Yesterday I was at the 31st annual NBER conference on macroeconomics (along with fellow blogger Mark Thoma). Among the many interesting contributions was development of an extended data set on 25 different indicators for 17 advanced economies going back to 1870 by Jorda, Schularick and Taylor (2016).

The authors described one of their findings as a “financial hockey stick”. After nearly a century of stability, loans by banks to the nonfinancial sector began after 1950 to grow systematically faster than GDP around the world.

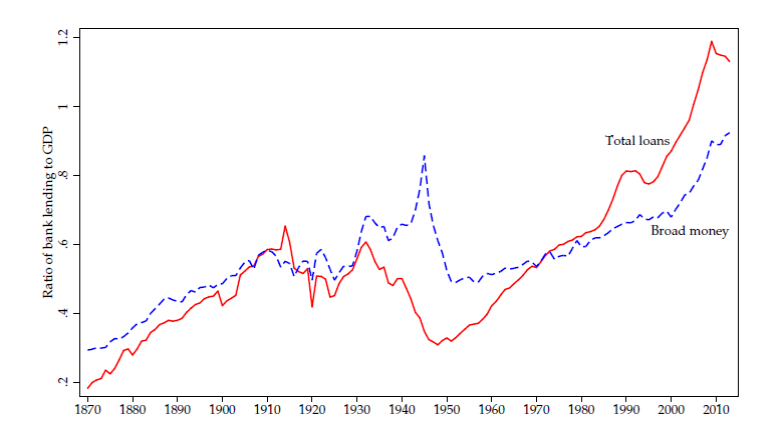

Average ratio of bank loans to the non-financial private sector to GDP across 17 advanced countries (in red) and ratio of M2 to GDP (blue). Source: Jorda, Schularick and Taylor (2016).

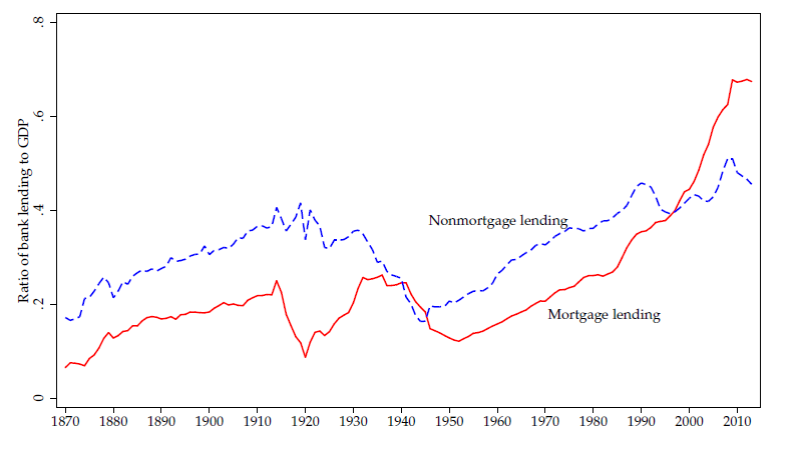

This growth in credit was concentrated in mortgage loans as opposed to unsecured lending to businesses.

Average ratio of mortgage lending to GDP (red) and for other lending (blue). Source: Jorda, Schularick and Taylor (2016).

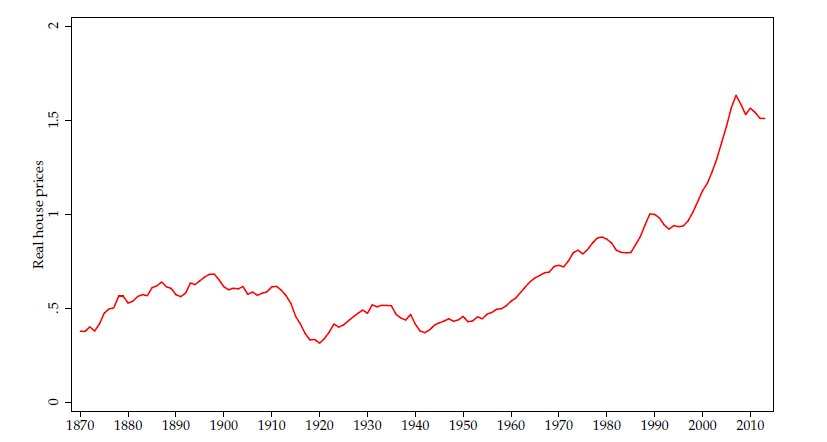

This “hockey stick” in mortgage lending was accompanied by a similar pattern in real house prices. These too had been largely stable for nearly a century. Since 1950, house prices have grown faster than inflation around the world.

Average house price deflated by CPI across 14 advanced countries. Source: Jorda, Schularick and Taylor (2016).

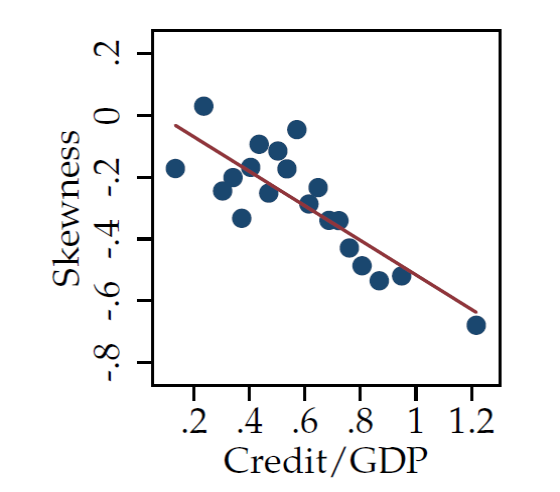

The authors find that as economies have become more leveraged, the standard deviation of output growth has become smaller, consistent with a phenomenon that has been described as the Great Moderation in the United States since 1985. Interestingly, however, the standard deviation of stock prices has increased. They also find that the skewness of GDP has become more negative– big movements up have become more subdued relative to downturns.

Vertical axis: skewness of GDP within country i over a 10-year period. Horizontal axis: credit/GDP for that country over that period. Data summarized in terms of 20 bins. Source: Jorda, Schularick and Taylor (2016).

At a basic level, our core result– that higher leverage goes hand in hand with less volatility, but more severe tail events– is compatible with the idea that expanding private credit may be safe for small shocks, but dangerous for big shocks. Put differently, leverage may expose the system to bigger, rare-event crashes, but it may help smooth more routine, small disturbances.

Government has subsidized and forced riskier loans on lenders and then when lenders lose on riskier loans, government blames lenders. So, recoveries have become weaker, until lenders recover.

“Government has subsidized and forced riskier loans on lenders ”

the government has not forced riskier loans on lenders. you keep repeating this drivel ad nauseum. it sounds like a hack.

Even you wouldn’t make risky loans on your own to go broke. So, don’t give me more nonsense.

“It is certainly possible to find prime mortgages among borrowers below the median income, but when half or more of the mortgages the GSEs bought had to be made to people below that income level, it was inevitable that underwriting standards had to decline. And they did. By 2000, Fannie was offering no-downpayment loans. By 2002, Fannie and Freddie had bought well over $1 trillion of subprime and other low quality loans. Fannie and Freddie were by far the largest part of this effort, but the FHA, Federal Home Loan Banks, Veterans Administration and other agencies–all under congressional and HUD pressure–followed suit. This continued through the 1990s and 2000s until the housing bubble–created by all this government-backed spending–collapsed in 2007. As a result, in 2008, before the mortgage meltdown that triggered the crisis, there were 27 million subprime and other low quality mortgages in the US financial system. That was half of all mortgages. Of these, over 70% (19.2 million) were on the books of government agencies like Fannie and Freddie, so there is no doubt that the government created the demand for these weak loans; less than 30% (7.8 million) were held or distributed by the banks, which profited from the opportunity created by the government. When these mortgages failed in unprecedented numbers in 2008, driving down housing prices throughout the U.S., they weakened all financial institutions and caused the financial crisis.”

source?

http://www.theatlantic.com/business/archive/2011/12/hey-barney-frank-the-government-did-cause-the-housing-crisis/249903/

wallison and his “analysis” was clearly at odds with the consensus of the FCIC report. why do you take the lone dissenter and not the rest of the FCIC members as accurate? As i recall in the report, the conclusion was the Fannie/Freddie subprime mortgage pool performed better than the subprime pool held by the private banks. wallison conveniently gives a pass to the most egregious players in the mortgage crisis-the private sector mortgage originators and securitizers. in doing so, he really loses all credibility in his analysis. you need to remember, his complaints against the government were for policies that had been in effect for over a decade without creating a problem. the problems began when the private sector decided to supercharge their involvement. at that point, the system imploded. peak, you need to find more intelligent and unbiased sources of information, or else you will continue to repeat those same false arguments ad nauseum.

PeakTrader’s favorite source is AEI. Here is the link:

http://www.aei.org/publication/hey-barney-frank-the-government-did-cause-the-housing-crisis/

My favorite sources can’t be disputed. For example, the New York Times couldn’t dispute Congressional action and the data. However, it tried to paint a liberal Republican as a conservative. And, normally, I have more faith what moderates say than extremists. Moreover, when an extremist doubts his actions, like Barney Frank, that just further supports what the moderates said.

There are so many problems with Wallison it is hard to take him seriously. He just makes up his own definitions, so of course things fit his explanations. Anyway, thanks for at least giving us your source. Now you dont have to be taken seriously.

Steve, there are so many problems with your statement it’s hard to take you seriously. You just make things up. So, of course, it all fits your explanation. Anyway, thanks for giving us your statement. Now you don’t have to be taken seriously.

peak, wallison is extremely cavalier about what he refers to as subprime, and then he implies that all subprime was of dubious quality. he then makes his arguments from ideology-something you know well. a low income borrower who gets a mortgage in a low cost neighborhood is not the problem if they can pay the mortgage, although he implies this person is subprime garbage. the subprime garbage was the no document loans for the multiple condos in downtown miami. these were not hud, fannie, freddie, etc loans. these were private sector loans. not all subprime is equal, and this bears out in the default rates of the agencies versus the private sector-they were different. you and wallison do not want to acknowledge this reality.

It was government policy borrowers were able to borrow for homes they couldn’t really afford, investors took risks for returns and potential losses, and lenders were the intermediaries making more loans. Government created a bubble before the 2007-09 recession.

“It was government policy borrowers were able to borrow for homes they couldn’t really afford”

peak, your statement is false. this is why you lack credibility in these discussions. you promote falsehoods as truth, and then make arguments based on those falsehoods. alt-a and no document loans were not part of government policy. they were constructs of the private sector mortgage business. as i have told you in the past, go read the big short and educate yourself on the mortgage business of the bust, as you clearly are not educated on the details of the mortgage bust.

Baffling, you’ve been watching too many movies and believing what politicians, who have all day blaming others, say. I’m sure, you’ll keep trying to get that square peg in the round hole.

peak, actually it is a book that i read. the movie takes too many shortcuts. but please explain to me what was inaccurate about the book? ahhh, that it right. you never read it (or even saw the movie). you just assume it is inaccurate, because that fits your world view. as i said, you have demonstrated a complete lack of knowledge on what actually happened leading up to the financial crisis. educate yourself please.

i actually lived in the supercharged real estate world of florida prior and post real estate bust. i saw it first hand. i rented a condo from a real estate agent, who happened to own about 5 different properties. she was foreclosed on all of them. the government was not the entity which pushed those mortgages through-and she would not be considered one of “those” poor people being pandered to by fannie and freddie. she had private sector mortgages and was massively over leveraged. she collected my rent until i moved out, then the property went into foreclosure. the reality of the financial crisis resulting from the real estate bust is much different then your ideology leads you to believe.

so when you say “Baffling, you’ve been watching too many movies and believing what politicians, who have all day blaming others, say. ”

the reality is quite the opposite. i have a pretty clear understanding of what actually happened. your conservative talk radio infomercials have led you astray.

So, everything you believe is based on one book, a Hollywood movie, and a real estate agent, who bought too many properties.

I worked in the financial industry, including commercial banks, along with passing the comp exams in Money & Banking, in grad econ.

what i know, not what i believe, is based on a bit more than a movie, book and real estate agent. i have spent a fair amount of time educating myself on the financial crisis from an investors perspective. but i will ask you again, what was wrong in the michael lewis book? i find it amazing you could have such a strong education and work background in banking, and be blind to what actually happened? or were you one of the fools in the banking sector that led us to the crisis? that would explain alot of the denial and scapegoating away from the banking sector…

You need to remember that in 2004, Bush was pushing the “Ownership Society”. Fannie and Freddie ‘weren’t doing enough’ according to Bush.

“Yet the Federal government and the American taxpayer should not undertake this effort alone. The real estate and mortgage finance industries have benefited greatly from government policies that supported greater homeownership. They share an interest in ensuring that all families have access to the American Dream. The government-sponsored corporations created to increase the liquidity of mortgage markets, so more capital would be available for mortgage loans, are supposed to lead the market in reaching underserved populations. While these corporations have increased their commitments to these efforts, they lag behind private lenders in this regard, according to government studies. The Administration will revisit the regulatory goals for these corporations’ purchases of affordable housing loans, which are set to expire in 2003. The federal government should demand more and should hold such publicly-chartered corporations accountable for better performance. ”

Link: http://georgewbush-whitehouse.archives.gov/infocus/homeownership/homeownership-policy-book-background.html

That 2001 statement basically only states homeownership is good and should be fair. By 2004, the Bush Administration tried to slow the amount of risky loans, while Barney Frank and others ramped up risky loans. In 2007, when the crisis began to emerge and unfold, and it was too late, only then Congress decided there were way too many risky loans.

the bad loans were on the books of lehman, merril, goldman, citi, boa, etc. the shoddy insurance on those pools of mortgages were on the books of aig, morgan, goldman, citi, etc. notice those are all private sector enterprises. and the government did not force any one of them to take on their risky loans-they did it because they believed they could make profits, but were inadequate in their risk assessments.

H.R. 3703 and its Effects on Government Sponsored Enterprises

By Peter J. Wallison | House Subcommittee on Capital Markets

(September 06, 2000)

The GSE form–at least as it is embodied in Fannie Mae and Freddie Mac–contains an inherent contradiction. It is a shareholder-owned company, with the fiduciary obligation to maximize profits, and a government-chartered and empowered agency with a public mission. It should be obvious that it cannot achieve both objectives. If it maximizes profits, it will fail to perform its government mission to its full potential. If it performs its government mission fully, it will fail to maximize profits.

[T]he incentives of their managements [are] to increase their own compensation.

This has direct consequences in the real world. Since 1992, Fannie and Freddie have had an obligation to assist in financing affordable and low income housing. Obviously, doing so would be costly, and would thus reduce their profitability. Studies now show that their performance in financing low income housing—especially in minority areas—is far worse than that of ordinary banks. In other words, despite the fact that Fannie and Freddie receive subsidies to perform a government mission—in this case support of low income housing—their need for and incentives to retain a high level of profitability is an obstacle to their performance.

Also, it should be remembered who controlled Congress and the White House in 2004. Somehow a minority congressman controlled both houses of Congress and the POTUS. Quite a feat.

The Bush Administration tried to regulate Fannie and Freddie in 2003!, but was filibustered by Sen Dodd and Rep Frank (funny how politics actually work):

http://www.nytimes.com/2003/09/11/business/new-agency-proposed-to-oversee-freddie-mac-and-fannie-mae.html

I doubt if “they” were inadequate in their risk assessments. These investors knew quite well that it would be a major dump for the major “fall-guy”. The majority of US citizens would have to pickup the default. The burden of responsibility has been passed on to the usual pawn, the general public.

That great anomoly that will have to deal with the consequences over the next 50 years or more. Just the typical pass-the-buck game, business as usual…..

actually, there were plenty of folks who were completely ignorant in their risk assessments. aig was a prime example. some players did act nefariously with knowledge, but many, many private sector players were simply ignorant of the risks they were accumulating. lehman went under for the same reason. they may have all thought they could pass the buck if things went bad, but they did not realize the severity of the situation would effectively lock them into their trades.

Certainly government encouraged subprime lending more than they should, in their defense these loans had not been performing badly – borrowers did have jobs.

But banks went far beyond subprime because they ran out of regular subprime so, actively encouraging liar loans, and of course banks would never have gone there if they held what they knew was toxic on their books, they had to sell it. And of course buyers would never have knowingly bought liars loans, the banks had to fraudulently state the loans were good.

And it was the rapid default on liar loans that stopped residential construction, spreading to other subprime, and then prime borrowers, too, as the recession spread.

Fraudulent bankers are now paying massive penalties, 100b so far, on account of their countless frauds, sadly the penalties are far less than the damage to millions across the country, indeed far less than their corrupt profits.

Lenders knew Congress wanted to create a giant social program and lenders received Congress’s blessing. The policy was forced upon them anyway. It was perfectly rational for lenders to turn a bad policy into their advantage. It turned out like taking candy from a baby. When the politicians, who pushed this policy, since the ’90s, realized they’d actually have to pay for the giant social program, it was too late. So, given they are politician-lawyers, they went after the lenders.

The idea that ‘the policy was forced upon them..’ is a laugher to anyone that follows financial regulation. So we have the worst of both worlds now. Citizen United allows massive influence peddling but once the ‘efficient’ markets collapsed many want to blame it on it on government.

If I subsidize your risk taking does it make your risk taking my fault? Of course not. There are plenty of policies that the private sector resists tooth and nail. I know of no evidence that the policies being discussed here were among those.

Typically, lenders don’t make risky loans, because they don’t want to lose money.

You can thank your generous government for the large amount of risky loans.

during the financial crisis, there were large numbers of commercial real estate loans that went bust. i suppose the government was behind those risky commercial loans? or today, the oil patch has created large numbers of bank loans which are extremely troubled. i suppose the government was behind those loans as well. because as we know, the private sector would not make risky loans and lose money. it must be the governments fault, somehow and someway!

A steep economic downturn in itself will increase bad debts. You can thank government for creating a worse downturn that affected the entire macroeconomy, including commercial real estate. The U.S. oil boom was needed for declining oil production in other countries. The free market achieved its objected – more oil at lower prices.

classic. commercial real estate AND oil loans failed because of the government!

Mr. Hamilton, the authors’ conclusion only leaves me on edge. But that last graph interest me.

The economy tends to be vigorous when the private/public debt ratio is low, and sluggish when the ratio is high.

Arthurian: Here is a question for you. How do you rip the blindness off the eyes of academics whose bread is buttered in such a way that if they truly saw the utter falsity of the debt-slave paradigm they espouse, and if they had even a modicum of integrity, they in all good faith could no longer stay in academia?

One of the fall outs of increased leverage is surely lesser volatility but as the author points out, the systemic risk rises. This rise of systemic risk is actually attributable to horizontal intermediation, where one agent is passing off the risk to the other just like a clearinghouse. Dis-aggregation of such risk although attempted by the regulatory agencies never saw the light of the day.

Count me deeply skeptical that private real-sector indebtedness reduces growth volatility. Concluding so from correlation of one event each of decreased volatility and increased indebtedness seems rather unscientific.

Mr. Hamilton, the PDF you linked is most interesting.

It took me a few days to figure out why your last graph caught my eye. Jorda, Schularick and Taylor come very close to saying that the growth of debt *caused* a slowing of economic growth. If growing debt caused GDP growth to slow, then by Okun’s law debt caused unemployment to increase. If this is true, the growth of debt changed the Phillips curve.

If that is true, then the story of the expectations-augmented Phillips curve is not entirely correct. This is huge.