day for 10 years, we would need the productive equivalent of:

(1) 20 times the 2013 Marcellus average production rate*, or

(2) 28 times the peak production rate of the Barnett Shale Play (5.7 BCF/day, now declining at about 6% to 7%/year), or

(3) 10 times the combined 2012 production from Denmark + UK + Norway

*I’m assuming a 2013 average production rate of about 8 BCF/day

We have been on a production plateau of about 66 BCF/day since late 2011, which is another way of saying that basically 100% of all new gas production since late 2011 has gone to offset production declines from existing wells.

Depending on storage levels at the end of the heating season, and depending on how much new gas production is brought on line in 2014, as noted in the WSJ article it’s possible that we might face some potentially severe natural gas supply problems next winter.

Note that we are seeing some very significant regional declines in gas production. Combined Louisiana + Federal offshore gas production* fell from 14.8 BCF/day in November, 2011 to 8.1 BCF/day in November, 2013, a decline of 6.7 BCF/day in two years. This is a simple percentage decline in monthly production of about 23%/year (annual decline rate would be lower). Note that this is the net decline, after new wells were put on line. The Citi Research number was the estimated overall US annual decline rate, if no new wells were put on line in 2013, versus 2012.

*Marketed gas production (EIA); they don’t have regional (processed) dry gas production numbers

Steven Kopits

You might be right, Jeffrey.

From my perspective, the question is what the economics are at $6-7 / mmbtu, where I think we will eventually end up. Remember, right now the Marcellus is gutting alternative supply in the US and Canada. If prices rise, then non-Marcellus sources will ramp production.

Also, there’s quite a lot of noise regarding the Utica. Allegedly, it’s bigger than the Marcellus and lower cost to produce. I can’t attest to the veracity of the claim, but it’s out there.

Steven Kopits

Joe –

Send me an email, and I’ll send you my Princeton presentation. It has the numbers both historically and prospectively.

To his credit, Steven Kopits has been remarkably prescient regarding this topic.

aws.

Jeff,

That’s true, Steven has been remarkably prescient and I have learned a good deal from his work. What confuses me though is that having illustrated to us that we are scraping the barrel Steve’s recommended solution seems to be “scrape harder”. That’s as absurd as suggesting that the “beatings must continue until morale improves”.

In his response to you just above this comment he throws out the Utica shale as our next great hope! Hasn’t it been shown that the last few great hopes were over-hyped”.

When do good PO analysts like Steven, and he’s not alone, start to suggest that we need a new approach to supplying our energy needs, one that recognizes that we have no choice but to transition to a Post Carbon economy. I’m sure he knows fossil fuels are finite, and he’s definitely helped us recognize that we can’t grow production much more. So why does he condemn wind and solar? I can’t see how he’d think that the single minded extraction of fossil fuels offers us any viable way forward.

Perhaps you can help explain his thinking to me, I believe you know him better than me?

Steven Kopits

AWS –

You raise a number of issues. Let me address a few.

As regards the Utica, please re-read my comment. I wrote: “Allegedly, it’s bigger than the Marcellus and lower cost to produce. I can’t attest to the veracity of the claim, but it’s out there.” I am referring to investment banking reports that come across my desk and industry chatter. I have not taken a position on the matter–my comment makes that entirely clear. But I can say that the Utica is a recurring topic in investment banking reports that come across my desk as well as in industry chatter.

Steven Kopits

AWS –

As for “scrape harder”:

I strongly believe that GDP is a function of land, labor, capital and/i> energy. Within that, oil is critical to transportation. There is no ready substitute. For example, hybrids have been mentioned above. But how good are the economics? A hybrid version of a Camry or Accord costs $4,000-$8000 more than the gasoline version. The improved mileage only really applies to city driving, where braking recharges the battery. If you drive as I do (2/3 local, 1/3 highway), then the payback period on a hybrid is around 11 years. And we know a consumer requires a 3 year payback period to make an investment. So a hybrid doesn’t pass the test for most people. And that’s the best we have right now.

I have several times in the past laid out the vision for the future of the transportation system. In the short to medium term, I would emphasize CNG vehicles, keeping in mind that they are subject to the same payback criteria applicable to hybrids or any other type of car. Second, my post-2020 vision revolves–at the margin–around self-driving electric vehicles, which I see as taking an approximately 25% market share, and I have urged the Administration and Congress to be more aggressive on the issue. But this still implies that oil-powered vehicles would be more than 50% of the global fleet. So oil doesn’t go away.

I would also add that gasoline consumption in China is growing at around 8%, which is what we would expect to see. China’s not going away, either. It’s true, diesel and naphtha in China grew at 0.1% and -10% respectively in 2013, suggesting that heavy industry and at least parts of the manufacturing sector are in a de facto recession there. But these will bounce back, and China’s call on oil will resume. Do the numbers, and you’ll see that the China’s oil demand growth in the second half of this decade is likely to be eye-popping. And there won’t be enough oil to go around, just as there hasn’t been since 2005.

So it comes down to how fast the economy can adjust. Again, I have posted on this many times. Nick suggests swapping a low mileage car for a high mileage one. And I agree–and it’s happening! But the purchase decision is not “Should I buy a low mileage car or a high mileage one?” Rather, the decision is, “Should I keep my current vehicle or buy a new one?” Thus, the economic decision is not efficient new car vs inefficient new car, it’s inefficient old car that’s paid for vs efficient new car that’s not paid for. Of course, at some point, the old car will go, and an efficient new car will be purchased. But that takes time, and it is precisely this time which determines the pace of efficiency gains in the economy. Therefore, the key issues are the following:

– Is there a cheaper or better alternative to current energy sources? Is something better than oil, keeping in mind that the consumer will require a three year payback period for a vehicle that’s Pareto optimal in every other sense. If there isn’t, then you’re going to continue to provide the best energy source as much as you can. Today, that’s still oil. (And if Tesla’s cheaper, Nick, bring around your “S” when you’re next in New York and take me for a ride.)

– The second question asks, “How fast can we adjust without material reduction in economic growth?” And we have a pretty good idea of that number. It’s probably not more than 2.5% efficiency gains per year, and may be not more than 1.5% per year. In such a case, you’d like to manage oil supply growth to prevent material damage to GDP growth. I am making a kind of Keynesian argument, that infrastructure and social organization are “sticky”, and that the pace of change has to be gradual, or the economy will suffer. Now, if you try to maintain consumption by incurring debt without supporting adjustment, then you’ll just incur a lot of debt with unsatisfactory GDP growth–just what we’ve seen. On the other hand, if we want to adjust while maintaining GDP growth, then that adjustment has to be to a better or cheaper transportation solution than oil. And that’s either CNG or self-driving electric. By this way of thinking, the ARPA CNG project was not an interesting initiative of the Obama administration, it was the critical initiative of the Obama administration. But they didn’t see that.

So, as I look forward, I am balancing a portfolio of issues: oil supply cost and growth, the impact of China, the viable pace of efficiency gains, the potential and cost/benefit of various transportation solutions, the cost and institutional structure of renewables, and the relationship of all these to GDP growth. I live in the world of spreadsheets, where we try to move beyond anecdote to analysis.

I have been described here as “prescient”, which I take as a compliment. But this prescience comes from actually checking the numbers. None of my analysis is creative or original. It’s all just analyzing a given topic, researching drivers, and making reasonable forecasts based on knowable trends, in general all from public or accessible sources. The cumulative effect may be creative, but the process is mechanical. Any reader could reproduce my work. I don’t have any special tools, but I do try to apply the tools that I have systematically.

So, AWS, when you suggest that I advocate “scraping the barrel”, keep in mind I am looking at a broader range of issues where maintaining and growing the oil supply is, for all that, a critical component of sustaining GDP growth.

baffling

kopits,

would you be against government sponsored R&D with the transformative potential to rid the use of carbon fuels and implement renewable energy and distribution systems which make the country energy independent?

we understand transitions should be smooth. but we have also faced significant resistance from vested interested in looking into technology which could be transformative on the energy landscape. if we develop that technology, then a “smooth” transition is no longer a good thing, and a fast overhaul to the better system should occur. unfortunately, we have a lot of interests who do not want this research done due to the demise of existing interests. but if in the long term these new technologies are superior-we should invest in them today even if it requires abandoning a “legacy” of infrastructure built up over 50 years.

the argument made against you and “scraping the barrel” really is why should we continue to pursue an energy landscape that does not hold a long term future? disruption is going to occur with the change, but is it better to transition before we run out of oil? then you change on your own terms-or terms you have better control over.

Steven Kopits

I am not against government research, but government’s a cost center, not a profit center. As a friend of mine says, “Structure is strategy.” Structure ain’t that good. The Plasma Physics Lab is here is Princeton. Have these guys produced any value-added in the last forty years?

“Vested interests”

Who are the vested interests opposing renewables? BP, ConocoPhillips, these guys had renewables arms, and a very tough time making it work. A million barrels a day of oil is whole lot of wind turbines. But let me give you a concrete example of “resistance”. So, I was visiting with a marine construction company in Houston, explaining to a manager the economics of offshore wind. “Well, it’s like this. Offshore wind costs $6 bn a GW of nameplate capacity, which might actually produce 40% of the time. Of the $6 bn, $3 bn is subsidy, and we want to do 3 GW in New Jersey, so figure $9 bn in subsidies, or about $1,000 per capita.” The guy literally burst out laughing. He thought people on the East Coast had gone insane.

“Why should we continue to pursue an energy landscape that does not hold a long term future?”

“We” are not pursuing anything. Oil companies are making project by project investments based on expected returns. It is not about some theoretical “long term investment”, it is about a specific investment over a specific period of time with a quantified expected return. It’s not abstract, it’s entirely concrete. But if you want policy, I have repeatedly called for greater emphasis on CNG vehicles. That’s Pres. Obama’s call. Where is his sense of urgency?

baffling

kopits,

inherent in all of your arguments is the “need” to keep oil in the equation. have you ever considered a world without oil? of course talking to a man in the offshore oil business will result in ridicule of offshore wind-that is until he realizes he may be part of the offshore wind services group in the future. opportunity awaits those who are willing to adapt. unfortunately most of the loudest and shrillest voices are those who are too lazy to adapt to a new and better environment, but want to keep us in an environment where they currently have some advantage. i certainly understand this mindset, but it should not drive the direction of the country.

as for your insult to the plasma physics lab-where do you think the scientists and engineers get their education and training? it does not come from the private sector at any level close to what happens in these labs. the private sector does employ and do good work-but they are not very good at training and nurturing young talent-they want somebody else to do this, typically the university. private sector has been punting on this area for a long time to their detriment.

aws.

…keep in mind I am looking at a broader range of issues where maintaining and growing the oil supply is, for all that, a critical component of sustaining GDP growth.

So you don’t anticipate global C+C production declining? Or North American hydrocarbon gas production declining?

What do you foresee the average annual price of Brent, and the Henry Hub gas price, rising to in order to maintain (not grow) oil & gas supply. Is that price compatible with sustainable GDP growth?

Steven Kopits

C&C Decline:

Right now, US shales and Canadian oil sands are pretty much what stands between us and peak oil. So I accept that oil is a finite resource that is increasingly challenging to extract. But that’s a whole different story than saying, for example, that we should walk away from $1.2 trillion worth of oil in the Alaskan Outer Continental Shelf.

North American gas production could run for some time. Hard to say. The true economics are not entirely visible yet, but we can certainly afford $6 / mmbtu gas, and that’s where I expect we’ll be going. But smarter people than me think it’s $5 or less. But, yes, I think there’s a lot of gas out there at some price.

I see Brent rising at i) global GDP growth + ii) efficiency gains (say, 2-2.5% per year) + iii) dollar inflation. This puts me among the bulls on oil prices, below Barclays but above Goldman Sachs and way above Citi.

hybrids have been mentioned above. But how good are the economics?

This is risible. Once we include all of the costs, including supply security and pollution, hybrids are far cheaper and have a far superior ROI.

A hybrid version of a Camry or Accord costs $4,000-$8000 more than the gasoline version… the payback period on a hybrid is around 11 years.

Absolutely not true. Go to Edmunds.com and compare the base Camry ICE model with the base hybrid: compare the cumulative annual costs, and you’ll find that you’ll save money after the *second* year, and the five year cost of the hybrid is $1,851 less than the ICE conventional sedan.

That’s a two year payback!

GDP is a function of land, labor, capital and energy. oil is critical to transportation. There is no ready substitute.

That’s unrealistic on the face of it. There are many ready substitutes. If we’re focusing on GDP (*Production*), then we’re focusing on freight for industrial/commercial transportation. Rail is an obvious substitute, using 70% less diesel compared to trucking, and it can be electrified. Trucks can and are going to CNG and LNG.

I think you’re focusing on “ready”, but the pace of adoption isn’t linear: it’s slow right now because companies are still uncertain whether oil prices will stay above $60: remember, we’ve got Republican presidential candidates promising $2 fuel!! If prices rise above $120 for a good period, things will accelerate. In any case, growth is exponential, and slow growth now will translate into fast growth later on. we know a consumer requires a 3 year payback period

Are we seriously going to rely on the flaky 33% ROI demanded by a fictional consumer?

In the short to medium term, I would emphasize CNG vehicles… Second, my post-2020 vision revolves–at the margin–around self-driving electric vehicles

A red herring, like fuel cells. Hybrids and plug-ins are ready now.

the decision is, “Should I keep my current vehicle or buy a new one?”

Absolutely not true. If a used car owner is strapped for money, they can (and do) trade for another used car. The volume of used car sales in the US is 3x as large as the volume of new cars: used cars turn over often, and most of the time not for a new one.

if Tesla’s cheaper, Nick, bring around your “S” when you’re next in New York and take me for a ride.)

Well, I’ve already reduced my driving to about 1,500 miles per year: I take an electric train to work. On the other hand, all of the taxis I take are hybrid: their owners know they’re much, much cheaper and better.

I am looking at a broader range of issues where maintaining and growing the oil supply is, for all that, a critical component of sustaining GDP growth.

It’s really not. The sooner we kick the oil habit, the better off we’ll be.

kopits,

a better comparison is between a camry and prius. compare cars that were directly designed as gas and hybrid-not modified to fit that category. in the 5 year cost of ownership the camry was $35,900 and prius $33,475. Within that number, fuel cost was $9900 and $5500 respectively. That spread will only increase in prius favor as gas prices rise. Also, the camry has slightly better depreciation and financing cost, which will improve as more hybrids become accepted. Overall for 5 years, camry is $0.48 a mile and prius is $0.45 a mile. this does NOT include any tax credits. the hybrid and EV advantage will only grow with time…

Now go to True Cost of Ownership: For 5 years, the Camry costs $38,018 to own, while the Camry Hybrid costs $36,167. The Hybrid costs $1,851 less to own over the first 5 years, and costs about $110 less over just the first 2 years.

If you check your example at Edmunds, you’ll find that the five year savings in gasoline are almost identical to the cost differential. So on that basis, the payback is five years. Interestingly, the factor that makes the hybrid more attractive is the insurance, calculated at about $360 less per year than the gasoline powered LE. Don’t know why.

In my case, all the family cars do 12,000 miles per year, not 15,000 as the sample would have it. Based on our share of city versus highway, the savings come out to $500 per year at gasoline prices prevailing in our neighborhood ($3.43 per gallon). Thus, the payback period, calculated on fuel alone, is about 6.7 years for the Edmunds example. This alone would probably not induce me to buy one.

If I include the insurance differential, the payback is 3.9 years, which is approaching three years. Assuming those savings were real, yes, I would consider a hybrid, assuming I had confidence in the technology and re-sale value.

baffling

kopits,

if you compare the camry and prius, which is more appropriate since this is not a “converted” hybrid, you will see the fuel savings is substantial. Also, you use $3.43 as the cost per gallon of fuel. Since you are the expert in this area, do you expect that price to hold over the next 5 years for gasoline? Or do you expect a greater probability of much lower or higher gasoline prices?

Steven Kopits

That should read “Drilling Productivity Report”

Duracomm

Nick G said,

As long as oil, gas and coal companies (and their industrial/commercial partners) manage to use disinformation and insider influence to prevent the proper recognition of the costs of climate change, wind and solar companies will be at a disadvantage.

Wind and solar are subsidized and mandated. They are disadvantaged by physics, not political policy.

Actually, it’s coal, oil and gas which are disadvantaged by physics: they are limited in supply, and they emit CO2 when burned, which is expensive to sequester, and even more expensive to leave in the atmosphere.

Duracomm

Niick G,

So you agree that the fact that solar and wind are subsidized and mandated shows that they are politically advantaged?

baffling

duracomm,

if something has a better long term prospect for the country, what is wrong with it being politically advantaged? there is a legacy economic advantage to oil, but it is not the future of this country. must we wait until that economic advantage goes bust before proceeding on the right course of action?

Ulenspiegel

Duracomm wrote: “So you agree that the fact that solar and wind are subsidized and mandated shows that they are politically advantaged?”

That is a strawman, and BTW not a very clever one:

1) The current market rules and infrastructure have been shaped by utilities over decades, in Germany since 1935. To assume that a newcomer can fight within a few years on a leveled field is naive, esp. when the new capacities have different owners than the existing ones.

2) Little Gedankenexperiment: If you were able to make tabula rasa and were able to create a new system from scratch, how would it look with current production costs of new capacity? Please, do not tell me we would see nuclear power or (conventional) base load for 80% of the demand and the production capacity would be owned by a few companies. 🙂

3) Conventional power plants have received huge subsidies in the past, in Germany the situation (without nuclaer weapon development) is quite clear: Nuclear got 200 billion EUR, coal 400 billion EUR.

Some of these made from a strategic point of view perfect sense, even when nuclear power failed to deliver cheap energy. However, to deny REs the same support despite their clear strategic advantages sounds less convincing IMHO.

I have no problems to let REs compete in a free market, when they have reached 45-50% (2030), until then I would support some FITs at least for PV and offshore wind.

Duracomm

Facts are facts not strawmen.

The really dreary argument that always shows up appears here

Conventional power plants have received huge subsidies in the past

So because industry A robbed consumers 75 years ago we need to pass laws that make it possible for company B to steal from consumers today.

Not a serious argument. Not serious but made without fail by advocates for never-ending corporate welfare at the expense of the consumer.

Ulenspiegel

@Duracomm

Duracomm wrote: “So because industry A robbed consumers 75 years ago we need to pass laws that make it possible for company B to steal from consumers today.”

You sell me it is ok that company A has robbed the consumer/taxpayer for decades and has used these resources to create a structure that suits it now, i.e. company A has used its gains to create a defense against potential competitors.

I would tax company A or give subsidies to company B. But this is only a cosmetic problem.

The basic issue for which you do not propose any solution is (point 2 in my last post): Almost nobody disputes that the differential costs between a green energy generation + electrification of transport and space heating on one hand and a conventional scenario on the other will turn negative around 2030 (even without externalities), so why not investing 400-600 billion until 2040-50 for the transformation when we have a good chance to write black numbers within a generation? This is a purly strategic question. A byproduct would be the reduction of CO2 emissions and reduction of other externalities. For me – I grew up in a country that has to import 80% of its primary energy – the answer is clear.

Oil, coal and gas have far more political power than wind, sun or even nuclear. The carbon industries (and related industries, like the car industry) have successfully fought and delayed the inevitable transition, and received enormous indirect subsidies recently, including $2 trillion oil wars.

The interstate highway system, and local roads, are heavily subsidized: their total direct and indirect costs (including foregone property taxes, which are paid by competitors such as rail) are much higher than the fuel taxes which nominally pay for those roads. What other industry manages to keep all of it’s taxes for it’s maintenance (and pull in general revenues in addition!), instead of contributing to the general overhead cost of running government?

The indirect subsidy of unregulated CO2 emissions is an enormous subsidy – the fact that Climate Change has been heavily disputed in the US, and that very few Republicans are willing to admit that Climate Change is a serious problem, is a dramatic statement of the political power of the carbon lobby.

Do you agree that Climate Change is a serious problem? If so, don’t we have to fix the price incentive so that free markets can work properly, by taxing carbon or subsidizing non-carbon energy?

Doug of North Texas

I was taking Oil and Gas Accounting at Univ of Texas Dallas in the early 1980s and saw the same pattern in the data from 1975 to 1980 – a doubling or tripling of expenditure to obtain oil and gas, but only a small increase in the US of energy produced – good for drillers, but not for anyone else. This stuck with me because it was so obvious in the data and not commented on then (don’t ruin the game?).

But item number 2: don’t look to the big players for efficiency in production – it has been the smaller players driving it while the bigger players look for huge bonanzas requiring huge expenditures and lower odds – this is the corruption of size and it exists in and beyond the energy patch – compensation based on project size, not project efficiency. See if you can get data on BP – they seem to personify the search for the White Whale, with oversized pay for undersized results.

Ricardo

I am still not sure the point. Is capital investment a good thing or a bad thing? It seems to me that if the big oil companies did not believe they would receive a positive return in the future they would not make the capital investment but invest the money elsewhere until a better time. It seems obvious that the oil companies believe that capital investment in their current projects will give them a return. That seems to be encouraging for the future.

baffling

ricardo,

it could also show you that private enterprise is not always the intelligent, efficient decision maker some folks would like to believe. perhaps the decision makers are biased by preserving their legacy, recognition of bagging the white whale, etc which overshadows the good of the company at large.

Duracomm

2slugbaits said,

So we need a benevolent government bureaucrat to force us to do the right thing.

That mythical creature does not exist.

What you are going to get is a self serving bureaucrat implementing policies carefully crafted to help the politically connected.

Tax breaks for Hollywood, NASCAR, windmills, algae and multinational corporations ended up in the “fiscal cliff” bill thanks to President Obama, according to Senate Republican sources. But they were spawned by a web of lobbyists, donors and staffers surrounding Democratic Sen. Max Baucus of Montana.

Pick any one of the special-interest tax breaks extended by the cliff deal, and you’re likely to find a former Baucus aide who lobbied for it on behalf of a large corporation or industry organization.

General Electric may have been the biggest winner from the cliff deal.

But more important for the multinational conglomerate was an arcane-sounding provision that became Section 222 of Baucus’ bill and then Section 322 of the cliff bill: “Extension of subpart F exception for active financing income.”

In short, this provision allows multinationals to move profits to offshore financial subsidiaries and thus avoid paying U.S. corporate income taxes. This is a windfall for GE: The exception played a central role in GE paying $0 in U.S. corporate income tax in 2011 when it made $5.1 billion in U.S. profits.

Prowitt, Finley, Heck and Evans are only a few examples. Baucus’ chief counsels, legislative directors and chiefs of staff litter K Street. They make sure their clients get their tax carveouts, and they make sure their former boss gets his campaign contributions.”

baffling

duracomm,

if we had simply passed a straight fiscal cliff bill to pay our bills, no negotiations would have been needed and hence no amendments. when you create chaos in the process, this is what happens. and i’ll bet there was crap from the other side of the aisle in the bill as well. although your note indicates this was for tax breaks. and there is not a conservative around who would veto a tax break!

so are you one of the folks who complains about tax hikes AND tax breaks? or simply anti-Obama?

I think that many government staffers have good intentions, supported by good professional expertise and related scientific research, but I agree that they’re often overridden by the power of special interests.

Again, the fact that the scientific community (and the international community) has said quite clearly that Climate Change is an enormous, expensive problem, but the US government is barely able to talk about it, let alone begin to implement simple and effective solutions like fuel taxes, tells us just how powerful the carbon industry is, and how successful it is in preventing a necessary transition to low-carbon energy.

2slugbaits

Duracomm,

Sen. Baucus and his useless staffers were not bureaucrats. They were part of the Legislative branch. Bureaucrats are career folks who work for the Executive branch. And good riddance to Baucus and Sen. Ben Nelson.

Duracomm

2slugbaits,

Thanks for recognizing the damage folks like Baucus cause.

Nice change from the unfortunate tendency some have to defend whatever policies their political team develops, no matter how bad they may be.

We’ll all think much more clearly if we try not to choose a “team”.

Just let the facts fall as they may.

reason

Seems like your heading is only true for Chevron, the others have actually still been increasing their output. But given that existing well are being exhausted and new wells require more investment this is hardly surprising.

James_HamiltonPost author

Reason: Down for all three since 2010.

anon2

!

Duracomm

Lots of goods and services are shipped to the US from foreign countries.

If the US military keeping shipping lanes open is a subsidy to the oil companies then US military spending is absolutely, positively a subsidy to companies like apple and google.

Probably more of a subsidy for apple and google because percentage wise it is likely more of their product is manufactured overseas and shipped to the US than the percentage of foreign oil shipped to the US from non neighbor countries.

One other important point that gets missed.

One of the reasons the US ended up with a massive military is because of a trade with European countries. The trade was Europe can exist under US military protection. Because of that protection Europe did not need to build standing armies with the ability to project offensive military power.

Considering the way armies with the ability to project power turned Europe to a slaughterhouse for unfortunately long periods of time in the 20th century this was a good tradeoff for Europe and the US.

No doubt European countries would develop the military capability to protect oil shipments from the middle east if the US was not keeping the oil shipping lanes open.

No doubt this type of European military expansion would have considerable downside risk and consequences.

I think we’re in agreement that international shipping (oil and non-oil) is being subsidized by “free” military protection. Whether that military protection is an optimal military or foreign policy strategy is an interesting question, but it’s not relevant to whether someone is getting a “free lunch”.

And we know that “There Ain’t No Such Thing As A Free Lunch”‘ right?

Ulenspiegel

Duracomm,

DC wrote: “If the US military keeping shipping lanes open is a subsidy to the oil companies then US military spending”

Here you mix two aspects. If we are talking about global anti-pirate operations then the contribution of other countries is more important than the US contribution. Only because you send a tank bat for a job that could better be done and is better done by a platoon of riot police does not make a good argument. Carrier battle groups do not do the job, that is a myth. 🙂

On the purely strategic level, stability of the ME, you may still have a point: However, you should also factor in the instability the availability of power projection capabilities have caused (two useless wars). The picture is not that clear.

DC wrote: “The trade was Europe can exist under US military protection. Because of that protection Europe did not need to build standing armies with the ability to project offensive military power. ”

Here you ignore the point that until 1989 the Europaen armies provided more than 75% of the ground forces in central Europe, which bound most of the WP forces and allowed the USA to focus on other stuff. The decision not to scale back after 1989 was a US one, please do not blame other for some of the resulting problems.

Aligning sustainabel economic capacity with realistic political and military goals is a centerpiece of solid startegy. Here the US have a real problem.

DC wrote: “No doubt European countries would develop the military capability to protect oil shipments from the middle east if the US was not keeping the oil shipping lanes open. ”

Here a more sober assesment would be: With the depleting resources in the ME and the increasing domestic demand of the ME countires, a strategy that tries to secure these rapidly decreasing net resources is stupid. If we spend the money on energy efficiency and transition to REs (70% savings would be enough) the strategic result would be much better. We are talking about two or three decades. To have a military to secure resources that are not longer there would be a joke.

baffling

duracomm,

“Probably more of a subsidy for apple and google because percentage wise it is likely more of their product is manufactured overseas and shipped to the US than the percentage of foreign oil shipped to the US from non neighbor countries.”

while it is true others benefit from our shipping lane protections, I don’t think you can even dispute the large amount of money directed to protection and military activity in the middle east region is primarily a subsidy to oil interests, not google and apple. middle east costs have dwarfed spending around the remainder of the globe. or let me state this another way. if the us were to halt all military activity around the globe and send our ships home, who’s product would be most affected by this action: google, apple or oil industry?

Duracomm

Steven Kopits,

When an advocates preferred renewable energy source fails the implementation hurdles of physics, engineering, and economics (a Trifecta of fail) the problem is “Vested interests”.

Except that they don’t. In fact, renewables are better than fossil fuels when analyzed using physics, engineering and economics. If you disagree, you might want to provide some specific arguments, rather than generalities. Read through the arguments I’ve had here with Steven, and look at the specific information provided. Ask yourself whether you disagree with the consensus of the scientific community about climate change. Ask yourself whether we owe something better to our veterans, who are suffering catastrophic disabilities and PTSD in mind-numbing numbers, all to protect our access to an unnecessary supply of oil.

The question of “vested interests” only arises when the analysis is finished, and we’re left asking ourselves how fossil fuels have survived so long, given their deep deficiencies. How is it, for instance, that Republicans can’t talk about Climate Change, and simple solutions like carbon taxes are shunned, even though they’re (quietly) supported even by the most conservative of economists?

Duracomm

Nick G said,

In fact, renewables are better than fossil fuels when analyzed using physics, engineering and economics.

Good point, the fact that renewables are steadily gaining market share without the use of subsidies and mandates prove this.

You seem to be assuming that subsidies and mandates are necessarily a problem – I don’t think you’ll find support for this from reputable economists, even very conservative ones.

Again, do you agree that Climate Change is a serious problem? If so, don’t we have to fix the price incentive so that free markets can work properly, by taxing carbon or subsidizing non-carbon energy?

baffling

duracomm,

if you were given a clean slate to rebuild the energy and transportation infrastructure for the next 100 years, what would you do? build it for oil? or electrify it with renewables? something else? if oil is not your answer, then it is a “vested interest”.

Duracomm

Baffling asked

if you were given a clean slate to rebuild the energy and transportation infrastructure for the next 100 years, what would you do?

I am not ignorant enough to think anyone has the knowledge to do such a thing.

That is a fools errand mostly attempted by folks with no real world experience who are filled with equal parts of ignorance and hubris.

baffling

duracomm,

this is a perfectly legitimate question for anybody who thinks strategically. these types of questions are asked all the time in business. in essence, if you were not locked into legacy decisions, would the landscape be the same or different? and if different, is the cost of change worthwhile in the long term? your dismissal of such questions indicates either a laziness to consider such questions or a fear of the outcome.

we have redefined the industry status quo throughout history. tesla supplanted the DC grid with AC. analog went digital. horse and carriage replaced by automobile. canals to railroads. all these changed existing infrastructure and use. this is called progress, and requires strategic thinking.

baffling

kopits

“But that’s a whole different story than saying, for example, that we should walk away from $1.2 trillion worth of oil in the Alaskan Outer Continental Shelf.”

But how much of that $1.2 trillion goes into the extraction cost? So we are spending (wasting) how much money extracting oil for xx in profit. as those profit margins diminish, that becomes wasted money. this is what creates the drag on the system, too much money wasted to obtain x barrels of oil. the idea of the PTC and other policy tools is to move that extraction money into more useful areas with better LONG TERM prospects.

Steven Kopits

Of the $1.2 trillion of oil Shell envisions developing in the Alaskan Outer Continental Shelf, the expected revenue split would be as follows:

Cost to first oil: $50 bn (one 300 kbpd platform in the Chukchi Sea)

Additional cost to develop other platforms: $100 bn (3 x 300 kbpd platforms in Chukchi, 6 x 100 kbpd platforms in the Beaufort), paid from revenues

Profits to Shell (after-tax): $400 bn

Profits to Government (mostly federal right now): $650 bn (based on North Slope precedent, 62/38 split govt/operator)

Note that the returns to Shell are 8x, but over a 40 year period–not really a great return, considering the risks.

So there’s no subsidy here. Rather this is a whopping bonanza to the US government, worth about one year’s defense budget. Personally, I would have no qualms about allocating some of the Federal revenue to offshore wind, if that’s what it takes. A build-out of offshore wind on the Atlantic Coast (where it matters, for a number of reasons), would imply about 12 GW, with a subsidy on the order of $36 bn. This sum could easily be paid from OCS government revenues. I would call the program “Energy to Power”.

What are the risks? In particular, what are the odds of finding that much oil, and what is that estimate based on?

What’s the breakdown of the 62% govt split?

Steven Kopits

Nick –

There are all sorts of risks, but they fall into three broad categories:

Exploration Risk: So far, Shell has two half wells. We don’t know how much oil can be reasonably extracted. The value at risk to get this knowledge is on the order of $10 bn, of which $6 bn (including lease costs) will have been expended through 2014. This is normal exploration risk for Shell, and they understand the math on this topic.

Political Risk: Soup to nuts, from tax rates, to safety and environmental regulations, to let’s-sue-you-forever stuff. This is the biggest risk.

Logistics, cost overruns and delays: Operating in Alaska can be very challenging. Costs can balloon pretty easily. But the greater risk, in an irr sense, is delays. With a short operating season, it’s very easy to lose a year. Shell just did–costing about $1 bn–albeit that was directly as a result of political risk.

Duracomm

Ulenspiegel said,

You sell me it is ok that company A has robbed the consumer/taxpayer for decades and has used these resources to create a structure that suits it now, i.e. company A has used its gains to create a defense against potential competitors.

I would tax company A or give subsidies to company B. But this is only a cosmetic problem..

I am guessing that you are referring to the centralized power generation system that currently keeps the lights on.

Government initiatives are what put much of the current centralized system in place, example

It is naive to think that additional government initiatives (taxes and subsidies) will be anything more than a method for different companies to gain private profit at public expense.

That argument primarily benefits fossil fuel incumbents who (rightly) fear change.

Again, do you agree that Climate Change is a serious problem? If so, don’t we have to fix the price incentive so that free markets can work properly, by taxing carbon or subsidizing non-carbon energy?

Steven Kopits

I’ll be presenting on supply-constrained forecasting at Columbia University on Tuesday.

Chevron is explained by the Gorgon project (Shell probably has a similar project). If the capital expenditures are primarily (small) flows to maintain current fields or maintain exploratory operations, then a lumpy field project would distort these proportional figures. For example, Gorgon was never expected to produce until 2014 whereas the capital expenditures are all upfront (if they missed production deadlines, that would be another story). In addition, Gorgon is a “megaproject”, and (judging from the reporting) a much bigger expenditure than the typical oil field development. But there is no comparison between the cost per expected lifetime production of this project versus past projects, i.e. there may be a correspondingly higher lifetime production value capitalized at a single point in time (although I doubt it). A longer horizon would highlight the lumpiness of the capital expenditures and compare it to the declining production (which you’ve highlighted in other posts).

I agree with the general sentiment that oil and gas low-hanging fruit are depleted, but I find these graphs to be a little misleading.

Note that Chevron also has another LNG product off northwest Australia Wheatstone. So there are two big projects underway at once.

The big issue is how much nuclear will be used in Japan in the future? That is a significant determination of the viability of these projects.

Note that Gorgon was first discovered in 1981, so it has not been a fast process to develop the field due to it being essentially in the middle of

nowhere.

Really, you’re going to leave it at that?

Steve: I’m pressed for time this afternoon, and plan to write on another topic this weekend. Just hoping you’d pick up the ball here in the comments!

Touche!

So are we saying that they would have gotten a better return if they had invested in solar or wind? ;->

… or maybe not.

http://www.smh.com.au/business/carbon-economy/eu-move-to-drop-mandatory-renewable-energy-target-for-2030-irks-wind-solar-industries-20140124-31ccg.html

Bruce Hall,

that affects PV and offshore wind, the crucial question for utilities is whether or how onshore wind is affected: Onshore wind already produces cheaper than new coal, NG or nuclear power plants.

Or from a German POV, nobody plans to build new coal power capacity even when 2022 additional 8 GW nuclaer capacity will be gone. All added capacity until 2015 is legacy from the time before 2005, when almost everybody expected increasing demand until 2030. Therfore, each added GW onshore wind capacity eats away FLH of conventional power plants and erodes their economic base in a energy only market.

From discussion on other boards, the problem of oil companies is that they have no technological advantage when investing in wind or most other REs, they would be in the same situation as McDonald or Münchener Rück. 🙂

Can you give me one example of a wind power plant build without subsidies, PTCs, ITCs, or feed in tariffs? I keep hearing that wind is cost competitive, in which case, all public support should be discontinued.

Steven,

Are you really saying that you don’t think that Climate Change is a real problem? That’s the only justification I can see for such a question. After all, there’s plenty of coal in the world, and if we don’t care about it’s pollution (especially CO2), then we should just burn as much as we want, right?

On the other hand, if Climate Change really is serious, then it’s cost should be internalized into carbon, or non-carbon energy sources should be subsidized.

kopits, as soon as the oil industry pays back its shipping and military subsidy, they we can talk about removing the PTC from wind, solar, etc. we provide subsidy to industries who are not yet mature-you cannot make that claim about oil and yet they do get significant, even if indirect, subsidies.

What shipping subsidy? Product, crude and chemical tankers change hands at market rates. Here’s page on the various Baltic indices which measure, among other things, dirty and clean tanker rates. http://en.wikipedia.org/wiki/Baltic_Exchange

If anything, the Jones Act substantially raises the cost of shipping for US producers.

As for military costs, these are primarily related to the Persian Gulf. I have addressed those elsewhere.

As for military protection in the Persian Gulf (Strait of Hormuz):

Some 17 mbpd of crude, and I believe another 2.5 mbpd of product, move through the Strait daily. That’s more than 20% of global oil production.

Of this, equity oil for the oil majors (BP, Exxon, etc) is probably around 2 mbpd, depending on how you want to count. The rest is Saudis (9 mbpd); Kuwaitis, Iranians, Emirates, and Iraq. So the military presence in the Gulf overwhelmingly serves to protect the oil flows of the Gulf’s national oil companies.

Further, on the consuming side, only 11% of Gulf exports find their way to the US. Nearly 90% of Gulf exports flow to Europe, India, China, Japan and other countries.

If you want to get huffy about the matter, criticize the US government for subsidizing Gulf oil exporting countries and the consumers of the other major global economies. US producers and consumers are the least of it.

criticize the US government for subsidizing Gulf oil exporting countries and the consumers of the other major global economies.

I agree completely! I think there’s a pretty good case that the US has gone overboard in it’s interventions over the years in defense of the “stability” of the international oil market, starting with Roosevelt’s guarantee of the Saudi family’s control over the Arabian peninsula, and continuing with it’s intervention in Iran in 1954 which ended so badly in 1979. Unintended consequences…