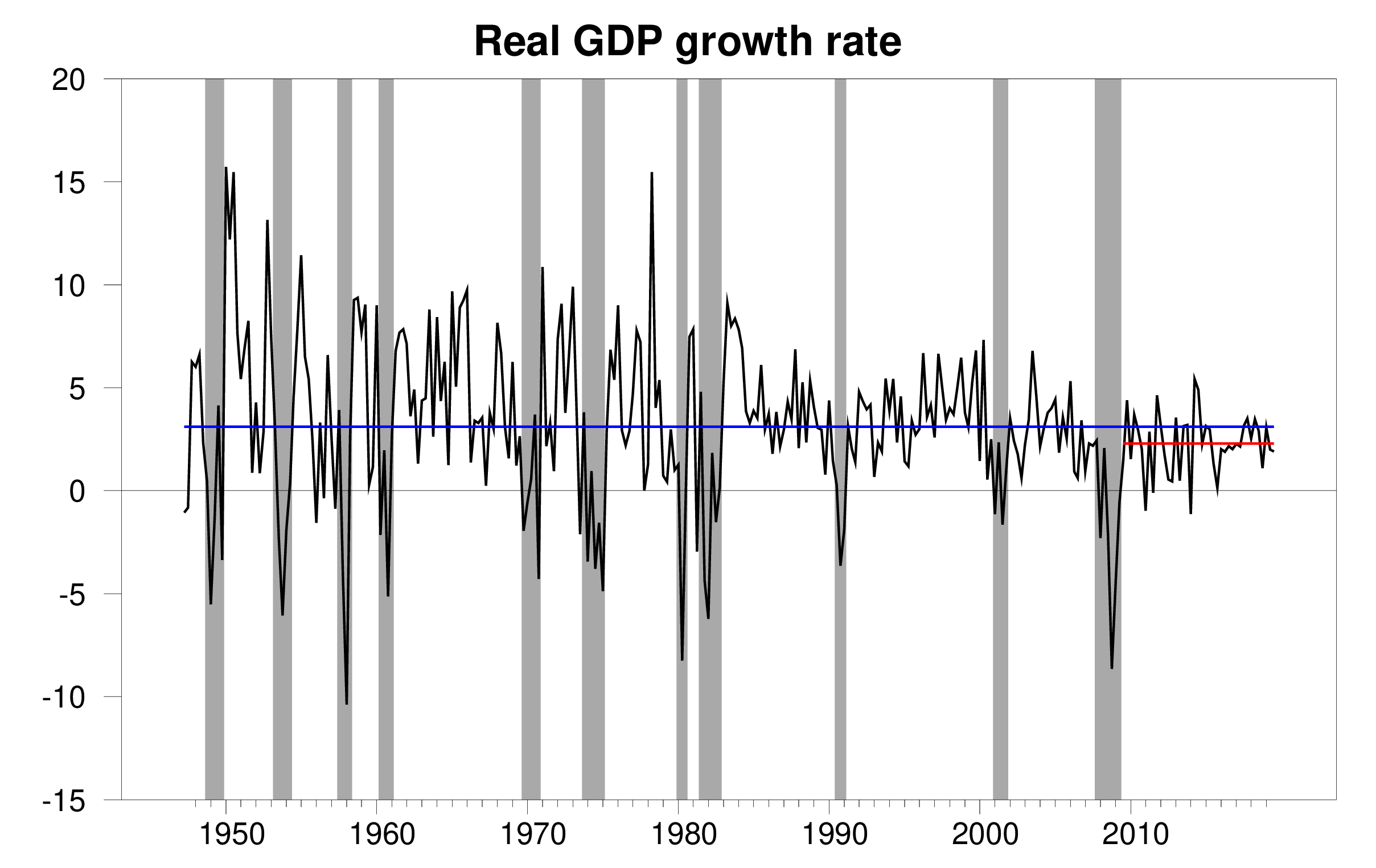

The Bureau of Economic Analysis announced today that U.S. real GDP grew at a 1.9% annual rate in the third quarter of 2019. That’s a little below the 2.3% average rate since the recovery from the Great Recession began in 2009:Q3.

Real GDP growth at an annual rate, 1947:Q2-2019:Q3, with the 1947-2019 historical average (3.1%) in blue and post-Great-Recession average (2.3%) in red.

Year-over-year growth rates have been slowing a little.

Quarterly GDP growth at an annual rate (top panel) and year-over-year growth (bottom panel), 2009:Q4 to 2019:Q3. Vertical lines denote first quarter of year.

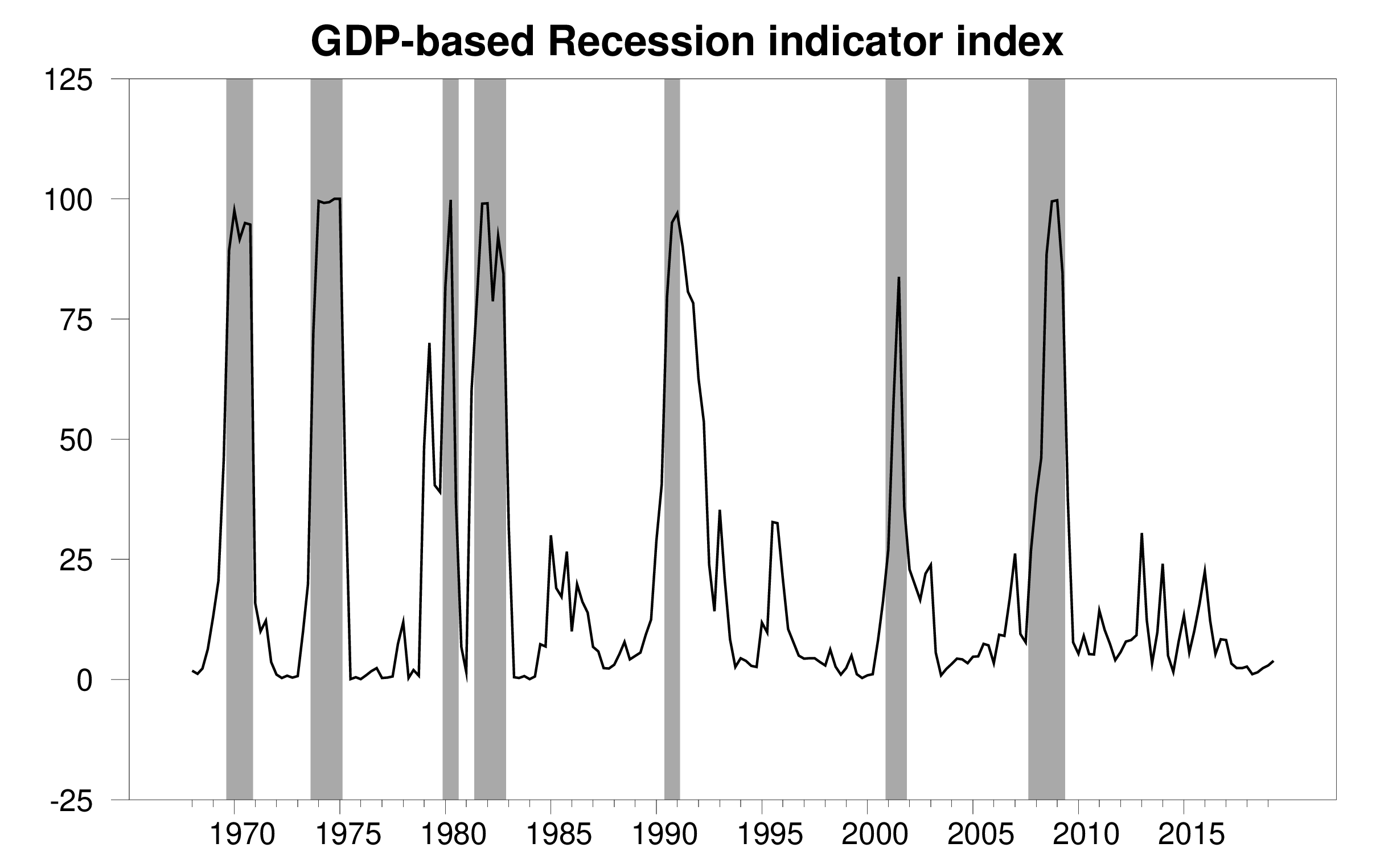

The new release brought the Econbrowser Recession Indicator Index up to 3.9%, still keeping the index in the very low range we’ve seen over the last two years. That signals that the U.S. economic expansion has now been under way for more than 10 years, setting a new record for the longest U.S. economic expansion.

GDP-based recession indicator index. The plotted value for each date is based solely on information as it would have been publicly available and reported as of one quarter after the indicated date, with 2019:Q2 the last date shown on the graph. Shaded regions represent the NBER’s dates for recessions, which dates were not used in any way in constructing the index, and which were sometimes not reported until two years after the date.

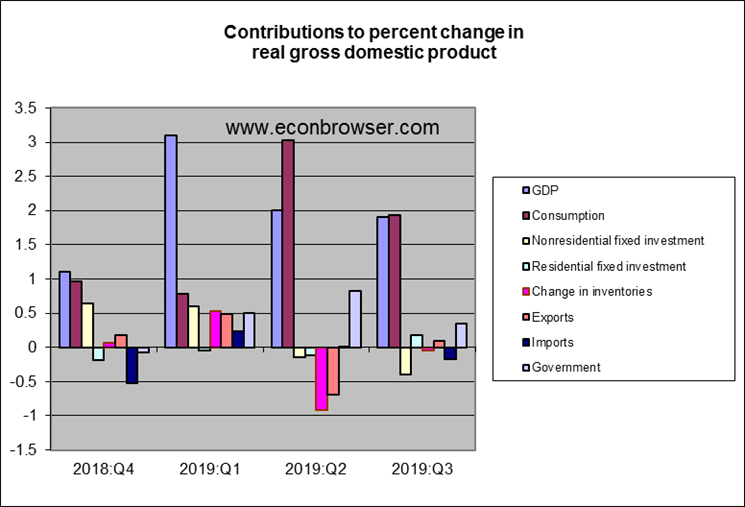

In terms of the individual components of GDP, the growth came from consumption spending and … not much else. A drop in business fixed investment offset the boost from higher government spending.

A $10 billion decline in transportation equipment contributed to the decline in investment spending, reflecting Boeing’s continuing problems with the 737 Max and a strike at GM. But equally large drops in computers and mining structures point to a broader problem. Uncertainty about the economic outlook may be taking a toll on forward-looking business spending.

Another account of the details:

Consumption growth = 2.9%. This was driven by consumer durables.

Fixed investment fell. Residential investment was up but business investment on structures was way down.

Exports barely rose with imports rising by more.

Government purchases growth = 2%. Better growth for Federal nondefense but anemic growth for state & local government.

“A drop in business fixed investment offset the boost from higher government spending.”

So the investment boom promised by the tax cuts for the rich didn’t pan out. But fiscal stimulus from government spending did pan out.

It’s almost like everything Republicans have told us for decades turns out to be a lie.

I am shocked. Shocked!

I think Dr. Hamilton’s co-blogger deserves a victory lap for daring to suggest the Trump fiscal stimulus might involve some good old fashion crowding out.

BTW – real government purchases are not soaring but those tax cuts did seem to give private consumption a boost. Either way – the national savings schedule shifted further inward.

pgl,

I think this is a bit more complicated, and I do not think traditional “crowding out” plays much of a role, although maybe a bit. There was an uptick in fixed business investment on the immediate heels of the tax cut, although not spectacular, with the decline starting later. There were rising interest rates last year, so the subsequent slowdown may have been partly due to that, although frankly, those rates never got all that high before they turned around and started goiing down again pretty much all this year.

Rather I think it is more other things Menzie has stressed, such as the rise of policy uncertainty, not to mention the ongoing effects of Trump’s trade war, and the economic decline in the reest of the year gradually leaking into the US economy, even as consumer spending has continued to hold up. Prospects for expanding future markets do not look so good, while by now high interest rates are simply not the problem, with high interest rates the usual channel fo traditional crowding out to operate.

“Rather I think it is more other things Menzie has stressed, such as the rise of policy uncertainty, not to mention the ongoing effects of Trump’s trade war”.

Actually I agree. Let’s do this in terms of the old-fashion IS-LM model. The Trump fiscal stimulus ceteris paribus would have moved the IS outwards. The trade war as badly as it was done lowered net exports which moved the IS inwards. Uncertainty and its negative impact on investment also tended to move the IS curve inwards. So the net change in the IS curve was nil. Aka – no crowding out as I defined it but total policy ineffective nonetheless!

I meant to say in second paragrraph, “decline in rest of the world gradually leaking in,” not “rest of the year.” I really should do more proofreading of my comments here before posting. I apologize for my lazy sloppiness in that regard.

In any case, I figured you agreed, pgl, and this just reinforces main message in way I suspect you also agree with.

I think JDH’s GDP growth chart may be Fake News. I looked at the chart provided by the White House and there is a black Sharpie line that goes distinctly upward.

I hear Vindman tried to take away the sharpie but Kelly Anne interviewed and did not let Vindman stop the Sharpie-in_Chief.

I can only imagine what happens when BEA will start publishing “Alternative Facts”!

Residential investment has been in a long slide over the last three years. Menzie’s recent post showed weakening home prices. Today’s GDP report showed a slight uptick in residential investment.

FRED agrees with you:

https://fred.stlouisfed.org/series/PRFIC1

Real Private Residential Fixed Investment

This slide started as of 2017QI.

Since I am over 60 I can repeat myself.

annualised figures are garbage. Use only SAAR figures like every other developed country.

AND why use an advanced estimates which includes forecasts from the agency.

Only in the USA

Thank-you Professor Hamilton

It is your factual and unbiased post that keeps the good name of Econbrowser alive.

Ed

Ed,

Menzie’s co-blogger, Jim Hamilton, also follows the same high standard of being focused on what is factually correct and knowable and known.

Ed’s intent was to smear Menzie so it is a good thing you set the record straight here. Ed – come on man. That comment of yours was even beneath Trumpian.

OK, obviusly I forgot this was posted by Jim. Anyway, both of them take their data and facts seriously. Too much Halloween candy, :-).

the data seems to indicate trump has been unable to improve upon obama’s recovery, even with the trillion dollar tax cuts for the rich. so trump created a huge hole in the deficit with tax cuts for the wealthy, and got the same economy as obama. just the factual and unbiased data menzie also publishes on this site. which is why people continue to read this blog, ed.

I’m curious and haven’t done the research: Is consumption outstripping income growth? Who, exactly, is driving the consumption increase? If it’s rich people buying fancy non-GM cars and automobile elevators for them, that’s still growth, but it’s not affecting most Americans one way or another. I’m probably missing a fine point or two here.

Real disposable income jas been rising more rapidly than real personal spending for the past several quarters. That’s the magic of a late cycle labor market. Strong job growth and real wage gains combine to lift household incomes.

New jobs and wage gains at the low end tend to add more to spending than gains higher up the income ladder, and so have been a driver of consumption gains. This will only last as long as firms are confident enough to hire. Let’s see if the talk of a trade deal improves business confidence.

Thank you.

One more comment from the Willie School of Shamelessly Visual and Non-Mathematical Analysis. The Econbrowser Recession Indicator Index spikes upward in an unpredictable amount of time before an actual recession sets in. It didn’t spike upward until the Great Recession was already underway. The twin recessions in the early 1980s appear to have had a predictive flourish from the index before they happened. They were a bad time to enter the workforce, but never mind that. Other recessions were ushered in by rises in the index that appear to have headed up no more than a quarter or two prior to the recession. We are in a lull before the storm.

I’m sticking to the fearless and mathematically unproven prediction of a recession sometime starting in mid-2020 unless some miracle happens and all the trade messes get magically cleaned up. If any more political nonsense gets larded onto the world’s plate, from Trump to Brexit to trade wars, or if a real war or some other crisis breaks out, the economy could head down sooner.

AS As I recall you submitted a 2019Q3 forecast of 1.8% for the Fed’s forecast game. Pretty close to the official 1.9%. Well done.

Thanks.

I was pleased with my September 2019 estimates. I managed to score 985.3 points out of 1,000, However, my score was able to earn only a ranking of 136. The top ten monthly scores ranged from 998.1 to 992.5.

I have a lot of trouble trying to forecast PAYEMS. I was only off by 12,000 for September, but that is much better than my usual difference. Would be great to be in a forecasting class to get some help from those who know what they are doing.

My 2019Q4 GDP estimate is most likely too high, but I am trying to stick with the model output to be consistent rather than adjust the model output for what I think may happen.

@ AS

You might try the lazyman’s route (you know, like how I would do it) and see if the banks and brokerages are making estimates and take that the average of the median number from those PAYEMS numbers and plug it into your competition numbers. I think “TradingEconomics” website has those, and I am sure Bloomberg news would report some estimates (maybe late in the quarter??). Since banks/brokerages “talk their book” those numbers may be overly optimistic, so you could take the number just below the average number and see how that turns out. To test my little “lazyman’s theory on PAYEMS” you could check how that number for the last 4–8 quarters would have worked compared to your “ideal student ‘AS’ crunching the numbers” theory and my lazyman’s route and see if your number would have been closer. Just an idea that might at least help you get above your 136 ranking.

I think Menzie and Professor Hamilton would scold me for taking you down the lazyman’s road to hell—but I still think it might get you better numbers. Like I said you can compare your own numbers to what that would have been the last 8 quarters to see if it works.

Thanks for the thoughts. I am trying to see if I can develop a model that is somewhat accurate rather than just trying to climb the scale of rankings. If I knew an economics prof. in my area, what I would really like is to buy some coaching time.

To answer your question about comparisons with professional forecasters, the Econoday consensus for September was for a change of 145,000 in non farm payrolls (FRED: PAYEMS). My estimate was 148,000. The actual change was 136,000. I don’t have confidence that my estimate will be as accurate for October. One model says 107,000 and another model says 150,000. It was difficult to decide whether to average the forecasts and submit 129,000 or to choose one or the other. The test for in sample accuracy favored the 150,000 forecast. So I may well be off by 50,000 to 60,000 for October.

The Econoday consensus is 90,000. However, the ADP estimate for private employment change as shown on Wednesday, October 30 was 125,000 same as the consensus.

Thus the difficulties of an amateur.

@ AS

In the end you obviously have to make your own call. I think your grasp of the numbers (and how to crunch them) is much better than mine. Based on Trading Economics consensus number of 89k I think it’s indicating the odds are more on the downtrend. So out of respect for your two models I think I would actually split the difference between the average of the two numbers and your low number. In other words add your 107k to your 129k and divide by 2 to get your 118k. Don’t forget your Boeing and your GM strike. If that gets into these numbers, it’s definitely looking like a downward number with a pretty big jump on the following month (I assume).

I would go with 118k with trust in your own models and weighing it 3/4 to the downside, while allowing that 1/4 for error to the upside—if that statement makes any sense to you. Good luck!!!

Another way you might do it, not accounting for things like Boeing and GM, is just take the last 4 months numbers (From June onward, including June) and try and create a trend line with those 4 numbers. If you can take those number and create a trend line using natural log, I would think that would be a good number—my GUESS is, it would again take you close to that 118k number or slightly above that 118. I still like 118k though.

What’s interesting is that the dollar amount of exports and imported goods dropped, but because the PRICE of exports fell more, it was recorded as a net increase.

And goods consumption GDP was also helped by this type of deflation. That might be good for GDP, but I can’t think it’s good for any kind of growth of jobs or the economy for the future.

We won’t fall into recession until jobs are being lost, but I’m not seeing how the growth can get above 2% anytime soon. Recent retail sales and manufacturing reports aren’t promising for the future either.

Jake of…

Domestic prices of exports and imports have not fallen. They have risen at slower rates. This is “disinflation,” not “deflation,” which is falling prices and is not what is going on. However, the substance of your remark holds for different rates of slowing price increases across exports and imports.

No, they’ve fallen. If you look at the GDP report, here are a few price indexes for the goods sector.

Price index, Q3 2019

Consumption, goods -0.8%

Business spending, equipment -0.9%

Exports, goods -3.9%

Imports, goods -4.0%

Same thing shows up in the PPI reports. It’s surprising to me that there are fewer orders at lower prices, but that we don’t have more layoffs as companies get squeezed.

Nominal GDP is growing quite slowly. It’s a lot like 2015-16, which now looks like a manufacturing recession and a situation that led to some disgruntled voters choosing Trump out of hopes their economic situation would improve

I do not know what your source is, Jake, but I just checked the BEA, the most widely accepted source for price changes, and according to them price changes for consumption goods in Q# of 2019 were +1.4% year to year. Sorry, but I think you are wrong.

Also, even according to your own numbers there is almost no differences between price changes for export and import goods, so you do not seem to have much of a story in any case, Jake. Sorry.

today’s September construction spending report came in better than expected, and better than the BEA had estimated, which should add 9 basis points to the 3rd quarter’s growth rate, if i have my figures right…

the BEA’s key source data and assumptions (xls) that accompanied the 3rd quarter GDP report indicates that they had estimated that September’s residential construction would increase by an annualized $3.6 billion from previously published figures, that nonresidential construction would decrease by an annualized $5.7 billion from last month’s report, and that September’s public construction would decrease by an annualized $1.0 billion from last month’s report….this report indicates that residential construction increased at a $3.0 billion rate in September after August’s annualized residential construction was revised $1.2 billion higher, that nonresidential construction decreased at a $1.1 billion annual rate after August’s figure was revised $3.5 billion higher, and that annualized public construction rose by $4.7 billion after August’s public construction was revised $5.1 billion lower…netting those September figures, that means the BEA had underestimated September’s construction spending by an annualized $6.2 billion…in addition, the annual rate of construction spending for August was revised $0.2 billion lower, and the annual rate of construction spending for July was revised $5.6 billion higher…thus, for the 3rd quarter as a whole, the advance GDP release under-reported nominal construction spending by an annualized $4.0 billion… assuming that the inflation adjustments to those figures remain roughly the same, that under-reporting would suggest that 3rd quarter GDP will be revised a net of 0.09 percentage points higher across those 3 components to account for what the September construction report shows…

(NB i know my August figures differ by $0.2 billion but i assume that was due to rounding all the monthly sums…even if i could, i am not inclined to go back and add another decimal place to each of those figures to see if that’s the case)

i already see a stupid error in those figures; i had added the $0.2 billion downward revision to August to the quarter’s total rather than subtracting it; that means the advance GDP release under-reported nominal construction spending by less than $3.9 billion, annualized….that still leaves the net expected revision at +9 basis points, but not quite as solidly…