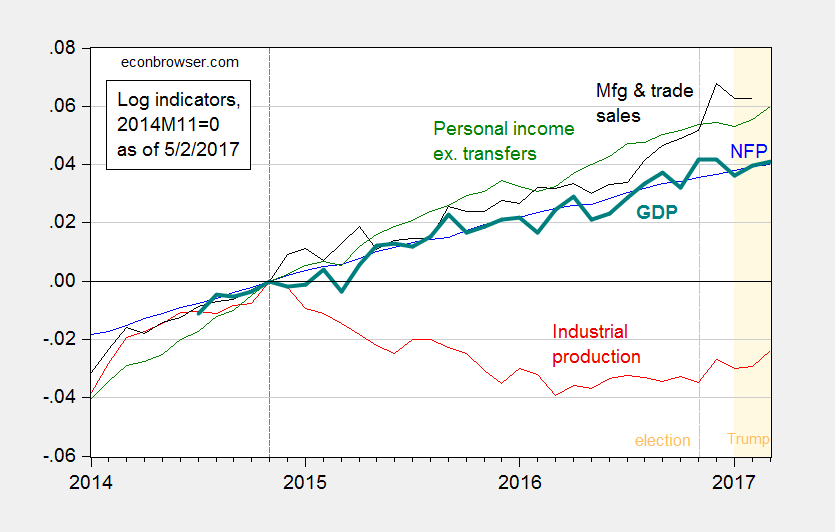

Reader Steve Kopits writes “I am thinking the business cycle rolls over right here.” Here are five key indicators that the NBER Business Cycle Dating Committee have consulted in the past, as of today.

Figure 1: Log nonfarm payroll employment (blue), industrial production (red), personal income excluding transfers, in Ch.2009$ (green), manufacturing and trade sales, in Ch.2009$ (black), and monthly GDP, in Ch.2009$ (bold teal), all normalized to 2014M11=0. Source: BLS, Federal Reserve, BEA, and Macroeconomic Advisers (17 October release), and author’s calculations.

As of March, the indicators (save sales, for which data was not available) were still rising — with industrial production still below prior peak levels. So, as of today reported data for March suggest no recession (with the caveat that these data are subject to revision). That conclusion does not speak to May 2017 — hence I will not “pull an Ed Lazear” and declare “no-recession” now (or a “Don Luskin” for that matter).

On a separate matter, I note that recession prognosticator David Malpass, who predicted a recession in 2012, and no recession 2008 has been nominated by President Trump to be Undersecretary of the Treasury for International Affairs.

Agree, Prof. Chinn. We are not rolling over yet. But bad reports by the big automakers today continues a 4-month slide. Combine that with sliding oil prices in the last month, and those aren’t good signs, even if it’s flattening out inflation

no one have cristall ball…..

overconfidence on Trump Plan still on soft data. https://pbs.twimg.com/media/C-RP1IFW0AIFnNa.jpg

but hard data after 02/2017, sameone soon and sameone after, go down.

AND sign of consumer stress is all around https://pbs.twimg.com/media/C-vY4kQUwAArpNu.jpg:large

income is credit and credit is income: higher cost of living covered by debt, but student loans, auto loans, credit card loans, healthcare costs prob all impacting consumer discretionary & retail https://www.ft.com/content/10c2691c-2c60-11e7-9ec8-168383da43b7

I don’t know that we get an NBER-style recession here. I think the Japanese variant is more likely. A soft negative quarter, then a better positive quarter, then near zero, then a bit negative, then GDP up better. This is the kind of pattern we’ve seen from Japan since 2000. No real conviction on GDP in any direction, ostensibly economic under-performance, but near full employment the whole time. It’s a productivity and demographic issue, not a business cycle issue.

I’d add it’s for this reason that we need to see a full US balance sheet, including health and human capital. I could argue that maybe 2/3 of increased health spending has not increased underlying GDP at all. It’s prevented GDP from falling. The healthcare sector keeps lots of people busy, but is doesn’t make us better off. It prevents us from being worse off. In that kind of model, you could get poor productivity and GDP performance, and yet be running at full employment. That’s what I mean by a Retirement Recession. It flattens out the business cycle: shallow expansions and weak contractions, but everybody has a job, directly or indirectly, taking care of their aging parents.

The sudden, sustained, and substantial downshift to 2% real growth, since 2009, cannot be explained by demographics. And, without the smaller trade deficits and the fracking boom, growth would’ve been even worse. This is a policy induced depression. Highly accommodative monetary policy and NAIRU don’t reflect full employment. We can get to long-run 3% real growth.

its hard to see why demographics is not a significant contributor. please explain why demographics does not play a role?

I really want to understand what goes on inside your head that forces you to repeat the same lie over and over and over and over again.

U.S. GDP grew by 1.8% in 2007 and contracted by 0.3% in 2008. There has been a marked slowdown in GDP since 2000, and it was absolutely accelerated by demographics.

The average annual change in working-age population since 2008 was 0.5% versus an average of 1.2% in the prior 30 years. https://fred.stlouisfed.org/graph/fredgraph.png?g=dAzl

In 2001-07, real GDP expanded at a 2.69% average annual rate. The expansion was built upon the economic boom of 1982-00 and the mild 2001 recession. Over the entire long boom, in 1982-07, it expanded at an average annual rate of 3.37%. It should be noted, by the mid-2000s, trade deficits reached 6% of GDP, which subtracted from GDP.

Demographic shifts take place slowly, not suddenly. A good proxy to measure demographic shifts may be the labor force participation rate of women, which peaked around 2000 and has been in a slow decline.

Per usual, you argue in non sequiturs.

And the 2001 recession, in retrospect, was not very mild. Labor for participation rate never recovered after it, GDP per capita was flat for 2 years after it ended, and almost every other employment indicator was worse than previous recessions. http://digitalcommons.ilr.cornell.edu/cgi/viewcontent.cgi?article=1194&context=key_workplace

You just seem to consistently skew every date and every piece of data to fit your “it’s all Obama’s fault” narrative. It’s very frustrating.

“Demographic shifts take place slowly, not suddenly.”

if you have a bulge in your demographics (baby boomers) coupled with a significant economic event (financial crisis), it is not hard to imagine a much more dramatic rather than slow change occurring. the retirement cycle of many boomers was effectively compressed. late 50’s and early 60’s workers with little to no legitimate technology skills effectively all retired at once. i would imagine there were plenty of older folks in the financial field that fit this description, because their tech skill was internet surfing.

Of course, it’s frustrating for you to create the narrative the 2001 recession was one of the worst recessions, because it isn’t true. Your many other false narratives don’t fit either. For example, in the late ’90s, actual output exceeded potential output and the country was beyond full employment. Consequently, many people not normally in the workforce were hired and many of them didn’t come back into the workforce during and after the recession. Per capita real GDP was generally flat in 2001 and the unemployment rate didn’t rise much. It was one of the mildest recessions in U.S. history.

I’ve explained why your theory is wrong before based on data. Yet, you continue to cling to it. The last of the Baby-Boomers will reach 65 in 2029, and over this weak recovery, many older workers kept their jobs longer. Job growth was slow to absorb the jobs lost in the recession and to keep up with population growth. The policies in 2009 and later resulted in many unemployment extensions, more people going on disability, or being forced into early retirement. The slower growth than otherwise, and for this long, from the severe recession, in itself, destroyed some potential output, along with the slow shift in demographics. Slower growth is inevitable. However, the output gap still hasn’t been closed after eight years! It has been a waste, like I’m sure I’ve wasted my time again explaining part of it to you.

“or being forced into early retirement. ”

this is a result of demographics, as i stated previously.

“For example, in the late ’90s, actual output exceeded potential output and the country was beyond full employment. ”

this means you should be careful in considering this era when estimating what the growth trend should be today. in essence, the current growth trend should be slower than what was observed in the past. your argument for the output gap intentionally does not include this item. and that is why you are wrong.

Well, the slow down in labor force growth does explain a sizeable share of the slow down in GDP. It does not necessarily explain the collapse of productivity growth, which from 2000-2010 was 2.7% per annum, and is forecast at 1.2% per year from 2010-2020. (The actual is 0.6% from Q1 ’12 to Q3 ’16.) I don’t know that we understand productivity growth, but the last time it was so poor was during the first two oil shocks. Hmmm.

https://www.bls.gov/opub/btn/volume-6/below-trend-the-us-productivity-slowdown-since-the-great-recession.htm

I don’t think targeting 3% GDP growth is unreasonable. However, the administration has to decide its priorities. Are they liberal, ie, growth related? Are they conservative, based on tariffs and immigration restrictions which protect US workers but limit growth? Are they egalitarian, blowing out the budget to fund those with pre-existing conditions? All of these may be legitimate goals, but they are contradictory.

In politics, ideology is more or less the objective function. Trump’s problem is that he has no concept of agency, that is, no dominant ideology. The man is all principal, no agent. Lacking an ideology, he also lacks guidance. Now what does Trump say? “I’m a nationalist and a globalist.” So which one is it? These imply two different ideologies which lead to different policies.

And this also explains the in-fighting. “Hey, I’ll eat Chinese or Mexican.” So what are you going to eat? That’s simple. What everyone else wants to eat. You’re going to go with the flow. So the battle is really between everyone else — let’s call it the senior WH staff, the agencies’ leadership, and Ryan + McConnell. They will decide what you’re going to have for dinner after lots of infighting amongst themselves.

So by all means, let’s target 3% growth. That would be my preference. But then let’s do it seriously, and work towards that goal with the understanding that we may not address other potentially desirable objectives.

I stated before, in many ways, lower real wages, in itself, causes lower productivity. However, here’s more info:

http://www.nber.org/digest/nov05/w11354.html

Per my point:

https://www.wsj.com/articles/slumping-car-sales-are-latest-data-to-rattle-bets-on-growth-1493742225

http://mam.econoday.com/byshoweventfull.aspx?event_id=265&cust=mam

Motor vehicle sales are good indicators of trends in consumer spending and often are considered a leading indicator at business cycle turning points. One should note that manufacturers do not break out vehicle sales to businesses, which are a smaller but still significant percentage of the monthly total.

https://www.advisorperspectives.com/dshort/updates/2017/04/17/the-big-four-economic-indicators-march-real-retail-sales

Mixed bag.

We are in the 7th or 8th recovery year depending on your perspective, so it’s not unreasonable to expect some flattening of the economy; however…

http://projects.wsj.com/econforecast/#ind=gdp&r=20

Economists mostly see smooth sailing this year.

Thanks Menzie and Steven. Thanks Steven for your comment on the other blog post.

President Trump has clearly pushed down potential GDP growth. Though the magnitude of the impact may not be easily noticed. Cancelling the TPP was so incredibly stupid.

I expect slower US growth going forward. I also expect the cacophony of lame finger pointing to increase.