If one wanted to assess price trends in “the” US stock market, which measure would one want to use?

From Investopedia:

- The Wilshire 5000 Total Market Index is the broadest stock market index of publicly traded American corporations.

- It is often used as a benchmark for the entirety of the U.S. stock market, and is widely regarded as the best single measure of the overall U.S. equity market.

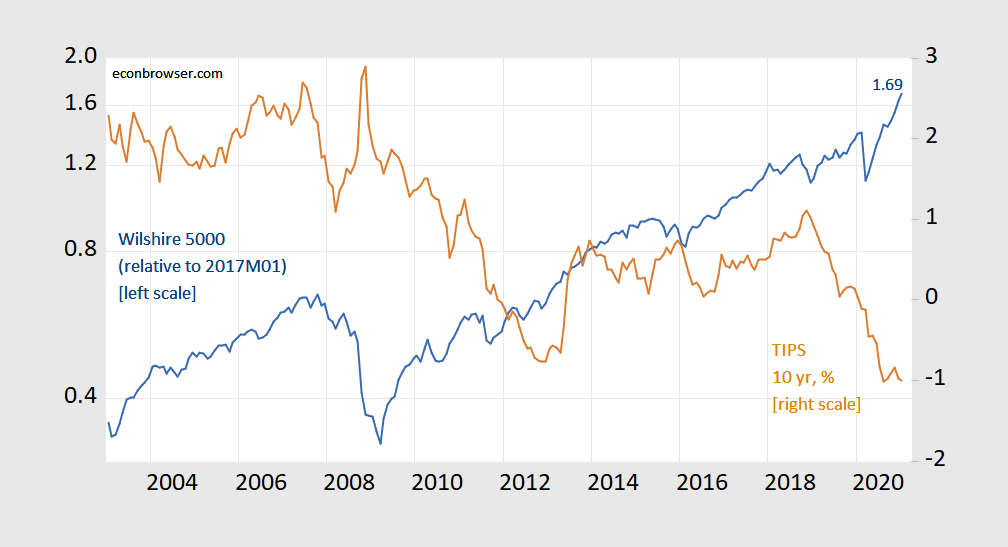

Using this index, stock prices have risen 69%, not 100%.

Figure 1: Wilshire 5000 price index relative to 2017M01 (blue, left log scale), TIPS 10 year yield, % (brown, right scale).

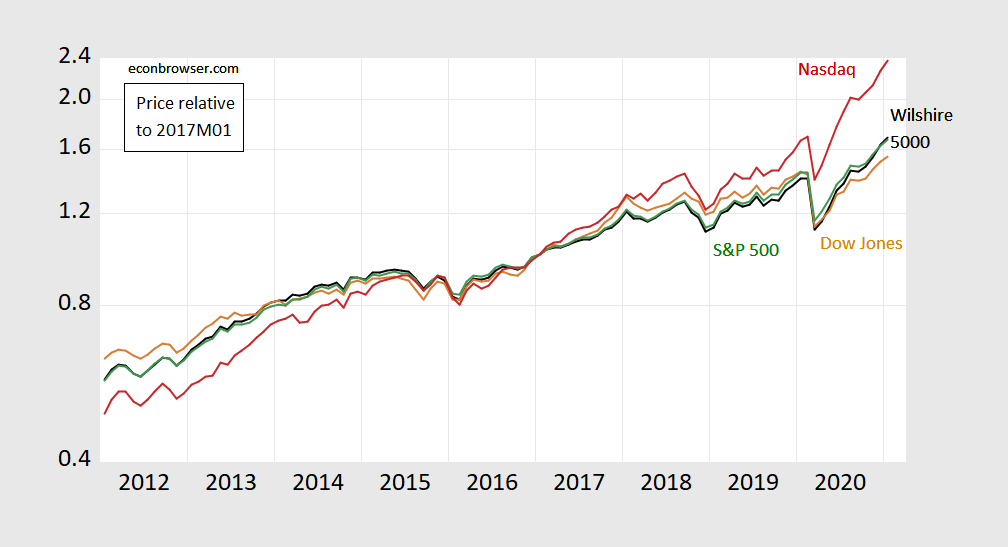

For purposes of comparison, here is the Wilshire 5000 vs. DJIA, SP500 and Nasdaq:

Figure 2: Wilshire 5000 price index (black), Nasdaq (red), S&P 500 (green), Dow Jones Industrial (brown), all relative to 2017M01.

This is why I used the Wilshire 5000 in this post on the stock market vs. the economy.

I should have known better than to address this forum in broad generalities such as ~ doubled and then give a couple examples of the various markets. That’s why I left a comment on the previous post that was more specific based on the more technical term “Equity Market” since there are so many indices that view segments of that total equity market.

In this comment – https://econbrowser.com/archives/2021/02/no-the-stock-market-which-doubled-under-trump#comment-249526 – I left a link to

https://siblisresearch.com/data/us-stock-market-value/ which at least attempts to quantify the entire “stock market”.

The salient information (quoted):

Total Market Value of U.S. Stock Market

The total market capitalization of the U.S. stock market is $50,808,508.7 million (12/31/2020). The market value is the total market cap of all U.S. based public companies listed in New York Stock Exchange, Nasdaq Stock Market or OTCQX U.S. Market (read more about OTC markets from here.) During the year 2020, the total market value of listed American companies increased a staggering 34.82%. Between 1/1/2010 and 12/31/2020, the market cap of public U.S. corporations increased 236.9%. The table below lists also the historical total market cap of the top 500 U.S. companies.

Total Market Capitalization of Public U.S. Companies (USD, millions)

Date U.S. Equity Market Value Top 500 U.S. Companies Market Value

12/31/2020 50,808,508.7 33,388,390.9

6/30/2020 35,503,373.1 26,962,939.0

12/31/2019 37,689,255.8 28,125,589.1

12/31/2018 30,102,771.2 22,065,655.2

12/31/2017 31,774,585.4 23,938,148.8

12/31/2016 27,362,567.7 20,222,191.7

Now, if you want to argue that this is unreliable data… and can demonstrate why as opposed to some derogatory remark… then go for it with an explanation and data that refutes it.

Yes, “doubling” was too much; 85.4% is less than “~ doubling”. But it is more than 58% used to mock my “eyeballing” estimate.

But what I find most interesting is that of all of the points I made, this was the one that drew all of the attention and it was the least important. Forest… trees.

Oh, just to be clear, the “anal retentive” percentage growth is 85.68%, but I rounded the dollars to tenths of trillions for ease so I “grossly understated” the percentage.

And your math has 58% closer to 100% than it is to 55%. You are a genius!

Gobbledygook and irrelevant statement by the master of snark and the failure of logic.

https://www.youtube.com/watch?v=EpHbwGRhf4A

Bruce Hall: Usually, when I hear talk of “stock market doubling”, I think of the price index rather than market cap. But, ok. If I told you GDP has shrunk 14%, I think you’d sit up and notice.

By the way, flow of funds indicates that US household sector increase in equities from 2016Q4 to 2020Q3 (latest available) is $30.1 trn minus $21.0 trn, i.e., 43.3% increase in what Americans hold.

https://fred.stlouisfed.org/series/BOGZ1LM193064005Q

I linked to the Federal Flow of Funds page for Bruce hoping he could figure out what this source noted. But I guess he needed your help to do his homework.

Now a little challenge for Bruce – figure out what happened to this measure during Obama’s term in office (cheat sheet – it almost tripled).

“The total market capitalization of the U.S. stock market is $50,808,508.7 million (12/31/2020).”

So says Bruce Hall’s unreliable source. Your FRED chart says only $30 trillion but that is 3 months old. I think the link I provided (the Federal Reserve Flow of Funds) did report Dec. 2020. I’m sure the new report is a bit higher than $30 trillion but nowhere close to this alleged $50 trillion.

Leave it to Bruce Hall to tell us about his ‘superior’ data which turned out to be totally wrong as usual.

pgl: I think Bruce has reported market cap of US corporations. I have reported *household holdings* of equities, which is not exactly the same — which is why the difference in part exists.

“Menzie ChinnPost author

February 19, 2021 at 11:16 am

pgl: I think Bruce has reported market cap of US corporations. I have reported *household holdings* of equities, which is not exactly the same — which is why the difference in part exists.”

Thanks. I was just thinking the same thing. Now this will confuse poor Bruce but the reality is that foreigners hold companies like Coca Cola and Americans hold companies like Toyota. So the question is how this nets out. Are we more likely to do international diversification or are foreigners more likely. Of course multinationals have their own international diversification.

But here is the real question for Bruce Hall and his Micky Mouse data collection shop. What precisely were they measuring with that $50 trillion? I’m sure he has no clue but we’ll wait.

Menzie,

Yes, that’s the problem with commonly used phrases such as “stock market”. That’s why I used a couple of examples of indices that people often refer to when talking about equities. But the overall equity market is broader than the Dow or some other surrogate.

As far as the GDP shrinking, I have no argument with that. We’ve seen so many examples of that, especially in states where the governors have insisted on shutting down businesses. In Michigan, we are bit more fortunate than some because Gov. Whitmer’s focus for shutdowns was on small businesses and the automotive manufacturers/suppliers in Michigan continued with far less impact. But, overall, actions by the governors certainly have driven the fall in GDP, so I had already sat up and noticed months ago.

I’m not sure who holds the ownership of the equities is relevant anymore than to say that tech oligarchs have benefitted more from the pandemic than the average household.

https://www.msn.com/en-us/money/savingandinvesting/these-47-billionaires-got-richer-during-the-pandemic/ss-BB19X4Zm#image=3

Of course, you measured the change to include the period of the pandemic, so it is natural that the significant fall off due to shutdowns would result in a lower overall growth than my cutoff in Jan. 2020 before the external event compounded by state policies “demonstrated” that the Trump administration economic growth drop was due to federal policies.

“I’m not sure who holds the ownership of the equities is relevant anymore”

Seriously? So if the stocks whose value are significantly risen are mainly owned by citizens of China, this is great for the average American? Gee Bruce if that is true all those MAGA hat wearers have been massively conned.

You do say the dumbest things!

“That’s why I used a couple of examples of indices that people often refer to when talking about equities.”

Silbis Research has an index that people often refer to? Lord – you are liar and a moron.

You have dusted off every way to misrepresent things possible. But you still have not learned first grade arithmetic. Amazing! Hey Bruce – take off your shoes so you can count past 10.

So Kelly Anne Conway dug up Siblis Research. I doubt anyone here has ever heard of this shop and I’m sure Bruce did not check on their credentials including this:

‘We are also frequently conducting custom data collection projects for our clients, ranging from a few hours of work to research projects occupying a full-time team of data scraping specialists.’

Customs data collection projects using data scrapping specialists for their ‘clients’. Roger Stone paid for this?!

Bruce Hall So aren’t you maybe just a teeny-weeny bit concerned that the growth in the nominal value of market capitalizations has wildly outstripped the growth rate in the nominal net value of the private capital stock?

He thinks he is making a killing buying up shares of GameStop!

2slug, if you are asking whether or not I am concerned about wildly speculative trading… no, I don’t get involved in that. Is the market cap of Tesla reasonable? Apparently some people think so. https://companiesmarketcap.com/tesla/marketcap/

If you can quantify the amount that is speculative versus based on solid estimates of future earnings, I guess that would be the basis for discussion. But I think that’s why there are so many different types of funds to address how far out on a ledge you want to go. The equity markets have always had some element of “wildly outstipping” and then there are “corrections” based on the slightest provocations.

I’d say overall that the “market” (example S&P 500) is moving into “iffy” territory (that’s a highly technical trading term).

https://www.multpl.com/s-p-500-pe-ratio

“I’d say overall that the “market” (example S&P 500) is moving into “iffy” territory”

So whatever stock market gains you attribute to Trump are not more than a Ponzi scheme? Gee – did you run this by Kelly Anne Conway?

Bruce Hall Then what was the point of your posting the growth of various stock indices and market valuations? If you’re not concerned, then presumably it’s because you believe wild speculative trading is of no macroeconomic consequence. And if it’s of no consequence, why did you feel the need to bring it up as somehow evidence of Trump’s wonderful economic policies?

If one wanted to look at a truly broad measure of the net worth of corporations, the Federal Reserve’s Flow of Funds is a better way of doing this over some Micky Mouse shop that Bruce Hall was alerted to by Kelly Anne Conway. In fact, this official source tells us the net worth of households.

https://www.federalreserve.gov/releases/z1/20201210/html/default.htm#balance

But in Bruce Hall’s world “corporations of people too my friend” which I guess is a good thing as Bruce Hall could care less about the lives of actual people.

But back to his little Mickey Mouse researchers. Their data show that their measure rose by 138.74% during the Obama years. Pretty amazing for someone that Bruce Hall calls a socialist.

And … the goalposts moved yet again.

Methinks the man doth protest too much.

When you say “broad” I bet Bruce Hall thinks you are referring to that hot woman who keeps refusing his unwanted advances.

What is really amazing is the fact that Bruce Hall wants to remind us over and over again about a comment where he declared that the S&P doubled even if the narrower DOW30 did not. Never mind the latter rose by 55% while the former rose by 58%. 58% is nearer to 100% than it is to 55%?

Yes the Wilshire 5000 rose by 69% which is not 100%. And we asked Bruce about the Russell 3000 and got crickets. Well the Russell 3000 rose by 67% which is not doubling either. But Bruce Hall is bragging that he thought 58% is the same as 100%?

Yes Bruce Hall is bragging that he failed 1st grade arithmetic!

pgl,

He is not so good at arithmetic because he has been too busy studying real analysis out of “baby Rudin,” :-).

Yes the increase in the NASDAQ was impressive. But as we pointed out to Bruce Hall, this index is dominated by high tech and biotech firms, which have done well responding to the pandemic. So yea Brucie – Trump mismanaging a health crisis that has cost us almost 500 thousand deaths and counting led to stock valuation gains in these two sectors. Take a bow for pointing out that Team Trump puts profits over people.

Ted Cruz is a great father according to Ted Cruz. After all, he blames his children for his own shortcomings:

https://www.statesman.com/story/news/2021/02/18/ted-cruz-flew-cancun-after-calling-austin-mayor-adler-hypocrite-cabo/4488804001/

Flying to Cabo during a pandemic – bad! Going to Cancun when people in your state are dying from brutal blizzard and complete power failure – good!

everybody is entitled to take a cancun cruz during a winter snow storm.

Baffling,

I appreciated your explanation on the Texas power “perplex.” * That was useful to me.

Also, I do wish you all well through this time.

* Krugman’s term for California power

thanks ltr.

aside from the recent failure, texas deregulation is a good example for people to study. it shows that free markets and deregulation can work, but there are significant risks that are conveniently ignored by those promoting the model. it really shows that all markets need some amount of regulation and oversight. a deregulated free market is probably worse than an over socialized public utility. if death or injury can result in a free market failure, then it needs strong regulations.

as for me, we fared well compared to others. no burst pipes. loss of power for 24 hours. loss of water for a day. still under a boil water notice. coming from the north, i have a habit of winterizing the house. that said, construction in the south makes it hard to do. too many exposed and uninsulated pipes. my 100 year old house in the north had far fewer drafts than my current new home in texas. and the fireplace is not much more than a decoration! we are looking at a solar panel/power wall to address any future issues.

https://www.nytimes.com/2021/02/18/us/covid-life-expectancy.html

February 18, 2021

A Grim Measure of Covid’s Toll: Life Expectancy Drops Sharply in U.S.

American life expectancy fell by one year, to 77.8 years, in the first half of 2020. It may rebound as the pandemic’s end approaches.

By Sabrina Tavernise and Abby Goodnough

Life expectancy in the United States fell by a full year in the first six months of 2020, the federal government reported on Thursday, the largest drop since World War II and a grim measure of the deadly consequences of the coronavirus pandemic.

Life expectancy is the most basic measure of the health of a population, and the stark decline over such a short period is highly unusual and a signal of deep distress….

https://www.thelancet.com/journals/lancet/article/PIIS0140-6736(20)32545-9/fulltext

February 10, 2021

Public policy and health in the Trump era

By Steffie Woolhandler, David U Himmelstein, Sameer Ahmed, Zinzi Bailey, Mary T Bassett, Michael Bird, et al.

And Bruce Hall would dismiss these deaths as just another Trump policy to reduce future Social Security costs.

February 18, 2021

Coronavirus

US

Cases ( 28,523,524)

Deaths ( 505,309)

India

Cases ( 10,962,189)

Deaths ( 156,123)

UK

Cases ( 4,083,242)

Deaths ( 119,387)

France

Cases ( 3,536,648)

Deaths ( 83,393)

Germany

Cases ( 2,372,201)

Deaths ( 67,547)

Mexico

Cases ( 2,013,563)

Deaths ( 177,061)

Canada

Cases ( 837,497)

Deaths ( 21,498)

China

Cases ( 89,806)

Deaths ( 4,636)

February 18, 2021

Coronavirus (Deaths per million)

UK ( 1,753)

US ( 1,521)

Mexico ( 1,364)

France ( 1,276)

Germany ( 805)

Canada ( 566)

India ( 112)

China ( 3)

Notice the ratios of deaths to coronavirus cases are 8.8%, 2.9% and 2.4% for Mexico, the United Kingdom and France respectively.

ltr: Sigh.

https://news.cgtn.com/news/2021-02-19/Chinese-mainland-reports-10-new-COVID-19-cases-all-from-overseas-Y03xed96Xm/index.html

February 19, 2021

Chinese mainland reports 10 new COVID-19 cases

The Chinese mainland recorded 10 new COVID-19 cases on Thursday, all from overseas, data from the National Health Commission (NHC) showed on Friday.

No deaths related to COVID-19 were newly reported, the NHC said.

Eight new asymptomatic cases were also recorded on Thursday, and a total of 338 asymptomatic patients remain under medical observation.

The total number of confirmed COVID-19 cases on the Chinese mainland has reached 89,816, and the death toll stands at 4,636.

Chinese mainland new locally transmitted cases

https://news.cgtn.com/news/2021-02-19/Chinese-mainland-reports-10-new-COVID-19-cases-all-from-overseas-Y03xed96Xm/img/4b5062bac2dc4b7788afca03f5e755d7/4b5062bac2dc4b7788afca03f5e755d7.jpeg

Chinese mainland new imported cases

https://news.cgtn.com/news/2021-02-19/Chinese-mainland-reports-10-new-COVID-19-cases-all-from-overseas-Y03xed96Xm/img/0ec04ffdbd5d4590898777adf9164926/0ec04ffdbd5d4590898777adf9164926.jpeg

Chinese mainland new asymptomatic cases

https://news.cgtn.com/news/2021-02-19/Chinese-mainland-reports-10-new-COVID-19-cases-all-from-overseas-Y03xed96Xm/img/e7d32b664e0e4f87989d7b2ccb1de93c/e7d32b664e0e4f87989d7b2ccb1de93c.jpeg

ltr: Double. Sigh.

As someone who works in the investment field, we would generally use the S&P 500 as ‘the’ market. Dow Jones is too narrow, Wilshire is too broad, NASDAQ is too tech heavy. The S&P 500 represents a broad (enough) representation of the economy that is inclusive of most industries.

I know this is not orthodoxy, but I have felt for a long long time, probably going back to at least the late ’80s that the Dow Jones is an outdated index, and frankly have wondered for the longest time what is the point in quoting it. It certainly is not any kind of fathomable measure of “markets”. In fact I think I could make a pretty damned good argument the Dow Jones is a misleading market indicator for small and individual investors. Now if they want to say it’s a measure of a layer of the market, fine, but it’s not a measure of markets. And that’s coming from someone who has followed markets pretty consistently since his early teens. So take it for what it’s worth.

Moses, It was my understanding decades ago that formal observers of the equity markets and of the economy in general held that the DJIA was (is) a poor proxy for “the markets,” and that “the markets” were (are) a poor proxy for the economy. These judgments have only grown stronger since then, so I’d say that your opinion was and is quite orthodox.

Maybe the general public, whatever that comprises, hasn’t caught on yet, but when one thinks of how many of them are MAGA-nauts and/or Q-balls, I would disregard their opinions on this subject.

the dow has always been the popular index to report to the masses, so people have a better feel about the magnitude of its numbers and changes. many people, based on how CNBC and others report, have a pretty good feeling for what a 1000 point move in the dow represents. while the sp500 is a better metric, people lack perspective on the magnitude of its changes. is a 50 point change in the sp500 big or small? folks just don’t know. i am guilty of this as well, and appreciate the dow measurement intuitively much better than the sp500, even though i know the sp500 is more representative. its hard to overtake the established dow. can an old dog learn a new trick? for similar reasons, the metric system is a far superior system. and yet us customary units dominate much of american engineering and business. humans dislike change.

‘NASDAQ is too tech heavy’. Thank you. A point I have made three times. But Bruce Hall ducks it as he hates it when we catch this lying troll in cherry picking.

One question however – what is being very broad a bad thing?

Maybe ‘too broad’ is a bad explanation. The Wilshire 5000 includes ALL publicly traded equities. As such, the number of companies in the index changes over time. There were more about 5,000 companies when the index launched. By the late 90’s there were more than 7500 companies included in the index. Today there are about 3500. Yes – the number of publicly traded companies in the US has been shrinking.

The S&P 500 is more stable, utilizing the 500 (plus or minus 10 or so) largest companies.

Chalk this up as the most egregious tax evader ever who whines that they had to pay legal fees to fend off a reasonable challenge from the Canadian Revenue Agency:

https://www.theglobeandmail.com/business/article-camecos-legal-victory-seen-as-rebuke-to-cras-costly-pursuit/

Forget the comments by these lawyers who do not have a clue. Cameco has the lowest cost mines for producing uranium being to able to produce it at $10/pound. So they sell it to a Swiss tax haven who gets to sell it in the real world for sky high prices making over $5 billion in income tax free. Of course the tax authority challenged. But Cameco hired a bunch of lying experts and got away with it for now. But they cry the tax authority is a mean dude? Just wow!

Is “Itr” now one of this blogs hosts?

You made me half-laugh, and the situation makes me laugh. The funny thing is, how hard is it for us to use the scroller. Well on my comp the scroller thing-y is kind of thin, so it is kinda annoying, but really that’s the scroller itself which is always annoying, not the act of scrolling itself, if the way I explained that makes any sense. But even then, people like me not very dexterous can still use the arrow down button. Who it is the real pain-in-the-A for is the blog hosts. Because they HAVE to read it to clear it and then put the comment up.

My actual message here, although the way I have stated it sounds extremely contradictory is, ltr and the prolific commenters don’t bother me that much, because scrolling down is not that bigguh deal, and if it is that bigguh deal, I can read who is making the comment and skip it and scroll down. Surely we haven’t gotten that lazy?? If it was regularly 200+ per post maybe, but not when it averages out around 30-40. IT just doesn’t bother me. But I am a prolific commenter so “I would say that, wouldn’t I”. But for the hosts it’s more work, THAT I “get”.

Ted Cruz is being hammered for going to Cancun suffers from the extreme weather. Let’s turn the clock back a decade when Gov. Chris Christie took the family to Disney World during a massive blizzard that rocked New Jersey:

https://www.cbsnews.com/news/chris-christie-under-fire-for-disney-world-vacation-during-blizzard/

Here’s an interesting take by Olivier Blanchard on the Biden stimulus.

https://www.piie.com/blogs/realtime-economic-issues-watch/defense-concerns-over-19-trillion-relief-plan

To me, it is interesting to see the focus on inflation rather than asset bubbles. (Where is the M2/Q going?) I look at the topic of this post and am appalled. Since the beginning of the pandemic, the NASDAQ is up more than 50%. During a horrible downturn. Since July, house prices have been rising by 1.1% per month, and the Case Shiller National Index is higher than its peak in 2007 in real terms. What part of financial bubble is hard to understand here? Do economists not care about this sort of thing anymore? Last time, it took us a decade and suffering through four years of Trump to get over it.

Steven Kopits I’m sympathetic with Blanchard’s concerns over potential GDP, but I believe Blanchard has made some self-inflicted wounds with regard to his comments on stimulating aggregate demand. Notice that Blanchard implicitly assumes that 100% of Biden’s $1.9T stimulus will be spent in FY2021. That’s a rookie mistake, so comparing the value of the stimulus to the output gap for FY2021 alone doesn’t make a lot of sense. That $1.9T will be spread out over several years. Blanchard should really take a course in the way the government comptroller operates.

And a little nitpicking. Blanchard cites a famous paper by Valerie Ramey. While I admire the historical detail in some of her work, I think her work on defense spending as stimulus badly misunderstands the differences between “commitment spending”, “obligation spending” and actual Treasury disbursements. For example, one of Ramey’s historical examples refers to the Vietnam defense build-up in 1966. I actually know a lot about the details with respect to that budget and some of her assumptions are historically wrong. For example, in calculating the multiplier from that spending she assumed that the expected budget increase was very large based on mainstream news accounts of the expected budget. Internal DoD memos document that the budget announced to the media was very much smaller than what insider defense contractors were expecting. In fact, the internal DoD budget was so much smaller that MIT was contracted to estimate the negative impact on operational readiness. Should we be surprised that the measured multiplier was less than what was expected based on media accounts?

“I’m sympathetic with Blanchard’s concerns over potential GDP”

He takes the CBO estimate of 4.2% after admitting that such calculations are difficult. He then echoes your concern that supply disruptions will lower this by around 1%. But if we have a go go economy, these supply disruptions will tend to go away. Not overnight as Princeton Steve had claimed but this will not take forever either.

So his guess of a 3% output gap strikes me as way too low. Those of us who follow the employment to population ratio for 25/54 crew put the gap at 6%.

“A healthy debate has erupted. This blog post addresses three main issues in that debate and explains why I am concerned: first, the size of the output gap—i.e., the gap between actual and potential output in the economy; second, the size of the multipliers—i.e., the likely effects from the stimulus; and third, how much inflation an overheating economy may generate.”

A healthy debate indeed and what he wrote is much more than an interesting take. But what does Princeton Steve do – some stupid use of the failed Quantity Theory of Money? I guess this discussion was over your head as usual.

But you did get your bubble mania in which tells me that in all of your consulting you never learned basic finance. Like the low interest rates today should have no impact on the market value of assets. Damn – the real economists over at Princeton University are having a good laugh at you.

Mortgage rates were over 6% back in 2007 but are only 2.8% now:

https://fred.stlouisfed.org/series/MORTGAGE30US

But in the world of Princeton Stevie pooh, this should not have any positive effects on housing values. Lesson learned – no one should EVER even consider hiring this fool as a consultant.

“To me, it is interesting to see the focus on inflation rather than asset bubbles. ”

if you are wealthy, which concerns you more? inflation.

I did check a couple of NASDAQ favorites. Pfizer’s P/E ratio is only 20% so I doubt this company is overvalued especially given the demand for its vaccine.

Apple is another matter. Its stock value has soared in the last 5 years. OK sales have risen from $225 billion to $275 billion per year but is operating margin is slipping as operating profits seem to have peaked at $70 billion. Maybe they are spending a lot of R&D to put Samsung and that Chinese competitor down but I still have to wonder.

Of course never trust the consultants at Steve little Princeton basement outfit to do real research on the valuations of an actual company.

“the Case Shiller National Index is higher than its peak in 2007 in real terms.”

Check ltr’s graphs. Based on 2000 = 100, this real index was 170 back in 2007 but is 158 now. Gee – your consulting includes ideas such as 158 > 170. Your clients must be impressed.

ltr also graphed housing values/rents which were 70% higher in 2007 than they were in 2000 v. now only 38% higher than in 2000. In plain English for morons like you – real rents are higher.

And interest rates are lower. Now if you passed freshman finance (which you clearly did not), you would know that when rents are higher and discount rates are low, the fundamentals suggest an increase in asset valuation. That is not a bubble.

BTW I linked to a CalculatedRisk post. Read it and read Bill McBride’s links. You might actually learn something for a change.

An interesting post on blocking comments:

Zeynep Tufekci: ’I try not to block actual criticism but things I’ve started pretty much automatically blocking to make Twitter usable: Snitch-tagging; “Oh you’re surprised?” reply guys; People who respond to an article I wrote with a point made in the article as if I could have no idea. People who respond to an article I wrote with a point made in the article as if I could have no idea. I started blocking them! There are people who sit on their keyboards all day telling others—who never asked them—that what they just said is obvious. And then others reply to them. And then my mentions are unusable. I’ve never had a useful interaction with any of the above categories, and they are just cluttering up my mentions especially since others then respond to them, and it’s an endless, pointless series of pings that hide any signal that may hide in my mentions.

I’m a big fan of hers. She has a newsletter you can get sent to your email if you like her writings. I’m generally against giving my email for newsletters, but she is one of the ones I make “exceptions” for. Her writing is pretty solid.

https://fred.stlouisfed.org/graph/?g=mSzQ

January 30, 2018

Case-Shiller Composite 20-City Real Home Price Index, 2000-2020

(Indexed to 2000)

https://fred.stlouisfed.org/graph/?g=oCkD

January 30, 2018

Case-Shiller Composite 20-City Home Price Index / Owners’ Equivalent Rent of residences, 2000-2020

(Indexed to 2000)

I remember Robert Shiller tracking real home prices in Amsterdam over several hundred years and finding them roughly constant over the extended time. Also, I remember Paul Krugman distinguishing between home prices in cities constrained in area and cities that were sprawling (I forget the terms used for the moment). What I never got was the “rule.” Why should home prices track inflation over generations, as Shiller argued? I get the data, but the reasoning puzzles me.

There’s actually very little connection (at least as far as the USA market is concerned). There’s no mint coin to be made though if you say “These things may run in parallel but the short to intermediate term movements may be drastically different”. You can’t sell books or get invited to CNBC that way. Nearly everything rises in price “together” if you shift the horizon out, that’s not terribly “insightful”. Housing costs/prices have been “untethered” from inflation for quite awhile. You might as well draw a connection between post 2016 stock prices and GDP. Of course, you can find people selling books who will tell you that makes sense as well.

I’m not a Shiller fan, I’m sure some here will be happy to take me out behind the woodshed on that one. HIs amalgamation of data is great—his own personal “insights” I don’t care too much for. A lot of longwinded talk which doesn’t tell you too much you didn’t already know.

No link to the price to rent ratio? OK – Bill McBride provided the graph:

https://www.calculatedriskblog.com/2020/12/real-house-prices-and-price-to-rent.html

So this ratio is at the same level as it was in 2004. Which is not surprising since interest rates now are much lower than they were in 2004. But of course people who flunked Finance 101 (as in Princeton Steve) will not get the basics of evaluating assets values.

“the Case Shiller National Index is higher than its peak in 2007 in real terms.”

Your graphs show that Case-Shiller Composite 20-City Home Price Index / Owners’ Equivalent Rent of residences, 2000-2020 is at 2004 levels which is far below the level this was in 2007. Of course the real value of Case-Shiller Owners’ Equivalent Rent of residences is 20% higher than it was in 2004 so one would expect a 20% increase in the real value of houses if interest rate had not changed.

But interest rates back in the 2004-2007 period hovered around 6% but are now only 2.8%. Which could be seen as housing being undervalued.

Of course Princeton Steve cannot understand the roles of rent and discount rates in the evaluation of assets values. Financial economics is not his thing.

The Wilshire 5000 was created as a marketing tool. No more, no less, speaking as someone who was around during the birthing. To say that its utility is marginal is an overstatement.

Any index that is cap-weighted is essentially the S&P 100 – not 500 – with a Disneyesque diversity thrown in.

Want to effectively capture the entire US stock market? Use a model with the S&P 100 along with the Nasdaq QQQ. This more than sufficient.

Now if you want to get a touchstone for how major public corporations, broadly, are doing as a reflection of the broader economy (even though they account I believe for less than 15% of GDP), may I suggest using an equal-weighted S&P 500 etf as your proxy.