Today, we’re fortunate to have Willem Thorbecke, Senior Fellow at Japan’s Research Institute of Economy, Trade and Industry (RIETI) as a guest contributor. The views expressed represent those of the author himself, and do not necessarily represent those of RIETI, or any other institutions the author is affiliated with.

How can a basketball team guard the Golden State Warriors’ Kevin Durant? Should they put a shorter man on him to stop him from dribbling? If so, the 7-foot tall Durant may shoot over the defender. Should they use two men to defend him? If so, two other Warriors’ shooters, Stephen Curry and Klay Thompson, may be open. Every choice has problems, and the ultimate test is whether the strategy works.

Economic policymaking in Asia is like this. This is clear in the case of trade imbalances between China and the U.S. Because parts and components for China’s exports flow from East Asia, China’s surpluses are actually Asian surpluses. These surpluses have generated protectionist pressures, tariffs, and a trade war with the U.S. These impediments to trade are difficult for Asia because exporting contributed to miraculous growth in Japan, South Korea, Taiwan, ASEAN, and China.

One strategy is for China to seek a truce by buying more soybeans and wheat. The problem with this approach is, because the imbalances are driven by macroeconomic factors, these purchases will not prevent large U.S. trade deficits and protectionist pressures from returning. Another strategy is for Asia to work with the U.S. to resolve the imbalances. A precedent for this is the 1985 Plaza Accord, when France, Germany, Japan, and the U.K. deflected U.S. protectionist pressures by appreciating their currencies against the dollar. The U.S. in turn agreed to reduce its budget deficit. The Accord was followed a few years later by the last current account surplus the U.S. has run. The problem with appreciations is that they squeeze the profit margins of Asian firms and reduce their exports (see, e.g., Thorbecke 2014[1]).

Exchange Rates and China’s Processed Exports

How would appreciations affect China’s surpluses? These surpluses are concentrated in the processing trade regime. Imports for processing are parts and components that enter China duty free and that can only be used to produce goods for re-export. Processed exports are the final goods produced using imports for processing. China’s global surpluses in processing trade exceeded $300 billion in every year from 2010 and 2018. Its surpluses on ordinary trade, on the other hand, rise and fall with the value of imported primary products and averaged $85 billion per year over this period.

Cheung, Chinn, and Qian[2] (2012), using the CPI-deflated real effective exchange rate and dynamic ordinary least squares (DOLS) estimation over the 1994Q3-2010Q4, reported that a 10 percent RMB appreciation would reduce processed exports by between 9 and 12 percent. Patel and Wei (2019)[3] noted that processed exports should also depend on exchange rates in supply chain countries. If Japan produces parts that go into phones that China exports, a weaker yen should increase the price competitiveness of China’s phones.

In ongoing work we have investigated how exchange rates in upstream countries affect China’s exports (see Thorbecke and Smith, 2010). We calculated a supply chain exchange rate (ssrer) as the geometrically weighted average of exchange rates in the nine countries providing the most imports for processing to China.[4] ssrer can be included in a DOLS regression together with the CPI-deflated renminbi real effective exchange rate (rmb) and GDP in OECD countries (yOECD) to explain processed exports (ex). The results are:

ext = -1.33***rmbt – 2.67***ssrert + 5.82*** y tOECD + …

(0.44) (0.95) (0.53)

DOLS (1,1) estimates. Sample period = 1993Q3-2017Q4. Adjusted R-squared = 0.968, Standard error of regression = 0.158, HAC standard errors in parentheses. *** denotes significance at the 1% level.

The results indicate that a 1 percent appreciation of the renminbi would reduce the volume of processed exports by 1.3 percent, a 1 percent appreciation in supply chain countries would reduce export volumes by 2.7 percent, and a 1 percent fall in rest of the world GDP would reduce volumes by between 5.8 and 7.1 percent. We can also use the model to perform out-of-sample forecasts over the 2018Q1 to 2018Q4 period using actual values of the independent variables. The root-mean-squared error measure of the model’s forecast error (RMSE) equals 0.386. If we exclude ssrer, the RMSE increases to 0.608. This implies that exchange rates in supply chain countries still help to forecast processed exports in 2018.

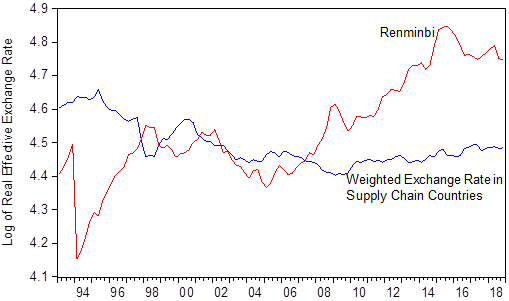

How have the renminbi and exchange rates in supply chain countries evolved? Figure 1 shows that the renminbi has appreciated 10 percent between the first quarter of 2012 and the last quarter of 2018. It also shows that ssrer has the same value at the end of 2018 as it did in the first quarter of 2012. Over this period 55 percent of ssrer‘s value has been driven by Taiwanese and Korean exchange rates and 80 percent by Taiwanese, Korean, Japanese and Singaporean exchange rates. Taiwan’s current account surplus from 2010 to 2018 averaged 12 percent of GDP; Korea’s averaged 5.7 percent; Japan’s averaged 2.5 percent; and Singapore’s averaged 17 percent. In spite of these enormous surpluses, their currencies have barely appreciated.

Figure 1. The Renminbi Real Effective Exchange Rate and a Weighted Exchange Rate of Countries Supplying Parts and Components to China. Note: The Weighted Exchange Rate is the geometrically weighted average of real effective exchange rates in the nine leading suppliers of imports for processing to China. Source: CEIC Database and calculations by the author.

Exchange Rates and China’s Electronics Exports

China’s surplus in electronics goods has averaged $330 billion per year since 2011. This equals more than half of China’s overall surplus. Electronics goods include consumer electronics, telecommunications equipment, computer equipment, electronic components, precision instruments, clock making, and optics. China’s electronics exports are produced using electronic parts and components (ep&c) from upstream countries. Exports can again be modeled as a function of the Chinese real exchange rate, exchange rates in upstream countries, and GDP in importing countries. China’s exports to major importing countries are examined. These are: Australia, Canada, the Czech Republic, France, Germany, Japan, Malaysia, Mexico, the Netherlands, the Philippines, Poland, Singapore, South Korea, Taiwan, Thailand, the United Kingdom, and the United States

To investigate how exchange rates in upstream countries affect the price competitiveness of China’s electronics exports, a weighted average of exchange rates in countries providing ep&c is constructed. Since 2000, more than 90 percent of China’s imports of electronic parts and components has come from Taiwan, South Korea, Malaysia, Japan, Singapore, the Philippines, the U.S., Thailand, and Germany. Exchange rates in these countries are used to construct a weighted exchange rate in supply chain economies.[5]

Weighted exchange rates between the leading suppliers of ep&c to China and the countries purchasing electronics goods from China are calculated using the formula:

![]()

where wrerj,t is the weighted exchange rate between the nine countries providing ep&c to China and country j importing electronic goods from China, wi,t is the value of ep&c exported from upstream country i to China divided by the value of ep&c exported from all nine upstream countries to China, and reri,j,t is the bilateral real exchange rate between upstream country i and country j importing electronic goods from China. An increase in wrerj,t represents an appreciation in upstream exchange rates relative to the country importing China’s electronic goods. The volume of China’s electronics exports to country j can be regressed on wrerj,t , the bilateral real exchange rate between China and country j (rmbj,t ), and real GDP in importing country j ( yj,t *). Panel DOLS estimation yields:

EXj,t = -1.40***wrerj,t – 1.19***rmbj,t + 1.67** yj,t * + …

(0.44) (0.39) (0.85)

Adjusted R-squared = 0.956, Standard error of regression = 0.212, Sample period = 2001-17 cross sections included. Standard errors in parentheses. *** denotes significance at the 1% level.

All of the coefficients are correctly signed and statistically significant. They indicate that a 1 percent appreciation in countries providing ep&c to China would reduce China’s electronics exports by 1.4 percent and that a 1 percent appreciation of the renminbi would reduce exports by 1.19 percent. A 1 percent increase in GDP in the importing countries would increase China’s exports by 1.67 percent. These results and the results for processed exports both indicate that appreciations in supply chain countries cause larger decreases in China’s exports than appreciations of the renminbi.

Figure 2 presents weighted exchange rates for wrerj,t and rmbj,t . The figure shows that the by this measure also the renminbi has appreciated significantly but that exchange rates in supply chain countries have not. This supports the findings in Figure 1 with very different exchange rate measures indicating that, despite large current account surpluses, exchange rates in Korea, Taiwan, Japan, and Southeast Asian countries have not appreciated.

Figure 2. The Renminbi Real Exchange Rate and Weighted Exchange Rates in Supply Chain Countries Relative to the 17 Leading Importers of China’s Electronics Goods. Note: The exchange rates are geometrically weighted averages of the renminbi and exchange rates in supply chain countries relative to the seventeen leading importers of China’s electronics goods. The weights are determined by the share of China’s electronics exports going to each individual country relative to China’s electronics exports going to all 17 countries together. Source: CEPII-CHELEM database and calculations by the author.

Discussion

There is a debate about whether the renminbi exchange rate should be included in China-U.S. trade negotiations.[6] The results presented here suggest it would be more productive to include the Korean won, the New Taiwan dollar, and the Japanese yen in the China-U.S. talks than to include the renminbi.

It would be difficult for Korea, Taiwan, Japan, and other Asian economies if their currencies appreciated. However, appreciations would disrupt trade much less than equivalent tariffs. Benassy-Queré, Bussière, and Wibaux[7] (2018) investigated bilateral trade flows between 110 countries at the Harmonized System (HS) six-digit level. They found that a 10 percent tariff reduces exports by 1.3 percent and that a 10 percent exchange rate appreciation reduces exports by 0.5 percent. Tariffs thus reduce exports three times more than appreciations do. This effect is called the international elasticity puzzle, and has also been reported by Fontagné, Martin, and Orefice (2018), Fitzgerald and Haller (2014), and Ruhl (2008).

The disruption caused by tariffs is multiplied by the uncertainty that accompanies trade wars and protectionism. Bloom (2009) showed that heightened uncertainty deters investment. Capital formation is crucial for East Asia’s flagship industry, electronics, and for many other industries. By reducing investment, uncertainty jeopardizes the ability of Asian firms to stay close to the technological frontier.

Appreciations would not only be less disruptive than tariffs and trade wars but would also benefit countries in the region by increasing the purchasing power of consumers and allowing them to import more. Cheung, Chinn, and Qian[8] (2015), using an autoregressive distributed lag model over the 2001Q1 – 2012Q4 period, reported that 90 percent of China’s imports from the U.S. are from the “ordinary trade” customs regime and that a 10 percent renminbi appreciation would increase ordinary imports by 17 percent. Thorbecke[9] (2011), using panel DOLS estimation and data from 1979 to 2007, reported that exchange rate appreciations would increase consumption imports into several East Asian countries. Updating the estimates up to 2017 confirms that appreciations in East Asia still increase imports. These results imply that stronger exchange rates may allow Asian consumers to supplant American consumers as a source of demand for the region’s exports.

To strengthen the potential for East Asia to be an engine of growth, economies in the region should establish ironclad free trade agreements among themselves. When South Korea and Japan faced off over wartime labor, the Japanese Finance Minister threatened tariffs on Korean products (Japan Times[10], 2019). When South Korea deployed the US-built Thaad missile shield, Beijing banned Chinese tour groups from visiting South Korea (Harris et al. [11], 2017). Asian countries should eschew protectionism and employ other policy instruments to address difficult issues.

To appreciate together Asian countries need to decrease the weight of the U.S. dollar in their implicit currency baskets. Ogawa and Ito (2002) noted that if an important trading partner of Asian country A puts heavy weight on the U.S. dollar, it may cause country A to do so also. This can produce a Nash equilibrium. On the other hand, if A’s trading partner put more weight on regional currencies, then it may be optimal for A to put more weight on regional currencies. This would also be a Nash equilibrium. Putting more weight on regional currencies however would facilitate a concerted appreciation against the dollar.

No Asian country wants to let its exchange rate appreciate against the U.S. dollar for fear of losing price competitiveness relative to its Asian neighbors. However, perennial surpluses put pressure on their currencies to appreciate. Policymakers should consider acceding to these market forces and allowing their currencies to appreciate together. In addition, if Japan put less emphasis on its 2 percent inflation target the yen could appreciate. If South Korea and Taiwan reduced outflows from insurance companies and government pension funds, the won and New Taiwan dollar could appreciate. If China extended fewer high interest rate loans to poorer countries, the renminbi could appreciate. None of these countries should act unilaterally though. Rather, given the intricate value chains linking Japan, Korea, Taiwan, China, and ASEAN, policymakers should view exchange rates as a regional issue and confer deeply about exchange rate policy. They could propose a deal with the U.S. resembling the Plaza Accord whereby their currencies appreciate against the dollar in response to assurances of free trade and reductions in U.S. budget deficits.

East Asia’s miraculous growth occurred as Asian countries succeeded at exporting in industries such as electronics with tight profit margins. Investments in human and physical capital and the discipline of competing in world markets contributed to learning by doing and productivity growth. Exchange rate appreciations could act as a stick and open markets abroad as a carrot to goad Asian firms to continue assimilating technologies and innovating.

References

Bénassy-Quéré A, Bussière, M.& Wibaux, P. (2018). Trade and currency weapons. CESifo Working Paper Series 7112.

Bloom, N. (2009). The impact of uncertainty shocks. Econometrica 77, 623-685.

Cheung, Y.-W., Chinn, M., and Qian, X. (2015). China-US trade flow behavior: The implications of alternative exchange rate measures and trade classifications. Review of World Economics 152, 43-67.

Cheung, Y., Chinn, M., and Qian, X. (2012). Are Chinese trade flows different? Journal of International Money and Finance, 31, 2127-2146.

Fitzgerald, D. & Haller, S. (2014). Exporters and shocks: Dissecting the international elasticity Puzzle. University College Dublin School of Economics Working Papers 201408.

Fontagné, L.Martin, P., & Orefice, G. (2018). The international elasticity puzzle is worse than you think. Journal of International Economics , 115, 115-129.

Harris, B., Jung-a, S., Ju, S., and Hancock, T. (2017). China bans tour groups to South Korea as defence spat worsens. Financial Times, March 3.

Japan Times. (2019). Finance Minister Taro Aso ponders tariffs in spat with South Korea over wartime labor, March 12.

Ogawa, E., & Ito, T. (2002). On the desirability of a regional basket currency arrangement. Journal of the Japanese and International Economies 16, 317-334.

Patel, N., & Wei, S. (2019). Getting exchange rates right. Web blog post. www.project-syndicate.org, 17 April.

Ruhl, K.J. (2008). The International Elasticity Puzzle. New York University Stern School of Business Working Papers 08–30.

Thorbecke, W. (2014). The contribution of the yen appreciation since 2007 to the Japanese economic Debacle. Journal of the Japanese and International Economies, 31, 1-15.

Thorbecke, W. (2011). How elastic is East Asian demand for consumption goods. Review of International Economics, 19: 950–962.

Thorbecke, W, & Smith, G. (2010). How would an appreciation of the RMB and other East Asian currencies Affect China’s exports? Review of International Economics, 18, 95-108.

Footnotes

[1] http://www.cepii.fr/CEPII/en/publications/wp/abstract.asp?NoDoc=4772

[2] https://www.ssc.wisc.edu/~mchinn/cheung_chinn_qian_JIMF12.pdf

[3] https://www.project-syndicate.org/commentary/real-effective-exchange-rate-global-value-chains-by-nikhil-patel-2-and-shang-jin-wei-2019-04

[4] Over the 1993-2018 sample period, the average value of imports for processing coming from each economy individually relative to the value coming from all nine economies together was: 0.268 for Taiwan, 0.258 for Japan, 0.231 for South Korea, 0.080 for the U.S., 0.046 for Malaysia, 0.039 for Thailand, 0.034 for Singapore, 0.024 for Germany, and 0.022 for the Philippines.

[5] Over the 2001-2017 sample period, the average value of electronic parts and components coming from each economy individually relative to the value coming from all nine economies together was: 0.230 for Taiwan, 0.183 for South Korea, 0.177 for Malaysia, 0.173 for Japan, 0.082 for the Philippines, 0.057 for the U.S., 0.051 for Singapore, 0.035 for Thailand, and 0.012 for Germany.

[6] https://www.project-syndicate.org/commentary/america-china-trade-deal-renminbi-exchange-rate-by-kenneth-rogoff-2019-05

[7] https://ideas.repec.org/p/cii/cepidt/2018-08.html

[8] https://www.ssc.wisc.edu/~mchinn/CCQ_RWE2015.pdf

[9] https://www.rieti.go.jp/jp/publications/dp/09e006.pdf

[10] https://www.japantimes.co.jp/news/2019/03/12/national/politics-diplomacy/finance-minister-taro-aso-ponders-tariffs-spat-south-korea-wartime-labor/#.XNCAcfZFzpM

[11] https://www.ft.com/content/9fc4b1b4-ffb1-11e6-96f8-3700c5664d30

This post written by Willem Thorbecke.

A very detailed and well reasoned discussion of the actual issues and economics. Of course it is WAY over Trump’s mental capacities so I guess he will have to turn to his economic advisers to give him this drawn in crayons and emojis for him. Of course his economic team includes clowns like Kudlow and Wilbur Ross so that it not going to work.

OK – maybe our Usual Suspects can perform this needed service for their leader Trump. Then again we will need to draw this in crayons and emojis for them first.

“In spite of these enormous surpluses, their currencies have barely appreciated.”

And all of these countries have massive foreign exchange reserves. The only way you get such reserves is by intervening in foreign exchange markets to depress your currency. This strategy is far and away more effective than tariffs for producing trade surpluses and importing aggregate demand from abroad, as it is equivalent to simultaneously taxing your exports and subsidizing your imports.

“They found that a 10 percent tariff reduces exports by 1.3 percent and that a 10 percent exchange rate appreciation reduces exports by 0.5 percent. Tariffs thus reduce exports three times more than appreciations do. This effect is called the international elasticity puzzle, and has also been reported by Fontagné, Martin, and Orefice (2018), Fitzgerald and Haller (2014), and Ruhl (2008).”

I suspect this is just a case of omitted variables. Currency appreciation can come from conscious policy (reduced foreign exchange accumulation, for example), but it is probably most often endogenous, for example, a result of productivity growth, in which case on would not expect it to have an adverse effect on the trade balance.

I agree that this was a well reasoned piece. I wonder how long the U.S. global deficits can last before there is a reckoning. A decade more? Three decades more? As Stein famously noted (I’m paraphrasing) “When a thing can’t keep going as it has been, when it simply can’t continue, …. it won’t”

Of course, I’m poking fun of my own lack of math skills here, but sometimes it pays to skip large portions of math in the paper and get straight to the text. See here:

“They could propose a deal with the U.S. resembling the Plaza Accord whereby their currencies appreciate against the dollar in response to assurances of free trade and reductions in U.S. budget deficits.”

Regarding the last part of that sentence, exactly which fantasyland world were they expecting this to happen in?? Would that be “Westeros”, “Arda”, “Middle-earth”, the “Enchanted Forest”, “Narnia”, “Valhalla” or the “Black Fortress” spaceship in “Krull”???

Moses, you said it slightly differently than I was formulating, but you hit the nail on the head.

This is a nice piece, and at least a couple of steps ahead of the current situation. The political implication is that an Asian currency bloc capable of coordinated negotiation and action (under Chinese leadership?) is required, and that’s a little spooky from the American perspective, although I guess the abandonment of TPP was a step in that direction, and certainly if your referent is the 1985 Plaza Accord, it comes with the territory. Hmm . . . .

For the time being, we are getting a real time test of the payoff matrices that have been posted a couple of times on this website. My guess is that the Chinese have decided that they can afford a trade war started by the United States, and given the differential in growth rates between the American and the Chinese economies, it may well be that, for China, the pain in relatively more tolerable. I don’t know, but from the peanut gallery, I’d guess that the current global IP regime will be a casualty of the conflict, sometime after the American farmer, but before the almighty Dollar. Hold onto your hats, and don’t assume peace is either government’s current objective.

Why is the CEO of John Deere frustrated with Trump’s trade war?

https://finance.yahoo.com/news/deere-fiscal-2q-earnings-snapshot-102637816.html

“Deere cut its profit and sales expectations for the year as a trade war between the U.S. and China escalates and farmers try to recover from a planting season besieged by heavy rains. Prices of soybeans targeted by Chinese tariffs last year fell to a 10-year low this week as the countries traded jabs. “Ongoing concerns about export-market access, near-term demand for commodities such as soybeans, and a delayed planting season in much of North America are causing farmers to become much more cautious about making major purchases,” Deere Chairman and CEO Samuel Allen said in a prepared statement Friday.

The warning from Deere pulled the entire S&P industrial sector down on fears that the nation’s largest manufacturers will see similar damage. Deere now expects to earn about $3.3 billion in 2019, down from its forecast three months ago for profits of about $3.6 billion. The company is less optimistic about revenue as well, lowering its forecast of a 7% increase, to just 5%.

Company shares slumped 6% to a new low for the year. China has targeted U.S. farmers , particularly soybean farmers, in retaliation for tariffs put in place by the Trump administration. The effects of China’s actions have not taken full force in the U.S. Farm Belt.”

Samuel Allen made very similar comments back in February 2019 when their previous quarterly earnings also came up below expectations.

Banco John Deere S.A. is John Deere’s Brazilian affiliate that manufactures and sells equipment to Brazilian farmers. While the John Deere production in the U.S. has declined in large part because Midwest farmers are not selling that much in the way of corn and soybeans to China, overall John Deere revenues were strong in 2018 in large part because Banco John Deere S.A. is doing incredibly well selling equipment to Brazilian soybean farmers. Make Brazil Great Again!

“And all of these countries have massive foreign exchange reserves. The only way you get such reserves is by intervening in foreign exchange markets to depress your currency.”

The reason all of these countries have such massive foreign exchange reserves is because the IMF brutally abused them during the Asian Financial Crisis in the 1990s. They learned a hard lesson that if they did not protect themselves from western hegemony, they would be under the thumb of the west forever.

The sociopaths at the IMF, under the control of the US Treasury officials, instead of heading off the crisis by doing their job as lender of last resort, applied brutal moralist austerity measures that cause widespread misery and depression. Some story as always, bailouts for the reckless bankers and oppression of the innocent citizens.

So these countries learned their lesson well. Never count on the IMF for anything and do everything you need to protect yourself from the elite monsters, which means keeping larger foreign reserves.

Do you honestly believe that? By far the biggest stocks of foreign reserves are held by Japan and China. I doubt either country amassed their reserves in fear of IMF bullying. A much more believable story is that Japan used the tactic to spur export-led growth (a strategy started well before the Asian Financial crisis) and China followed suit.

Pull out your smart phone as you read this:

“This is clear in the case of trade imbalances between China and the U.S. Because parts and components for China’s exports flow from East Asia, China’s surpluses are actually Asian surpluses. These surpluses have generated protectionist pressures, tariffs, and a trade war with the U.S. These impediments to trade are difficult for Asia because exporting contributed to miraculous growth in Japan, South Korea, Taiwan, ASEAN, and China…How would appreciations affect China’s surpluses? These surpluses are concentrated in the processing trade regime. Imports for processing are parts and components that enter China duty free and that can only be used to produce goods for re-export. Processed exports are the final goods produced using imports for processing. China’s global surpluses in processing trade exceeded $300 billion in every year from 2010 and 2018. Its surpluses on ordinary trade, on the other hand, rise and fall with the value of imported primary products and averaged $85 billion per year over this period…Patel and Wei (2019) noted that processed exports should also depend on exchange rates in supply chain countries. If Japan produces parts that go into phones that China exports, a weaker yen should increase the price competitiveness of China’s phones….The figure shows that the by this measure also the renminbi has appreciated significantly but that exchange rates in supply chain countries have not. This supports the findings in Figure 1 with very different exchange rate measures indicating that, despite large current account surpluses, exchange rates in Korea, Taiwan, Japan, and Southeast Asian countries have not appreciated.”

If Foxconn (China) was paid $250 for your smart phone, it paid $225 for components made in Japan, Korea, and Taiwan and only $25 for its labor and the return to its capital. This is the basics of processed trade, which the Idiot in Chief has never grasped. Too bad none of those clowns he calls his economic advisers get this basic point.

Germany, Japan and China are all mercantilist countries. China provides labour for the former two.

Note:

1. China’s own industrial production is too volatile to predict (just as the US’s).

2. However China’s Total Export is very stable to predict.

US’s industries cannot freely trade in China, as tech, media, publishing. Basically most of those that US is competitive in. Menzie: you should read the entire Wikipedia article on WTO and re-quote it here for your anti-US mob. Check at the same time China’s state directorate policy regarding those industries.

Don’t fixate on soybean. You should check soybean milk price and all processed products’ prices. Ask your friends in shipping and trading.

If you’re proud of and your self-défense is being intellectual, your should work more.

Did you check GBP3M vs SP500 through 2018-2019, why didn’t you update the post or do a new one?

Germany and Japan are mercantilist? Utter rubbish. The Euro floats, the yen floats, and both nations are less protectionist than Trump’s America. I guess they legalized weed in your neighborhood as you are clearly smoking something.

Zi Zi has written similar nonsense before:

“Did you check GBP3M vs SP500 through 2018-2019, why didn’t you update the post or do a new one?”

I think this troll is talking about the 3-month LIBOR UK rate but who knows with his insane ranting.

https://fred.stlouisfed.org/series/GBP3MTD156N

This UK rate has bounced between 0.82% and 0.94% over this period. WTF this has to do with the S&P 500? Zi Zi does not know but he sure is off on his usual angry and incoherent rants!

“Germany, Japan and China are all mercantilist countries.”

Don’t drink and post, boy.

Foxconn’s Taiwan boss is running for Taiwan president. Now you see the grand plan, Professors?

(The cross-Atlantic slave trades were cooperated by African kingdoms; some of whom continued the trades after the UK abolished it.)

Zi Zi cannot even tell us the name of this very successful Taiwanese business man? Hey Zi Zi – his name is Terry Gou.

https://www.businessinsider.com/foxconn-ceo-terry-gou-taiwan-president-sea-goddess-mazu-2019-4

“The billionaire founder and CEO of Foxconn, the Taiwanese electronics supplier, is running for his country’s presidency because he said a sea goddess told him to do so. 68-year-old Terry Gou announced on Wednesday he will take part in the Kuomintang party’s upcoming primary elections. If he advances in the primaries, he will take part in the self-governing island’s 2020 presidential race. Gou said he was encouraged to run under the instruction and blessing of Mazu (or Matsu), a popular Taoist and Buddhist figure who is regarded as the patron of the seas.”

Yea a bit odd. But here is something else that Zi Zi cannot be bothered to tell us. Gao is retiring as the CEO of Foxconn. He is also calling for closer ties to China and less close ties to the Trump Administration.

A very well-reasoned and thought through analysis. Highly appreciated.

pgl do you understand the Germany, Japan’s industrial, economic policies? Social traditions?

Yes their currencies float, but are they “too” strong or “too” weak? “Too” strong — well that’s caused by US’s pressure. So either Europe opens up their border and get cheap labour, or Japan goes into a dormant state with all the “zen”.

Domestically, inside these two countries there’re asymmetric tariffs. I don’t have time to write why the societies, industries are organised like this in these challenger nations.

Basically this is a deeply US-centric, uni-polar world. The challenger nations have their own problems though. However the status quo could change at any moment cuz newcomers keep pushing with whatever means.

“dno you understand the Germany, Japan’s industrial, economic policies? Social traditions?”

Like you do. Sorry dude but not feeding trolls like you.