We tell our students not to read too much into the strength or weakness of a currency. However, the dollar’s trajectory since November 2016 is quite striking.

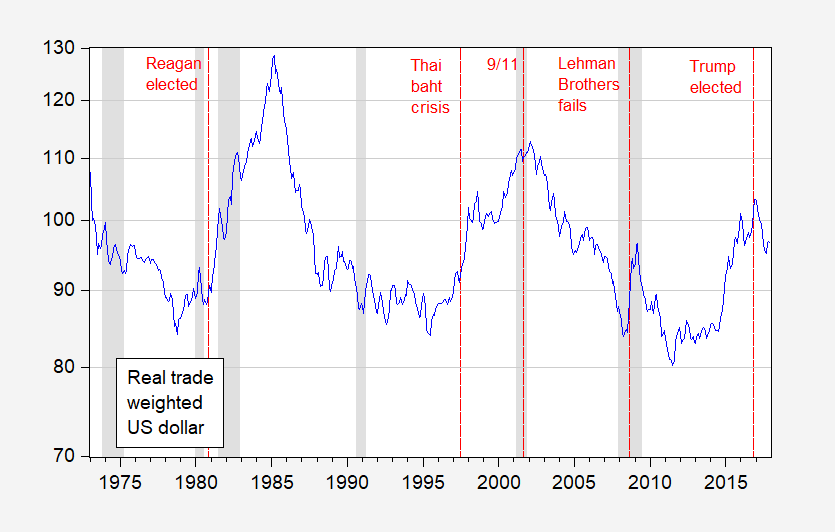

Here is the trade weighted real value of the US dollar against a broad basket of currencies, through December 2017.

Figure 1: Real value of US dollar against broad basket of currencies, 1973M01=100, on log scale. NBER defined recession dates shaded gray. Source: Federal Reserve via FRED, NBER.

It is interesting that as of December the dollar is now 2.6% weaker (log terms) than it was in October 2016; it was 6.5% 6.6% weaker than the peak in January 2017 December 2016.

This occurs against a backdrop of an expansionary fiscal policy, suggesting (1) the tax bill is not particularly stimulative, and (2) further stimulus by way of for instance an infrastructure bill has been discounted.

A weakening dollar will be helpful for keeping the trade deficit from expanding further than it otherwise would’ve. (So the question the President asked General Flynn during his short-lived stint as national security adviser was a good one!)

A year ago I would have guessed that the dollar’s trajectory would have followed the first half of the Reagan era. But that’s not what happened. My take is that shortly after Trump’s election the markets expected big tax cuts, NAFTA repeal, big deficits, blah, blah, blah. And in the immediate aftermath of Trump’s victory the dollar did appreciate. But after a few weeks the markets began to think that tax cuts, NAFTA repeal and big deficits might not happen afterall because Trump’s White House was so chaotic and ineffective at passing legislation. But then….pretty much out of the blue…the tax cuts passed at the very end of the year, and since then we’ve started to see interest rates start to climb and the dollar appreciate.

If the early Reagan years repeat themselves and the dollar appreciates the way it did in the early 80s, the brunt of Trump’s policies will fall hardest on the tradable goods sector; i.e., rust belt workers and farmers…the very demographic that voted him into office.

Some of us worried that we would get big Trump tariffs which would lead to an offsetting $ appreciation. The tariffs have not happened – at least yet. Of course the early 1980’s had a Federal Reserve in full blown monetary restraint to offset a massive Reagan fiscal stimulus. As Menzie notes – we have not seen much in the way of a Trump fiscal stimulus at least yet. And thankfully this FED has not jacked up real interest rates. Of course the Trump White House is even more confused than the White House back in 1981 with regard to macroeconomics. So who knows what the future holds.

The E.U. economy did better than expected in 2017, and the euro appreciated.

Really?

Yes, really:

https://qz.com/1163174/the-economic-surprise-of-2017-was-europes-best-year-in-a-decade/

REALLY?

https://fred.stlouisfed.org/series/DEXUSEU

Let me make this easy for you. The Euro devalued from 2014 to 2017 and then saw a partial offset. Your own story says real GDP grew by 2.2%. If you think you comment is an accurate reflection of what happened in Europe – you are even dumber than Stephen Moore.

That wasn’t really a question. I was just surprised that you would heap such lavish praise on the EU after all these years of dissing those socialist/commie/pinko/welfare loving Europeans and regularly treating us to diatribes as to how godawful EU regulations were choking growth. Will you be wearing a red beret anytime soon?

Was Bottom Trader’s latest Stupidity or Mendacity? I wonder if he even read the entirety of his own link here. 2.2% growth is considered strong. REALLY?

The arbitrary peak was, contra-Menzie’s claim, December2016. But maybe Menzie is only focusing on 2017 although his opening line is focusing on “the dollar’s trajectory since November 2016.” more than likely, it’s just Menzie being sloppy (again). ¯\_(ツ)_/¯

Menzie states that “It is interesting that as of December the dollar is now 2.6% weaker (log terms) than it was in October 2016; it was 6.5% weaker than the peak in January 2017.”:

I wonder if it was equally interesting that in Dec2009, the dollar was -6.9% weaker (log terms) than it was in October 2008; it was -10% weaker than the peak in March 2009 (possibly recession related?) ¯\_(ツ)_/¯

Wonder what Menzie thinks about the 10.8% weaker dollar in July2011 than it was in June 2010? Seems like a lot to dismiss. ¯\_(ツ)_/¯

I’m no fan of the Trump administration’s policies regarding economic policy, but I am interested in the Madison, WI cherry crop? ¯\_(ツ)_/¯

rtd: Thanks for pointing out the error of dating the peak. It’s fixed now.

I’m not sure what your other comparisons are getting at. The election of Trump revised expectations of fiscal and hence monetary policy, and we expected (and got) changes in the value of the dollar. The fact that the appreciation dissipates is of interest. The other dates you compare have no particular significance that I can think of offhand, but I’m willing to be enlightened.

“The election of Trump revised expectations of fiscal and hence monetary policy” I can certainly *possibly* agree with, but not with a net impact as monetary offset rules the day. However, if you don’t think the central bank would (can?) move to offset (potential negative) fiscal policies of the Trump administration, I’m willing to be enlightened.

rtd: Monetary policy under a Taylor rule would tend to lean more against expansionary fiscal policy as opposed to less expansionary. Hence, monetary policy in such a scenario would shrink the expansion, but exacerbate the interest rate increase. One of the more robust stylized facts is that higher real interest rates are associated with stronger currency. Hence, why the dollar (in my view) appreciated upon election. Its subsequent depreciation was due to re-assessment of the extent of fiscal stimulus (as well as some enhanced prospects for monetary tightening in eurozone).

This is standard open economy macro – nothing controversial as far as I know.

You lost me at “Taylor Rule” Hahahaha. Wtf.

Menzie

I am looking at similar curve starting in 2009.

I remember fiscal stimulus such as “shovel ready jobs”, and the 2910 tax cut continuance and fica reduction.

I’ll quote you, “This occurs against a backdrop of an expansionary fiscal policy, suggesting (1) the tax bill is not particularly stimulative, and (2) further stimulus by way of for instance an infrastructure bill has been discounted.”

Seems to correspond to a greater degree.

Or perhaps the different mechanisms can effect the “Course of the Dollar.”

Does your new paper address this?

Ed

Ed Hanson: In that case, monetary and fiscal policy were working to expand GDP, but expansionary monetary policy reduces interest rates, tending to weaken a currency, ceteris paribus. My paper does try to take all these into account by using ex post realizations of the right hand side variable, what is sometimes called an ex post historical simulation.

This line must be from a new Yorum Bauman routine: “expansionary monetary policy reduces interest rates”

Menzie

In general, you are right that it is helpful for monetary and fiscal to pull the same direction. But lets face it, often the government whether the central bank or the political class (or both) get it wrong.

Also remember there were times the fed was pulling opposite the fiscal and both were absolutely correct. The first Reagan term may be the best example of this..

Getting back today, the supply side tax reform and cuts are absolutely correct. The Fed, on the other hand, seems confused. It has consistently been unable to achieve its target, but now, after years of being below, it is tightening. I have two wishes. One, that they would be more transparent in their reasoning, and two, that its short term rates are so low, their slow rate of increase is either correct for the future or at least,harmless.

Ed

Ed Hanson: I wasn’t making a normative statement about the desirability of monetary and fiscal policy working in the same direction. Rather, I was making the point that when monetary and fiscal policy point in different directions, you are likely to get larger movements in the exchange rate than if they work in the same direction.

Menzie

That is most interesting. Just to clarify, you mean the movement as change in exchange rate, higher or lower, not volatility.

Ed

What does the recent rise in ten year yields and equity prices say about growth? We also know that expectations for growth from the consensus economics community has picked up.