As of March, the FOMC’s median funds rate estimate for the end of this year was 3.4%, unchanged from December. SOFR contracts now run about 23 basis points higher than the Fed’s SEP median estimate.

For end-2027, the March SEP’s median funds rate estimate was 3.1%, also unchanged from December. Here, too, SOFR contracts run about 23 basis points above the SEP estimate.

In February, when neither Fed officials nor market participants knew about the war, SOFR contracts were pricing in a funds rate path lower than the FOMC’s median estimates. Now, SOFR contracts are higher. Market pricing often leads adjustment to the FOMC’s published funds rate projections, in part because of the SEP are published only a few times a year. February pricing might have reflected a Warsh effect that is no longer front-of-mind. It is, however, notable that FOMC members saw fit to leave their own funds-rate expectations mostly unchanged as of March 18, when the war had already resulted in the closing of the Strait of Hormuz. Note also that, in the March SEP, the end-2026 spread between the funds rate and core PCE inflation was 0.7 ppts, vs a long-run average of 1.1 ppts; as of mid-March, the FOMC anticipated running accomodative policy this year. And next year, too, though less so.

SOFR contracts aren’t pricing in tight policy, just something closer to neutral. If the Fed were to shift to even a slightly restrictive policy stance, it it would lead to a substantial market adjustment. If restrictive policy were imposed in response to higher-than-expected inflation, add even more basis points and more market adjustment.

Macroduck

A collection of current headlines suggests a sudden blossoming of spinal columns –

From CNN: Trump’s many threats of possible war crimes reach a crescendo in Iran

Forbes: Why Trump’s Bombing Of Iran’s Infrastructure Would Likely Be A War Crime

MS Now: Trump abandons all subtlety with talk of possible war crimes in Iran

NBC New York: Trump brushes off war crime concerns, repeats threat to Iran’s infrastructure

The New Republic: Iran Mocks Trump’s Deadline After Easter War Crimes Threat

Huffpost: Ann Coulter (!) Blasts Trump For ‘Committing War Crimes’ In Iran

Huffpost: Donald Trump Threatens War Crimes As Easter Bunny Awkwardly Looks On

Fox News: (Nothing I can find.)

CBS: (Nothing I can find.)

I suppose it was too much to hope that every news organization would grow a spine…

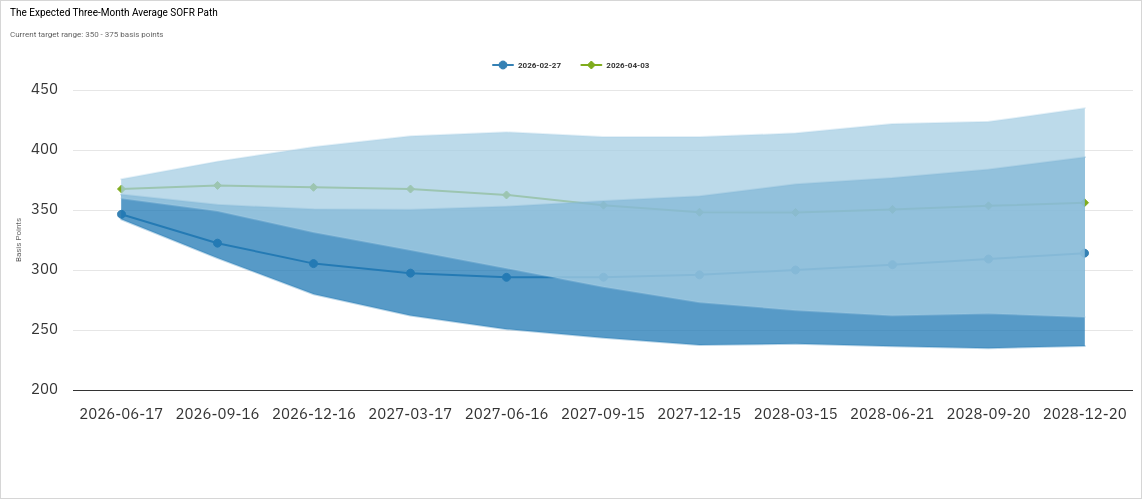

We can compare the SOFR track to the FOMC’s own estimates of the future funds rate from the March Summary of Economic Projections:

https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20260318.htm

As of March, the FOMC’s median funds rate estimate for the end of this year was 3.4%, unchanged from December. SOFR contracts now run about 23 basis points higher than the Fed’s SEP median estimate.

For end-2027, the March SEP’s median funds rate estimate was 3.1%, also unchanged from December. Here, too, SOFR contracts run about 23 basis points above the SEP estimate.

In February, when neither Fed officials nor market participants knew about the war, SOFR contracts were pricing in a funds rate path lower than the FOMC’s median estimates. Now, SOFR contracts are higher. Market pricing often leads adjustment to the FOMC’s published funds rate projections, in part because of the SEP are published only a few times a year. February pricing might have reflected a Warsh effect that is no longer front-of-mind. It is, however, notable that FOMC members saw fit to leave their own funds-rate expectations mostly unchanged as of March 18, when the war had already resulted in the closing of the Strait of Hormuz. Note also that, in the March SEP, the end-2026 spread between the funds rate and core PCE inflation was 0.7 ppts, vs a long-run average of 1.1 ppts; as of mid-March, the FOMC anticipated running accomodative policy this year. And next year, too, though less so.

SOFR contracts aren’t pricing in tight policy, just something closer to neutral. If the Fed were to shift to even a slightly restrictive policy stance, it it would lead to a substantial market adjustment. If restrictive policy were imposed in response to higher-than-expected inflation, add even more basis points and more market adjustment.

A collection of current headlines suggests a sudden blossoming of spinal columns –

From CNN: Trump’s many threats of possible war crimes reach a crescendo in Iran

Forbes: Why Trump’s Bombing Of Iran’s Infrastructure Would Likely Be A War Crime

MS Now: Trump abandons all subtlety with talk of possible war crimes in Iran

NBC New York: Trump brushes off war crime concerns, repeats threat to Iran’s infrastructure

The New Republic: Iran Mocks Trump’s Deadline After Easter War Crimes Threat

Huffpost: Ann Coulter (!) Blasts Trump For ‘Committing War Crimes’ In Iran

Huffpost: Donald Trump Threatens War Crimes As Easter Bunny Awkwardly Looks On

Fox News: (Nothing I can find.)

CBS: (Nothing I can find.)

I suppose it was too much to hope that every news organization would grow a spine…