Nominal GDP targeting has been proposed as an alternative to the Taylor principle. One challenge to implementation is the relatively large revisions in the growth rate of this variable (and don’t get me started on the level).

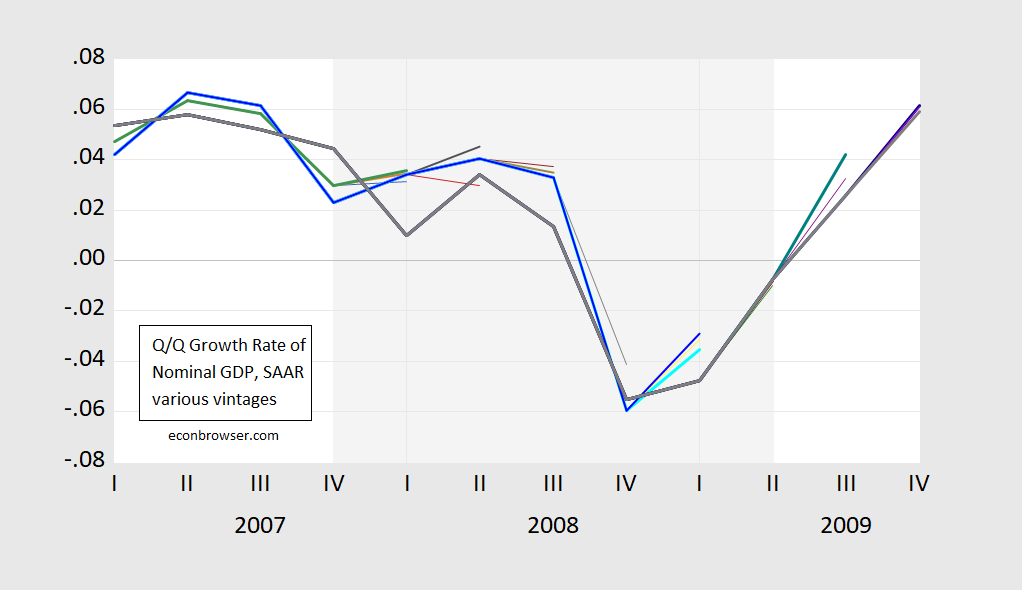

Figure 1: Q/Q nominal GDP growth, SAAR, from various vintages. NBER defined recession dates shaded gray. Source: ALFRED.

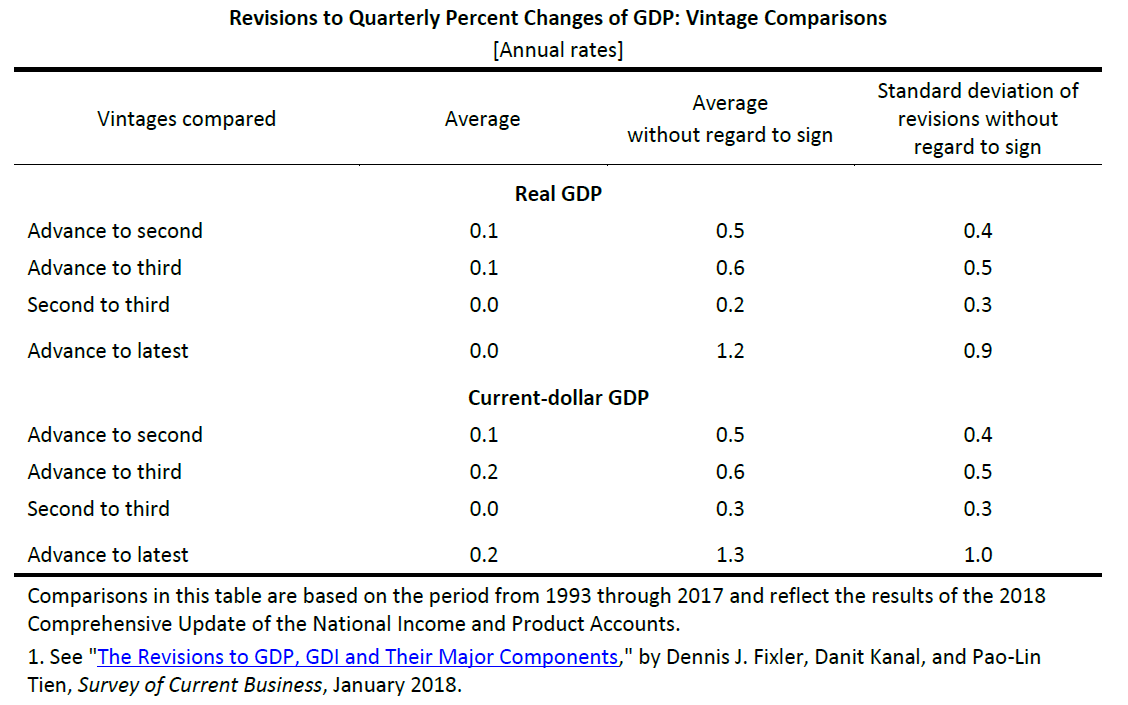

How big are the revisions? The BEA provides a detailed description. This table summarizes the results.

The standard deviation of revisions going from Advance to Latest is one percent (annualized), mean absolute revision is 1.3 percent. Now, the Latest Vintage might not be entirely relevant for policy, so lets look at Advance to Third revision standard deviation of 0.5 percent (0.6 percent mean absolute).

Compare against the personal consumption expenditure deflator, at the monthly — not quarterly — frequency; the mean absolute revision is 0.5 percent going from Advance to Third. The corresponding figure for Core PCE is 0.35 percent.

Admittedly, the estimation of output gap is fraught with much larger (in my opinion) measurement challenges, as it compounds the problems of real GDP measurement and potential GDP estimation; this is a point made by Beckworth and Hendrickson (JMCB, 2019).

On the other hand, the unemployment rate can be substituted for the output gap in the Taylor principle, by way of Okun’s Law. As Aruoba (2008) notes, the unemployment rate is not subject to large and/or biased revisions. (The estimated natural rate of unemployment, on the other hand, does change over time, as estimated by CBO, and presumably by Fed, and others, so there is going to be revision to the implied unemployment gap.)

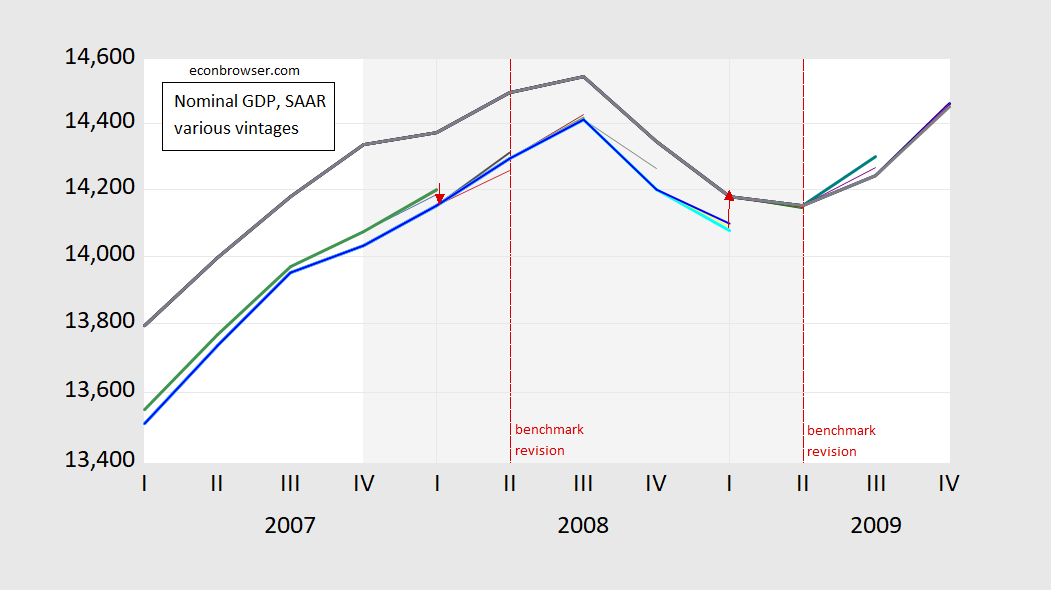

One interesting aspect of the debate over nominal GDP targeting relates to growth rates vs. levels. If it’s growth rates, there is generally a “fire and forget” approach to setting rates. An actual nominal GDP target of the level implies that past errors are not forgotten (McCallum, 2001) (this is not a distinction specific to GDP; see the inflation vs. price level debate). Targeting the level faces another — perhaps even more problematic — challenge, as suggested by Figure 2.

Figure 2: Nominal GDP in billions of current dollars, SAAR, from various vintages. NBER defined recession dates shaded gray. Dashed red line at annual benchmark revisions. Red arrows denote implied revisions to last overlapping observation between two benchmarked series. Source: ALFRED.

Revisions can be large at benchmark revisions, shown as dashed lines in the above Figure. But even nonbenchmark revision can be large, as in 2009Q3. ( Beckworth (2019) suggests using a Survey of Professional Forecasters forecast relative to target and a level gap as means of addressing this issue — I think — insofar as the target can be moved relative to current vintage.)

None of the foregoing should be construed as a comprehensive case against some form of nominal GDP targeting. But it suggests that the issue of data revisions in the conduct of monetary policy is not inconsequential.

Addendum, 9pm Pacific:

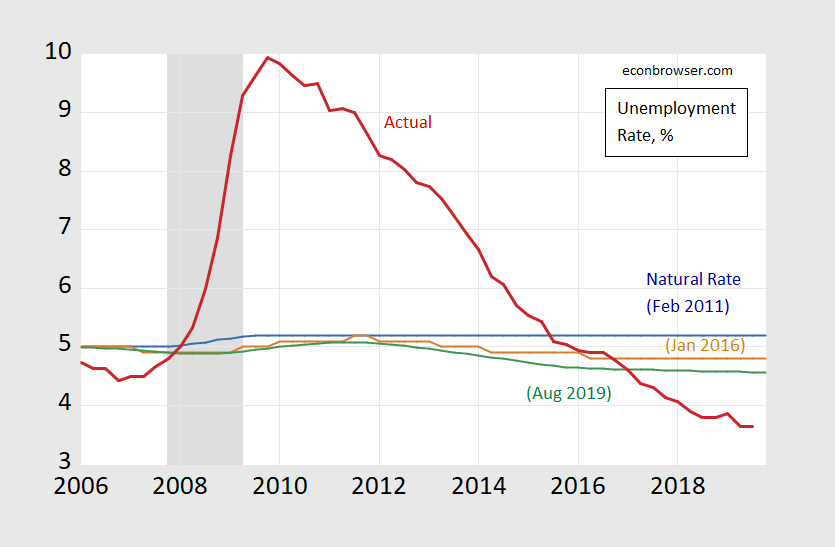

Reader joseph notes the revisions in the natural rate. Here is a graph of various vintages of natural rates (long run) as estimated by CBO.

Figure 3: Unemployment rate, latest release (red), long run natural rate of unemployment rate, February 2011 release (blue), January 2016 (orange), August 2019 (green), all in percentage points. NBER recession dates shaded gray. Source: BLS, CBO via FRED, and NBER.

Not a John Taylor fan. I basically hate the man’s guts, so I can’t comment on it in an unbiased way.

I have to wonder if this was prompted by:

‘Should monetary policy, a la Scott Sumner, target NGDP growth of x (say, 4%) and employ MMT is that’s necessary to get inflation high enough to reach NGDP targets given that QE does not appear to be particularly effective? Or is it ok for the ten year rate to go negative? What, in your opinion, is the correct policy? (Steven KopitsOctober 4, 2019 at 12:52 pm)’

This was a reaction I guess to the observation by Jeffrey Frankel that Germany currently has negative interest rates which makes monetary policy ineffective, which is why Jeffrey is advocating fiscal stimulus. In this light, Princeton Stevie’s rant here is beyond irrelevant. Then again it is pretty well established that Princeton Stevie is completely lost when it comes to even basic macroeconomics. MMT to make monetary policy effective? Oh boy!

Now when it comes to international macroeconomics, Stevie is even dumber than the Trump team as evidenced by:

“Again, let me ask you: What are you trying to stimulate? A reduction in the current account is not a legitimate objective of itself, unless you are suggesting that the Fed or the US Congress should set explicit goals for the US trade and current account deficit, a la Trump.”

Menzie offered him a Jackson Hole paper which I’m sure Stevie has not read yet and even if he had – he does not get. Which is why I provided that link to the Meade-Swann diagram discussion of the Eurozone issues. Not that Stevie will get this simpler discussion either.

So because nominal GDP has measurement issues, the Fed instead uses NAIRU which they can’t measure at all?

NAIRU has one advantage. Being an arbitrary completely made-up number, the Fed can use it to justify their decades long war against wage earners ever getting a raise.

joseph: Nairu is completely arbitrary? Didn’t know that. Will have to tell my students.

I think there have been government officials who have fought against increasing minimum wage and other things which hurt mid to low income folks. But I’m trying to remember when the Federal Reserve had done this?? Mind you, I have taken arms up over some Fed Res policies and actions, but I don’t know they have ever specifically had it out for “Wage earners”.

Menzie, you didn’t let joseph sneak into the Ron Paul brand caramel apples to get sick again did you?? I thought we agreed he has to wait until Halloween. Really now……

Can you tell me it’s value, even to one significant digit, except after the fact? Four years ago Yellen said it was 5% and time to raise interest rates.

joseph: See addendum to the post for CBO estimates.

The addendum illustrates my point. Vintage 2011 was horribly wrong. Vintage 2016 was also wrong. And here we are in October 2019, with unemployment a full point below the “natural rate” and where is the accelerating inflation? What use is a metric that seems to have no relation to reality? My belief is that the Fed simply uses a made up NAIRU to justify interest rate increases that make them feel good and safe from any possible wage increases.

At least you can measure GDP, whatever its weaknesses. But NAIRU is always just a guess that you can never verify, right or wrong, until you actually get accelerating inflation.

joseph: Well, you might think that Fed staff just makes up the NAIRU estimates. By the way, those are CBO estimates graphed — so you believe CBO just makes up the estimates as well?

Essentially it is. “Unemployment rates” are totally guesses as well. Neither GDP or “Nairu” are calculated accurately.

What an insulting comment with respect to the professionals at the Bureau of Labor Statistics. Oh wait – you have no clue what they do. Never mind.

@ joseph

I’m very sympathetic to your frustration (and anger??) over certain recurring issues and what seems to always be a convenient rationalization for those issues which never go away. However you should know not even the FOMC members agree on everything. Yes, they do tend to “fall in line” with the Chair. But not always and they are much more transparent, then say in 1989 about disagreements and which members of the board disagree. It’s a little more difficult to have a “conspiracy” when you don’t have agreement among the “conspirators”. If you want to go down the conspiracy route, the Fed Res passive attitude on bank regulation is the place to look. Rate moves upwards have little connection as far as I can tell to national wage moves. I’m happy to be corrected on that last sentence by anyone if I’m wrong.

Moses, I suggest you look again.

Fed funds have an 0.8 correlation with the growth of average hourly earnings.

@ spencer

Why don’t you show me the link for that?? I knew some jack*ss would have to pipe up Barkley style on that. What I mean is specifically Fed moves, and you might remember that rates are usually raised when the market/economy is doing well. So as the worn out cliche goes “correlation does not equal causation”

I honestly don’t mind being corrected. But you need to show me a semi-respected link that shows the two are connected.

I can tell you that it’s usually hottest between 2:00pm–4:00pm where I live, but I’m not certain that if I move the dials on the clock to that time, I can instantaneously make it hotter outside.

I did it myself. It is very easy to get fed funds and hourly earnings data into

a spread sheet and do the analysis. I”ll be happy to send you mine.

HaveChinn give you my email address.

@ spencer

You’re almost as hilarious as CoRev. My desktop is still puking up bile from CoRev’s spreadsheet. Why don’t you send it to Menzie’s email and he can put it in a blog post. That way everyone can see your “penetrating analysis”. I’d nearly pay to see that one. On my computer?? No thanks.

I am still failing to see the usefulness of NAIRU. Regardless of who is estimating the number, it has consistently been over-estimated for the last 40 years. It has been used as an excuse to suppress employment and wage gains.

At this moment, unemployment is a full point below the estimated “natural rate”. Where is the accelerating inflation? Why use a metric that is always wrong? Why use a metric that seems to consistently be biased pessimistically?

@ joseph

I have a theory which is most likely to sound preposterous by both you, the readers of this blog, and the hosts. Would you like to hear it?? It is in fact why I have said for years now (you can ask Bruce Krastings this, if he is still breathing, as we went back and forth on this probably as far back as 2010) for a long time that inflation is not a real imminent threat. Let me know, as I normally don’t like to make myself available to have paint gun shots fired point blank in my face.

joseph I’m not unsympathetic with your concerns over the NAIRU; however, I think those concerns are really more about the way the Fed has failed to test the NAIRU in a robust way. In other words, you’re on firmer ground in arguing that in practice the Fed doesn’t seem to want to truly explore the boundaries of the NAIRU, and as a result we’re left with theoretical arguments as to what it might be rather than basing estimates of NAIRU on empirical observations. In principle the Fed ought to be able to test the boundaries of the NAIRU by simply keeping interest rates low until inflation begins to accelerate. But in actual practice it seems like the Fed wants to stop short of allowing inflation to accelerate. As a result, we really don’t know what the NAIRU is. We have some theoretical arguments and some extrapolations by lots of serious economists, but no actual testing of the NAIRU threshold. That said, there are some advantages to using the NAIRU over nominal GDP. For one thing, the unemployment rate and inflation rate are published at a higher frequency. That strikes me as an important advantage. Another advantage is that the household survey based unemployment rate can be cross-checked using the establishment survey data. We also understand the seasonality adjustments for the unemployment and inflation rates far better than we understand the seasonality adjustments for nominal GDP. Not sure why that’s true, but it seems to be a fact of life…at least recently.

I think the best way to evaluate the relative merits of nominal GDP versus NAIRU is to consider the relative risks associated with any errors. And are those risks asymmetric? But that’s a topic for some young grad student, and I’m neither.

Not to mention that the relationship between compensation gains and inflation seems to have weakened substantially. The wage-base Philips curve is in somewhat better shape than the inflation-based curve, but that doesn’t help much in calibrating monetary policy.

“That said, there are some advantages to using the NAIRU over nominal GDP. For one thing, the unemployment rate and inflation rate are published at a higher frequency. That strikes me as an important advantage.”

Well, you can measure unemployment and you can measure inflation, but how do you measure NAIRU? It’s just a made up number, whatever theoretical trappings you want to wrap it in. What we do know is that NAIRU, whatever its source, has been consistently biased to the inflation side for decades. And that has real effects on wages.

joseph Well, you can measure unemployment and you can measure inflation, but how do you measure NAIRU?

I’m not following you. Doesn’t your question answer itself? As you said, each component of the NAIRU is measurable.

@ joseph

Some reasons why inflation may be slow to take off. Personally I don’t think that these are the main reasons, but these are no doubt contributors to inflation being less likely to “ignite”.

https://www.stlouisfed.org/publications/regional-economist/first-quarter-2018/why-inflation-so-low

High inflation can nearly be as terrorizing as unemployment. Obviously nothing is worse than losing your job. But high inflation can wreck millions of lives. pre-WW2 Germany is the obvious example. Tons of others. But telling people how painful inflation is who have never experienced it, is kind of like telling someone age 15 what life was like before the internet. You can describe it, but it’s really hard for them to internalize that feeling.

the problem with inflation hawks is they treat every level of inflation equally bad. to your point, we have not had “high” inflation since the early 80’s. We get people ready to jump off the bridge if you were to mention 4% inflation. at 6% inflation, you would think the world would end. for the average person, i would imagine that 6% or higher inflation with an economy that still has decent employment is good. for most folks, their biggest cost is their mortgage. the higher rates will have some impact, but inflation will appreciate the house over the long run. low inflation is a problem right now for many people.

Interest rates are not a solution to every problem under the sun. And I am not the only person (I suspect Menzie agrees with me on this) that is very afraid we are about to find out rates are not a solution for everything under the sun, when we are now near the ZLB and there’s negative rates all over Europe. The proper answer under these conditions, as a pretty wise friend/brother of Menzie’s recently pointed out (somewhere?? where was it??) is more apt to be a semi-aggressive, strategically targeted, fiscal spending policy. Rate moves will help, but do very little in actuality at this point.

In my personal opinion, we are at a stage it no longer does much good to get worked up and aggravated about FedRes rate moves—that may change in the future, but right now those moves don’t amount to much.

Good post.

Of course it undermines your latest BS. But yea it is a good post even if you have no clue why.

Today’s “Princeton”Kopits economic commentary sponsored by “Abilify”. “Because you know you need it, and you can pronounce it”. At a New Jersey pharmacy near you.

Prof. Chinn,

Can you elaborate on Wu-Xia shadow fed funds rate and the current downturn? I think the fed may have over tightened by ending QE , shrinking the balance sheet(inverse of growing the balance sheet and Wu-Xia rate), and raising rates.

With the massive injections of repo funds the last weeks it seems the economy is starving for liquidity, and overtightened.

The Trump Tariffs are a part of it, but not the full picture. They are a blunt weapon that might help our economy in the long term, not considering the national security implications.

I’d like your analysis on these topics.

Thank you

Anonymous,

While awaiting the “official” reply, mind my asking why Wu-Xia? That measure reverts to the nominal fund rate once the lower bound of the target range reaches .25%. Essentially, it has lost any independent meaning since the Fed moved away from zero.

So, the whole point seems to be that since we don’t have the ability to actually measure all economic activity, we have to accept that estimates have some degree of error… accepted. Unfortunately, that’s not what the message to the public is: if the government publishes a number, it is a fact. Well, I guess no one wants to hear reports that say, “Economic growth last quarter was [terrible/bad/fairly bad/better than nothing/okay/good/great].” But the reality is that with two or three “adjustments”, those descriptors might work out just as well [okay that’s “a little” factitious].

“Unfortunately, that’s not what the message to the public is: if the government publishes a number, it is a fact.”

Well maybe you accept any number you see as a fact. Of course you tend to read Trump’s tweets and the intellectual garbage from Fox and Friends, which you accept as “facts”. The rest of us know how to do research unlike Single Statistic Bruce “no relationship to Robert” Hall.

I’ve brought up the issue of revisions to Scott Sumner multiple times as a concern, but it’s usually in the context of specific NGDP targeting ideas. However, I think there are ways to structure level tar getting rules so that they are less exposed to revision issues.

“I think there are ways to structure level targetting rules so that they are less exposed to revision issues.”

Really? Pray tell how would you do this? I’m sure the good folks at the American Economic Review are eager to review you incredible paper!

Mainly my thought on this is “so what.” The Taylor rule itself started off as nothing more than a statistical description of Fed behavior, as if Greenspan held some magic 8-ball telling him which way to move rates. Ex-post, a lot of words and NBER papers were written attempting to justify the Taylor rule in terms of minimizing the variance of output and inflation. Which inflation metric? PCE? CPI? GDP Deflator? Trimmed mean? Chain-weighted, or not? Remember the days when Greenspan would lecture congress on the nuances of various inflation metrics and why CPI might overstate inflation? A debate which led to the Fed’s “preferred” measure Which unemployment metric by the way?

Different formulations of the so-called Taylor rule lead to wildly different signals.

Moreover, the Taylor rule and NAIRU framework depend a lot on what you think the Phillips curve looks like. With 3.5% unemployment, sub 3% wage gains, and 2% inflation, why should I believe in the Phillips curve or NAIRU anyway? I am not seeing a whole lot of wage or inflation pressure, even at 3.5%.

Ultimately, a lot of sweat went into more precise measures of inflation, because post-Volcker, a lot of emphasis was put on inflation and inflation expectations. After the great recession, a lot of economists came to the realization that U-6 or labor participation might be more important than headline unemployment.

I am 100% certain that if the Fed decided NGDP was important, better than the Taylor Rule, a lot of sweat would go into collecting better data and refining initial estimates.

The question should be: in this digital age of ecommerce, why exactly are revisions so substantial and how can we make them better? Separately, is NGDP the right framework, and under what conditions?

Anyone notice how New York Times has Bernie dropping dead any moment now?? Because guys age 78 never have heart attacks and bounce back days later just fine. That never happens. Dick Cheney had a heart transplant and he’s dead now, did you guys know that?? Yeah. Heart problems.

Maggie Haberman is a joke, because the moment she found out rural women didn’t vote for Hillary Clinton, she started fawning over trump in the White House.

https://www.youtube.com/watch?v=-1smr3-p7tU

You know the tough part of life for Maggie Haberman?? When her “writing partner” was no longer part of the deal she voluntarily left her book deal (that was still on the table for her). She didn’t get paid for saying “I don’t want to do the book anymore”. Can you imagine they could do that to a reporter?? What an outrage.

https://www.buzzfeednews.com/article/rosiegray/maggie-haberman-book-thrush

I wonder who was going to do the heavy lifting on that White House book?? Well, we’ll never know now will we?? But one thing we do know—Maggie Haberman is the master of the “mmm hmmm” “mmmm hmmmm” “mmm hmmmm” “mmmm hmmm” style of investigative journalism. No one better:

https://www.nytimes.com/2017/07/19/us/politics/trump-interview-transcript.html

“Dick Cheney had a heart transplant and he’s dead now, did you guys know that??”

moses, you are now in trump territory with the falsehoods. dick cheney never had a heart to begin with.

See, you tricked me, I was about to have hot steam spewing out of my ears on that one, and then you made me laugh with the last sentence. baffling, you dare to do such black magic trickery??

so trump appears to believe he is immune from both prosecution or investigation while president. in addition, it appears he also believes anybody associated with him also receives the same treatment. exactly how is a president held accountable by the two other arms of government if this is the case? this guy continues to believe he is a dictator or emperor rather than an elected president beholden to the constitution and people of the united states of america. i find it appalling that even hacks such as rick stryker continue to support this scofflaw. apparently in some quarters of the republican party, disrespect of the constitution is acceptable behavior.

Well, donald trump applauded a NYT journalist being murdered by the Saudi leadership. Now he’s telling Turkey they can take large sections of Syria with no deterrent from America. This is how donald trump and the Republicans play “tough guy” with Middle East dictators?? Who are Moscow Mitch and Lindsey Graham going to blame when it turns into a clusterF— ??

Poor Moscow Mitch McConnell. After little donnie trashed Mitch’s house several times and Moscow Mitch said “Aawww, he’s just a kid, let him play”, now we’re up to the 10,000th offense and the “very stable genius” just squatted and took a large dump on Moscow Mitch’s living-room carpet after a quadruple serving of Big Macs.

https://www.nytimes.com/2019/10/07/us/politics/turkey-syria-trump.html

No worries, Mitch just checked and he’s doing super awesome in the polls:

https://fivethirtyeight.com/features/mitch-mcconnell-is-the-only-senator-more-unpopular-than-susan-collins/

They’re saying Rick Perry will be gone by the end of November. Does anyone find this hard to believe?? Who gains now, other than William Barr and Pompeo (both trying to avoid criminal prosecution) by staying in donald trump’s cabinet?? Moscow Mitch McConnell’s incompetent do nothing wife??

https://www.youtube.com/watch?v=VLqrvL3rn4k

Nothing “Earth-shattering” here. Just some pretty good political banter and discussion of impeachment as it relates to history. 3-4 humorous moments. It is hard to laugh when these things are so troublesome and disturbing, but humor can help us keep perspective or give us that badly needed half-minute of respite:

https://www.youtube.com/watch?v=Smc1Y0iCJa8

Meacham is one of those guys who can fool you, because he has this stiff and stern exterior but actually a pretty funny guy. The Brooks reference cracked me up pretty good.

Get ready for a literal blood bath on the Kurdish people. America’s best friend in the Middle East next to possibly Israel. We told the Kurdish people America would be there for them, like their soldiers supported America, and now this BASTARD donald trump has sold the Kurdish people down the river. Who will believe America about anything now when we happily watch our friends get slaughtered ???

Thanks Mitch McConnell!!!!! Thanks Lindsey Graham!!!!

I’m sure CoRev and the rest of the usual suspects will all agree that Trump’s decision to leave the Kurds to their fate is the product of a “stable genius” with “a great and unmatched wisdom.” As Richard Engel pointed out, who talks that way other than someone like Muammar al-Gaddafi? Trump is just batshit crazy and getting worse each month. If he weren’t president I suspect and hope the family would have arranged for an intervention.

Maybe the Turkish government has some dirt on Biden to give to Trump.

On the blood bath that is inevitable to happen:

https://www.youtube.com/watch?v=xcA9P9aEWDY

Thanks for causing the deaths of thousands of innocent Kurdish allies of America!!! THANKS donald trump!!!

Folks, this is apt to be the BIGGEST humanitarian disaster since what happened in Yemen:

https://www.youtube.com/watch?v=vKFSmyS002I

Lindsey Graham and Mitch McConnell ENABLED donald trump and ENABLED this situation—they have blood on their hands now. I hope Mitch McConnell and Lindsey Graham are proud of their blood-stained hands. They enabled this slaughter of the Kurds, and when they meet their God one day, they will answer for the deaths of most likely THOUSANDS of innocent people. Not to mention the ripples in the water that are caused by this.

https://www.youtube.com/watch?v=UlzfXkOz-V8