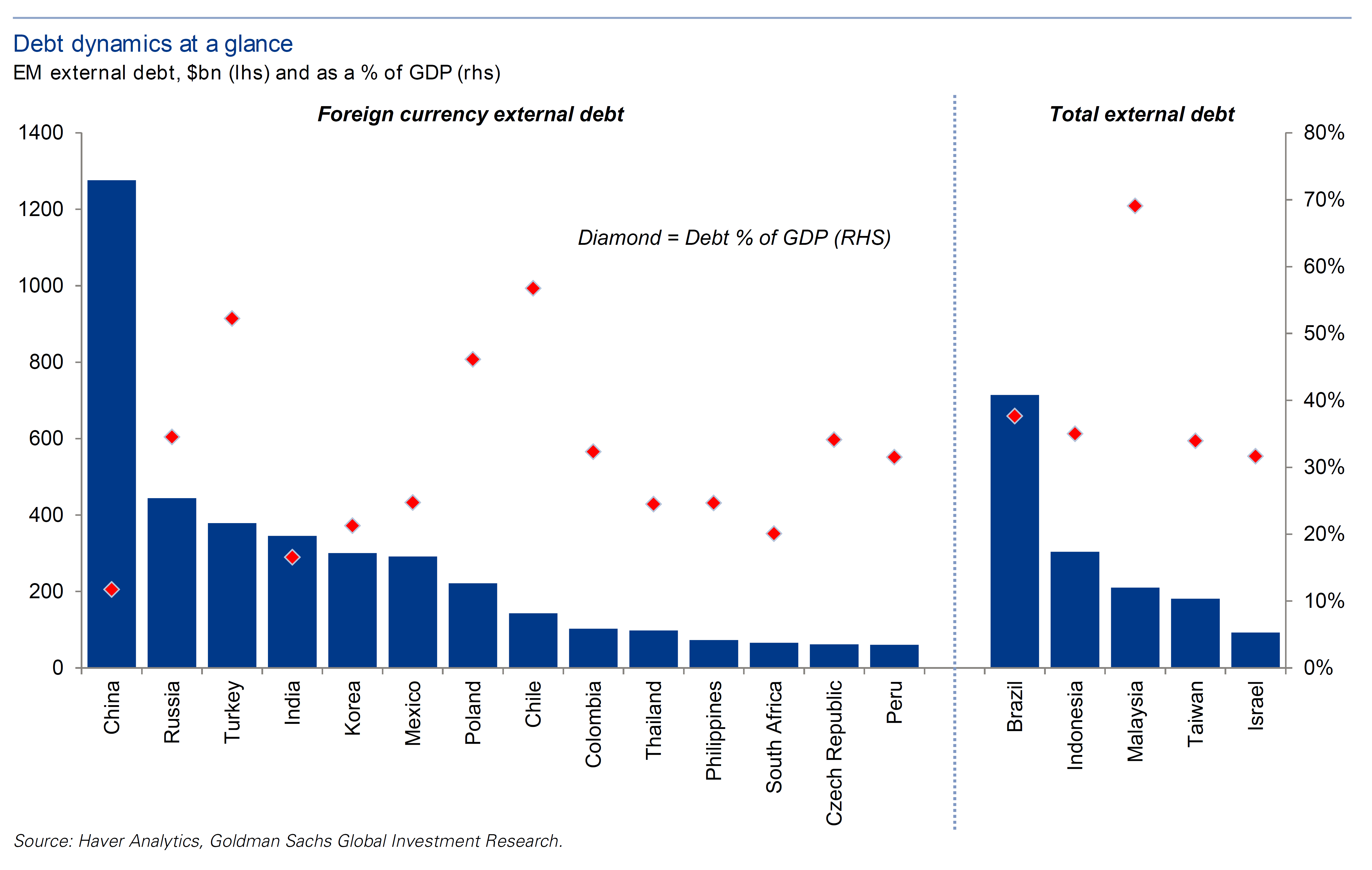

One constraint on devaluation as a means of stimulating the economy comes from the balance sheet. When there is a big stock of external debt denominated in foreign currency, a devaluation increases the amount of debt evaluated in domestic currency terms, potentially driving some firms into insolvency. How does China look in these terms?

From Goldman Sachs’ Top of Mind publication (February 9, 2016; “China Ripple Effects”) [not online]:

Source: Caesar Maasry, “The $5 Trillion Issue,” Top of Mind, Goldman Sachs, February 9, 2016.

The foreign currency debt expressed as a ratio to GDP does not seem particulary extreme. In addition, Maasry notes:

[W]hen offshore borrowings are included, China’s total external debt totals an estimated $2.1tn as of end-2Q15 (latest figures), or 20% of GDP, with 60% of total external debt ($1.28tn), or 12% of GDP, listed in foreign currency. When including onshore FX loans, the total amount of

FX debt borrowed by China’s corporate sector as of mid-2015 jumps to $1.8tn. Although this figure is sizeable, net FX debt (after deducting the corporate sector’s FX assets) is only $793bn…