Today, we are pleased to present a guest contribution written by Daniel Soques (University of North Carolina Wilmington). The views presented represent those of the authors alone and do not reflect the views of their respective institutions.

A recent CNBC survey found that Wall Street investors largely believe a Biden presidency could mean lower stock market returns (https://www.cnbc.com/2020/12/28/investors-believe-the-stock-market-could-see-headwinds-under-a-biden-presidency-.html). Despite this view, the S&P 500 is up 11% since Election Day, with much of the focus on the announcement and roll-out of the various COVID-19 vaccines. But what should investors expect when the market’s attention turns back to standard macroeconomic policy issues, such as a potential tax increase?

To get a better sense of how the stock market is likely to respond to a change in tax policy, investors can look to what happened after the 2016 election. The conventional wisdom is that Trump administration policies played an important role in the 25% increase that was observed over the following year. And this concurs with President Trump’s view, “The reason our stock market is so successful is because of me,” as he stated on November 6, 2017. In a recent paper (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3727719), myself along with coauthors Anthony Diercks (Federal Reserve Board) and William Waller (Tulane University) evaluate this narrative in a comprehensive and exhaustive forensic analysis of this time period.

We analyze major financial news stories to make judgments about primary drivers on each of the 283 days between the 2016 election and the signing of the TCJA in late 2017. For robustness, we also conduct a machine-driven textual analysis based on the Bloomberg News Trend Function. We conclude that tax news did play a positive role in the observed increase, confirming the president’s assertion about the performance of the stock market. However, we find that the 52 days in which tax news was most important only contribute 1 – 2.5%, on net, to the 25% market return. Instead, days associated with U.S. economic data, earnings, and news about monetary policy contributed a greater share to the large rise in the stock market.

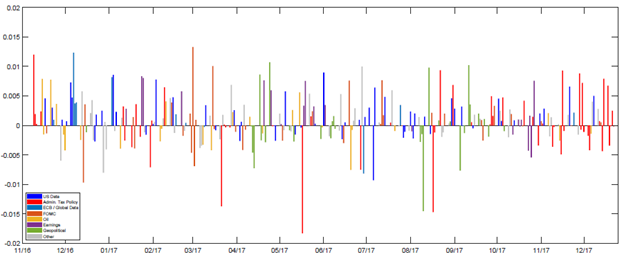

Figure 1: Daily Human Attribution – This figure shows the category for which each day’s return is attributed based on our human-audited news approach. The height of each bar shows the daily CRSP value-weighted index returns from November 9, 2016 to December 22, 2017.

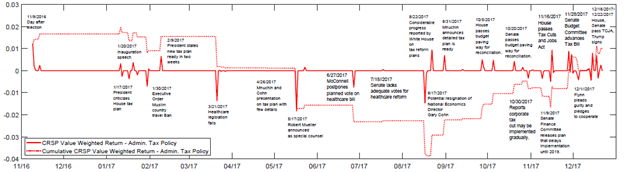

Figure 2: Days Attributed to Tax Policy News – This figure shows the returns for each day attributed to tax policy news based on our human-audited news approach. The height of each bar shows the daily CRSP value-weighted index returns from November 9, 2016 to December 22, 2017.

We argue that existing studies which focused on the beginning and ending of this time period provide an incomplete picture. That’s because they miss key events that took place in the summer of 2017, when the prospect for tax legislation seriously declined following multiple failures to pass healthcare legislation and the announcement of Robert Mueller as special counsel. Each of these events reportedly led investors to question the administration’s ability to pass tax legislation and were associated with the largest declines in the stock market over this time period.

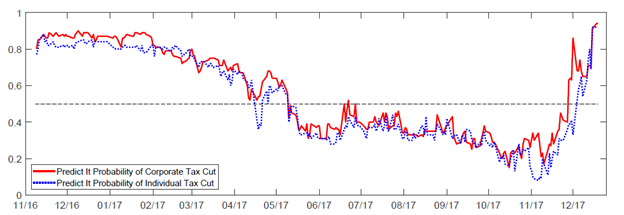

Figure 3: This figure shows the probability of tax legislation based on the PredictIt market. The red line shows the probability of new corporate tax legislation by the end of 2017. The blue line shows the probability of new individual tax legislation by the end of 2017.

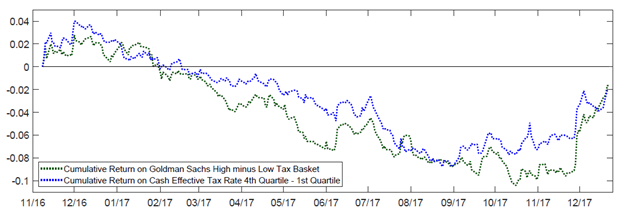

Further calling into question the importance of taxes over this window, we show that the Goldman Sachs High minus Low Tax Basket ended up lower, on net, indicating that high tax firms actually may have underperformed low tax firms.

Figure 4: This figure shows the relative return of high tax firms compared to low tax firms. The green line shows the cumulative return for the Goldman Sachs portfolio that goes long in the 50 highest-taxed S&P 500 firms and short in the 50 lowest-taxed firms. The blue line shows a similarly-constructed portfolio using all publicly-traded firms based on the quartiles of cash taxes paid.

How could a 14 percentage point drop in the corporate tax rate only translate to a 1-2.5% increase in the aggregate stock market? We illustrate through a simple Gordon Growth discounted cash flow model that this counter-intuitive result could be explained by four factors. First, most firms were not paying the statutory tax rate before the TCJA due to a number of loopholes and other deductions. Second, the legislation also included new limits on net interest deductions and the repeal of several other deductions in an attempt to broaden the base. Blanchard et al. (2018) and Wagner et al. (2020) find that the effective corporate tax rate fell only 4 to 5 percentage points. Third, investors likely did not view the corporate tax cut as permanent. Even assuming a relatively long horizon of 50 years for the TCJA corporate tax rate considerably reduces the implied return in the model compared to assuming a permanent rate cut. Lastly, a modest response from monetary policy (due to inflation concerns) would drive up the discount rate and reduce returns. The FOMC did in fact increase its SEP projections in the meeting following the election by 25 basis points. After accounting for these four factors, the modest stock market effect of the TCJA is perhaps unsurprising.

So if taxes weren’t the driver of the run-up in the stock market during 2017 then what was? Our analysis finds that global growth played a substantial role. For example, the Eurozone and China were having some of their best economic performances in over half-a-decade. Likewise, the value of the dollar fell dramatically in 2017 — coinciding with the decline in the prospects for tax legislation — and this boosted multinationals (40% of revenues for S&P 500 is foreign) and export demand for manufacturers. Additionally, we argue the deregulatory policies of the Trump Administration may have also been a factor in boosting stock market returns.

This new paper speaks directly to investors’ concerns about the stock market effects of a potential Biden tax increase. Our findings imply that the prospect of future tax increases will likely be associated with a lower stock market. However, our analysis also suggests that the net effect of a tax hike on the stock market is likely to be very modest. All in all, other macroeconomic factors, such as U.S. economic data, global economic data, and factors related to the COVID-19 pandemic will likely play a relatively larger role in determining the performance of the overall stock market moving forward.

This post written by Daniel Soques.

I had all sorts of problems with the 2017 TCJA including the bizarro international tax provisions which all sounded fancy but in truth was nothing more than the Full Employment Act for tax lawyers. Biden seems to hate GILTI even if was supposed to be one of the provisions to stop income shifting to tax havens. But it has not worked in part because it was designed not to work. And then we have BEAT and FDII. BEAT is bizarro and FDII is a tax incentive for exports which not only reduces corporate taxes for companies like Boeing but will also be attacked by our trading partners as an illegal trade subsidy. Of course this is what one gets when the Republicans get to write the law in cloak filled rooms with no input from the other side.

Hey I hear Bernie Sanders heads the Senate budget committee. This could get interesting!

The comparison of high vs low tax indices is a lovely touch. I isn’t novel to this study, but is just a perfect compliment to the event study. Nicely done.

So the economy !matters, because before-tax earnings matter. Also, as Barkley has pointed out, index composition matters.*

The broader question, one which should concern policy makers much more (perhaps to the exclusion of equity market concerns), is what tax policy does to economic performance, and to social and environmental indicators. Biden has not, to my knowledge, asked Andrew Yang to join his administration. Still no carbon tax, really? However happy the results of the Georgia Senate elections, the Democratic caucus will be dominated by moderates; that’s the logic of a tiny majority.

*For those with a punter mentality, small caps have recently outpaced large caps, while large caps have themselves done quite well. Mid-caps have lagged the wider market. Mid-caps have historically out-performed the market at the 12-month mark in equity market recoveries. Warning Label: I know next to nothing about equity investment.

Oh heck, md, don’t you know that I know so little I am an embarrassment to the taxpayers of Virginia?

I don’t think macroduck ever asserted that. That was more likely me that said that. I probably wouldn’t have said embarrassment though, more likely I said a waste of state revenues or a person that if I was a student I would look extra hard for alternative professors for that class.

Of course he didn’t, Moses. Everybody here knows it was you, who have done it repeatedly. But then, as you just said, “I don’t think…”

Earth to stock forecasters. the US experienced an explosive boom in the 1990’s when Clinton signed tax increases in 1993.

In 2001 & 2003 , Bush 43 signed tax cuts into law. then, we saw a 72 month old expansion that ended in the severe drop from Nov 2007 to March 2009.

BHO signed tax increases at the end of 2012. The stock market boomed in the mid 2010’s/

then Trump came in and caused the worst pandemic in 100 years.

the economy slumped and the promised investment boom in equipment never materialled.

the moral of the story is that higher taxes a beneficial to the market & economy.

Too few data points to draw a moral. And besides, the moral is that tax policy is mostly irrelevant to the economy and markets. Tune fact that Jack Kemp thought taxes matter is all the evidence one needs that taxes don’t matter at all.