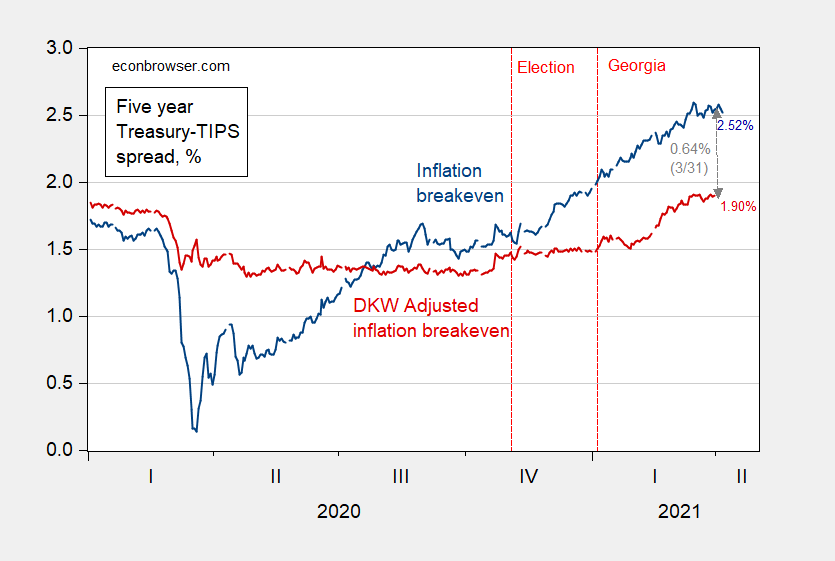

As of today, the five year constant maturity Treasury yield has stabilized for the last month at about 0.9%. The inflation breakeven implied by the spread between Treasurys and TIPS has plateaued at 2.52%. After accounting for the estimated term premium and liquidity premium, the implied inflation rate is 1.90% .

Figure 1. Five year inflation breakeven calculated as five year Treasury yield minus five year TIPS yield (blue), five year breakeven adjusted by term premium and liquidity premium per DKW, all in %. Source: FRB via FRED, KWW following D’amico, Kim and Wei (DKW), and author’s calculations.

The unadjusted 5 year Treasury-TIPS spread is:

Where tp is the term premium on the Treasury yield, and the lp is the liquidity premium on the TIPS yield. Using the DKW estimates of the Treasury term and TIPS liquidity premia as reported by Kim, Walsh and Wei (2019, data 2021), one obtains the following estimates of expected inflation show as the red line above.

As of 3/31/2021, the unadjusted series is 0.64 percentage points higher than the adjusted. If the gap between the two premia has remained constant for the subsequent four business days (no reason that would be true), then expected inflation remains below 2%.

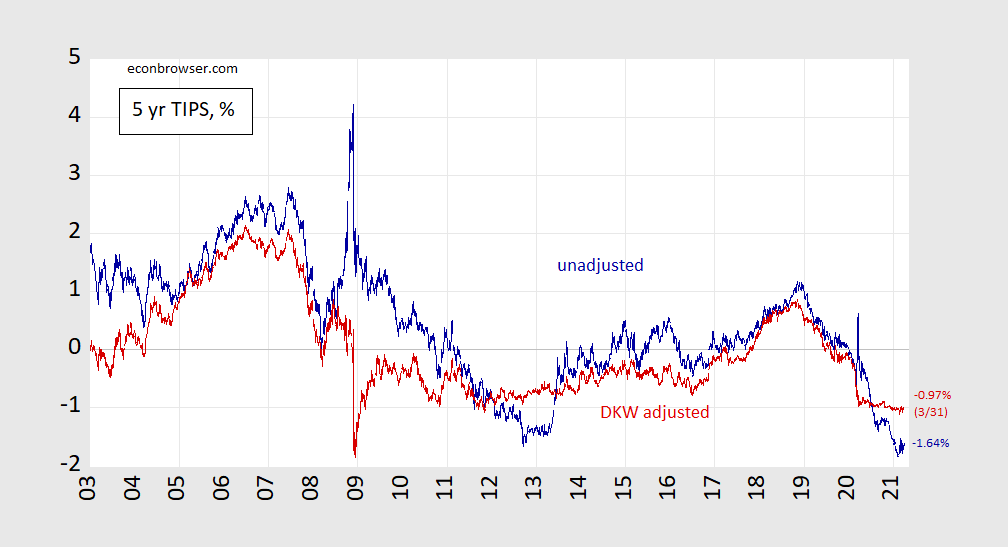

An interesting side point is that while the TIPS 5 year yield is at record low levels (-1.64% on 4/6), the expected average real interest rate over the next five years is about -1% — unchanged over the past year.

Figure 2. Five year TIPS yield (blue), five year TIPS yield adjusted by liquidity premium per DKW, all in %. Source: FRB via FRED, KWW following D’amico, Kim and Wei (DKW), and author’s calculations.

As is one of my procrastinatory habits, I was reading through old NYTs I have strewn around here. This was in the January 3 hardcopy NYT and I thought it was quite interesting. Although way off-topic I thought Menzie might humor me:

https://www.nytimes.com/2020/12/29/business/cooperatives-basque-spain-economy.html

One almost gets the idea that the broader welfare of society at large (Is that redundant, or can society be “at small”??) and its efficiency might be better served taking care of the workers doing the actual work, than executives taking exorbitant salaries for doing next to nothing. I know, a strange concept in “the good ol’ US of A”.

Hi Moses – thanks for posting this idea, Over by my office park in Madison WI – a new Amazon prime shipping warehouse has been constructed, It is a hive of activity with delivery trucks coming and going. I imagine it filled with warehouse workers having to interact with robots to fulfill orders. Also behind this warehouse is a wetlands area/park/forest that is owned by the city, Madison is built on an isthmus between two lakes and this area provides millions of $ in ecosystem services and run off area to prevent flooding. During the last year – a tent village of homeless has sprung up in this area. I’ve noticed the city has provided some washing stations and portable toilets. There are several such sites around Madison – I call them Trump-villages,

As you say – what has struck me is contrast/lack of efficiency in our economy when one CEO can afford hundreds of thousands of single family homes while others live rough (FYI -living outside in a Wisconsin winter is no picnic), And all the while blustering old fools (GOP Senators) and CEOs complain about a penny more in corporate tax while taking advantage of state provided – educated workers and road networks, Isn’t it time for these corporate freeloaders to pay for some of these services?

Thanks for your comments –

Make Amazon pay taxes. And unionize its work force.

@ James

I appreciate your thoughts on it, and sharing some of your impressions from living your daily life. You strike me as an observant, perceptive, and most importantly, a person with a great deal of empathy, even to people you don’t “personally” know. That’s a rarity and a gift to the world, James, so don’t ever lose that empathy. Even if future bumps in the road encourage you to feel jaded.

Plus, I don’t get much compliments on my internet comments or my IRL statements, so that totally proves you are a cool guy (joke).

Doubtful that the United States can be ‘at small’ anytime soon, since concentrated industries are pervasive.

https://concentrationcrisis.openmarketsinstitute.org/

Benyamin Appelbaum, in his book The Economists Hour, documents how elites, along with prominent economists doubling as public intellectuals, began to increasingly tolerate concentration on the pretext that it was more efficient that competition. Having spent much of my career with a monopoly enterprise, I can say that it was really good for investors, not for customers.

I have yet to see much pushback to this curious notion from anywhere.

“Economies of scale” is one of the arguments here. It has some truth in it, but has been vastly oversold. If the economies of scale are not shared with society, I would argue it only becomes gluttony, for those who dictate the rules on where those margins in profit go. Often to those who in actuality had nothing to do in creating those economies of scale. I can dip the mouth end of a mason jar facing the flow of a river and drink the water. Does that mean I created the water flow??

“prominent economists doubling as public intellectuals, began to increasingly tolerate concentration on the pretext that it was more efficient that competition.”

Prominent economists who want less competition? WTF? Everyone of your comments starts with this insulting false premise. There is an entire literature of economists decrying increased concentration and the economic losses created. One of those economists happens to be Paul Krugman – the economist who are obsessed with insulting with this stupid set of lies.

As I mentioned, and pgl reflexively disregarded, Benyamin Appelbaum amply documented the shift from an emphasis on competition to a preference for efficiency and oligopoly in “The Economists Hour.”

Same old pointless boring lies year after year after year. OK – I’m sorry I kicked your dog.

“In June 2019, Open Markets published exclusive new concentration data on the health care sector. While concentration among insurers is broadly recognized and well-documented, the data presented here illuminates concentration in a broad range of healthcare-related markets, from syringes to medical patient financing. Growing monopoly power in the health care sector contributes significantly to the high prices, poor quality, and lack of access that millions of Americans experience when interacting with the health care system.”

Market power in the health care system. Why my oh my – no economists including yours truly has never complained about this according to St. JohnH.

Of course anyone who reviews my posts either at Econospeak and Angrybear will see that I have noted these problems for years. But St. JohnH will continue to claim otherwise. It is what this sad troll does.

It’s not just healthcare. As the Open Markets report shows, oligopolies are pervasive, and there has been all too little pushback from economists doubling as public intellectuals—the only ones who really matter in the public debate.

On a more micro level, “ Part of the reason for such a skewed result in favor of antitrust defendants is that dominant firms have access to high-salaried economists that are able to manipulate analyses to mask the corporation’s conduct to look like it is operationally efficient instead of engaging in predatory practices. Such a situation also deters antitrust litigation because a plaintiff will also have to incur the cost of an economist—which can cost several thousand dollars and, in some cases, several hundred thousand dollars. Thus, the battle over the legality of a business tactic under a consumer welfare framework and rule of reason legal analysis depends on access to immense financial capital and judicial appeasement of policies that favor corporate integration rather than common notions of fairness, equity, and deconcentrated markets—which was the original purpose of the antitrust laws.”

https://www.openmarketsinstitute.org/publications/slate-how-antitrust-lost-its-bite

Oligopolies exist? Who knew? Next thing you will be telling us that it gets cold in the winter.

Our kitchen bistro table and chairs come from a design cooperative that is part of the larger Basque group. They have won several international design prizes.

Imagine my extreme shock upon the moment of seeing Nancy Pelosi’s name mentioned.

https://theintercept.com/2021/04/06/democratic-party-dccc-political-consultant-factory/

Anyone have some smelling salts for me, now that I have passed out??

Moses, See also: “DCCC Vendors Work for Corporations Lobbying Against Democratic Policies“

https://prospect.org/power/dccc-vendors-work-corporations-lobbying-democratic-policies/

I do not know about you but I’ve grown tired of the incessant stupidity in Princeton Steve’s arrogant but really dumb comments. Let’s take his claim that the CBO is nuts not to realize that the debt/GDP has to explode over the next decade combined with his dismissal that that primary surplus forecasts are irrelevant if nominal interest expenses exceed them.

A simple example – an economy has current nominal GDP = $20 trillion with Federal debt now = $20 trillion. Inflation will be 2% over the next decade and the primary surplus will be 2% of GDP (non interest spending = 21% of GDP and taxes = 23% of GDP). So the primary surplus starts off at $20 billion per year and grows over time in nominal terms at 4% per year if we reasonably assume real growth (n) = 2%.

Let’s also assume a real interest rate (r) = 3% so the nominal interest rate = 5%. The nominal deficit starts at $50 trillion (nominal interest expenses) minus $20 trillion (primary surplus) in the first year or $30 trillion. Nominal debt grows by 3% but GDP grew by 5%. Of course real interest expenses were only $30 trillion. And the present value of the primary surplus = $20 trillion/(r – n) = 200% of current GDP so with the real debt growing at 1% per year and real GDP growing at 2%, the debt/GDP ratio falls over time.

All of this is basic finance. Princeton Steve claims he knows ROI which is laughable as he clearly flunked finance 101. Now Steve might whine that my assumptions are not the same as his but if this pompous idiot would actually read the CBO report he mocks, he would see what they assumed. But of course Princeton Pompous will not bother and even if he did – he would not understand any of the analysis.

‘primary surplus = $20 trillion’

What I get for typing at 5AM before the morning run. A 2% surplus is $400 billion. So feel free to redo my sleepy attempt at arithmetic but the general point still holds.

By my count – the prosecutor in the Derek Chauvin trial has called 9 police officers so far. And they all make the same basic if not otherwise obvious point – Chauvin used unnecessary and deadly force which killed George Floyd.

The defense attorney is grasping at straws, using racist tropes, and generally making $hit up as he goes.

Menzie,

Thanks for these posts that estimate “rational” market forecasts of inflation over longer time periods. I appreciate that you are adjusting the garden variety “breakeven” inflation expectation that I think most people look at by the Treasury premium and the TIPS liquidity premium. It seems this has only really been enunciated and studied seriously quite recently, with not that many people in the public knowing what this is about.

It might be useful to do a post to explain these items more fully and why they need to be accounted for in this calculation, please.

Might also get more comments relevant to the topic than you have gotten here so far.

Barkley,

Thanks for your request. As a non-economist, I am interested in a numerical example from the data to more fully follow the calculation.

@ AS

I’m not trying to be a smart-aleck, but did you skim the Fed Res link Menzie gave pretty well??~~they give alot of the rationalizations behind the calculations and there’s a CSV file with the data points (numbers). Now I do not claim to hold the fortitude to crunch out those numbers, but I assume you could take the numbers from the CSV file for your inputs, then check the Fed’s final numbers and graphs to see if you got the same end result. If it’s wrong then you could do some “trial and error” or back-check your calculations. Menzie has been relatively kind on these things in the past, especially if you meet him halfway and do some trial number crunches. I wager if you ran some calculations and got something in the ballpark Menzie would help you find what the snafu was.

Moses,

Last time I looked at the data and model(from a previous blog entry), the calculation did not seem clear.

When I am fresh, I will look again.

Moses,

I do not think AS was claiming that he thought there was a snafu anywhere here. He simply would like to see more explanation and more numbers, although indeed some are provided in the link.

BTW, I have posted on my own on this at Econospeak, although the underlying paper has more in it than I talked about or that Menzie mentions here.

AS: From FRED series (DGS5-DFII5) I subtract “inflation.risk.prem.5” and add “tips.liq.prem.5” (these two series from KKW spreadsheet). This comes close but not exactly to “exp.inflation.5”

Thanks,

In order to show a chart similar to yours, I had to add the “inflation.risk.prem.5” and add the “tips.liq.prem.5”. Have KKW already adjusted the effect of inflation and liquidity on the (DGS5 – DFII5) series, such that one adds both?

AS: If you see “exp.inflation.5” in the KKW spreadsheet, I believe that is *fitted* 5 year Treasury yield minus *fitted* 5 year TIPS yield, adjusted by the two premia. Hence the difference between their measure and what I plot as “adjusted”.

I think what has not really been explained all that clearly is what these two items are that since 2018 people have arguing need to be used to adjust the old garden variety “breakeven” inflation expectation one gets by basically subtracting the appropriate TIPS yield from its same period Treasury security yield (5 years in this case for both). That is, what are the “Treasury premium” and the TIPS “liquidity premium” whose difference should be added to the simpler number to get a more accurate measure of market inflation expectations for the time period involved?

The first is buried in the equations Menzie showed, that in looking at that 5-year Treasury yield one must account for the sequence of short run yields that will occur during the 5 year period. It is the risk associated with this sequence that generated the tpr or Treasury premium rate. This has gone up and down over time, as the underlying article lays out.

The TIPS liquidity premium, lp, arises from TIPS being less liquid than regular Treasury securities, something I would not have realized was the case. This has also gone up and down over time. Anyway, the current estimated difference according to those whom Menzie has linked to is -o.64%, which when added to the 2.52% breakeven expected inflation rate lowers it to 1.88%, although somehow the post calls this 1.90%, but close enough I guess, and indeed below the Fed targeted inflation rate of 2%, and only about 0.2% above the latest 1.7% inflation rate.

Menzie can correct me if I have gotten any of this wrong.

Barkley Rosser: Your description is exactly correct. I would say that anybody who was looking at TIPS yields in November of 2008 would’ve known there had to be a liquidity premium for TIPS.

Professor Chinn,

Thanks for instruction.

For 3/31/2021 I find:

FRED series, T5YIE = 2.54

KWW series, exp.inflation.5 = 1.83

Difference = 0.71, somewhat close to 0.64 as reported in the blog

Is this due to update of data by KWW?

Also, how do we test the accuracy of the forecast? Do we lag the KWW data by 60 months and compare to actual CPI?

AS: Not sure why the difference, but as I explained before, I think KWW calculate using *fitted* values of DGS5 and DFII5, and not actual.

For testing accuracy, yes, lag the implied forecast by 60 months.

Professor Chinn,

Apologies, the lagged comment did not “sink-in” regarding lagged vs actual data used for comparison to expected inflation.

Thanks again

Well, I know this doesn’t fit on an economics blog, but after the last 4 years, I just can’t resist.

I guess if you’re a “conservative” Republican and you like trading in pay to play underage girls, you now know who your core constituency is:

https://www.yahoo.com/news/matt-gaetz-scandal-pro-trump-womens-group-pardon-extortion-justice-department-180231490.html

Another “proud moment” for MAGA people everywhere. Bruce Hall and sammy must be beaming with pride. We’ll have to check in with “Princeton”Kopits to see if he considers this statutory rape if the victim of the MAGA perpetrator is a brown person. Updates soon.

https://www.nytimes.com/2019/08/24/opinion/sunday/economics-milton-friedman.html

August 25, 2019

Blame Economists for the Mess We’re In

Why did America listen to the people who thought we needed “more millionaires and more bankrupts?”

By Binyamin Appelbaum

In the early 1950s, a young economist named Paul Volcker worked as a human calculator in an office deep inside the Federal Reserve Bank of New York. He crunched numbers for the people who made decisions, and he told his wife that he saw little chance of ever moving up. The central bank’s leadership included bankers, lawyers and an Iowa hog farmer, but not a single economist. The Fed’s chairman, a former stockbroker named William McChesney Martin, once told a visitor that he kept a small staff of economists in the basement of the Fed’s Washington headquarters. They were in the building, he said, because they asked good questions. They were in the basement because “they don’t know their own limitations.”

Martin’s distaste for economists was widely shared among the midcentury American elite. President Franklin Delano Roosevelt dismissed John Maynard Keynes, the most important economist of his generation, as an impractical “mathematician.” President Eisenhower, in his farewell address, urged Americans to keep technocrats from power. Congress rarely consulted economists; regulatory agencies were led and staffed by lawyers; courts wrote off economic evidence as irrelevant.

But a revolution was coming. As the quarter century of growth that followed World War II sputtered to a close, economists moved into the halls of power, instructing policymakers that growth could be revived by minimizing government’s role in managing the economy. They also warned that a society that sought to limit inequality would pay a price in the form of less growth. In the words of a British acolyte of this new economics, the world needed “more millionaires and more bankrupts.”

In the four decades between 1969 and 2008, economists played a leading role in slashing taxation of the wealthy and in curbing public investment. They supervised the deregulation of major sectors, including transportation and communications. They lionized big business, defending the concentration of corporate power, even as they demonized trade unions and opposed worker protections like minimum wage laws. Economists even persuaded policymakers to assign a dollar value to human life — around $10 million in 2019 — to assess whether regulations were worthwhile.

The revolution, like so many revolutions, went too far. Growth slowed and inequality soared, with devastating consequences. Perhaps the starkest measure of the failure of our economic policies is that the average American’s life expectancy is in decline, as inequalities of wealth have become inequalities of health. Life expectancy rose for the wealthiest 20 percent of Americans between 1980 and 2010. Over the same three decades, life expectancy declined for the poorest 20 percent of Americans. Shockingly, the difference in average life expectancy between poor and wealthy women widened from 3.9 years to 13.6 years.

Rising inequality also is straining the health of liberal democracy. The idea of “we the people” is fading because, in this era of yawning inequality, there is less we share in common. As a result, it is harder to build support for the kinds of policies necessary to deliver broad-based prosperity in the long term, like public investment in education and infrastructure.

Economists began to enter public service in large numbers in the middle of the 20th century, as policymakers struggled to manage the rapid expansion of the federal government. The number of economists employed by the government rose from about 2,000 in the mid-1950s to more than 6,000 by the late 1970s. At first they were hired to rationalize the administration of policy, but they soon began to shape the goals of policy, too. Arthur F. Burns became the first economist to lead the Fed in 1970. Two years later, George Shultz became the first economist to serve as Treasury secretary. In 1978, Volcker completed his rise from the Fed’s bowels, becoming the central bank’s chairman.

The most important figure, however, was Milton Friedman, an elfin libertarian who refused to take a job in Washington, but whose writings and exhortations seized the imagination of policymakers. Friedman offered an appealingly simple answer for the nation’s problems: Government should get out of the way. He joked that if bureaucrats gained control of the Sahara, there would soon be a shortage of sand….

A good review: “ Applebaum, for example, marches through the Chicago School’s influence in loosening antitrust enforcement and the industrial consolidation that followed. He quotes Milton Friedman who advocated that antitrust laws be repealed entirely because they do more harm than good by punishing natural economic winners. He also quotes the scholar and federal jurist Richard Posner claiming, in 2001, that, other than the economic approach, there was no longer any other perspective—political or legal—taken seriously in antitrust policy. Appelbaum then quotes Posner again, in 2017, as asking “antitrust is dead, isn’t it?” That economists committed the murder barely even needs to be said.” http://bostonreview.net/class-inequality/marshall-steinbaum-games-economists-play

UW’s own Edwin Witte and Selig Perlman were trailblazers in economists’ march to power, serving as technocratic, apolitical policy makers, only to be followed by the free market ideologues who ruled the roost after 1980.

“Applebaum, for example, marches through the Chicago School’s influence”

Like all economists agree with the Chicago school? I’m glad Anne posted this in full. Why because people who teach at Princeton, Berkeley, and even MIT never advocated such free market BS. Quiz for you since you are so obsessed with Krugman. Where did he used to each and where does he teach now?

Careful an honest answer is going to show your obsession is not but a pack of lies. So given us a made up resume. Snicker!

What Krugman teaches at college and publishes in his textbooks and what he preaches from his bully pulpit at the NYT are not necessarily the same thing.

pgl is free to review Krugman’s column and tell us exactly how many times he addressed the pervasive problem of oligopoly in the past year.My cursory scan found barely a mention. With Bernie running for the Democratic nomination, it would have been a great opportunity for a teachable moment.

“What Krugman teaches at college and publishes in his textbooks and what he preaches from his bully pulpit at the NYT are not necessarily the same thing.”

Do you even have a clue WTF you are babbling about? Of course not as you have shown a complete disinterest in reading what he has really said. Not that a moron like you would understand it if you did. You are a pathetic little lying troll. This false attacks on Paul Krugman are a total waste of time. But yet you persist with this pointless parade of dishonesty.

JohnH: I’ve used Krugman’s textbook (now Krugman-Melitz-Obstfeld). I’ve read Krugman’s columns. I’m not sure I’ve ever seen anything in a Krugman column that is contradicted by something in his portion of the textbook.

Krugman is aware of oligopolistic market structure (I certainly know this from suffering through his book w/Elhanan Helpman). In 1984, he published: “Import protection as export promotion: International competition in the presence of oligopoly and economies of scale, 11 in Monopolistic Competition in International Trade, ed. Henryk Kierzkowski, Oxford, UK: Oxford University Press, 1984, 180-193.

Oligopoly shows up in the 6th edition on pages 121, 130, and particularly page 277.

In popular discussion: Monopoly capitalism is killing the US economy. It was cited in an article published by this obscure think tank called… Brookings Institution.

Seriously, of all the people you’re taking issue with, why Krugman?

Why is it that the public has to learn about Krugman’s views on monopoly at Brookings or from a 2016 article in the Irish Times, sources that have relatively little readership in the United States?

I mean, if it’s fit to print at the Irish Times, why not at the New York Times? After all, a NY Times column is one extremely powerful way to influence the debate. And if Krugman truly believes that monopoly capitalism is killing the economy, why not say so from his bully pulpit? How else are the American people supposed to know?

By avoiding, the issue, Krugman actually helps the monopoly capitalists avoid public scrutiny and preserve the suboptimal status quo. This begs the questions: does he not have the courage of his convictions? Or is he just being a politician, saying different things to different audiences? If the latter, what is the public to believe? Personally I no longer go past most of Krugman’s headline, because most of it seems like so much pablum, echoes of opinions found in many places.

For a while, I toyed with the idea that Krugman might have been forced to mince his words in deference to Times advertisers. I now doubt this. Benyamin Appelbaum, the former business and economics editor at the Times, seems to have had no such qualms. Why should Krugman?

https://www.nytimes.com/2019/08/24/opinion/sunday/economics-milton-friedman.html

If Krugman truly believes that monopoly capitalism is killing the economy, why not dedicate one–just one–of his 104 columns (1%) every year to educating the public on how monopoly capitalism is killing the economy, particularly in a year like 2020, when corporate greed was a big issue? Does he prefer they not know?

JohnH: OK, now you revise and extend your remarks, so Krugman was not silent, but he was not loud enough… in the places deemed influential by you. But heck, his int’l textbook is the biggest seller, and Brookings is the premier think tank in the world (in my opinion). But heck, what about that obscure platform called twitter.

Do you really want me to spend my hours looking for more and more instances? Geez.

(By the way, consider this NYT column from 2012).

JohnH: For your reading interest, see this Krugman column:

“My cursory scan found barely a mention.”

Yea right – you did not want to find any mention of market power so you failed to do so. Which shows you are either lazy, stupid, or both.

It took me two seconds to find 365 thousand hits where Krugman mentioned monopoly power. I loved this one but it seems our host has pointed it out already:

https://www.irishtimes.com/business/economy/paul-krugman-monopoly-capitalism-is-killing-us-economy-1.2615956

But this is your standard faire – bash an economist in the most dishonest way and then whine when you get called out on it. Pointless and stupid as always.

“If Krugman truly believes that monopoly capitalism is killing the economy, why not dedicate one–just one–of his 104 columns (1%) every year to educating the public on how monopoly capitalism is killing the economy, particularly in a year like 2020, when corporate greed was a big issue? Does he prefer they not know?”

JohnH, perhaps if the right did not intentionally create dumpster fires all across the economy, we could settle down and deal with these systemic problems. but the past four years, for instance, trump was busy creating intentional crisis after crisis that was being addressed in real time by krugman and others. if we can move past these types of distractions for a while, perhaps we can begin to address some of these bigger issues. if you notice, biden is minimizing such distractions, and truly addressing big problems such as economic issues related to covid and our ignorance of infrastructure for decades. this will probably permit folks like krugman to similarly begin to address systemic issues on a bigger scale.

https://www.nytimes.com/2021/04/05/business/economy/robert-mundell-dead.html

April 6, 2021

Robert A. Mundell, a Father of the Euro and Reaganomics

His insights on global finance earned him a Nobel, while his more iconoclastic theories fostered the adoption of a single European currency and supply-side economics.

By Tom Redburn

Robert A. Mundell, a Nobel Prize-winning economist whose theorizing opened the door to understanding the workings of global finance and the modern-day international economy, while his more iconoclastic views on economic policy fostered the creation of the euro and the adoption of the tax-cutting approach known as supply-side economics, died on Sunday at his home, a Renaissance-era palazzo that he and his wife restored, near Siena, Italy. He was 88.

The cause was cholangiocarcinoma, cancer of the bile duct, said his wife, Valerie Natsios-Mundell.

Professor Mundell, a Canadian who taught at the University of Chicago and Columbia University, among other places, was awarded the Nobel Memorial Prize in Economic Sciences in 1999 “for his analysis of monetary and fiscal policy under different exchange rate regimes and his analysis of optimum currency areas.”

His remarkably clear-minded work, mostly conducted from the mid-1950s through the early ’60s — a time when exchange rates were stable and global capital movements were modest — was far ahead of its time.

“Mundell chose his problems with uncommon — almost prophetic — accuracy in terms of predicting the future development of international monetary arrangements and capital markets,” the Nobel committee wrote.

Professor Mundell is credited as the co-developer of the Mundell-Fleming model, which added a crucial dimension to the field by creating an elegant way to move beyond the study of self-contained national economies. (Marcus Fleming, a colleague at the International Monetary Fund in the early 1960s, came up with similar ideas at roughly the same time.)

“You have created modern open-economy macroeconomics,” Jacob Frenkel, a former governor of the Bank of Israel, wrote in the inscription of a book on Professor Mundell’s theories. “My generation of economists owe you all that we know.” …

Mundell’s open economy macroeconomics was a real break through. Now his supply side musings were a bit sad.

Dr. Martin Tobin just finished his testimony in the Derek Chauvin trial. What an outstanding witness for the prosecution. The defense attorney’s cross was as lame as the rest of his racist and demeaning questioning of witnesses. I said it earlier but it looks the defense strategy is an appeal based on incompetent counsel.

Core CPI was up 1.3% y/y in February, same as the 3 month annualized rate of change. An expected 1.9% inflation rate anticipates a moderate acceleration, but only to about the recent 5-year average for cor CPI. This is a 5-year period which the FOMC has assessed inflation to be too slow. The Fed’s goal in the coming 5 years or so is to push inflation above 2%. Oops.

Biden needs to spend more? Assuming the infrastructure plan manages to boost productivity, term premium should rise. However, if inflation stalls around the 5-year average, a modest rise in term premium and a Fed that will not have reached it’s inflation target mean Treasury yields won’t rise all that much.

Apologies for getting back on topic.

I’ve discussed this matter with the Elders of QAnon, and we’ve decided if this is a one time event, we’ll let your on-topic comment slide. Just don’t let it happen again.

I will humbly comply.

The rate of wholesale inflation over the past 12 months climbed to 4.2% in March.

https://www.marketwatch.com/story/u-s-producer-price-inflation-posts-biggest-annual-increase-since-2011-11617974918

Steven Kopits Good thing you provided a link. That way readers can do what you didn’t do; viz., put that PPI rise in context:

Big picture: The data show that supply-chain issues combined with recovering demand is placing upward pressure on a broad array of prices at the producer level, said Josh Shapiro, chief U.S. economist at MFR Inc. Federal Reserve officials expect these gains will be temporary.

The key word is the last word…temporary.

Come on man – if Princeton Steve is not allowed to cherry pick and manipulate how do you expect him to get back on Fox and Friends?

Let’s also back up a sentence earlier:

‘Core prices, which strip out volatile foods, energy and trade prices, rose 0.6% in March and were up 3.1% year-on-year, its highest level since September 2018.’

But we should not be interrupting Stevie’s cherry picking as he really needs another appearance on Fox and Friends to pay the bills.

Auto prices are due for further gain in the near term. Microchip shortages are leading to factory shutdowns, as has been anticipated for some time.

Covid related? Well, kinda. Auto firms expected weak salrs, so cut back on chip orders. Oops.

This, too, is a temporary phenomenon. So not a monetary policy phenomenon, but we will no doubt be urged to panic when vehicle prices rise.

Cherry picking data again? Has oil prices past $100 a barrel yet?

Our host has request commenters provide sources to reliable data such as this from FRED on the producer price index:

https://fred.stlouisfed.org/series/PPIACO

That is a good thing especially given the last misrepresentation from Princeton Steve. From the summer of 2018 to early 2020, PPI had flat lined. When the pandemic hit, PPI fell sharply. So when Stevie frets that PPI has risen quite a bit over the past year – he is deliberating misrepresenting reality.

Look I have given up on him write a coherent comment involving basic finance or economics, but down right dishonesty? Yea that is Princeton Pompous Steve all over.

2 Slugs,

To follow-up on your comments.

It looks like we will see “high” inflation for the remainder of 2021 for Producer Price Index Final Demand, FRED series, PPIFIS, if the index remains at the March 2021 value of 123.1 or goes higher.

https://fred.stlouisfed.org/series/PPIFIS/

Assumed ending value of 123.1 for PPIFIS

Month Y/Y % change

2021-04-01 5.5

2021-05-01 5.0

2021-06-01 4.7

2021-07-01 4.1

2021-08-01 4.0

2021-09-01 3.7

2021-10-01 3.1

2021-11-01 3.1

2021-12-01 2.8

If the index retreats to the December 2020 value of 119.7, the inflation rate will be in a more “friendly” range.

Assumed ending value of 119.7 for PPIFIS

Month Y/Y % change

2021-04-01 2.6

2021-05-01 2.1

2021-06-01 1.8

2021-07-01 1.3

2021-08-01 1.1

2021-09-01 0.8

2021-10-01 0.3

2021-11-01 0.3

2021-12-01 0.0

I like your FRED graph. Could you please Princeton Steve what the PPI inflation rate as from the summer of 2018 to just before the pandemic? And can you remind this cherry picking troll what happened to PPI after the pandemic began.

There is a reason we rarely see macroeconomists use PPI as CPI as the measure of inflation. Something called variability. Then again maybe Princeton Pompous will pull a Judy Shelton and use gold or oil prices to capture general inflation.

I have praised this post by Menzie and generally approved of the methodology here. Nevertheless I must note a caveat on all this. It is that the estimates for both the Treasury premium and Liquidity premium are both derived from models. They are not hard numbers in and of themselves in the way that the nominal 5-year Treasury note rate is or the 5-year TIPS rate is. Their difference, the “beakeven inflation” number is a hard number derived simply by subtracting one market number from another, and it is almost certainly what most people views as the “rational market” forecast of the rate of inflation 5 years from now, even if such “rational” forecasts have not had all that great of a forecasting record.

The arguments for adjusting for tpr and lp are sound. The problem is that there is not an unequivocal or clear way to know precisely what those numbers are. They are estimated from models that make assumptions that may not be correct. Bottom line is that those numbers are fuzzy, so nobody should bet their mortgages on that 1.9% real 5 year inflation forecast. About the best that can be said is that recognizing those factors means that the 2.52% breakeven inflation number is almost certainly too high. But how much too high depends on what model one uses to estimate tpr and lp.

I have noticed at least two FRED inflation estimate series, T5YIE https://fred.stlouisfed.org/series/T5YIE

and T5YIFR . https://fred.stlouisfed.org/series/T5YIFR.

We have discussed T5YIE but have not discussed T5YIFR as defined below.

This series [TY5IFR]is a measure of expected inflation (on average) over the five-year period that begins five years from today.

This series is constructed as:

(((((1+((BC_10YEAR-TC_10YEAR)/100))^10)/((1+((BC_5YEAR-TC_5YEAR)/100))^5))^0.2)-1)*100

where BC10_YEAR, TC_10YEAR, BC_5YEAR, and TC_5YEAR are the 10 year and 5 year nominal and inflation adjusted Treasury securities. All of those are the actual series IDs in FRED.

Starting with the update on June 21, 2019, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department.

The April 9, 2021 estimate for T5YIE is 2.51%

The April 9, 2021 estimate for T5YIFR is 2.11%

Some expert explanation seems required.