Three times.

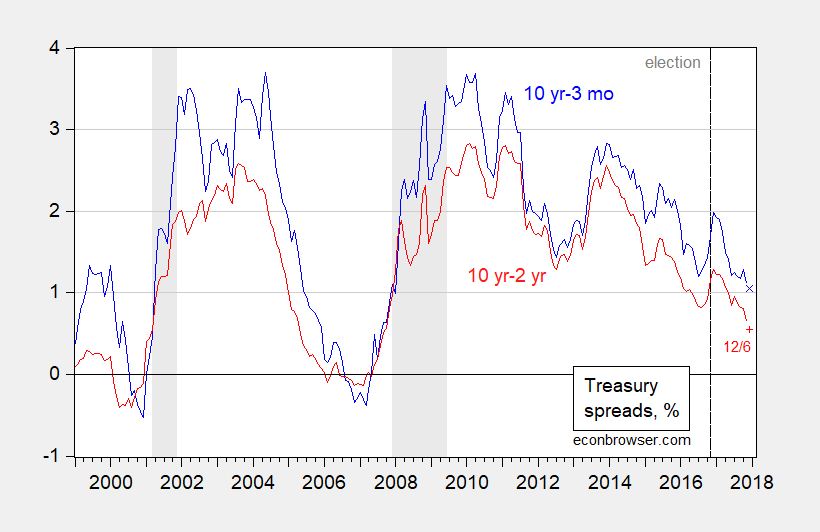

Figure 1: Ten year minus three month Treasury spread (blue), and ten year minus three month Treasury spread (blue). December observations pertain to 12/6 daily observation. NBER defined recession dates shaded gray. Source: Federal Reserve via FRED, NBER and author’s calculations.

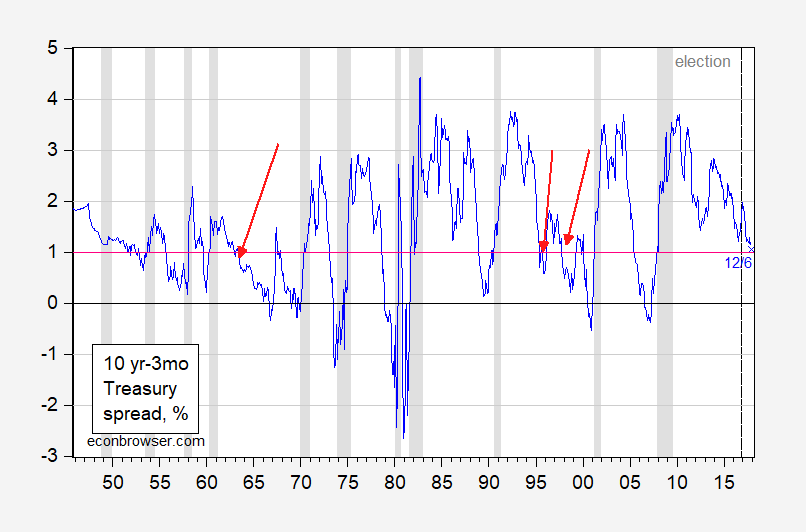

In general, once the yield spread is shrinking, it continues to shrink (so the question posed pertains to observations of the 1% threshold being breached as the spread goes down). You can see these instances where the yield curve breaches 1% from the topside in the following graph (red arrows).

Figure 2: Ten year minus three month Treasury spread (blue); December observation (blue x) pertains to 12/6 daily observation. NBER defined recession dates shaded gray. Red arrow denotes observation where spread cuts 1% threshold from above and then rises again and/or no recession follows. Source: Federal Reserve via FRED, NBER and author’s calculations.

So…inversion (which is increasingly considered plausible) is not necessary to say a recession is likely impending.

This is a informal approach; a formal, statistical approach involves running a probit regression 1967M01-2017M11:

recessiont+6 = -0.332 -0.575×(GS10-TB3MS)t + ut

Both coefficients are statistically significant (the McFadden R2 = 0.22); the implied probability of recession is 16% for May 2018.

This is slightly higher than the estimates I obtained using this specification back in September. Of course, this formal forecast assumes that the behavior of the term premium is unchanged over time, a presumption that is questionable.

For more formal, cross-country, analyses, see Chinn and Kucko (2015).

The Econbrowser recession indicator is only at 3.3%? Is that right? What is this inversion telling us, if not recession?

randomworker: The Econbrowser index refers to current conditions (as of 2017Q3), while the term spread is a leading indicator of recession. I’m pretty confident that we are — as of the 3rd quarter — not in recession, given readings of IP, NFP, etc. If inversion occurs in 2018, I can believe a recession will occur in 2018-19. The two are not necessarily mutually exclusive.

Shouldn’t we put some parameter on the amount of time until recession? If the recession didn’t occur for 2 years and the yield curve remained sub 1%, was it really a valuable or timely indicator? I’d argue no

mp123: 16 months on average.

two points:

1- monetary policy was materially different in the Volcker/Greenspan era. In that era, recessions were engineered to disinflate the economy. I would not include pre-1979 data in the regression.

2- What was happening between Jan 1993 and Jan 1995? The Fed was raising rates. Then between Summer 1995 and Spring 1996 they backed off and lowered rates. From summer 98 to spring 99 they lowered rates, then they reversed and raised rates until Sept 2000.

The the troughs in the graph roughly correspond to turning points in monetary policy stance.

In other words, “once the yield spread is shrinking, it continues to shrink” is really a statement about monetary policy. All this regression estimates is how many times the Fed has engineered a recession once the 10-2 or 10-3 spread has declined this far. Or, the Fed propensity to screw up and turn the screws too far.

16% chance of screwing up by May 2018? Nah, I rate it 90%. With no evidence of wage inflation, a flat Philips curve, persistently low inflation under 2% which puzzles the committee, and no idea how winding down the balance sheet will affect the economy, they should be on hold with rates. The present course of monetary policy will lead to recession, its only a question of when. The FOMC has consistently overestimated growth and underestimated inflation over the last 10 years. The compressed 10-2 spread is a warning that they are about to tighten the screws too far.

Right now, I give the FOMC only a 10% chance of changing course before their margin of error runs out. Powell is a wild card, we will see in a few months. The good news, if they is any, is that fiscal policy will to some degree compensate for their error. Of course, I would rather not see a trillion and a half added to the national debt. But the choice right now seems to be a FOMC- engineered recession in a 24-36 months, which will surely add trillions to the debt, or a tax cut which will add to the debt while staving off a recession.

I think a tax cut now will yield, in sequence, a Kansas-like event followed by an Illinois-type event, or more precisely, a recurring series of crises like Illinois.

If we allow 2.5% real growth over the 2018 to 2027 horizon (the historical average), use the CBO’s revenue-to-GDP ratio and spending assumptions, and use the JCT’s estimates of the effects of the Republican tax plan, the deficit averages $800 bn to 2023 and $1.1 trn from 2024-2027. (I would note that I have budgeted a modest recession for 2021, as I think it highly unlikely that we could avoid one; and if I want to be historical, I could budget two recessions in the next ten years. I have allowed for one modest downturn, while maintaining an average of 2.5% real growth rate to the horizon.) So that’s a kind of better case scenario.

I would, however, note that the CBO’s revenue-to-GDP ratio appears improbable from 2024, certainly given current partisanship. First the CBO sees income tax rates rising to levels achieved in only two years — the best of the Clinton era — since 1967. The odds of reaching those levels in something less than an absolute boom economy are, I think, pretty close to nil.

Second, the CBO sees total tax revenues from all sources reaching 18.3% and 18.4% of GDP from 2024. This level has been reached only in ten years in the prior 50. The go-go Clinton years (lots of capital gains taxes) account for half of the 18.3% or better group by themselves. The Carter years cover another three (no wonder everyone hates him), and there are a couple years in the 1960s. Thus, the odds that the average level of federal taxation can be brought consistently to or above 18.3% of GDP without a concerted bipartisan effort is unsupported by the historical record.

I would note, if you look at the deficits in CBO’s budget outlook (June 2017 version adjusted for Republican tax plan effects per the JCT), they average an unsustainable 5.1% of GDP from 2024 — and that’s with the CBO’s highly optimistic tax revenue forecast!

Thus, while we may be able to increase the share of taxes in GDP by some modest amount, say, 1 pp of GDP, this will be in no way cover deficits averaging 4% over the horizon even with tax increases. Most of the work has to be done on the spending side. That is highly unlikely given the current climate in Washington. Therefore, change will likely arise by force from a series of recurring crises. The first of these will involve a reversal of the corporate tax cuts currently contemplated, a la Kansas.

Later changes will come from meaningful cuts to social programs, and if I read my numbers correctly, stiff increases in payroll taxes. Of course, the deficit will be of sufficient magnitude that the associated political deals will have to be sealed by coercion in two or three crisis-like events spread over eight or nine years. Much as we see in Illinois.

If you’d like to run your own numbers, send me an email to info@prienga.com and I’ll send you the associated spreadsheet.

It may play out like this:

As the labor force becomes more productive, through demographics, and the capital stock becomes modernize, through lower taxes, we’ll have higher productivity growth. Next year, the Trump Administration will begin to tackle entitlement reform to get more people working. So, we’ll have stronger GDP growth, along with more tax revenue and less entitlement spending, to start reducing the national debt to GDP ratio. In 2018, the Republicans may hold on to the House and gain in the Senate. There will be more entitlement reform that will reduce costs and shift money to the states. There may be a mild recession, given there wasn’t an economic boom, and another close election in 2020 where Trump wins. By the mid 2020s, the national debt may have declined to around 50% of GDP, although defense spending is a greater share of GDP. Mike Pence wins big in 2024 🙂

Yeah, there are a couple of different versions possibly. I’ll write a couple of pieces on this (I have threatened this earlier).

It is very hard in any of them to get much lower than 55% debt to GDP by 2027. The key driver is 25 million Americans hitting retirement age between now and 2030.

Send me an email, and I’ll send you the related file, and you can do your own versions.

Although, the spread falling below 1% didn’t always precede a recession, every recession was preceded by the spread falling below 1% (except, it looks like in the late 1940s).

Some are predicting the 10 year yield will rise next year on rising inflation expectations, stronger wage growth, and foreign economies strengthening (to buy fewer U.S. Treasury bonds). And, they’re predicting the Fed will hike three times next year. Maybe, they’ll be correct this time 🙂

I think that watching the 10 year – 30 year Treasury yield response to potential/likely Fed tightening is probably the single most important indicator of where the macroeconomy is likely headed in 2018 and beyond.

If the ten year yield stays under 2.60% and the thirty year stays under 3.00%, then the market is suggesting that Fed tightening (and who knows what’s happening in China?) and the yield curve inversion are forecasting a recession in 2019 . . . . . . . . and if the intermediate-to-long end of the curve rises smartly in response to tax cuts and an accelerating economic growth environment, then probably not.

Menzie Since there are only a few observations in which the spread crosses the 1% threshold, I’m guessing that the there’s a large difference in the sample sizes between the “0” and “1” observations. If that’s the case, then wouldn’t it be better to use a logit distribution and adjust the constant parameter (but not the slope coefficient)? My understanding is that for most purposes it doesn’t matter whether you use a logit or probit model…it’s largely just a matter of convenience; however, if there is a large difference in the sample sizes of the two binary groupings, then there are advantages to using a logit with a correction to the constant parameter if you intend to use the equation as a predictor.

2slugbaits: You’re right I think, if I’d run a regression comparable to my threshold-crossing rule. The regression reported is an utterly conventional probit regression where LHS is binary 1/0 recession indicator, and RHS is spread. I probably wasn’t clear in my exposition on that. 1’s are about 15% of the sample over the 1967-2017 period.

My own hyperinflated $.02 worth, but I’ve done quite a bit of number-crunching on this topic over the years.

Actual inversions (spreads below zero) are what I watch for when recession-predicting, with a median lead-time of 12 months to recession start after the inversion first occurs.

More for my own amusement than anything else, I also calculate recession probabilities for the different spread levels. Currently, there is a 30.55% probability of current recession.

JMO, FWIW, and YMMV.:)

Sebastian

On balance, Fed tightenings usually produce an inverted 2s-10s yield curve and then a recession follows in 9-18 months. Not every time, but that’s the way to bet.

US inflation expectations have been decreasing and are on the low side these days. I believe that is all these tea leaves err charts are telling us.

Perhaps the charts are also telling us that the tax cuts can ramp up deficits without a major risk of ramping up inflation.

There is some risk that the current account deficit will worsen but perhaps nobody will notice as US real GDP growth bounces up to 4%.

Without a major rise in expected inflation. Expectations matter, but aren’t the same as reality.

expectations ARE reality. As long as the FOMC remains committed to crushing the economy with high unemployment to tame even the risk of 2.5% inflation, actual inflation will remain well below 2%.

dwb: “Expectations are reality” is pretty PoMo…

PoMo??

dwb: Post Modern.

Gentlemen ,

Can I advise you as an old yield curve junkie an inverted yield curve only predicts a recession if the Central Bank of that nation has put up short term interest rates that are higher than the Bond yields.

The bod market used to take some time to realise this!

Menzie,

dwb is correct to some extent. Expectations play an important role in a big chunk of modern economic theory. I do not recall theorists claiming that these expectations have to be ex ante or ex post correct to have impact.

Not that I am encouraging ‘sound bite’ analysis…..

Which leads me to the part I do not understand: How is “expectations are reality” Post Modern?

Erik Poole: Agreed, expectations are important. Most of my int’l finance work involves expectations implicitly or explicitly. But it’s important to recognize that the steady-state rational expectations hypothesis which implies forecast errors cum innovations is very much unsupported by the data. Consider the Livingstone inflation series…that’s the sense I mean PoMo.

Thanks but I guess I was really hoping for an explanation of what post modernism means in the economics world. An explanation or definition that I can honest-to-God, truly understand. Much of what is ‘post modern’ strikes me as similar to structural approaches to social behaviour that are impossible to refute/verify.

The Livingstone survey of forecasters is simply a survey of expert forecaster expectations. One only takes them seriously if one has little or no knowledge of the cost-effective accuracy of forecasting in general, let alone macroeconomic forecasting at any kind of useful horizon.

If market players have been making good coin on the Livingstone survey, I am not aware of that.

Here’s a piece I wrote for The Hill today. I took some serious heat for it–and I relish the debate.

On performance-based pay for members of Congress.

http://thehill.com/opinion/white-house/363820-trump-can-win-on-deficits-solve-the-debt-ceiling-and-own-congress-forever#bottom-story-socials