Today, we are pleased to present a guest contribution written Hiro Ito (Portland State University) and Robert N. McCauley (formerly Bank for International Settlements). The views presented represent those of the authors, and not necessarily those of the institutions the authors are affilliated with.

One basic role of international financial markets is to share risks across economies. For instance, investors swap the equity of firms at home for those abroad in order to diversify away from sources of loss that are unique to the domestic economy. In an ideal world of complete risk-sharing, domestic investors would bear such a loss only to the extent of their share of world wealth (“CAPM”).

Thus, a small economy would lay off on the rest of the world almost all risk that is unique to it. Natural disasters pose such a risk. In theory, financial markets might spread their risk around the world to approach the ideal.

However, the reality is different.

The losses from the 2011 earthquakes in Japan remained in Japan, while reinsurance spread the losses from that year’s New Zealand earthquake to the rest of the world. Furthermore, the losses remaining in Japan are much larger than the CAPM theory suggests. Even the losses that New Zealand shared through reinsurance fell well-short of the nearly 100% the theory suggests.

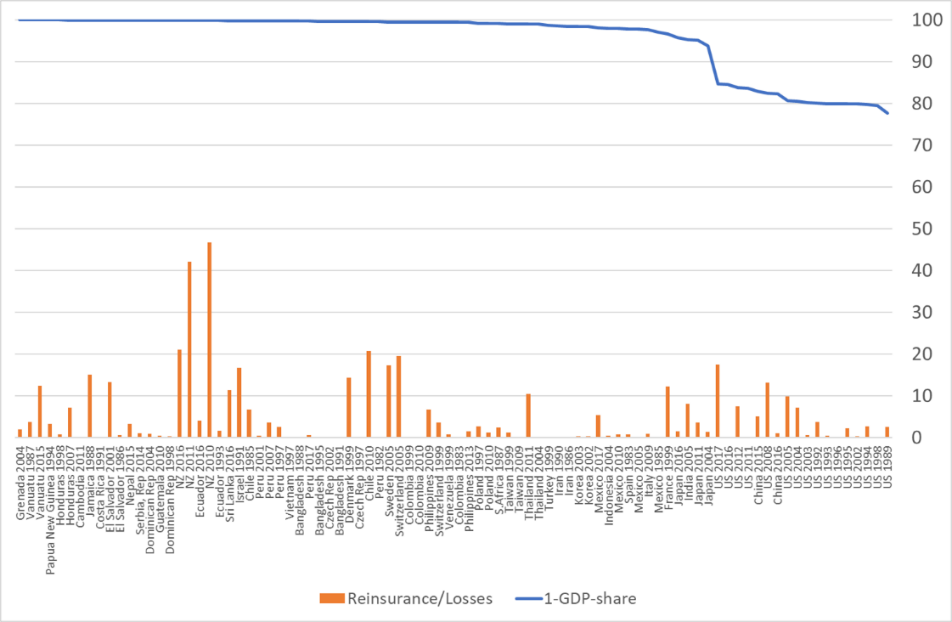

Our recent paper (Ito and McCauley, 2019) finds that losses from natural disasters are shared internationally to a generally very limited extent. We find the mean portion of economic losses received offset by reinsurance is less than 5%. On a value-weighted basis, the degree of international risk-sharing is still only 7.5%. These findings are far below a textbook norm of full international risk-sharing. This finding of home bias in disaster risk-bearing poses a puzzle of international risk-sharing (Figure 1).

Figure 1: Shortfall of reinsurance coverage of disaster losses relative to a CAPM-type ideal distribution of risk

In this paper, we use data compiled by Munich Re, a major reinsurer, on the largest natural catastrophes. These give us estimates on the monetary value of the direct losses and the fraction covered by insurance. We then search balance of payments data to identify related receipts of reinsurance payments from the rest of the world. This method identifies for the first time the cross-border flow of reinsurance payments to 88 economies that experienced insured disasters in the 1985–2017 period. Using the data, we decompose international risk-sharing into the portion of losses insured and the portion of insurance that is internationally re-insured.

We find that the failure of international risk-sharing begins at home with low participation in insurance. That is, the lack of insurance coverage is the overwhelming factor in the shortfall of reinsured loss from the textbook level (Figure 2). The contrast of international risk-sharing of the losses from the 2011 earthquakes in Japan and New Zealand arises mostly from the coverage of insurance.

Figure 2: Decomposition of the shortfall into insurance cover and reinsurance. Sources: NatCatSERVICE data; IMF balance of payments data; authors’ calculations.

Regression analysis points to economic development and institutional/legal quality as important determinants of insurance participation. The reinsurance share is related to small size, as theory would suggest, while higher levels of international reserves holding are also found to be positive contributors. As a form of international financial integration, the international reinsurance share is also positively related to overall de facto international financial integration (as measured by the ratio of international assets and liabilities to GDP). In addition, we also find that more internationally wealthy economies reinsure less, suggesting that net foreign assets substitute for international sharing of disaster risk.

The lack of international risk-sharing against the background of low insurance coverage poses profound questions about the role of government. The practical alternative to ex ante insurance, however organised, seems to be demand for government spending to serve as ex post insurance. Indeed, the trend in both Japan and the United States looks to be toward greater spending in relation to disaster losses over time.

The difficulty is the empirical observation that those advanced economies which enjoy less international risk-sharing also enjoy less fiscal space. Thus, the realization of a disaster risks ratcheting up already high public debt levels. In this manner, disaster risk can morph into financial risk. Bond holders should insist that the government should implement policies to identify and better-share disaster risks. Large-scale natural disasters, including those which are increasingly affected by climate change, tend to require the central government to provide an implicit backstop for insurers or local governments and to function essentially as ex post de facto insurer.

This post written by Hiro Ito and Robert McCauley .

Something about “rational actors”…….. buduh buduh buduh…….. ?? I’m getting older, the sensory neurons aren’t firing like they used to and I have no nearby access to alcohol which increases my social anxiety. Could be the farther your life stretches out to eternity the less empirical evidence you have that the players are…….. rational. As I said the sensory neurons aren’t firing like they once were. The ghost of Weitzman was calling out to me from the dark void and told me if I don’t have any immediate feelings of dyspepsia and I still have a shot at “Citizen of the Year” in Yates Center Kansas I should hold out for 2-3 more days just to see what happens.

https://www.reddit.com/r/brexit/comments/d0e0z3/live_footage_of_boris_johnson_leading_the_uk_out/

INdirectly related to the topic:

https://arstechnica.com/science/2019/09/crops-under-solar-panels-can-be-a-win-win/

This home bias aka the lack of international risk-sharing is certainly not helped by those MAGA hat wearing America first types. I guess it would help if the Trump Administration would join the rest of the world in terms of dealing with climate change to reduce the incidences of disasters. It would also help if we raised taxes to address that lack of fiscal space issue. Of course the know nothing Republican Party is against tax increases and all for undermining any attempt to address climate change.

No maybe FEMA will do good by helping the Bahamas. FEMA certainly came up short in terms of helping Puerto Ricans after Maria. And some of us thought people in Puerto Rico were Americans. Oh wait – BROWN Americans do not count in the Trump White House. Never mind.

Out here in the Gamma Quadrant of California (Urban Wildlands Interface) insurance companies are laying off risk by canceling home owner’s fire insurance. If they don’t cancel they jack rates to unaffordable. Local agencies could deny permits to build. Or change codes to require fire proof bunker construction. In some areas codes require a 5000 gallon fire water tank in new construction.

Human nature will go back to business as usual if we get a couple of years of no large fires. The media and politicians will go back to obsessing about the next new bright and shiny thing.

The last sentence may be the only solution.

“Large-scale natural disasters, including those which are increasingly affected by climate change, tend to require the central government to provide an implicit backstop for insurers or local governments and to function essentially as ex post de facto insurer.”

Today’s hardcopy NYT has a story about $62 million that was supposed to go to a school going to the wall. The “very stable genius” is also flying up the flag pole the elimination of a decades old refugee program. I’m still seeing TONS of farmers and truckers praising him like he’s King Solomon and upper income enjoying the free for all on regulations, killing of Net Neutrality etc. Did life really get better after Reagan?? You even see papers like the NYT and “liberal” pundits speak of Reagan in glowing tones, and no one discusses how deficits were much worse during Reagan’s time. We’ve got people like David Brooks in a “liberal” paper writing crap I could get a 12 year old in the Young Republicans Club to write and holding his snob nose in the air every time he says “identity politics” in condescending tones as if he himself only had created the term yesterday. In fact the term means nothing—it’s just another way to refer to economic class wars—which the Republicans are the ones who started that–now they decided the phrase “economic class wars” makes them look like the A-holes they truly are, so if we can change the common lingo to “identity politics” maybe we can get some poor person to feel shame that they might want to quit getting stepped on by people like donald trump who can never have enough. Brooks gets paid to tell us “Well I don’t like donald trump, I mean I really really don’t like him, but my job is to make you feel apathetic about it while I collect a paycheck, so just think of my NYT columns as lube and bendover people”

This country is going to get what it deserves if it votes for MAGA again in 2020 (I’m putting it at 60% right now trump wins a 2nd term) , and I am beyond caring about a general populace that can’t be bothered to read anything. Does anyone here feel sorry for Italy right now?? Why the hell would they?? So why in the hell should I care about their intellectual counterparts walking around at your nearest American Wal Mart??

did this study control for the impact of national design codes? in general, the wealthier a nation, the better their design codes and resulting construction to natural disasters. think california for earthquakes and hurricanes for south florida. yet those codes are not even uniform within a single nation like the use, as the midwest designs against neither of those natural disasters to any significant extent (although that is also because we get no losses from those natural disasters in the midwest either). there are some poor countries who do not design well (think haiti and earthquakes), while chile (which i do not consider prosperous) actually is pretty resilient against earthquakes. my point is that good design codes reduce the risk (and risk sharing) while poor design codes increase the risk of large scale damage and cost.

i guess this also relates to the magnitude of the natural disaster as well. for a hurricane, good design codes will defend cat 3 very well. poor design codes may fail miserably at cat 2. neither will handle a cat 5 without catastrophic damage. so a cat 3 storm subjects uneven damage on an area depending upon the quality of the construction (and thus economy), but a cat 5 is going to damage both immensely. similar arguments are to be made with earthquakes. miami would look like the bahamas right now if dorian had sat over south florida for 36 straight hours at 185 mph.

so while i think the results of this study are quite interesting, my question is simply how many hairs did you split when doing the analysis with respect to both quality of the design codes in the specified country as well as magnitude of the natural hazard that caused the damage? and were underinsured areas ill prepared for an expected hazard, or was the hazard of much greater magnitude than historically expected in that area?

From what I saw in photos of the damage around Marsh Harbor, water was the source of damage to well built structures.

Gee, I wonder why Youtube took down the video for this. It’s so much better to watch with your own eyes a man who probably can’t stop himself from talking like a sorority girl with the maturity of a 14 year old after he had 1 and 1/2 bottles of beer at lunch. That way we can judge “as an individual” a “writer” who stereotypes groups inside the same column where he complains about people who stereotype.

https://thinkprogress.org/david-brooks-a-republican-senator-put-his-hand-on-my-inner-thigh-for-a-whole-dinner-party-25d266a521a4/

Is this girl Bari Weiss one of Brooks’s cousins?? Because people who put ignorant views up in the NYT that are supposed to pacify the masses while they take a dump on your head are so much better than people who express themselves on blogs or social media, everyone knows that. Because people using their notoriety from being another NYT columnist douche to sell pop psychology books have much more “moral justification” for politically venting than those dirty people on blogs or social media do. Everyone knows that. Some vulgarity in this first link.

https://www.youtube.com/watch?v=jS-sxJFn6O0

Matt Taibbi and Alex Pareeve, reading from a very “deep” column by David Brooks titled “Spinners and Tuners”. This was risky because David Brooks says it’s a felony to criticize David Brooks, so you have to be careful, you can only criticize people in newspapers, you can’t do it in other online forums because David Brooks says that’s like “icky” and lower-class behavior if you criticize him online.

https://youtu.be/z9nB_I5e3nw?t=128

It’s a New Hampshire Public Library folks. Where else did you think our wise military veterans and bright young minds would be hanging out?? Cool T-shirts too

https://www.youtube.com/watch?v=TnOt3MRfrVc

Calculation/decision costs are not small.