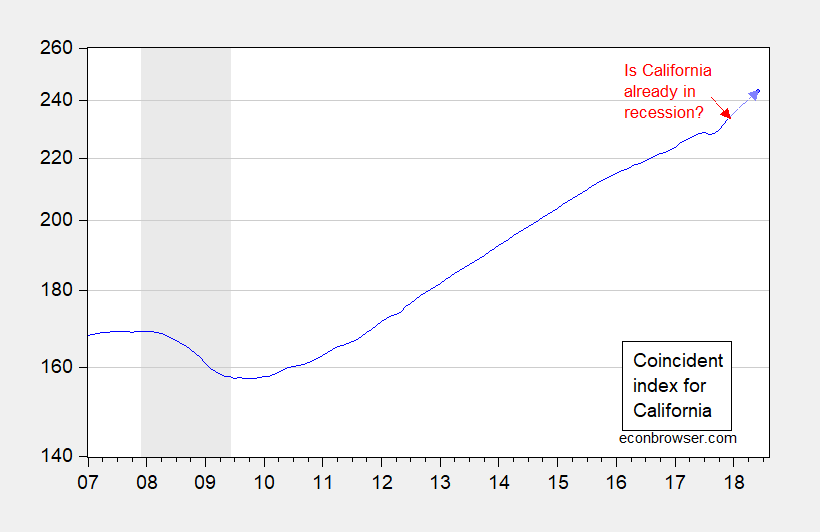

Back in mid-December, Political Calculations asked if California was in recession. Data released by the Philadelphia Fed suggests the answer is no.

Figure 1: Coincident index for California (blue), and implied index value for June 2018 using leading index (light blue arrow, blue dot) against log scale. NBER defined national recession dates shaded gray. Red arrow at date of Political Calculations post. Source: Philadelphia Fed [1], [2], and author’s calculations.

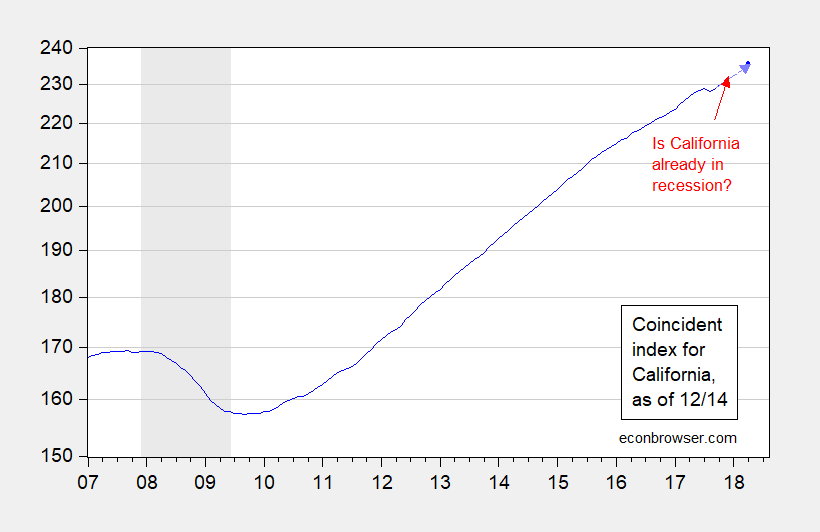

We have more data now than as of 12/14/2017, so it’s useful to retrospectively look back at what the indices showed as of that date. This is shown in Figure 2.

Figure 2: Coincident index for California (blue), and implied index value for April 2018 using leading index (light blue arrow, blue dot) against log scale. NBER defined national recession dates shaded gray. Red arrow at date of Political Calculations post. Source: Philadelphia Fed [1], [2], and author’s calculations.

So, as of December, some conventional near-nowcasting variables and leading indicators suggested growth after a small bump.

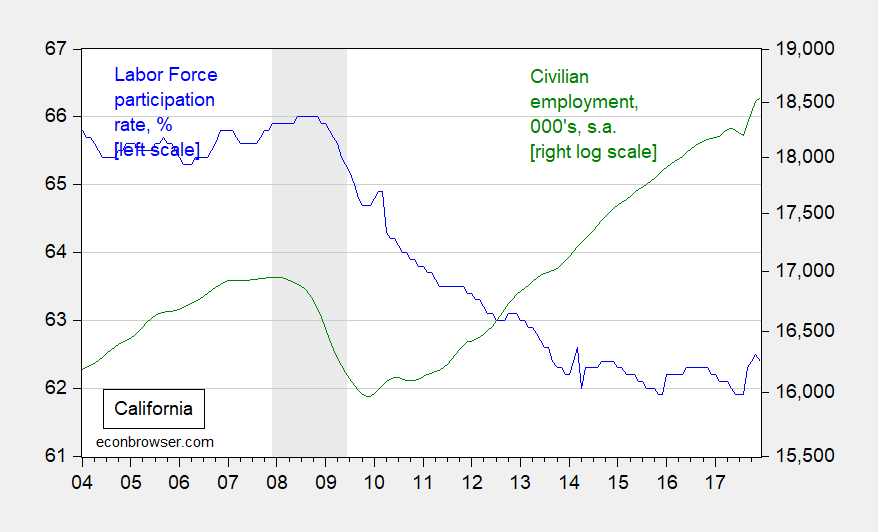

Political Calculations stresses labor force participation rates as important predictive factors (including the teenage participation rate) for growth. Below, in Figure 3 I plot the labor force participation rate and civilian employment.

Figure 3: Labor force participation rate for California, % (blue, left scale), and civilian employment over age 16 (green, right log scale). Source: CA EDD and BLS via FRED.

For me, I don’t see an incipient slowdown (or recession) in these data. However, I’m not familiar with the use of the LFPR as a reliable leading, or concurrent, indicator of recession, at either the state or national level, so I may be missing something.

For more on California economic statistics, see here and here.

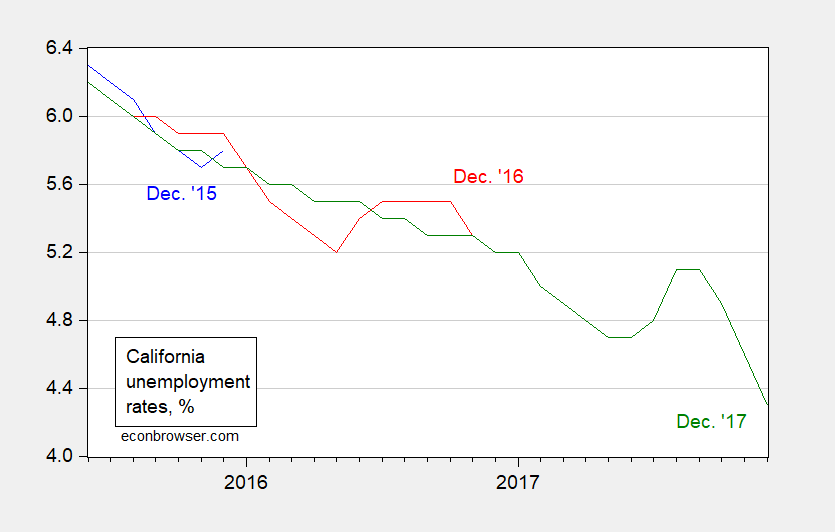

As an aside, the state-level household survey is subject to considerable revisions, even in a state as large as California. In order to show the pitfalls of making inferences about the business cycle by over-relying on state-level household survey based information, I plot various vintages of California unemployment rates in Figure 4.

Figure 4: California unemployment rates, %, December 2015 release (blue), December 2017 release (red), and December 2018 release (green). Source: St. Louis Fed FRED and ALFRED.

Notice how the apparent cyclical behavior in the December 2016 release is erased by the subsequently benchmark revised series in the December 2017 release?

@Menzie

I always get the distinct feeling/impression that economists (even the “liberal” ones surprisingly, while Republican economists seem to vacillate their opinion on LFPR by which party resides in the White House) have a strong dislike of LFPR. It seems to me many economists resent the LFPR being quoted or brought up as a topic as they view it as some kind of statement that “Economists unemployment numbers are largely bullcr*p”, and as some kind of personal affront to economists.

Menzie, my sincere/earnest question is, Am I imagining and conjuring this up in my own mind, or have you noticed this “phenomena” of economists attitude towards “LFPR”??

Moses Herzog: LFPR is useful for discerning trends (e.g., post recession why over a couple of years LFPR went down; why it rose during the 1970-1990). On the other hand, I am not familiar with using LFPR as a predictor of recessions. Among professional economists, I don’t discern a partisan bias in interpreting the LFPR.

@Menzie

I want to stress that I am not disagreeing with you. I agree that the vast majority of economists have no political bias on this topic (LFPR). I wouldn’t have asked if I didn’t respect your opinion and it was a genuine question on my part—deferring to your knowledge. Although I still hold I can find some exceptions, even among professional economists. Yes, a small minority.

However, I was wandering around online, and found this article, which I think, very loosely, relates to what we were discussing, though not directly related to LFPR. But it gives SOME credence to an argument I was presenting, as a side issue to my (formerly incorrect, but now changed) perceptions of professional economists views on LFPR:

https://krugman.blogs.nytimes.com/2017/12/03/la-trahison-des-clercs-economics-edition/?_r=0

@Menzie

I know my comment/question sounds a little odd/quirky (as I sometimes do), but like, I can give an immediate example that comes to mind. Larry Kudlow is one who is always twisting LFPR to fit his arguments at any particular moment (not that I listen to Kudlow much, 6 months goes can go by before I catch him). The same with Limbaugh. Herman Cain is another one. And I know the 3 just mentioned are NOT professional economists, those just popped into my head as guys who twist the LFPR to suit their narrative (and there are PRO economists that do this stunt also). When a Democrat is in office they quote the LFPR like it is sacred text, then when a Republican is in office, they portray LFPR as “just a bunch of bums who don’t want to work anyway”

As you know, I am an “armchair” wanna-be-economist. But my thought is, LFPR must not be a very good predictor of recessions as by definition the cats that are in the LFPR are not very well accounted for in the system (statistical sampling) to begin with, so, it’s a semi-unreliable number. I still think, though not a “predictor”, LFPR is nonetheless an important and overly ignored number.

FOOTNOTE I think LFPR might be a good predictor of large protest movements, such as “Occupy”, say “if the LFPR number went over ‘X’-percent, then large national protest movements would happen within ‘X’-timespan”)

“When a Democrat is in office they quote the LFPR like it is sacred text, then when a Republican is in office, they portray LFPR as ‘just a bunch of bums who don’t want to work anyway.'”

I think that what you have observed, especially from the partisan hacks, is that the LFPR was used primarily to discredit the low and falling unemployment rate under Obama. We frequently heard hacks insist that the unemployment numbers released by the BLS under Obama were bogus and that the real number was more like 20% or even near 40% (that’s where the LFPR would come in). It was all nonsense meant to confuse the voters in the conservative media bubble. As evidence, I will note that Trump now brags about the BLS numbers, which demonstrated a smooth continuity across the change in administrations.

* Obviously I should have said if the LFPR number goes under a certain “X”-percent, then large national protest movements would happen within “X’ timespan. Or you could obviously use the inverse LFPR number going over a certain %.

Of two minds on a California recession. One it would help my son afford to buy a house. Two it would also cause my son to lose his job.

@dilbert dogbert

Friendly advice. One of the wisest things you can do, not only for your savings, but also for loans, is get membership in an NCUA credit union. Not just any credit union but make sure it is NCUA because that is insurance, and it’s basically the credit union version of FDIC. Credit Unions nearly ALWAYS beat commercial banks’ rates both on saving deposits and on loans. That is, they pay you a higher interest on your savings, and charge a lower interest on loans. There’s different ways to get in—some you just need to be a teacher/educator, some you just need to be in military and/or have any member of your immediate family in the military (if you were in the army or any armed services you can probably get your son in). Many people think getting membership is hard–but usually credit unions will work with you to find a way. If he gets a 15 or 30 year mortgage, the savings on interest would probably shock you. The service is superior and they don’t spend their free time figuring out how to F you over like banks do. Here is a site, for finding NCUA locations near you—just put in you or your sons zip code or hometown:

http://mapping.ncua.gov

Also here is the main website for you to do your own homework on it:

https://www.ncua.gov/Pages/default.aspx

Tell your son, good luck from Uncle Moses.

Banking at the Bank of Mom and Dad also helps. He is saving around 3K a month. Not sure that keeps up the the crazy house prices. I told him to wait two years assuming there will be a price pull back then. Lotta Luck!!!

I would argue an NCUA credit union will still beat any bank on rates and service. But trust and relationships count for a lot, so if you have that then sounds like he’s in good shape. You also have leverage if you have a large account and can threaten closing your account if they mistreat your son. The hardest part when switching (or so I’ve been told) is getting the automatic electronic transfers set up again with the new account.

hey Menzie!!!!

Did you EVER think you would see a cartoon style message, perfectly customized for PeakIgnorance ???

https://twitter.com/Tortured_Verse/status/960362618706972673

The only problem with this is, Menzie…… you will have to let PeakIgnorance know that he is represented by the guy on the left, or he’ll get confused and think ANOTHER Nigerian is sending him a large bag of cash.

I liked the one about What the World Looks Like After Watching Fox News!

As Menzie states, the LFPR is certainly non-controversial among economists. (Real or professional ones that is.)

I am still surprised that the declining LFPR has not been more politically controversial. Not that it should be. But then pipelines are controversial while pushing NATO membership into former Warsaw Treaty countries is not.

Just in case anyone doubted that Trump has normalized fascism, he said in a speech today that Democratic members of congress who refused to stand and applaud his state of the union speech were “unAmerican” and committing “treason”. The Republican audience didn’t even blink at this demonstration of fascist authoritarianism. They just laughed. That is no joke.

No doubt Rick Stryker will jump in and shout FakeNews! in defense of his Dear Leader.

Rick has been notably silent since menzie opaquely identified him a couple of weeks ago.

@Joseph and @Menzie’s regular readers

Everyone got excited about Michael Wolf’s book. And I admit, I kinda “took the bait” at the beginning. But, even as a Democrat who strongly dislikes the VSG, I found the Nikki Haley accusations (and that’s what they were, accusations, no matter how much Wolf wants to hide under his mother’s skirt and whimper “Implications!!! Implications!!!” I said implications!!”) extremely bothersome. When you make false accusations, then it gives the VSG’s defenders ammunition to say that “the VSG’s critics will say anything”.

But here is the main point of my comment (I get easily sidetracked in my meandering thoughts). How did Wolf’s book get SO MUCH attention, and this article by Craig Unger get printed and not even register on the radar screen!?!?!?!?!

https://newrepublic.com/article/143586/trumps-russian-laundromat-trump-tower-luxury-high-rises-dirty-money-international-crime-syndicate

“But here is the main point of my comment (I get easily sidetracked in my meandering thoughts). How did Wolf’s book get SO MUCH attention, and this article by Craig Unger get printed and not even register on the radar screen!?!?!?!?!”

Short answer: Americans can’t get enough of celebrity gossip.

Long answer: There are plenty of journalists who have done a lot of digging into the topics covered in your link, but they generally aren’t TV journalists. TV news producers aren’t going to air a story that is just a bunch of rich people with foreign names bumping elbow with other rich people. The story right now is missing a dramatic point. It will probably take more investigative and legal firepower than journalists have to detect any criminal action by the Trump Org. on behalf of crooks involved in money laundering and other criminal activities. Mueller’s team, and perhaps the NY AG, have what’s needed. Where they use those resources will depend on where the evidence leads.