As I watch the financial meltdown in Russia (and work on a chapter on financial crises), I am pervaded by a sense of déjà vu.

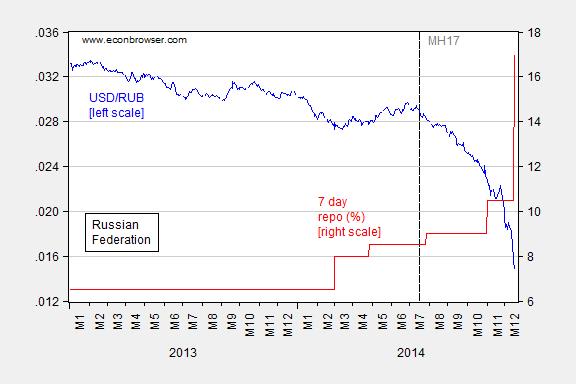

As Paul Krugman notes, the unfolding of the crisis is not mysterious, although the timing — and ferocity — is somewhat unexpected. Figure 1 depicts the collapse in the ruble even as the policy rate is hiked up, an astounding 6.5% yesterday.

Figure 1: USD/RUB exchange rate (blue, left scale), seven day repo rate, % (red, right scale). Vertical dashed line at 17 July 2014. A rise in the exchange rate is a rouble appreciation. Source: Pacific exchange service, Central Bank of the Russian Federation.

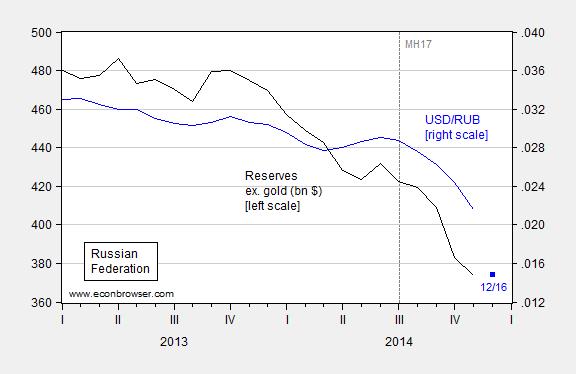

Foreign exchange reserves are being depleted at a rapid pace, even as intervention ceases.

Figure 2: Russian Federation foreign exchange reserves ex.-gold, in billions USD (black, left scale), and USD/RUB exchange rate, monthly average of daily rates (blue, right scale); December observation is for 12/16. Vertical dashed line at shootdown of MH17. Source: IMF, International Financial Statistics, and Central Bank of Russia (for September reserves), Pacific Exchange Services, and author’s calculations.

Earlier in the year, I thought targeted financial sanctions could very well have an impact.[1] [2] [3] Numerous commentators dismissed the predictions of Russian external vulnerability. What those commentators failed to foresee (as I did) was the rapid collapse in oil prices.

In addition, observers did not take into sufficient account the fact that much of Russian forex reserves are to varying degrees illiquid, as discussed in a recent Economist article:

Source: Free Exchange (Dec. 12, 2014).

In other words, reserves useful for defending the currency against speculative attacks are more like $200 billion than $400 billion. That has made the evolution of recent events much more akin to a classic Krugman first generation balance of payments crisis. It also has elements of third generation crises to the extent that balance sheet considerations complicate matters for Russian policymakers.

I would add there is an element of second generation currency crises to the extent that the increase of the policy rate to 17% is simply not credible (as Krugman alludes to). Raising the rate and maintaining it at this new level will result in a recession, and it is not clear to me that in the end Russian policymakers will endure a recession merely to defend the ruble. From Bloomberg:

The higher interest rate will crush lending to households and businesses and deepen Russia’s looming recession, according to Neil Shearing, chief emerging-markets economist at London-based Capital Economics Ltd.

For a discussion of various generations of crisis models, see this paper.

Per Steve Hanke;

“Currency Wars, the Ruble and Keynes”

A currency board is one answer Russia’s currency troubles. Along with linkage to the US dollar as most major oil producers do.

I doubt if there is any chance Putin would go that direction.

Ed

The Ruble is a buy and certain Russian stocks are a buy. That’s my reply to the Krugman saga.

http://www.acting-man.com/?p=34797 “The Russian Rubble”

Menzie, do you remember springtime 2009 ?

Does anyone else find it curious that Keynesians are all over the decline in the ruble but were calling for more and more decline in the dollar in the early 2000s? The US inflation rate from 1913-1921 was 80.8%! The inflation rate from 2000-2010 was 26.6%. Does it still make sense to debase the currency to “stimulate” the economy. According to the common wisdom of the economic talking heads Russia should be in an economic boom the way its currency had declined. Wasn’t it Krugman who called for a real estate bubble and said TARP and the Obama stimulus were not enough?

As usual, I say Krugman is wrong and irrelevant : – )

I have a much simpler explanation for the Ruble exchange rate

http://de.slideshare.net/genauer/ruble-exchange-rate-vs-brent-oil-price

The oil output of Russia is nearly constant (actually decreasing by about 1% per annon since 2005)

Whatever export earning comem in, dependent on the Oil (Brent) price, can distributed internally with perfect elasticity.

That makes Brent price times Ruble rate a constant, just adjusted for (Russian) inflation. Taking into account the slight output variation and the US inflation of about 2% gives an evem more perfect fit. And the only input is the brent price and the russian deflator.

Russia has learned in 2008/2009 that defending an arbitrary exchange rate is very expensive, and now does not really fight the “natural” rate, I defined.

Krugtrons 1979 paper was the closest to have any real world relevance, but I hvent seen any quantitative comparison to any real world event so far.

And I am still waiting for one person in this world , who can name a specific Krugman PAPER, explain in a few sentences, in his own words, what is soo good about it, and is willing to defend his judgement versus questions from me

The EIA shows that Russia’s total petroleum liquids + other liquids production rose from 9.5 mbpd in 2005 to 10.5 mbpd in 2013. However, their net exports of oil have been flat to down since 2007 (at or below 7.2 mbpd since 2007).

Based on the 2007 to 2013 rate of decline in Russia’s ECI Ratio (ratio of production to consumption), I estimate that Russia has already shipped, through 2013, about 23% of their post-2007 CNE (Cumulative Net Exports).

Jeffrey,

I took the exchange rate relevant EXPORT numbers from the CIA world factbook (5.15 mio bbl/d in 2005 and 4.7 in 2013)

Ed,

The Cato Institute, and this Anders Aslund at Peterson Institute are deadly enemies of Russia. Of course they suggest the maximum damage option of pegging to the dollar.

In Germany we are fiercely proud of the independent Bundesbank, and have instilled that in the ECB as well, and defend that against the constant vicious attacks from the Socialists. But in a situation like Russia is in now, the de facto head of the central bank would be somebody out of the small war cabinet. This is no time to go wobbly.

My take on the situation is, that we could see prices as low as 40 in January but will come back to something like 70 mid 2015, after the pain just became too much, and some folks cut production. The russian and many other exchange rate is just controlled by the brent oil price, and that will kill others first.

And what might go bankrupt, are companies, but not the government. A company going bankrupt, first kills the share holders, many in London, second the bond holders, many in the US, or … .does anybody here have data ? Then the Russian state moves in and rescues the corporation after share and bondholders are wiped out, and owns the company.

When one reads the judicial artistery some Anne Gelpern made about the Russian bond with the 60% Ukraine GDP threshold, the Russian government calling “force majeure” on corporate dollar debt unredeemable is a no brainer. Pretty simple.

When you look at the Ukrainian Dollar bonds, even the 2 year (ISIN XS0276053112) is now priced at 55%, (meaningless rate of 37% : – ). They will default in 1Q2015, maybe earlier, and that will trigger some interesting consequences

I don’t know what metric that the CIA is using, but if we look at petroleum volumes, here are the EIA data by country for total petroleum liquids + other liquids production (which I use for calculating net exports of oil):

http://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm?tid=5&pid=55&aid=1&cid=regions&syid=2005&eyid=2013&unit=TBPD

At the same website, you can get liquids consumption numbers.

Russian net exports of oil rose from 6.7 mbpd in 2005 to 7.2 mbpd in 2007, but as noted above, they have been at or below 7.2 mbpd since 2007.

And here is the EIA page for Russia:

http://www.eia.gov/countries/country-data.cfm?fips=RS

Jeff,

somehow I seem to miss whatever your point is,

your first source says 5.222 mbpd in 2005 and 4.887 in 2010, no data for 2011- 2013. your second source gives some “estimated” numbers to be taken from a graph.

Do you feel your source contradicts the CIA in any meaningful way ? And I gave you their metric “mio bbl/d”, same as what you call “mbpd”

My point is, you can forget about all those crisis metric and dynamic models, the CBR runs the simple optimization of keeping the CA slightly positive with a simple formulae

The following link shows Russian total petroleum liquids production of 9.5 mbpd in 2005 and 10.5 mbpd in 2013:

http://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm?tid=5&pid=55&aid=1&cid=regions&syid=2005&eyid=2013&unit=TBPD

And as I noted, if you click on the consumption tab on the same website, you get consumption numbers, which puts Russian net oil exports at 6.7 mbpd in 2005 and at 7.2 mbpd in 2013.

And if you click on the petroleum graphs on the second EIA link, they have complete data through 2013, and if you “hover” with your mouse in the graph, they give you the data points by year for production, consumption and net exports:

http://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm?tid=5&pid=55&aid=1&cid=regions&syid=2005&eyid=2013&unit=TBPD

And the second link shows 2005 Russian net exports of 6.7 mbpd and 7.2 mbpd in 2013.

Sorry, this link shows the net export numbers:

http://www.eia.gov/countries/country-data.cfm?fips=RS

With apologies, genauer, but this appears to be one of those rare instances when you appear to be wrong and Krugman correct.

Oil prices alone don’t completely explain the Rubles’ collapse. As Russia exports other things besides oil, and since their imports are impacted by currency depreciation, a 43% fall in the price of oil should not cause a 50% decline in the ruble, which at one point was down closer to 60%.

You want a Krugman paper which is good? How about Krugman 1998, BPEA. Now regarded as one of the most, if not the most, influential macro papers written in the past 20 years. In hit, he reintroduces the concept of a liquidity trap and shows that when short-term interest rates are zero, even large increases in the monetary base are not necessarily expansionary. Many conservative economists who hadn’t read it went on to predict that QE would cause hyperinflation.

Or how about the other Krugman 1979, where he shows that the logic of increasing returns leads to another argument for international trade quite different from the traditional Heckscher-Ohlin/Ricardian theories.

Oh, but I’m sure Krugman is really as stupid as you say he is, and that you, genauer, are every bit as bright. I’m sure it’s not just the case that you’re conservative, and don’t like it that Krugman often writes things that conflict with your deeply held priors.

Genauer – ich verstehe Dich nicht, ganz und gar nicht. What does Krugman 1979 have to do with current event? It may, but you do not seem to explain. I have little or no sympathy for Krugman, since he morphed into some cheap political hack – but, I do think his Nobel is well deserved. Krugman has pathbreaking papers in Open Economy Macro and his paper on international trade under economies of scale was almost revolutionary (although Wilfred Ethier had similar concepts around the same time, and did not get recognition…).

Manfred,

that is my point exactly.

Krugman claims in the first link “I invented currency crises, … Really” with his situation then in 1979 (defense of a currency peg with a currency account deficit and dwindling foreign reserves, and played a little bit around with some equations. What relevance to what real world situation ever ? Anybody ?

The situation of Russia now is that they still have a current account surplus, pretty sizable foreign reserves, but that their export income just goes by the oil price.

And Russia runs the optimal strategy, namely keeping a slight currency account by adjusting the exchange rate to the oil price, as I showed.

My last sentence just shows my conviction that Krugman has never produced anything but equation gimmicks, and I am still waiting for one person to show me otherwise. Just ONE paper of value.

@Genauer — The idea that the Russian government caused a crash in the currency all the way to 60 (80 at one point) on purpose in order to keep a slight trade surplus as an optimal strategy is ridiculous. On the contrary, all the evidence is that the Russian government has worked hard to prevent a depreciation. This week, they effectively imposed capital controls on their largest exporters to prevent capital flight…

This other idea of yours, that you are very smart and Krugman is an idiot is equally wrong. I like the way you selectively quote him, when what he said is that he started the modern academic literature on currency crises.

In fact, most of Krugman’s papers are quite insightful, even though many are long-forgotten. How many papers of his have you actually read? There may be an idiot in this debate, but it isn’t Krugman.

Let’s just hope that Putin plays nice and this remains a genteel academic discussion topic. Putin must be tempted to divert his base with a little activity in the near abroad? We know that Obie would react in his usual vigorous way…

sense of humor in the early morning is always good …

genauer

Perhaps they were deadly enemies of the old Soviet Union, as every liberty loving, freedom loving persons should have been. But they are not deadly enemies of the new Russia, perhaps just enemies of the expansionist direction Putin and cronies are taking the country, as again all liberty loving people should be. There is nothing wrong with pricing oil with the US dollar. Overwhelmingly the oil producers do. I would expect more criticism with a currency board solution. It restricts dictator’s power to some extent.

What is missing from the post by Menzie is a more complete picture of where and why the reserve is draining. It is not just fleeing capital, but the usual suspect looming large. Poor action by the central bank. A chart, if it could be found, of the size and direction of foreign dept, public and private is needed. The following link is one example of why the ruble is in trouble. Rosneft is example of the Russian Central Bank monetizing foreign debt, not for the benefit of the general Russian economy, but for the favored Putin cronies.

“why-the-ruble-fell-as-oil-rose”

No mystery of the falling confidence of the Ruble it is the same story played out through history.

Ed

Ed,

your link to the Berhsidsky thing, that is the typical Bloomberg blather. Gigantic overinterpretation of a particular 3 hour time slice, and then endless nearly evidence free insinuation.

It does not matter for thinking about what will be in 1 month, 6 month, 24 month, whether things do not run “normal” to spme algorithm just within 3 hours.

To provide you with referenced data to the relevant questions http://de.slideshare.net/genauer/sampler-of-gdp-and-other-data-emphasis-on-russia:

Sampler of various graphs for various discussions

page

Real (PPP) GDP per capita over time for various nations 2

Government Gross debt / GDP for various nations 3

Ruble exchange rate and Ruble * Brent product 4

German gasoline station prices 5

Russian foreign reserves history 6

Time horizon and sector of Russian foreign debt 7

President Putin Approval ratings 8

Ruble exchange rate in the week 12/15 – 12/19/2014 9

Russian export revenue and Oil Price 10

Thorstein,

1. Ruble exchange rate

In contrast to your “should”, the Russian export does reproduce pretty exactly the oil price, as I claimed and the BIS shows, http://www.bis.org/publ/bppdf/bispap78s.pdf page 298, even in the turbulent year 2008. I put some more data together, for this and other discussions at

http://de.slideshare.net/genauer/sampler-of-gdp-and-other-data-emphasis-on-russia

2. Krugman Liquidity trap paper

Let us focus on the ONE thing, I asked for, the ONE paper, and YOUR arguments, not your gut feelings nor the alleged regards of other people, the BPEA 1998 paper.

What is in there, according to you (your sentences: a / b / c) ?

a) “Now regarded as one of the most, if not the most, influential macro papers written in the past 20 years.” Not to the content, in your words. What other people allegedly think is not an argument-

b) “In hit, he reintroduces the concept of a liquidity trap and shows that when short-term interest rates are zero, even large increases in the monetary base are not necessarily expansionary.”

1. The situation was well known (PK: “ in the late 1930s and early 1940s it seemed quite natural to assume that money was irrelevant at the margin. After all, at the end of the 1930s interest rates were hard up against the zero con-straint; the average rate on U.S. Treasury bills during 1940 was 0.014 percent.”)

2. “Every real world actor (“entrepreneur “) knows that he usually faces multiple constraints (lack of labor, lack of qualified labor, time to deadline, lack of capital, lack of capital at profitable conditions, lack of (critical) machines, lack of demand, lack of land, lack of (government) permissions) of which even in normal situations usually only 1 or a very few are really critical, the famous “bottlenecks”, on which he concentrates. If you would have ever made a sensitivity analysis of a real enterprise, you would find very easily that the last 1 percent of capital cost in terms of interest rates has a negligible influence, something everybody in the real world understand.

3. That Japan was running practically zero interest rates and rapidly increasing government debt, to somehow compensate for shy high household and corporate debt, very slowly deleveraging, was also well known in 1998 (e.g. see his Table 4)

4. Kenneth Rogoff remarks in the appended discussion, that “Jeffrey Fuhrer and Brian Madigan, Alexander Wolman, and Athanios Orphanides and Volker Wieland” wrote about it with respect to Japan,before.

c) “Many conservative economists who hadn’t read it went on to predict that QE would cause hyperinflation.”

1. That doesn’t show in anyway the merit of that Krugman paper

2. Do you care to show us some verbatim, referenced evidence for that claim of yours. To me that sounds like a typical Krugman strawman.

Thorstein,

I was tempted to go on trashing numerous parts of that voluptuous (69 pages) paper, with a lot of stuff, I see as little value and in little relation to Japan, but maybe you continue first, trying to show your inside in what makes that papers worthy for you.

Again, please stick to this ONE paper first, and do not take evasion to the next 3 things. And only after we are done with this one, then we go to the next, … unless you agree that this one is unworthy : – ).

genauer,

“c) “Many conservative economists who hadn’t read it went on to predict that QE would cause hyperinflation.”

1. That doesn’t show in anyway the merit of that Krugman paper

2. Do you care to show us some verbatim, referenced evidence for that claim of yours. To me that sounds like a typical Krugman straw man.

krugman showed how a liquidity trap environment will not result in high inflation when monetary action is taken. that is the merit you need to understand. it played itself out with the many, many folks (mostly conservatives) who argued the fed and QE would result in massive inflation. krugman had a model that said it would not happen. those folks had a gut feeling (or incorrect model, take your pick since both choices are wrong) that inflation would happen. the experiment occurred and we know the outcome-no inflation. it is not a strawman argument. or are you saying the conservatives have not warned of inflation problems? our problem has been the opposite-deflation.

baffling

I had explicitely asked for ” verbatim, referenced evidence” for this alleged claim of “hyperinflation scare”, a typical Krugman strawman, blaming some anonymous, who as ” many conservative economists” should have names, dates and links to be presented on them.

I do not see a single one. Please educated me with EVIDENCE.

genauer — Apparently, you’ve missed the entire past 6 years of the economic policy debate, haven’t you? Conservative economists have repeatedly warned of the specter of inflation. For example, here’s the infamous Cato ad: http://blogs.wsj.com/economics/2010/11/15/open-letter-to-ben-bernanke/

If you look, you can find more, by Cochrane, by Casey Mulligan, Stephen Williamson, by Martin Feldstein, and many others. And Feldstein warned of the coming inflation in 2009, and as of the summer 2014 he was still warning about it. This has all been talked about repeatedly everywhere.

Now, I’ll admit here, Krugman correctly predicted that large increases in the monetary base wouldn’t necessarily lead to inflation. It is true that people who paid attention to the Great Depression also could have gotten this correct before Krugman 1998, although Krugman gave liquidity traps the first modern treatment (it was a forgotten concept in Macro — even Greg Mankiw did not include it in his textbook). But a vast majority of conservative macroeconomists did not get this right. Macro isn’t actually that difficult, and Krugman’s worldview basically allows him to get things right. It’s only compared with the likes of Cochrane/Fama/Feldstein/Mulligan/Minnesota that Krugman’s insights qualify him as a towering genius. Notice that virtually all of the Macroeconomists who accuse Krugman of being ignorant were wrong about the impact of QE, and with the exception of Kocherlakota, none have admitted they were theorizing using the wrong model.

A friend pointed out to me that the decline in the ruble is comparable to the decline in the yen but the reaction to the ruble’s fall was negative while the reaction to the yen’s fall was positive. The decline in currencies actually seems to be evidence of deflation of the dollar as I have noted elsewhere. Yet we are seeing signs of recovery, as confirmed by Menzie. Doesn’t it seem strange that deflation is considered such an evil and yet most recoveries have been in times of deflation? Shouldn’t we at least question those who make a living off of the claims of deflation?