Today, we are pleased to present a guest contribution written by Laurent Ferrara (Professor of International Economics, SKEMA Business School, Paris), and Director, International Institute of Forecasting.

I recently discussed a very nice paper by Anna Orlik (FRB) and Laura Velkamp (NYU, Stern School of Business) on uncertainty shocks and the role of Black Swans, at the Paris School of Economics – SCOR Annual Conference. By playing with the data they used (real US GDP growth rate from 1968q4 to 2013q4, see Figure below), it is striking to see the degree of Non-Gaussianity of this series.

Note: Quarterly changes in log real Gross Domestic Product for the US and NBER recessions, source Fred database (GDPC1).

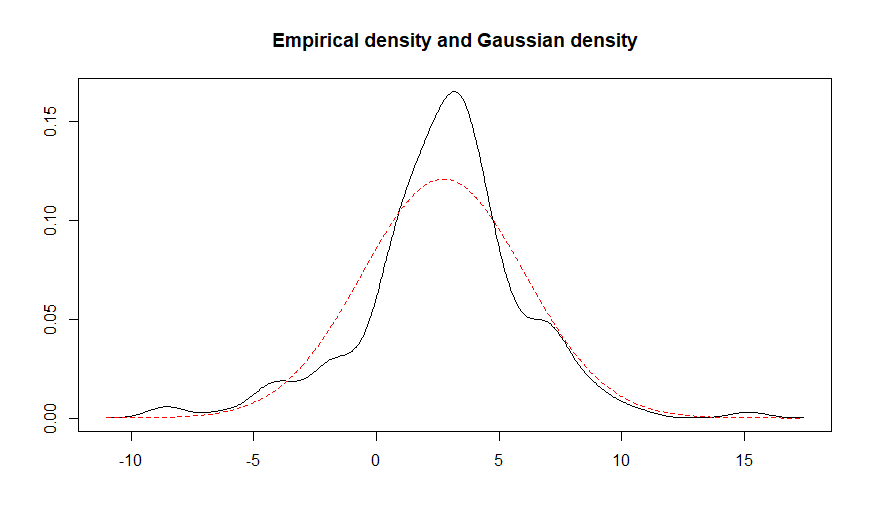

Indeed, there is an asymmetry to the left (Skewness= – 0.30) and the tails of the distribution are much thicker than those of a Gaussian distribution (Kurtosis = 4.98). A standard Jarque-Bera test strongly rejects the null of Gaussianity of this distribution. When plotting the estimated empirical distribution of the GDP growth rate and a Normal distribution with corresponding estimated mean and variance, we clearly see the gap between the two distributions (see Figure below).

Note: Kernel estimation of the US GDP growth using the R ‘density’ function with default options (black line). Sample mean is equal to 2.74 and sample standard error is equal to 3.30. Red line is the Gaussian distribution with those 2 estimated parameters.

In fact, the right tail of the empirical distribution seems to be quite in line with the one from a Gaussian distribution, but there are some clear divergences on the left tail, mainly due to the occurrence of seven recessions over the sample, as defined by the NBER Business Cycle Dating Committee.

By chance, econometricians have access to a battery of theoretical distributions accounting for asymmetry and fat tails. In a recent paper by Adrian, Boyarchenko and Giannone, just published in the AER, a Skewed-Student distribution is used to predict US GDP growth starting from a Financial Condition Index. This Skewed-Student distribution (see Azzalini and Capitanio, 2003) accounts for both asymmetry and fat tails using four parameters to be estimated, reflecting the first four moments of the distribution.

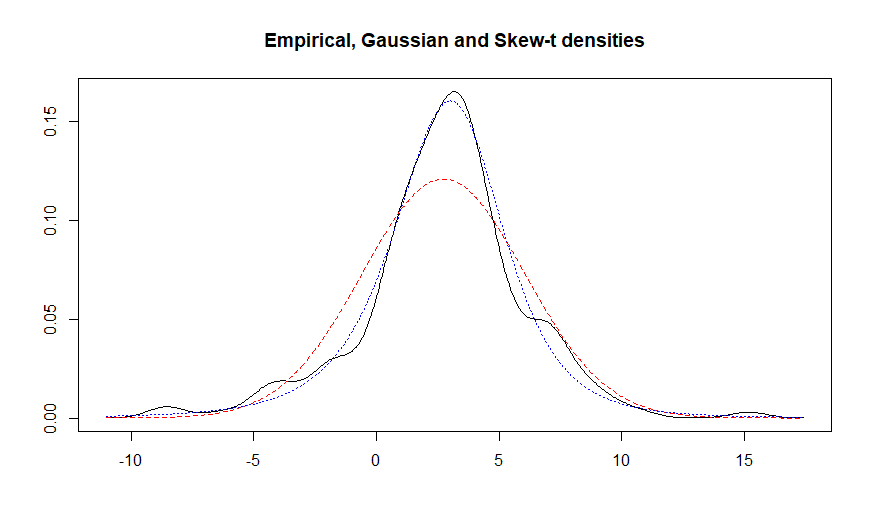

By fitting a Skewed-Student distribution to the US GDP growth through the Maximum Likelihood approach, we get indeed a much better fit than when using the Gaussian distribution (see Figure below)

Note: Kernel estimation of the US GDP growth using the R ‘density’ function with default options. Sample mean is equal to 2.74 and sample standard error is equal to 3.30. Red line is the Gaussian distribution with those 2 parameters. Blue line is the fitted Skewed-Student distribution using the R package ‘sn’

Does it matter to account of non-Gaussianity? For example, assume we want to estimate the (unconditional) probability of a Black Swan. We define a Black Swan as in the paper by Orlik and Veldkamp: a Black Swan is negative event that occurs on average every 100 years. Using our data, this corresponds to a value of GDP growth equal to -6.53%, based on the Gaussian distribution (ie: a quarterly probability of 0.0025). However, if we think that the correct distribution is a Skewed-Student, the estimated unconditional probability of a Black Swan increases to 0.0130. That is the unconditional probability of a Black Swan using a Skewed-Student distribution is more than 5 times higher than when using a Gaussian distribution.

A lesson from this small exercise at the current juncture is that recession probabilities estimated using Gaussian models are likely to be largely under-estimated.

This post written by Laurent Ferrara.

So I take this as another suggestion for Menzie’s last BLEG post; viz., the need to teach GLMs and not just OLS.

Menzie, programming is easy now. There is no reason to use canned distributions for ML probability estimates. Run a first stage on a continuous indicator. Toss the residuals in an empirical distribution and sample from that distribution to get probabilities wrt the continuous lhs variable.

Yes to conclusion.

BTW, in the paperback (2nd) edition of his The Black Swan, Nassim Taleb says there are three living economists who have influenced him:

Nouriel Roubini, Michael Spence, and me.

Barkley Rosser: “No really, but enough about me. Speaking of not talking about me, I was talking about myself the other day in reference to a book I’m writing about my great achievements, and it reminded me of a great thought I had while discussing something with myself……. ”

Dude, you are such a narcissist, at this point you’re making donald trump look like a rank amateur. It is good for laughs though, we can say that much.

Nassim Taleb is quite good in mathematics (I will give that to the man even though I strongly dislike him as a human being). As a self-aggrandizing “philosopher” the man is a laugh-riot.

Taleb plays a lot of child-like games with lexicon (semantics, pick your preferred term) in which he takes ideas that have been around a long time, and repackages them as his own:

http://falkenblog.blogspot.com/2012/11/taleb-mishandles-fragility.html

I invite anyone (who places zero value on their own personal time) to listen to this conversation with Taleb and tell me what impressions they come away with. It was hosted by…… wait for it….. wait for it….. wait for it…….. Mercatus.

https://medium.com/conversations-with-tyler/tyler-cowen-nassim-nicholas-taleb-skin-in-the-game-black-swan-104620da8a57

This post, in which someone manages to insert Taleb into the conversation is highly entertaining. The comment discusses Gaussian distributions also. Make certain to read the entire thread. It almost gives the idea someone’s feelings had been hurt more than once. This person, whose feelings had been hurt, suggested that a professor teaching graduate students “should not be teaching”. Well, all in a day’s work I guess. Possibly his way to spread peace and love across the internet. The entire thread is interesting, but personally I found commenter E. Barandiaran’s two cents the most insightful in the group.

https://www.econlib.org/archives/2009/08/the_best_questi.html

If all of that isn’t enough comedy theater for your weekend, try this philosophical gem (of probably hundreds) from Nassim Taleb. It’ll be one of the great epiphanies of your life, that is, if you’re not already busy deadweight training like Hulk Taleb is:

https://dealbreaker.com/2016/06/nassim-nicholas-taleb-deadlift

Moses,

It was completely relevant to bring up Taleb as he is the one who uses the term “black swan” in connection with extreme and unexpected events., which was used in this regard in the piece posted. As you can see from my post below I corrected the use in the post, which was not quite accurate. So in fact I know more about Taleb’s work and thought than does the poster, not to mention you.

He is certainly a colorful and controversial person. I do not agree with all his ideas, but on this core stuff about statistics he is on the money. At one point he had me on a list he kept on his websites of his enemies for criticisms I had made on the internet of some of his arguments. But we had a lunch in Washington where we made peace, which led to his mentioning me favorably in the second edition of his most famous book. He happens to be on the editorial board of the journal I currently edit, the Review of Behavioral Economics.

Thus I was in a position to correct the usage of the term “black swan” as it was used in the post here, and I was letting people know why I might be i a position to do that authoritatively.

You, OTOH, continue to make a fool of yourself with your ignorance of basic statistics and probability theory.

One instance, one use of a term which you claim to be “not quite accurate” is insufficient evidence to claim knowing “more about Taleb’s work” than does Ferarra.

You’ve gone some way toward confirming Herzog’s assertion. Also dangerously close to “argument by authority”. Better to let your ideas do the work.

macroduck,

I apologize to Menzie for forgetting that Ferrara made the misleading remark about the meaning of “blavk swan.” As it is, Ferrara is wrong. You want to defend this inaccuracy? Are you claiming I am wrong? I am not, Macroduck..Do you want to join Moses in a toilet of inaccuracy?

What I said is accurate: black swan means fundamental uncertainty, a la Keynes and Knight, the non-existence or irrelvance of any probability distribution. I have published quite a bit on this. You want to question it? And Taleb himself has been very clear: mere fat tails on known probability distributions are mere grey swans. This is an argument “by authhority”? Go read him. This is thefact. Yes, I know his work. Do you? Does not look like it.

No reply link is available to Rosser’s reply to me, so I will reply here.

” So in fact I know more about Taleb’s work and thought than does the poster, not to mention you.”

That is a pretty clear case of “argument by authority”, so I’ll stand by that.

Do I claim that you are wrong? So often, these exchanges include questions along the lines of “did you read what I wrote?” I did not take a position on who was right about Taleb. That should be clear from what I wrote. Goading me to take a position is a threadbare debating trick and I won’t bother responding. In fact, Taleb is irrelevant to the discussion, aside from your efforts to drag the discussion toward Taleb.

Just to repeat, Ferrara employs the definition of “black swan” adopted by Orlik and Veldkamp, not Taleb’s definition. Taleb does not own the expression. It was in wide use before he was born, so Orlik and Veldkamp can reasonably adopt a definition which ignores Taleb. Correcting Menzie, (oops) Ferrara (oops) Orlik and Veldkamp misses the point of the research and detracts from discussion of the post.

Will I join Moses in the porcelain pond? The fact that you have posed the question in those terms absolves me of any need to respond. Your behavior here answers for me.

Macroquack,

“Argument by authority”? So what? Yes, I happen to be an authority on the issues involved here, with the fact that Nassim listed me as one of the three economists he takes seriously a sign of this. I do know his work, and I have published fairly heavily cited papers on this as well.

I am perfectly wiling to admit that there are a lot of people who personally dislike Taleb, with some of them making strong criticisms of various parts of his work. But this matter is what he is most famous for and what he is most right about.

So, sorry, but nobody was using the term “black swans” in connection with macroeconomietrics prior to Taleb’s bstselling book of the title. He made people aware of it, leading to them using it.

That the Orlik_Veldkamp paper came out in 2014, only a few years after Nassim’s book makes it all the more egregious that they would misuse the term to mean “fat tails” or kurtotic outcomes, when in fact he used it to mean “uncertainty” in the Knight-Keynes sense. I do not see anything you, much less the hopeless Moses, have said that undoes that criticism, which is completely valid.

We’ll let Ferrara off the hook on this as he is simply following those who seem to have made the mistake, Orlik and Veldkamp, although maybe they were just picking this up from somebody else who had made the same mistake earliler. This is how these kinds of erros or misinterpretations get spread throughout the literature, and I think I am completely in my right s to point out that it is an error, period.

Everything old is new again…ideas that overlap w/Black Swan have been around for a while, more recently in the “disaster risk” literature, and *much longer* in the “Peso Problem” (for the int’l finance economists among us).

menzie is correct, this issue has cropped up in disaster risk over time as well. it was there when people began to assign probabilities to natural disasters many years ago, probably first with respect to earthquakes. then the anomalies would appear, like the japanese earthquake and tsunami of 2011. that magnitude of earthquake was not thought possible along the given fault system, so it was not accounted for in the tail. this was not really a fat tail issue, it was an unknown quantity not expected to be able to physically occur. yet it occurred.

the issue, and it appears in most of the stem fields, is between descriptive statistics, modeling and theory. one can create statistical distributions that capture the probabilities of tails better and better. but when one tries to move that information into a coherent modeling framework for others to use, the models become intractable and difficult to interpret. thus people move back to a gaussian distribution, because while it is not completely accurate, it allows for calculations and explanations to occur. i am not sure this is a justifiable argument, but this is usually why you see gaussian distributions being used to describe something that is not gaussian. and it is also why you then obtain this idea of the black swan. the accuracy of the results diminishes along the tails, the exact area you are most interested in.

an interesting thing about the black swan events is how they are incorporated after the fact. how and where do you fit in information about a black swan event, even after it has occurred and you try to update your model? what probability do you assign to it? just because it occurs once (in a million), do you increase its weight for future events? if you really want to see this idea taken to extremes, just look at quantum mechanics, where a measurement updates the probability to 1 for that outcome (even if it were originally 1 in a million), and zero for everything else. gaussian distributions play a large role in that theory. these issues nevertheless lead to interesting discussions.

I have now read your links, Moses. Falkenberg is parobably Taleb’s harshest critic. I think he does score a few points, but overdoes things. Seme with my old friend, Herb Gintis, for whom I had special issue of ROBE dedicated to target article by him. As it is, I published Taleb’s article on “Skin in the Game” in the first issue of ROBE.

The matter of the Econ-Log stuff is interesting in that it directly relates intellectually to this thread. This now ten year old exchange had me criticizing someone I have never met nor seen lecture, David Hummel, for arguing that the underlying probability distribution of business cycles is Gaussian normal, exactly what the main post here questions. I dragged in Taleb to criticize Hummel. I overdid it, saying he “should not be teaching grad students,” and David Henderson, the blog master, demanded I apologize, saying Hummel is a good teacher who prepares his lectures well, so I apologized for that while maintaining my position on the distributional issue. I have good and mutually respectful relations with Henderson, whom I know personally.

This is a sharp contrast with you, Moses. You have been caught once again in an outright lie, this time claimiing that the much-discussed article says that Native American ancestry is uniformly distributed over the European American population. Menziee has noted that this is clearly false. So, again, you owe an apology, but none has been forthcoming, just more inane insults. I apologize when somebody points out I have overdone it. You do not, not ever as near as I can tell. Pathetic.

Moses,

Speaking of digressions (as I do below), here’s one. The first link addresses Taleb’s “Antifragility”. The author of the link compares Taleb to Friedman, identifying both as authors he’d rather not read (preferring a Mayan apocalypse). There is another common feature to the popular writings of the two authors. Both coin words, phrases or comparisons as justification for writing books and the coinages tend to be nonsense. Antifragility isn’t a thing. The world isn’t flat, no matter how many anecdotes conclude with “The world is flat!” The Lexus comes from Japan, while olive trees do not, but Friedman points to Japan of clinging to the past in olive-growing fashion.

It can be hard to dismiss one’s own ideas when the publisher is waving around an advance. Taleb and Friedman are too easily tempted.

@ macroduck

It’s human nature for people to become enamored with themselves, especially after having attained a certain degree of success. Very few are “immune” to this. Especially in America where celebrity and “celebritization” (is that a word??) is so deeply engrained in the culture. You know it’s great if people can become celebrities through high accomplishment in mathematics and/or finance theory. That’s a great thing. America would be better off if we had more mathematics celebrities. But when that gets leveraged into something else, then you have problems. “I am good at finance calculus therefor I can opine about life in general”. It’s like the fashion model that wants to start a singing career. That doesn’t always work out.

People don’t begrudge Taleb a certain level of arrogance in his field of expertise, but 1) He needs to “stay in his lane” 2) An Ego not approaching the height and volume that reaches up to Earth’s stratosphere might be much easier to stomach.

So, I haven’t read the papers here before commenting (which is probably incredibly stupid, but there it is, I copped my plea), but I hope to get around to reading the papers.

The general idea is to get an “approximation” of the actual empirical distribution (which “smooth’s out” the asymmetry of the actual numbers), but economists are wanting something that makes a better approximation of the empirical distribution than Gaussian methods?? And they think Skewed-Student distribution is probably a better approximation of the actual distribution than Gaussian method has been up to now?? “Smooths out” the numbers–and yet gets them a better approximation or a better “fit” than Gaussian??

Menzie’s always on the busy side (not a complaint, just a statement of fact), so if commenter “AS”, 2slugbaits, or our good man Frank in Georgia want to clue me in on how close in the ballpark I am here in my basic understanding, that would be great.

Moses Herzog I made this up just for you. 🙂 I created the Cullen and Frey graph in “R” using the “fitrdistplus” package.

http://missionaryworkamongsavages.blogspot.com/2019/11/cullen-and-frey-graph-shows-observation.html

@2slugbaits

I am very flattered (and there is no sarcasm there as I tend to overuse that), Didn’t even know you had a blog, had I known I certainly would have visited it from time to time. I have a blog also, but it’s mostly just links and rephrasing of other people’s great observations, nothing that can touch what you have done here with the “R” package. You’re making me feel a little guilty on my “R” efforts, which have dropped off a little. I am still using the older “R” studio because my hardware is a little dated, so then I don’t think I can get the newer versions until I update my hardware. But I am going to look at the “fitrdistplus” and see if I can get a grasp on that. In fact I am going to commit to doing this tonight as it shouldn’t be that hard to see if I can at least download the package. I remember the term “bootstrapping” from the basic undergrad classes I took in college. I will try some of this out. But I greatly appreciate this. I appreciate it it more than your probably imagine and more than I can express on a blog. Thank you for this

@ 2slugbaits

This isn’t any form of criticism, as I am grateful you suggested this package and took the time on the GDP data. And I bet you know this, just was a typo. The package name is actually “fitdistrplus”. Just wrong placement of the r in the package name. I wanted to put this up for any others trying it that might have been thrown off by that. The only reason I knew, is when you type the first few letters out there’s a menu that shows the possible programs that might match the first few letters.

Short story made long, I have already downloaded the package, and much to my amazement the package DID install. The reason I say that is, again my “R” studio is old and I don’t think I can get the recent version because my hardware, just to be clear. So this causes problems on installs, especially with newer and better packages. Again, 2slugbaits I appreciate this greatly.

Thanks for the correction. Me and typos…

BTW, I don’t blog. On very rare occasions I will use it as a vehicle to put up a graphic or an extended discussion with someone. I’m strictly stone age. No Facebook, no Twitter, no Instagram. I even got rid of my cell phone when I retired. Trying to convince my wife to pull the plug on cable TV since 99% of what I watch is local news, public television, the Simpsons and non-cable NFL games.

I vacillate on internet being good or bad. Mostly I like to think of it as a library/newspaper resource inside the house. But I also use it for social media degeneracy, email can replace phone charges. I do use it a lot if the truth be told. For me it’s more of a plus than a minus, but things like reading blog posts may give me a false rationalization for not finishing books or doing other things more constructive. But I totally respect some of the, I forgot the word, luddite take some people have. But the fact you rarely use it makes me appreciate all the more that you extended that courtesy to me.

I don’t have cable TV, I am a cheap SOB and find between Youtube and the public library I can get most things I want free if I’m willing to have some small lag from the time most others watch them. Podcasts can be great if you learn to sift through the bad ones, which is pretty hard as there is A LOT of “chaff”.

I’m guessing some of the things you had said before hinting around some military and science duties you’ve had strongly hints you’re more technically proficient than me. Playing online doesn’t compare to proficiency with stats packages etc.

@ 2slugbaits

Meandering down this paper that relates mostly to the Skewed-student distribution (a significant portion that goes over my head) and found this link. I haven’t actually looked at it yet, but thought you, “AS”, or Frank in Georgia might find it interesting:

“A suite of R routines for evaluating the above log-likelihood and its derivatives has been developed, and it is available on the WWW at http://azzalini.stat.unipd.it/SN ”

I’m guessing for someone who really wants to crank this stuff, that is a treasure trove of a link.

ok boomer! 🙂

Slugger,

I had the same thought as Moses, then noticed the proselytizer post is the only one. Can we hope…?

Duck

Moses,

Looks like you have been set up to make a fool of yourself once again, which you have done. Smoothness is really not important here. What is important is whether one uses a distribution that allows for the presence of the third and fourth moments of probability distribution. The Gaussian does not do that, but the skewed-t (or student) does.

The first moment of a distribution is the mean. The second is the variance. Gaussian normal distributions can be fully characterized by just them. But it looks such a distribution does not fit the macro business cycle data as well as one that allows for the data to exhibit the third and fourth moments. The third is indeed skewness, which is asymmetry, and there appears to be a downward skewness in this data, which means in this case the median will be below the mean, unlike for the income and wealth distributions. The fourth moment is kurtosis (or leptokurtosis), popularly known as “fat tails,” and it looks like the data exhibits those as well, more observations in the extremes on both ends. Gaussian normal distributions exhibit neither of these at all.

Menzie was a bit off here. While he identified fat tails (the fourth moment) as “black swans,” that is not actually Taleb’s position. His view is that true black swans involve events not describable or modelable by any probability distribution, what is sometimes known as “Knight-Keynes uncertainty” (or “Keynes-Knight uncertainty” if you prefer). This kind of situation where one finds kurtosis in a measurable probability distribution is what he calls a “grey swan.” Gaussian normality is the world of “white swans.” A major focus of his is that financial market returns all pretty much have fat tails, even though finance textbooks ignore this, including widely used ones like Cochrane’s Asset Pricing. Neither “kurtosis” not “fat tails” appears anywhere in that 600 page widely used grad finance textbook, even though all traders know the data has fat tails. I have published several papers by Taleb on these matters in journals I have edited.

Ferarra, not Menzie.

And Ferrara (pardon the earlier misspelling) was very clear that he employed the term as defined in Orlik and Veldkamp, the paper he cited. Taleb may be relevant in a debate over who owns the lexicon but not so much here. This digression is looking more and more like “Moses 1, Rosser 0”, however much you may know about the math of statistics or about Taleb because the digression misses the point of the post.

Macroduck,

You are welcome to your views of “Antifragility,” but it has nothing to do with the questoin of the proper meaning of the term “black swan.” That others besides Ferrrara are mususing the term is irrelevant.

On the matter of the link Moses provided to EconLog, there is a further substantive issue involved there that is relevant to this thread. Hummel was dismissing the importance of studying the Great Depression because it violated the supposed Gaussian normal distribution of business cycle dynamics. It was an “out;lier” in his view, something to be dismissed and ignored. This fit with a longstanding view by many that sees the economy as a stable equilibrium that is shocked by Gaussian normal exogenous events. This underlies the currently dominant DSGE approach. Despite my swipe at Ferrara for the inaccurate use of “black swan,” it is accurate by him to argue that indeed business cycle dynamics exhibit skewness and kurtosis. The Great Depression is a massive reinforcement of that (along with the 1870s and 1890s), but Hummel wants to dismiss all that because, hey, Gaussian normal is how it is,

BTW, macroduck, if you are going to defend Moses, do you defend him lying and not apologizing for it?

Off-topic

I’m reading Susan Rice’s autobiography right now. And of course, being the intellectual type cat that I am, the first place I went in the book was where the pictures are.

https://www.youtube.com/watch?v=iYVO5bUFww0

I thought it was interesting, underneath one of the pictures in the book, where we see the back of President Obama’s head, Miss Rice sitting just to the President’s left, and basically a room jam-packed with white dudes, part of the caption reads:

“In this meeting I was alone in arguing that we should proceed with military strikes in Syria without seeking congressional authorization. President Obama decided to seek Congress’s approval, which was not granted, but he found a negotiated path to eliminating the bulk of Syria’s chemical weapons stockpile”

Mostly rhetorical question here, but feel feel to declare an objection: After a bloody civil war in Syria killing how many people and destroying how much resources, and donald trump cowardly running out of Kurdish territory (to please his Turkish master) without asking permission from Congress, and the Pentagon sitting around like deaf mutes as Kurds are murdered, who looks right on that NSC decision now??

Years after this decision was made, I have seen Susan Rice’s eyes literally water up and her voice inflection dramatically change when discussing chemical weapons in Syria and the deaths in and around Syria. You can tell this had an emotional impact on her. These were not Americans who suffered because of this decision–these were mostly Kurds and Syrians who ended up suffering—yet it bothers her in a deep, visceral way. This speaks incredibly highly of her as a person of very high character and morality, that she will even get emotional over a decision made, for which she has ZERO blame. She has something known in very small social circles as empathy, a trait of which America is in dire need of right now. If America ever gets back on the train tracks again—there is no justice in this world if this woman does not get a VERY high ranking job as a civilian military leader or in the State Dept. She is 105% C-L-A-S-S.

* feel free to declare an objection—- is how that should read in my comment just above. Sorry.

Moses,

Russia faces some unexpected burdens in Syria in the near term as a result of Trump’s green light to Turkey, but in the longer run, the reputational damage to the U.S. is in Russia’s favor. So is the new domestic political fracture in the U.S. that resulted. In press discussions of Trump’s decision, the point is often made that it serves Erdogan’s agenda, but it serves Putin’s, as well. Trump is truly, eternally in Putin’s pocket.

macroduck,

Russia’s “burdens” in keeping Syria out of al Qaeda’s thrall amount to what? Russia, Iran and Turkey have been attempting to undo the mess the US, Saudi prince and Gulf emirs made of Syria the past 7 years.

What “reputational damage” could the US suffer from not going to war with its NATO ally?

Trump is in Putin’s pocket as much as Harry Truman was in Stalin’s for firong MacArthur. So much mind reading because Trump is not lock step with Brookings! You are mind reading Trump like all the denouncer trooped out by Pelosi and Schiff?

Susan Rice claims corrupt Ukraine under Poroshenko was a US “partner”, whatever that means. She is a scion of the internationalist agenda run by Brookings and CFR.

Check the “whistleblower” over at OPCW concerning the scarcity of “chlorinated organic derivatives” and absolutely no report of levels observed.

Vhttps://wikileaks.org/opcw-douma/ Of course, OPCW protests but does not yield concentrations! The other two staged CW events have their cirtic including Ted Postol.

The Black Swan now is Trump’s trade war with China, the likes of which we have not seen since 1930.

Clearly, Trump has slowed international trade and made our trade deficit worse, so the question is whether Trump will cause a recession in 2020?

Will someone please advise in a definitive way?

Paul,

Don’t have a “definitive” comment, but wonder if Black Swan events are events that are anticipated prior to happening. If many investors anticipate that some activity will be the cause of a Black Swan event, could the expectation alter the impact of the event?

If we accede to Taleb’s definition, “Black Swans … are large-scale unpredictable and irregular events of massive consequence…and… models , theories, or representations…cannot possibly track them or measure the possibility of these shocks”. (Taleb, Antifragile, p.4)

AS,

Labels are problematic. Taleb offered one definition of “Black Swan”, but there are others. The original meaning of a “black swan” is something that doesn’t exist. Then, somebody noticed some black swans and “black swan” became a warning against relying on induction – I’ve only ever seen white swans, so there must not be any black swans. So a black swan (or a Black Swan – note capitalization a la Taleb) is historically something that is thought not to exist (a thing) or is unanticipated (an event). That’s not because of Taleb, though.

Taleb requires that a Black Swan be large scale and of massive consequence. The original finding of a real, living black swan did not cause economic collapse, war, political regime change or religious turmoil. So apparently, a black swan is not a Black Swan.

If I were you, I wouldn’t worry too much about any given definition of black swan. Better to define terms (as Orlik and Veldkamp did) and not worry about the “correct” definition.

Dear AS,

I can’t resist one thing in this discussion of black swans. Down at the University of Perth, their mascot, if you will, is a black swan. They are apparently more common in Australia than in the Northern Hemisphere.

I think Barkley Rosser would agree with me that black swans are fundamentally unpredictable. The expectation, if held by enough, could certainly alter an event. But the expectation, even if widely held, may not generate a lasting change if it isn’t verified by later events. For example, suppose the foreign exchange markets expect an appreciation of the dollar, that Powell will give in to pressure and go for negative interest rates, which might cause this. (It’s a strange world.) If the interest rates are not lowered, the forecast gets disproved, and the exchange rates are likely to come back down.

J.

Are you including “non-expert” advice here in your plea?? I have it at 33% he actually enacts and enforces the December tariffs. I am basing it on the fact that donald trump is in fact a COWARD and will not do something which in large part will kill his election chances.

What market bet could you make based on this 66% chance he does not enact the December tariffs?? I assume there would be some currency trades there or maybe a short-term bet on equities right before the announcement?? It also depends on how “baked in” it is to the market prices already if they have already accounted for a “delay” on the tariffs. Or you can just do what many businesses are doing now—sit on your cash. MAGA!!!!

This is NOT investment advice, more me thinking out loud. I was thinking this is pretty obvious but a “bet on equities” would be a short on some index if you thought the trade tariffs will actually be enacted. There’s good ones out there, but you have to be very careful because the longer you own one of those short bets the more the math involved on your investment doesn’t really work in an intuitive way. So most of those you’re already thinking of getting out almost before you got it. At least that was my experience when I tried it years ago. I made out on it, but I don’t think I held it over 1 week.

This is an interesting topic. Because many retirement accounts they won’t allow you to short stocks in the strict sense—but you can BUY funds that move up or down based on short bets. So if you’re using a retirement account for investments and you want some short bets to protect your principal (a highly unusual scenario but possible in a 2007-2008 type context) you can purchase the funds that go up or down on shorts, and “circumvent” that rule on shorts. In my personal/subjective opinion it’s a dumb rule, but I think it’s there with the good intention of protecting people since shorting stocks in 98% of contexts the risk is much much higher than being long on equities.

moses, you may want to consider the rising possibility that trump will not seek reelection. he may say he has cleaned the swamp as promised, but wants to return to his successful business career. he may actually be impeached. less likely, removed by the senate. he may use health reasons to step aside. his financials will reveal him to be a fraud. the military may turn its back on him. the possibilities are endless. in any event, i believe the odds are rising that he does not follow through with another election. then the gloves are off and the paybacks begin. he will tariff china to the ends of the earth. it will be scorched earth policy all the way around. this will not be a black swan event, but a very real possibility. scared animals are dangerous.

baffling,

Just a thought: As long as DoJ won’t prosecute a sitting president, Trump has reason to stay in office. At his age, four more years of (federal) legal invulnerability represents a step toward avoiding jail altogether. Fred lived into his 90s, so maybe the best his son can hope for is to limit his time in the pokey by running for a second term.

If I were Trump, I’d get Pence to do a Ford. That way, he could limit his legal jeopardy to state prosecution. Pence would agree and then run in Trump’s place.

@ macroduck

I doubt the latter would happen. Not that it wouldn’t be a smart move to possibly avoid federal charges, but that that move would involve donald trump relinquishing control to Pence—something donald trump will NEVER do. He is an unstable person–the same as Nixon. Nixon only made this move when he was looking directly at prison bars in his near future. Please don’t take this as disrespect, but a lot of people on this blog seem to be very confused about which party controls the Senate right now. That means until donald trump leaves office he has no worries of going to prison. We are in new ground here, and most (all??) people in this blog seem to be psychologically unable (NOT intellectually unable, psychologically unable) to digest what is now a fact of life—but prefer MSNBC and newspaper commentators to tell them comforting fairytales that are NEVER going to happen.

baffling

Well there….. now you’ve shoved me in a corner like a desperate bird flu and rabies infested rat. This may be one of the few things the geriatric in Virginia and I agree on (are you trying to make me question my own sanity now baffling ?!?!?!?! What an underhanded move on your part). Forcing me to admit I might agree with Barkley on a single issue, this should be a felony crime like “manslaughter to an internet acquaintance “. Vicious. I don’t see donald trump not seeking re-election. The orange leathery creature’s ego won’t allow that for starters. For seconders the orange leathery creature has a better chance of avoiding prison and penalties in the White House than it does out of the White House. Right now I put the chances of a Senate removal somewhere around 2%. I’ve tried every wishful thinking ploy I can to put that orange leathery creature out of the White House in 2020, and I see it still at 60% it wins. Now if you wanna argue the creature’s chances of losing the election are much higher than impeachment—that I will agree with you on. But even that I peg at lower than 50% chance.

moses, i agree that the possibility that he does not run again is low…for now. i think it is a possible outcome most have not considered much in the past, but i think it is an outcome that is growing in probability, not decreasing. his recent trip to the hospital is a strong indicator that health is not holding up. the presidency is much more stressful than he envisioned. i can see him rationalizing his was into retirement. for instance, he replaces rbg with a conservative and then says my work here is done. or his business documents come out and show him to be a big loser in business. i agree with you on trump and pence. trump will not give up power in that case. pence is not slick enough to pull off such a stunt either.

“As long as DoJ won’t prosecute a sitting president, Trump has reason to stay in office.”

macroduck, you have a point here. but it does create a situation where the president is above the law. senate republicans may fail in their duties with impeachment, but i think the republican brand of law and order is going to take a huge beating. especially with trump now circumventing military laws as well. it is hard to be the party of law and order when your leader acts with impunity to the law.

Dear Folks,

It is hard to argue with the graph above, but it is not an exogenous series. You have monetary restriction for all the recessions; even the 2007-2009 recession was initiated, not caused, when the Federal Reserve raised interest rates, and this pricked the CDO-led housing bubble. So the non-Gaussianity is describing other behavior; a bias towards reducing inflation by monetary restriction.

Julian

Paging Copmala Harris and Cory Booker!!!!! Paging Copmala Harris and Cory Booker!!!! You’re needed in the Reputation Rehab Unit on hospital floor 13.

https://www.nytimes.com/2019/11/25/us/politics/2020-election-black-voters.html

This “could” screw-up Barkley Junior’s Copmala Harris –Biden neck and neck photo finish prediction in South Carolina. Maybe Barkley only meant that in the “colloquial sense”. We report, you decide.

Moses,

Once again, I never said that Biden and Harris would be “neck and neck” in SC. What I said was that the outcome there would clearly indicate which of them had more support among African Americans. As of now polls indicate that is overwhelmingly Biden. My analysis was accurate, whatever their relative standing, and would still hold if their current poll positions were completelyi reversed.

This is you again making up phony and silly critiques of me, not to mention reminding folks of you lying about my noting that poll after the first Dem debate that showed both Warren and Harris ahead of Biden, which you insisted did not exist and that I had made up. You did finally admit that you were mistaken in your accusation that I was lying about it, but you still have not apologized for that lie on your part.

Are you going to apologize for lying about the claim that the infamous paper said that Native American ancestry is uniformly distributed across the European-American population, a claim you idiotically repeated again recently, pushing poor old Menzie into having to waste time in checking it out only to find out that you were lying?

Coming to an “All You Can Eat” buffet style restaurant near you:

Proper mood setting music for the documentary movie trailer—->> https://youtu.be/lV8i-pSVMaQ?t=20

https://www.nytimes.com/2019/11/24/us/politics/sarah-sanders-arkansas-governor.html

I noticed that the skew goes from -0.30 to -0.10 if you use the annualized percent change calculated by BEA and FRED rather than using log percentages.

https://fred.stlouisfed.org/series/A191RL1Q225SBEA

Perhaps some of the skew is an artifact of using logs.

Some interesting news on Devin Nunes. I’m still kind of ticked off noneconomist never told us about this stuff. Noneconomist, I told you to put your ear to the ground out in Cali. Come on man!!!!:

https://www.youtube.com/watch?v=2X_I_sX4krs

Devin Nunes has been pretending all this stuff is “closed door”. Interesting when Devin Nunez is visiting Ukraine long before the Impeachment Inquiry, talking to Pompeo, talking to donald trump, then tells people this is “closed door”??

https://www.youtube.com/watch?v=1SS0mGhc3UY

https://www.thedailybeast.com/lev-parnas-ready-to-testify-about-devin-nunes-role-in-trumps-ukraine-dirt-digging-mission-cnn

https://www.thedailybeast.com/lev-parnas-helped-rep-devin-nunes-investigations

More stuff on Pompeo and Mulvaney:

https://www.youtube.com/watch?v=fMj1uuL-6yc

Some people have theorized why Menzie put this post up. They think the focus here is Gaussian or Skewed-Student distribution. I suspect one of the reasons is Menzie just likes Mr. Ferrara as a colleague and they have a solid relationship. But I also suspect he likes the Orlik-Velkamp paper because it has results congruent with or similar data “kickout” as Baker, Bloom, Davis which for whatever reasons (all of them probably justified) Menzie seems borderline obsessed with. But I’m throwing darts in the dark there, so……

Moses,

You are probably right that friendly relations between Menzie and Ferrara are a factor here, especially that he is aware of this paper. They have coauthored at least four papers together, with Ferrara at the Bank of France. Neither orlik nor Ferrara have particularly high citations numbers, respectable macroeconomists, but not “authorities.”

The one who seems to be the bigger star is Laura Veldkamp, who is at NYU and is a coeditor of the Journal of Economic Theory. But that does not excuse her for misusing the term “black swan” in an econometric situation. It is colorful, shall we say, but distorts the meaning.

I think Menzie is genuinely interested in this issue, with indeed it being very widley the case that most macroeconomists do assume Gaussian normal shocks as driving macro outcomes, although it is clear that indeed outcomes are not Gaussian normal, being both skewed and kurtotic.

I cannot say for sure, and am not going to ask, but I suspect that he may also have been partly motivated by what I suggested earlier, especially given the timing of this post very shortly after he noted that you were making a false claim about uniform versus skewed distributions. I do not think you are in a position to say that this did not play a role in his putting up the post, although I think that was not the only reason.

Barkley Rosser: The timing of guest contributions is largely a function of the writer’s schedule and the content largely a function of my interests. They are seldom in response to a specific comment. (On the other hand, you can bet *my* posts are often a response to comments).

Menzie,

I agree, and in regard to the peso problem, etc. These ideas have been around for some time. It is the label that is new, although “black swan” has also been around for a long time, but overwhelmingly used previously in philosophical discussions of epistemology and even theology, not statistics or economics. Taleb’s bestselling book that came out about the time of the Great Recession shifted the use and made it sexy, which I think Orlik and Veldkamp, or whoever started using it to apply to downwardly skewed macro distributions with kurtosis, were probably using it for. Heck, we know sexing up a paper title tends to increase both acceptance rates and citation rates.

As it is, the deeper issue is this one of confusing quantifiable risk and non-quantifiable uncertainty, which has been going on for a much longer time than this latest goof by these authors. Thus back in 1973 or thereabouts, James Tobin published an enormously influential paper on quantifying risk, but he put “Uncertainty” in the title and in effect claimed he was solving the problem of uncertainty as raised by Keynes, which he most certainly was not. Now Tobin was a great macroeconomist and fully deserved the Nobel Prize he got, but he received criticism from quite a few people for a long time, especially Post Keynesians like Paul Davidson, on this particular point. So, this is not a new problem.

Lots of people mistakenly think that Taleb saw the crash and Great Recession as a black swan. But he explicitly did not, saying that they were grey swans, and that anybody with a shred of intelligence could see they were coming. His financial market example of a black swan was the crash in October, 1987, still the largest one day drop ever of the Dow, which did come totally out of the blue.

And 100 year floods are not black swans. They are also grey swans. They turn into black swans when one has 3 of them within a 10 year period, which has happened in some locations in recent years.

For those who are all down on Nassim, I shall tell one story, which I saw a variation of in one of those links Moses provided. It has been said that he is a philosopher, a statistician, and a trader. However, when he is with philosophers he emphasizes how he is (was actually) a trader and is a statistician; when he is with the statisticians he emphasizes how he is a philosopher and was a trader, and when he is with the traders he emphasizes how he is a philosopher and a statistician. I think there is something to that.

BTW, for the record, his PhD is actually in Management from one of the branches of the University of Paris, forget which one.

Menzie, I think it would be cool if you could invite guest contributors who can monopolize the meanings of economics/finance terminology. It shows deep professionalism on their part, isn’t catty like behavior, and could discourage dialogue in the comments section. Plus it avoids narcissists having to incorrectly tell highly credentialed guests how they “got it wrong” on a word that has multiple definitions.

Menzie, can you imagine such a person that would fit that profile?? instead of say, guest contributors such as Ferrara, allowing for multiple meanings of a word, but defining it as to how it fits the paper being discussed at that time.

I’m just trying to imagine how this word game plays out for some students on an essay exam, for example, in such a hypothetical professor’s class??. That must be “a delight” for those students to know their grade is dictated by such a prof’s subjective and singular view of what a word means. I guess it depends on the person who had made the term more popular in recent years and engaged in false flattery of the prof presiding over the exam. That’s the one definition the kids in Harrisonburg Virginia need to have handy.

Moses,

Sigh, yes, this is getting tiresome, and I have no interest in particularly picking on Ferrara who seems quite competent and whose study I largely agree with aside from my being picky about the way he used term “black swans,” which he picked up from Orlik- and Veldkamp, who misused it. But you say that I am being “singular.” Sorry, but prior to Orlik and Veldkamp (or maybe somebody they got it from) nobody was using the term “black swans” or “Black Swans” in the way they have, to represent events modeled by known but downwardly skewed with kurtosis distributions. This is not me all by myself making this up. This is how it was universally known until they came along and distorted the meaning.

Now I think I can see how people who superficially read Taleb’s book might have come to this misinterpretation. He does not go on and on about this distinction between black and grey swans, although he is clear about what it is when he does, citing Keynes and Knight and also Hayek (all of them dead now). But he spent lots of time pounding on standard finance types for assuming Gaussian normal distributions when it is obvious and well known to traders (and others such as econophysicists) that the returns are kurtotic with fat tails. So I can see how somebody sort of skimming the book might well decide that “fat tails are black swans” even though this is just simply incorrect, and not just at James Madison University singularly in my classes. Anybody who actually knows much about this knows this.

OTOH, as also noted, these folks are in good company as someone far more “highly credentialed” than anybody commenting here has basically made the same mistake, if involving different terminology. That would be the late James Tobin, of Yale and with a Nobel Prize, who confused risk and uncertainty, which is really the issue at hand. So those I have corrected are in good company. But that does not mean that they are all right or that it is fine to redefine terms to mean things that they do not, which is what has happened here.

My go to guy after Letterman retired has been Colbert. But I thought this was one of the better monologues I’ve seen in awhile:

https://youtu.be/BTNQVgxCQnk?t=181

Fair enough, Menzie. I accept that my speculation about the timing of this post was wrong.

BTW, on the matter of the traditional method of defining the meaning of “black swan,” I would say that it did not mean “something that does not exist” but “something that is assumed not to exist because none has ever been seen.” As it was, it was indeed in Australia that they first were seen.

Using both this and Taleb’s explicit identification of Black Swans with non-quantifiable uncertainty unable to be modeled by any probabiliit distrubtion as defined by both Knight and Keynes in 1921, it is clear that calling something that is expected to occur once every 100 years is not a Blackk Swan or a black swan. It is distortion by those defining it this way.

Dr. Ferrara, is it really the case that “recession probabilities estimated using Gaussian models are likely to be largely under-estimated”?

Perhaps this is true of severe-recession probabilities (tail isn’t fat enough, as illustrated in your exercise and graphs), but mild-recession probabilities are OVER-estimated by the Gaussian. Mild recessions also seem to be much more typical of recessions, so general recession probabilities may be largely over-estimated.