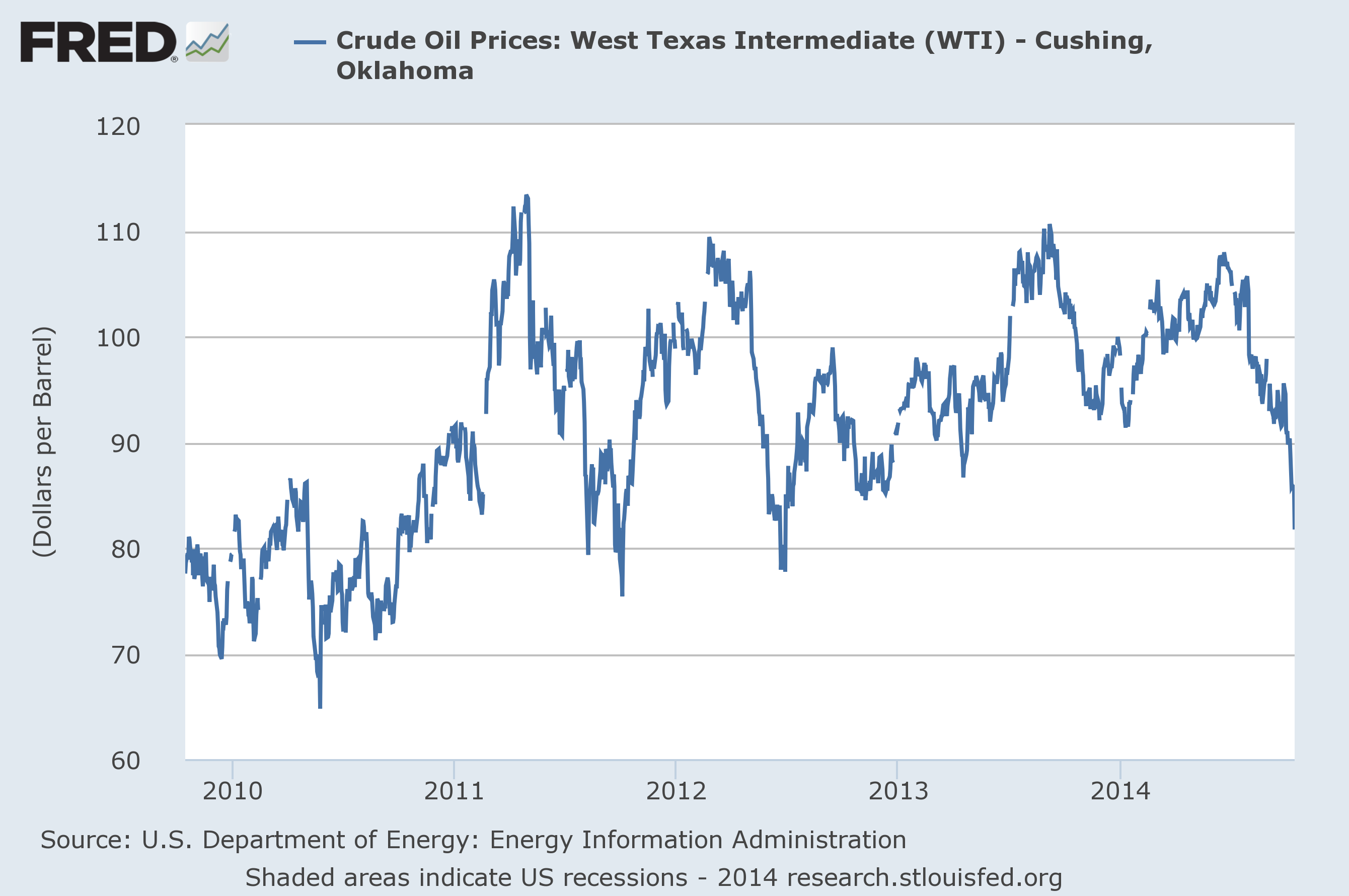

Oil prices (along with prices of many other commodities) have fallen dramatically since last summer. Some observers are waiting to see if Saudi Arabia responds with significant cutbacks in production. I say, don’t hold your breath.

Source: FRED.

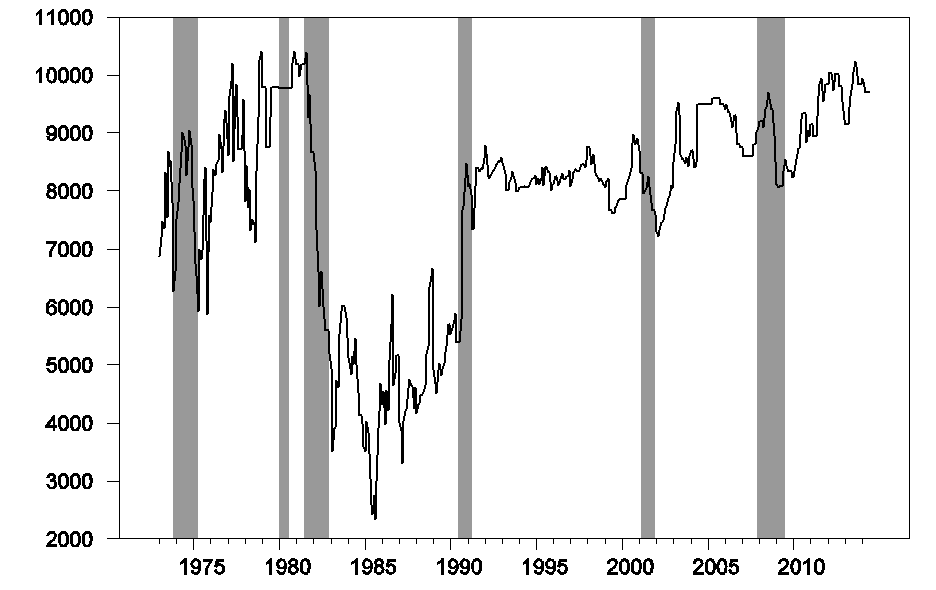

When oil demand fell in the 1981-82 recession, the Saudis cut production by 6 million barrels a day in an effort to soften the decline in oil prices. They also cut production in response to lower demand in the 2001 recession and the most recent recession. On the other hand, the kingdom boosted production quickly beginning in August 1990 and January 2003 in anticipation of lost production from Iraq in the two Gulf Wars. This historical behavior led many observers to believe that Saudi Arabia would always play the role of a swing producer to stabilize the price of oil.

Monthly crude oil production from Saudi Arabia, January 1973 to June 2014, in thousands of barrels per day. Data source: EIA. Shaded regions correspond to U.S. economic recessions.

But that’s hardly an accurate characterization of what happened during 2005-2007, when Saudi production declined even as prices skyrocketed. If that production decline was intentional, it was a dramatic departure from previous patterns. I think a better interpretation is that the market moves after 2005 became too big for the Saudis to control, and they gave up trying. I remain skeptical of the claim that Saudi Arabia is ever going to produce much in excess of 10 mb/d, regardless of what’s going on in the market.

Last week I discussed the three main factors in the recent fall in oil prices: (1) signs of a return of Libyan production to historical levels, (2) surging production from the U.S., and (3) growing indications of weakness in the world economy.

As far as Libya is concerned, the politics on the ground remain quite unsettled. It makes sense to wait and see if anticipated production gains are really going to hold before anybody makes major adjustments.

In terms of surging U.S. production, the key question is how low the price can get before significant numbers of U.S. producers decide to pull out. If world economic growth indeed slows, and if most of the frackers are willing to keep going strong even if the price falls to $80 a barrel, trying to maintain the price at $90 could be a losing bet for the Saudis. They’d be giving up their own revenue just in order to keep the money flowing into ever-growing operations in Texas and North Dakota.

And if some of the U.S. producers do move into the red at current prices, it’s in the Saudis’ longer-term interests to let that pain take its toll until some of the newcomers decide to pack up and go home. If U.S. production does decline, prices would quickly move back up. But if that happens after a shake-out, the next time there would be less enthusiasm for everybody to jump into the game if they always have to keep an eye on whether they might be undercut again. This may be less of an issue for the U.S. tight oil producers, who can move in or out much more easily than operations like deepwater or arctic, where there are huge fixed costs, long lead times, and a much bigger unavoidable loss if you gamble on prices always staying high.

And as for worries of another global economic downturn, so far they are only that– worries. If and when we see a downturn materialize, then I would expect to see the Saudis cut back production.

But until then it’s primarily a question of responding to surging output of U.S. tight oil. My guess is that Saudi Arabia would lower prices rather than cut production as long as that’s the name of the game.

And if it comes down to a game of chicken, I know who’s going to win.

Saudi Net Export Response to Rising Oil Prices

2002-2005 and 2005-2013

2002-2005

As annual Brent crude oil prices doubled from $25 in 2002 to $55 in 2005, Saudi net oil exports increased from 7.1 mbpd (total petroleum liquids + other liquids, EIA) in 2002 to 9.1 mbpd in 2005.

2005-2013

As annual Brent crude oil prices doubled from $55 in 2005 to the $110 range for 2010 to 2013, Saudi net exports have been below the 2005 rate for 8 straight years. In 2013, they net exported 8.7 mbpd, which was also their average net export rate for 2011 to 2013 inclusive.

In my opinion, the most likely scenario for 2005 to 2013 was that the Saudis were unable to match or exceed their 2005 net export rate of 9.1 mbpd, at least not without doing unacceptable long term damage to their oil fields.

Note that Saudi net exports did show a large decline from 8.8 mbpd in 2008 to 7.6 mbpd in 2009, as annual Brent crude oil prices fell from $97 in 2008 to $62 in 2009, which was (so far) the only large year over year decline in annual oil prices since the 2000 to 2001 decline.

I suspect that the Saudis have been justifiably concerned about rising US production. However, that they have been unable or unwilling to match or exceed their 2005 net export rate of 9.1 mbpd, they have been waiting for a material decline in oil prices, so that they could maintain their production and net export rates in the face of declining demand, as a way to hurt competitors, especially high cost tight/shale producers. Also, the Saudis are past their high demand summer season, which frees up more oil for export during the lower demand months.

However, a longer term issue to consider is depletion. By definition, it’s not whether the Saudis have depleted their remaining post-2005 CNE (Cumulative Net Exports), the question is by how much?

The Saudi Export Capacity Index (ECI, the ratio of production to consumption) Ratio fell from 5.7 in 2005 to 4.0 in 2013. Based on the eight year rate of decline in their ECI Ratio, I estimate that their post-2005 CNE are on the order of 60 Gb (billion barrels), with 25 Gb having been shipped from 2006 to 2013 inclusive, putting their estimated post-2005 CNE at about 40% depleted in only 8 years.

The Six Year Case History consists of the six major net exporters that hit or approached zero net exports from 1980 to 2010, excluding China. Based on the initial 1995 to 2002 rate of decline in their combined ECI Ratio, their estimated post-1995 CNE were 9.0 Gb. The actual value turned out to be 7.3 Gb.

Here is the critical Net Export Mathematical Fact of Life: Given an inevitable ongoing decline in production in a net oil exporting country, unless they cut their domestic consumption at the same rate as the rate of decline in production, or at a faster rate, the resulting net export decline rate will exceed the production decline rate, and the net export decline rate will accelerate with time. It’s a mathematical certainty.

Perhaps, the U.S. should expand capacity for the Strategic Petroleum Reserve and buy oil when it’s well below $100 a barrel.

“The Strategic Petroleum Reserve (SPR) has the capacity to hold up to 727 million barrels. As of October 2014, the inventory was 691.0 million barrels. This equates to about 37 days of oil at 2013 daily U.S. consumption levels of 18.5 million barrels per day or 70 days at 2013 daily U.S. import levels of 9.9 million barrels per day.

At $102 a barrel as of February 2012, the SPR holds over $26.7 billion in sweet crude and approximately $37.7 billion in sour crude (assuming a $15/barrel discount for sulfur content).

The total value of the crude in the SPR is approximately $64.5 billion. The price paid for the oil is $20.1 billion (an average of $28.42 per barrel).”

Bush 43 asked Congress to double the capacity of the Strategic Petroleum Reserve (of course, that didn’t happen).

A couple of corrections/clarifications to previous post:

And a couple of charts:

Following is a Six Country Case History* chart showing the normalized values (1995 values = 100%) for their combined production, net exports, ECI Ratio and remaining post-1995 CNE, by year, from 1995 to 2002. Note the correlation between a declining ECI Ratio and the rapid rate of decline in post-1995 CNE:

http://i1095.photobucket.com/albums/i475/westexas/Slide2_zps55d9efa7.jpg

Following is a Saudi chart showing the normalized values (2005 values = 100%) for their combined production, net exports, ECI Ratio and remaining post-2005 CNE, by year, from 2005 to 2012. Note the correlation between a declining ECI Ratio and the rapid rate of decline in estimated post-2005 CNE:

http://i1095.photobucket.com/albums/i475/westexas/Slide21_zpsd1963fe3.jpg

*The major net exporters that hit or approached zero net exports from 1980 to 2010, excluding China.

Good post, I agree. The broad majority of tight oil will remain profitable at lower oil prices. Some of the best areas of mckenzie county in Nodak break even at 21/bbl. This will only get better as supply chain and logistics continue to evolve/mature to support bigger and bigger frac jobs.

Maintaining production in the face of lower prices, may weaken shale production in the short run but doesn’t stop the secular increase in US shale prod. Seems like a very open ended strategy for the Saudis to commit to, given the impossibility to ever achieve a decisive victory. Their budget breakeven prices for oil are already bouncing around to $90-100 level and domestic consumption continues to grow at a unconstrained clip

A couple of news items:

Economist: The sword unsheathed

Protests break out after a Shia cleric is sentenced to death

http://www.economist.com/news/middle-east-and-africa/21625868-protests-break-out-after-shia-cleric-sentenced-death-sword-unsheathed

Saudi oil pipeline briefly set alight after shots fired at patrol

http://www.reuters.com/article/2014/10/18/saudi-oil-fire-idUSL6N0SD0GZ20141018

And a recommended book:

On Saudi Arabia: Its People, Past, Religion, Fault Lines – and Future

http://www.amazon.com/Saudi-Arabia-People-Religion-Future-ebook/dp/B007MDK5GM/ref=sr_1_1?ie=UTF8&qid=1413751560&sr=8-1&keywords=on+saudi+arabia

Book Description

Publication Date: September 18, 2012

FYI, an interesting book about the Saudis is John R. Bradley’s Saudi Arabia Exposed: Inside a Kingdom in Crisis. He was hired to work by a Saudi publication and was accredited as a Saudi journalist, which allowed him free travel around the country.

Let’s keep in mind that supply was entering the market at a 4 mbpd/ year pace during the last several months. That’s a big number.

Here’s my take on the matter. http://www.prienga.com/blog/2014/10/18/oil-demand-hasnt-collapsed

As you noted, the question is, what happened in the third quarter? Brent averaged $109 in the first half of 2014 (averaging $112 in June), and the decline in the Brent price really started to speed up in August.

Through June, the EIA shows that global Crude + Condensate (C+C) averaged 77 mbpd for 2014. If we subtract out estimates for rising condensate production, I suspect that we have seen little or no increase in actual global crude oil production (45 and lower API gravity crude oil) through the first half of 2014, versus the 2005 annual rate.

The following chart shows normalized global gas, NGL and C+C production from 2002 to 2012 (2005 values = 100%).

http://i1095.photobucket.com/albums/i475/westexas/Slide1_zps45f11d98.jpg

The following chart shows estimated normalized global condensate and crude oil production from 2002 to 2012 (2005 values = 100%). I’m assuming that the global Condensate/(C+C) Ratio was about 10% for 2002 to 2005 (versus 11% for Texas in 2005), and then I (conservatively) assume that condensate increased at the same rate as global gas production from 2005 to 2012, which is a much lower rate of increase in condensate (relative to the increase in gas production) than what we saw in Texas from 2005 to 2012.

http://i1095.photobucket.com/albums/i475/westexas/Slide2_zpse294f080.jpg

“Vehicle Miles Traveled: A Structural Change in Our Behavior:”

http://www.advisorperspectives.com/dshort/updates/DOT-Miles-Driven.php

Excellent post. Thanks for the link.

There really are no signs that weakening demand is causing oil prices to slide. That appears thought to be residual apprehension from the recession. James is right that Libyan production, an extra 700,000 barrels, since the start of this summer is causing the current slide in prices. He is also correct that lower prices do not necessarily help SA.

Is there any hard evidence (tankers leaving terminals, for example) that Libya has really ramped up production so drastically? All I can see is the oil minister, who’s in a hotel in Tobruk, throwing production numbers around, while the oil ministry itself is in the hands of islamists. Given the turmoil in the country it’s very difficult to know what’s really going on, and given the vested interests of the government in exile, perhaps it would be wise to treat their claimed production figures skeptically?

Arctic, not artic.

Thanks! Fixed the error.

Saudi’s know our hyperbolic production decline curve will bite us in the assets

There is no correlation between vehicle miles driven and oil price, there is no correlation between demand and oil price :

http://www.advisorperspectives.com/dshort/updates/DOT-Miles-Driven.php

Accept that James, once and for all.

I’m puzzled by this comment.

1st, I don’t see any reference by James to VMT.

2nd, the article you reference says there’s a weak correlation, not none at all.

3rd, Young people are the primary cause of declining per capita VMT. if you include a recognition by young people of the external costs of oil (climate change, pollution, and oil wars), you’ll see that part of the reason for their declining VMT is indeed a relationship between demand and overall cost.

SA announced a cut in oil production today.