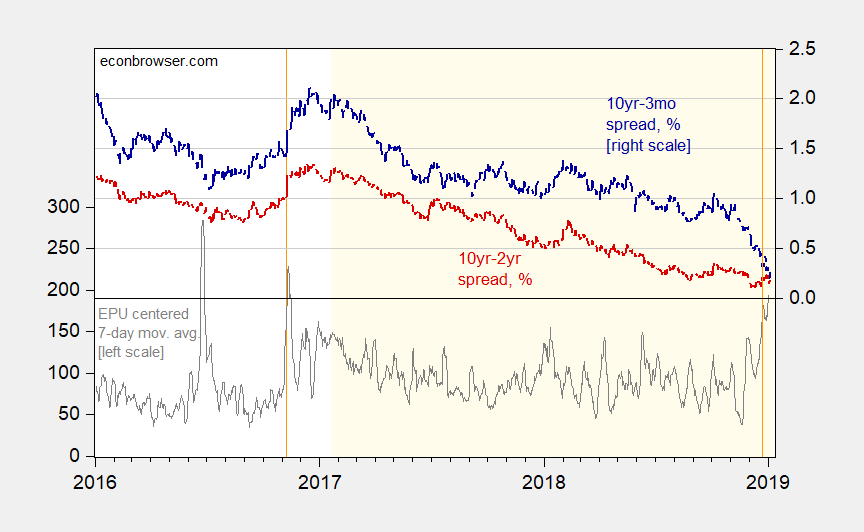

Do they matter?

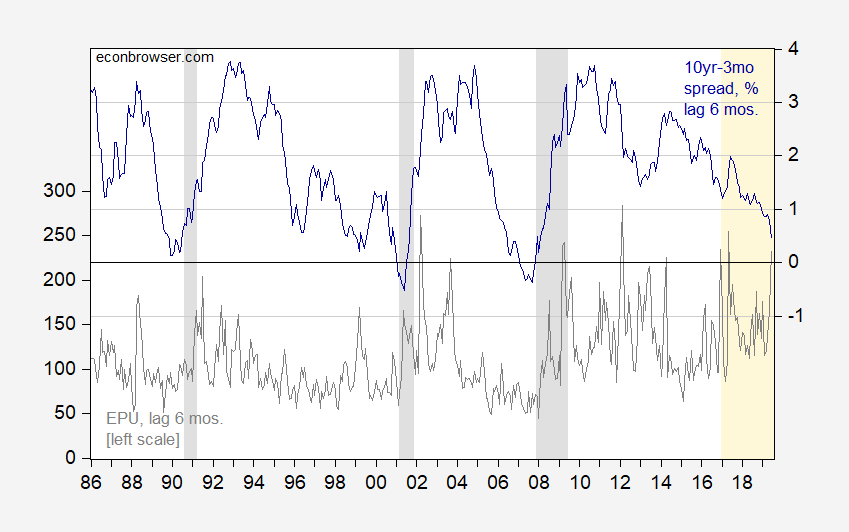

Why should we care? The spreads is of interest for well-known reasons. Interestingly, the economic policy uncertainty index (Baker-Bloom-Davis) seems to presage recessions at six month lags (statistically so, in-sample). I show this in the below graph, where both indicators are lagged 6 months.

Figure 2: Economic Policy Uncertainty (gray, left scale) lagged 6 months, and 10 year-3 month Treasury spread (blue, right scale), in %, lagged 6 months. NBER defined recession dates shaded gray. Orange denotes Trump administration. Source: policyuncertainty.com, FRED, and author’s calculations.

While lagged economic policy uncertainty is statistically significant in-sample, it’s not clear it would be helpful out-of-sample (note that in the 1990-91 recession, elevated uncertainty shows up as a correlate at a less than 6 month lag). Analysis is hampered by the small sample (3 recessions for the period spanned by the Baker-Bloom-Davis index).

Food for thought. Maybe Trump’s policies will give us an increase in the sample size.

Sarah Sanders goes onto Faux News hoping to tell one lie after another in defense of that stupid border wall. Funny thing – Chris Wallace nailed her on each and every one of her lies:

https://talkingpointsmemo.com/news/chris-wallace-fact-checks-sarah-huckabee-sanders-bogus-immigration-claim

Of course we can fully expect Rick Stryker to defend Sarah incessant’s lying. It is what he do!

Whatever Sara Sanders has to do with this post…….

Funny to me: democrats against Trump (afflicted with TDS) are in to the same logic the NRA uses against gun control.

It would be amazing to me if the democrat war party changed their logical stripes (like Liz Warren might have) and demand the pentagon produce results and facts for the trillions wasted there.