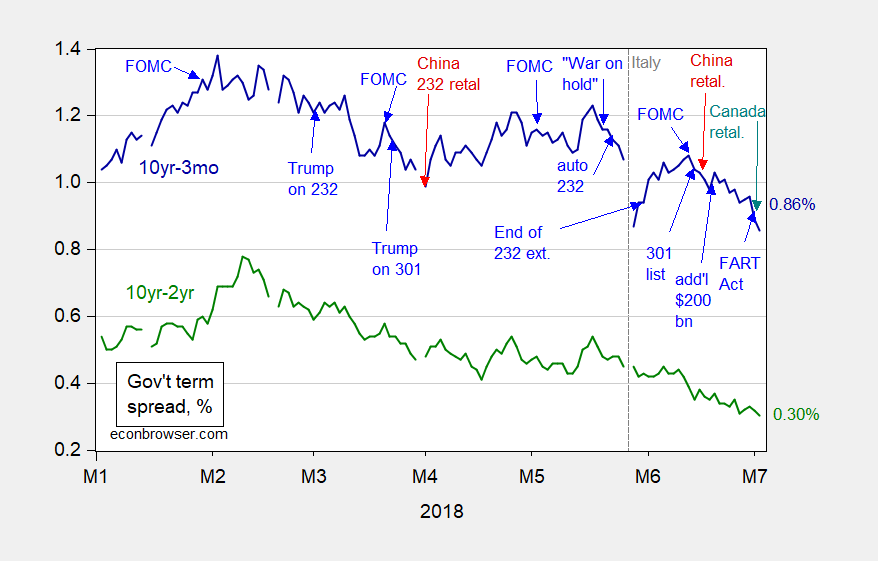

Down, down, down. 10yr-3mo at 0.86% at 2pm today. See Jim’s post for more on the spread.

Figure 1: 10 year-3 month Treasury spread (blue), and 10 year-2 year Treasury spread (green). Source: FRED, and Bloomberg for 7/2-7/3 and author’s calculations. 7/3 observation for 2pm Eastern.

Now, you might be wondering what trade policy has to do with recession/no recession as implied by the yield curve. As a recent note by Deutsche Bank (How to think about the impact of trade frictions on US GDP, 2 July 2018) observes, there are pluses and minuses to output arising from these trade action:

[H]ow [could] these trade actions could impact the macro economy[?] The threat and/or imposition of the tariffs could have potentially significant positive effects on GDP by lowering imports, but these effects would most likely be swamped by various negative effects if the tariffs are actually implemented.

Potential positives:

1. Threat of tariffs induce negotiations. The hope is that the threat of tariffs will beget larger concessions from China in negotiations to reduce China’s own trade barriers. But China may have a different view of the relative magnitude of trade barriers in the two countries. Chinese officials have said consistently that they will not negotiate under such pressure and that China will retaliate in kind to any measures the US takes. …

2. Tariffs reduce imports. …raising the total potential gain via reduced imports

to 0.5% of GDP.Negatives effects:

1. Rising prices depress consumption. The tariffs would raise the prices of imports of metals and autos from a number of countries and imports from China more broadly. The overall effect on US prices could be magnified if domestic or other foreign producers take advantage of the opportunity to raise their own prices. We estimate that the tariffs listed above could raise consumer prices in the US by about 0.6%. This increase in prices would depress real household income and consumer spending by the same percentage. With consumer spending accounting for 70% of GDP, total GDP would be depressed by more than 0.4%, offsetting most of the gain from reduced imports.

2. Retaliation depresses exports. Europe and Canada have already retaliated proportionately to the metal tariffs, others are in the process of doing so, and China has promised to raise tariffs on US exports if the threatened US measures are imposed. …raise negative impact on exports to 0.2% of GDP. If a 20% tariff on US imports of autos was matched abroad, as could be expected, US exports could be depressed by another 0.35% of GDP, bringing cumulative losses in US exports to about 0.55% of GDP.

3. Rising protectionism and declining world output depress confidence and hit financial markets.

4. Negative impact on global GDP could be similar in magnitude [to 1% of GDP]. The

disruption to global supply chains and greater dependence on world trade in many countries increases their sensitivity to the increase in uncertainty created by these trade conflicts. …

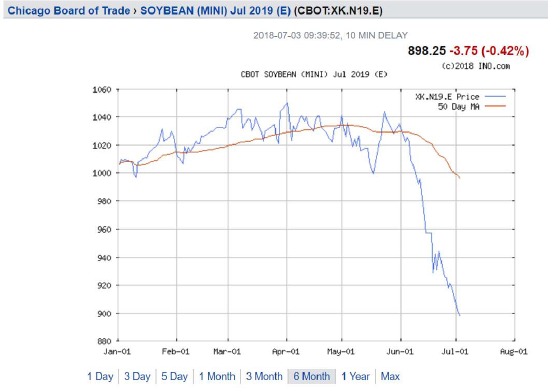

Many of the above are mere projections, and estimates. We can already see some concrete manifestations of the impact of trade policies and trade policy uncertainty on commodity prices — in particular, nearly one-year-ahead soybean futures (expiring July 2019). Planting plans and weather conditions right now should not directly affect output a year from now, so that trade policy effects should dominate. Carry costs should drive a wedge between actual and futures prices, but econometric work (Chinn and Coibion, 2014; Reichsfeld and Roache, 2011) suggest that futures are unbiased predictors of future spot prices, and smallest RMSPE among typical time series models. Now, contemplate the evolution of futures prices over the period corresponding to that in Figure 1.

Source: ino.com, accessed 7/3/2018, approx 2pm Eastern.

Just for yucks, here are yesterday’s soybean and corn prices for delivery to Iowa interior elevators:

https://www.iowaagriculture.gov/agMarketing/dailyGrainPrices.asp

Interesting stuff but I have two predictions. First CoRev will go on and on bitching about every single claim here as he always does. And you can bet the ranch PeakDishonesty will harp on the first two parts of this without noting the last two parts:

“Threat of tariffs induce negotiations. The hope is that the threat of tariffs will beget larger concessions from China in negotiations to reduce China’s own trade barriers. But China may have a different view of the relative magnitude of trade barriers in the two countries. Chinese officials have said consistently that they will not negotiate under such pressure and that China will retaliate in kind to any measures the US takes.”

I was trying to find the song on Youtube for that old weekend ag show that aired on Iowa Public TV. “Fly with me…. blablabla……… fly with me blablablabla” NO not the Sinatra song.

864 on the soybeans around mid-afternoon of the USA holiday. Even that seems significant since it was 888 not that long ago yeah?? I am kind of using 888 as a “bench mark” because 8 is lucky number in China, and that’s easy to see from that number if the drop is being persistent or maybe “sustained”. I mean it took awhile to get to 888, so if we’re seeing some more fall from 888 it’s an even more slam dunk than it already is that this is related to Trump’s decisions. You know that neither Trump nor Republicans are going to be ACCOUNTABLE for their own dumb-a$$ decisions, so we can just count off the days until the USDA subsidies on the taxpayer dole are handed out and Trump starts making things up like he took the soybean subsidies directly out of the Trump Hotel cash register. Maybe he can tell us the Russians that he launders money for with his real estate holdings “Will pay all the soybean subsidies, BELIEVE ME!!! My Russian mobster pals I launder money for will pay for ALL OF THE SOYBEAN SUBSIDIES!!!! BELIEVE ME!!!! If the Russians don’t pay for the soybean subsidies, then I am not a ‘germaphobe’ who fornicates with multiple porn girls!!!! BELIEVE ME!!!!!!”

so should be subsidize the soybean and other commodities and producers who are hurt in this trade war?

it is rather surprising all the critters on this site have nothing to say about this chart. corev (cliff claven), peakstupidity, eddie, bruuuuuce?

the silence is deadening! come on losers, let’s hear you spin a new tail on these graphs. or do you stand behind your weather and the negotiations are not finished yet arguments? those graphs gave you nothing more than a bI!t@h slap in the face, pardon my french.