Today, we are fortunate to be able to present a guest contribution written by Agustín Bénétrix and André Sanchez Pacheco (Trinity College Dublin).

The degree of international financial integration (IFI) of a country is conventionally measured using cross-border estimates of its external assets and liabilities. However, focusing on cross-border positions may leave important international investments out of the calculation. When analysed through a consolidated-by-nationality approach, we find that the U.S. economy is substantially more integrated to the rest of the world. U.S. consolidated-based IFI doubled between 1999 and 2018, driven mainly by U.S. multinationals expanding their global footprint. As an example of the many potential uses of these data, we document the relation between corporate income tax differentials and U.S. international financial integration not captured by standard cross-border statistics.

How can one measure the degree of financial integration of an economy to the rest of the world? One frequently used de-facto measure is the index of International Financial Integration (IFI) proposed by Lane and Milesi-Ferretti (2003). This measure is calculated as the sum of the external assets and liabilities of a country divided by its Gross Domestic Product. External assets and liabilities are typically estimated using a residence-based methodology in which only cross-border transactions are considered. Assets and liabilities are then apportioned according to the residence of the immediate counterparts of such transactions.

However, focusing on cross-border positions may leave important foreign investments out of the calculation. For example, consider the affiliate of a U.S. multinational enterprise (MNE) operating in a foreign country, say the Netherlands. The local assets held by this affiliate represent assets of a U.S. company located outside the U.S. (in the Netherlands) and liabilities of Dutch agents relative to a company whose ultimate owner does not reside within the same border. These assets can be characterised as international investments made by an U.S. company in a foreign country. Yet the local assets held by this affiliate are not booked as U.S. external assets nor Dutch external liabilities when using the cross-border approach. As a result, these will be left out when computing the IFI of both countries.

An alternative approach that accounts for these international investments is to apportion assets and liabilities according to the nationality of the ultimate owner. This is equivalent to consolidating the local assets and liabilities of affiliates to the parent company and then assessing the international exposure of countries. In our example, this consolidated approach would imply booking the local assets of the U.S. affiliate in the Netherlands as U.S. foreign assets and Dutch foreign liabilities even though these are not cross-border investments. In principle, we can apportion any asset or liability to their ultimate owner. One can aggregate assets and liabilities according to the nationality of their owners and construct the entire foreign balance sheet of a country using this consolidation procedure.

Bénétrix and Sanchez Pacheco (2021) construct an estimate of the U.S. foreign balance sheet adopting a consolidated-by-nationality approach for the period between 1999 and 2018. The methodology used follows that of BIS (2015) and relies on publicly available data to produce a novel time series estimate of the consolidated balance sheet of the U.S. We then use such series to compute the index of U.S. International Financial Integration and analyse its evolution over the sample period.

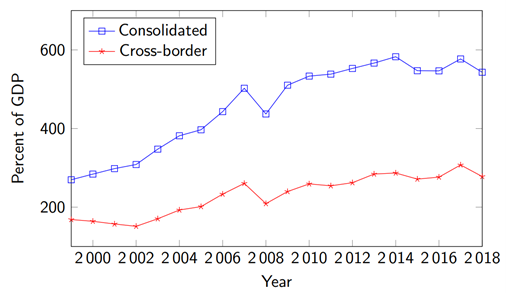

Figure 1 shows the evolution of U.S. IFI based on the consolidated approach and compares it to the same measure calculated using the conventional cross-border. This figure shows that IFI is on average two times larger when calculated using the consolidated approach relative to the cross-border approach. It indicates that U.S. nationals hold sizeable amounts of assets and liabilities relative to foreigners that are not captured by cross-border statistics.

Figure 1 U.S. International Financial Integration

Note: This figure shows the evolution of consolidated-based and cross-border based measures of U.S. International Financial Integration. U.S. IFI is computed as the sum of foreign assets and liabilities divided by GDP. Our calculations do not include financial derivatives given the existing challenges to determine the nationality of their ultimate owners.

This figure also shows that IFI increased substantially between 1999 and 2018. We find that the consolidated-based measure of U.S. international financial integration doubled in this horizon and represents 543% of U.S. GDP by the end of our sample.

The role of multinationals

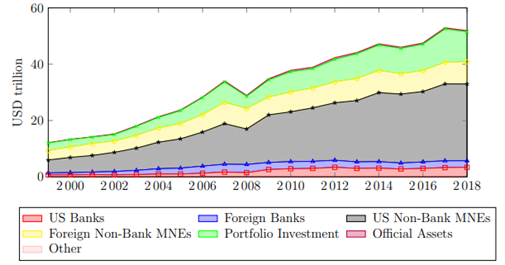

We then investigate the key drivers behind this extraordinary expansion. Figure 2 shows the evolution of foreign assets according to different functional categories/sectors described in our paper. Non-bank multinationals were the single most important contributor driving the expansion of U.S. foreign assets. Similarly, the same pattern emerges when analysing foreign liabilities. Around half of the IFI increase between 1999 and 2018 can be attributed to these companies.

Figure 2 U.S. Consolidated Foreign Assets. Note: This figure shows the time-varying composition of U.S. consolidated foreign assets over the sample period.

The important increase in foreign holdings by U.S. multinationals coincides with the documented rise in profit shifting activities by these companies. Zucman (2014) shows that the share of U.S. corporate profits booked abroad increased substantially since the start of this century.

Corporate taxation and IFI

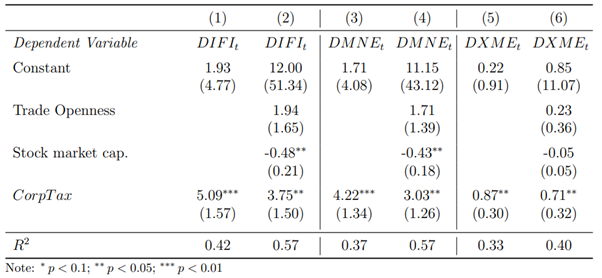

Dischinger and Riedel (2011) find that multinational enterprises shift the location of their intangible assets towards low-tax affiliates within the group. Given the prominent role played by MNEs, we study whether the statutory corporate income tax differential is positively related with IFI. We document a robust relation between tax differentials and IFI when analysing both its cross-border and consolidated-by-nationality versions. Moreover, we investigate whether the difference between the consolidated and cross-border measures (DIFI) is also correlated with the tax differential (CorpTax).

Table 1 shows the regression results of DIFI on the corporate income tax differential and control variables. Columns (1) and (2) show a positive and statistically significant coefficient estimate for CorpTax. To shed light on this result, we decompose DIFI into DIFI related to the activities of multinational enterprises (DMNE) and IFI unrelated to them (DXME). Columns (3) to (6) reveal that the positive coefficient estimates of CorpTax can be largely attributed to multinational enterprises.

Table 1 Regression results of the difference between consolidated and cross-border measures

Taken together, we interpret these results as indirect evidence of U.S. multinationals taking advantage of tax differentials in ways that go beyond what is captured by traditional Balance of Payments procedures. Such findings are robust with respect to different control variables and methodologies used to compute of the corporate income tax differential.

Conclusion

Bénétrix and Sanchez Pacheco (2021) construct the first consolidated-by-nationality foreign balance sheet of any country for multiple years. This approach reveals that the U.S. economy is substantially more integrated to the rest of the world. Using these novel data, we find that the difference between the two IFI measures is positively correlated with the corporate income tax differential. Such finding suggests that the tax differential is associated with an expansion of the global footprint of U.S. multinationals beyond what is captured by cross-border statistics.

This paper is the first of the broader Consolidated Foreign Wealth of Nations project that seeks to create publicly available estimates of consolidated-by-nationality foreign asset and liability holdings for multiple countries. This dataset will complement the seminal work by Lane and Milesi-Ferretti (2001, 2007, 2018) which provides estimates of cross-border based external assets and liabilities for all countries.

References

Bank for International Settlements. (2015). 85th Annual Report.

Dischinger, M and N Riedel (2011). “Corporate taxes and the location of intangible assets within multinational firms”. Journal of Public Economics 95 (7-8): 691-707.

Lane, P R and G M Milesi-Ferretti (2001). “The external wealth of nations: measures of foreign assets and liabilities for industrial and developing countries”. Journal of International Economics 55 (2): 263-294.

Lane, P R and G M Milesi-Ferretti (2003). “International Financial Integration”. IMF Working Papers 2003/086

Lane, P R and G M Milesi-Ferretti (2007). “The External Wealth of Nations Mark II: Revised and Extended Estimates of Foreign Assets and Liabilities, 1970–2004”. Journal of International Economics 73 (2): 223–250

Lane, P R and G M Milesi-Ferretti (2018). “The External Wealth of Nations Revisited: International Financial Integration in the Aftermath of the Global Financial Crisis”. IMF Economic Review 66: 189–222.

Zucman, G (2014). “Taxing across Borders: Tracking Personal Wealth and Corporate Profits”. Journal of Economic Perspectives 28(4): 121-48.

This post written by Agustín Bénétrix and André Sanchez Pacheco.

A common theme in this research:

“Dischinger and Riedel (2011) find that multinational enterprises shift the location of their intangible assets towards low-tax affiliates within the group.”

Back in 2017 we were told by Trump and his fellow Republicans that their tax cut for the rich would reverse all of this with fancy provisions known as FDII and GILTI as the dropping of the US corporate tax rate from 35% to 21%. Brad Setser who works for the Biden Administration knows why these claims are sheer BS. Biden’s team has great ideas of how to address such problems if two certain Blue Dog Senate Democrats get out of the away.

Just those 2?? The problem and truth Biden has with progressives is they are a dialectical lie. Lies cannot last

So do numbers like this include what was in the Panama Papers and the Pandora Papers??

The report is a testament to the success of corporate friendly “free” trade agreements’ investment liberalisation clauses, which were arguably the most important aspect of most agreements. It is also a testament to the success of the Washington Consensus prescriptions, which allowed Wall Street to strip developing countries of their Crown Jewels for pennies on the dollar.

JohnH: I want to remind everyone that “The Washington Consensus” as laid out by John Williamson at PIIE did not include capital account liberalization.

Williams, Williamson, it’s all the same the drunk guy said

Maybe Williamson revised his original list to include Liberalization of Inward FDI?”

https://www.piie.com/publications/papers/williamson0904-2.pdf

In any case, it’s moot. It was or quickly became an integral part of the Washington Consensus and Wall Street’s campaign to pillage the Crown Jewels of foreign countries after financial crises for pennies on the dollar..

“…investment liberalisation clauses, which were arguably the most important aspect of most agreements…”

Well, the post WWII grand-daddy of trade agrements was the GATT. The only binding investment liberalization clause in the initial GATT was, wait,…lemme look…just checking…uh, looks like there wasn’t one. In fact, from 1947 till 1984, the GATT more or less ignored investment liberalization issues. Pesky Canada had to go and spoil things.

But wait. The GATT wasn’t the only big trade deal during the post-war period. There was the Treaty of Paris, which got the ball rolling for European integration. Hang on…gotta check…oh. Uh, there was no investment liberalization clause in the Treaty of Paris.

Of course, there was that agriculture deal, the Common Agricultural Policy? I mean, that thing is just a massively important trade agreement…which was writen without an investment liberalization clause.

Yikes! The “most important aspect of most agreements” isn’t in any of these really important historic trade agreements. How could that be?

Unless Johnny is once again pretending to know stuff.

Johnny, I’ve mentioned this before, but, every time you pretend to know what’s what, I’m reminded of the “jejune” scene in “Love and Death”. ‘Cause I feel like that word was invented for you.

https://m.youtube.com/watch?v=btDqtCGIgGY

I gave up responding to this economic know nothing a while ago so I truly appreciate that you have decided to dissect his incessant confusions piece by piece. Look – there is a lot that multinationals do that should be called out but could we please have well informed critics?

I don’t blame Professor CHinn for correcting him. That’s quite a good thing. BUt we needn’t be too insulting about it. I think JohnH has good intentions about caring for “his fellow man”. Maybe we might take that into the broader picture before throwing french fries across the grade school lunch room.

Macroducks: You must be joking…or willfully ignorant about trade agreements: “Embedded in the North American Free Trade Agreement (NAFTA), the proposed Multilateral Agreement on Investment (MAI), the proposed Free Trade Agreement of the Americas (FTAA), and the terms of various structural adjustment programs of the IMF and World Bank is an agenda to liberalize the flow of investments (and capital generally) throughout the world.”

https://fpif.org/investment_liberalization_agenda/

Yes, initially trade agreements were mostly about trade. But as time went on, more and more things got included, one of the important being investment liberalization.

That isn’t “trade” John. You keep on getting trade confused with capital markets liberalization. Trade itself was irrelevant. Capital market’s no longer having rules of government policy supporting production is far more devastating.

So why was investment liberalization included in trade agreements?

The consensus as originally stated by Williamson included ten broad sets of relatively specific policy recommendations:

7. Liberalization of inward foreign direct investment;

https://en.wikipedia.org/wiki/Washington_Consensus

JohnH: Yes. But that’s not the same as capital account liberalization (e.g., including controls over portfolio investment, etc.).

In my one and only conversation with him in person, he stressed that point…

Right!!! Did I say anything about capital account liberalization?

There may be a legitimate complaint here but could you stop with this embarrassing know nothingism? Damn!

Once again you cannot be bothered to follow your own links:

“White House data reported in 2011 found that a total of 5.7 million workers were employed at facilities highly dependent on foreign direct investors. Thus, about 13% of the American manufacturing workforce depended on such investments. The average pay of said jobs was found as around $70,000 per worker, over 30% higher than the average pay across the entire U.S. workforce.”

I guess you have no idea what foreign direct investment even means. Let’s see – foreign based automobile multinationals manufacturing cars with US labor. Or those giant Korean semiconductor multinationals opening manufacturing facilities in the US.

Now I would think you would see this as as a good thing. But once again JohnH is babbling terms he does not even remotely understand.

As usual pgl tries to distract from the point I was making, which only gives me a chance to reiterate it and provide more evidence!

“Neoliberalism was supposed to reduce the income gap between Mexico’s relatively rich border states and the poorer ones in the country’s middle and south. Supporters claimed that privatizing banks and opening them to foreign ownership would make more capital available for domestic firms in domestic markets. But — in the depressingly familiar pattern of privatization the world over — the PRI reformers sold off the banks to friends, then bailed out the new owners when the peso collapsed a year after NAFTA was passed. Made whole with more than $60 billion of the taxpayers’ money, these crony capitalists resold their banks at a handsome markup to foreign investors. For example, an investment group headed by the well-connected Roberto Hernandez bought Mexico’s second-largest commercial bank for $3.2 billion and sold it to CitiGroup for $12.5 billion. Yet, as 85 percent of the country’s banking system was being turned over to foreigners, lending to Mexican business actually dropped from 10 percent of the country’s gross domestic product in 1994 to 0.3 percent in 2000. The global bankers were more interested in taking deposits and making high-interest-rate consumer loans than in developing Mexico’s internal economy.”

https://prospect.org/features/nafta-failed-mexico/

Wall Street grabitization at work…

“As usual pgl tries to distract from the point I was making”.

You made a point? Oh yea – you are as dumb as macroduck has routinely documented. NEXT!

I’ve talked before on this blog about how people create conspiracy theories, when there are enough real conspiracy theories to keep us all busy. This falls under the real conspiracy theories in my book:

https://theintercept.com/2021/10/11/bani-sadr-reagan-iran-hostages-october-surprise/

Claims? Everyone with any knowledge of this hostage taking knows Carter’s team negotiated the deal but Reagan made sure it was not executed until Jan. 20, 1981.

Of course the peace deal between the US and Vietnam could have been executed in 1968 rather than 1973 had it not been for Republicans in the State Department undermining LBJ’s efforts.

Yes the history of Republicans undermining our national interests for partisan gains does back to our youth.

You doubted? I never doubted, and I never even saw the story from “The Onion”.

In all seriousness, it’s just good to have things verified from different sources. I think it’s good journalism, to keep persistent on this story, as it was pretty obvious what had happened from the start and journalists at that time let Reagan and his staff manipulate them. BTW, I think pgl is letting her mouth/keyboard get ahead of her brain. My memory is Carter’s negotiations were separate from what Reagan was doing. pgl may find it interesting Biden’s prior support of William Casey though:

https://theintercept.com/empire-politician/joe-biden-and-reagan-cia-director-william-casey/

Here’s a breakdown on a lot of the William Casey stuff:

https://irp.fas.org/offdocs/walsh/chap_15.htm

“My memory is Carter’s negotiations were separate from what Reagan was doing.”

Reagan takes credit for what Carter did and old Uncle Moses falls for his spin. Reagan did not do a damn thing to get the hostages released.

Biden’s support for Casey? Did you even read the 1st sentence?

“Joe Biden waged a one-senator campaign to show that Casey was unfit to serve in the post.”

I guess there was some support here or there so Biden’s alleged support for Casey was at least better than your knowledge of basketball. But damn!

If you are going to invoke my name in your boring and worthless trolling – please do not write such incredibly STUPID things.

This was AFTER Biden supported Casey getting the post. Maybe if Biden wasn’t of only slightly superior IQ to you pgl, he would have recognized a corrupt loser upon first sight, and saved the nation a lot of aggravation and shame.

We have found someone even dumber than JohnH:

Moses Herzog

October 12, 2021 at 1:55 pm

Like I said – this drunk troll needs to read his own links.

It was about 9 1/2 years ago when Mitt Romney told AIPAC that Reagan got those hostages out of Iran. Apparently old Uncle Moses was in attendance eating up this praise of St. Reagan. Only problem – Romney lied to AIPAC. And of course old Uncle Moses was too stupid to realize it:

https://www.politifact.com/factchecks/2012/mar/07/mitt-romney/mitt-romney-says-iran-released-hostages-1981-becau/

A fine and important work by Agustín Bénétrix and André Sanchez Pacheco, for which I am grateful.

The extent of national corporate tax revenue loss by taking advantage of competing tax policies is startling. A question though that has puzzled me is how much have ordinary Irish citizens benefited from the adoption of Ireland as a tax haven. What does it mean that per capita GDP for Ireland in 2021 is estimated at ( $99,239) PPP as compared to ( $47,089) for the UK?

https://fred.stlouisfed.org/graph/?g=HDqz

August 4, 2014

Real per capita Gross Domestic Product for Germany and Ireland, 2000-2020

(Percent change)

https://fred.stlouisfed.org/graph/?g=HDqD

August 4, 2014

Real per capita Gross Domestic Product for Germany and Ireland, 2000-2020

(Indexed to 2000)

Ireland makes better beer than the Brits and they do income shifting better as well! Of course the Swiss outdoes all of Europe at income shifting even if their beer is not so great.

David Card a co-winner on the Nobel. This is double good news as it’s a sure bet he will have some kind words for Alan Krueger. So comforting to see this.

Just letting capitalism die is a start. The debt ponzi end game is the retribalzation of economics.

And we thought JohnH wrote gibberish!

Paul Krugman classes the development of the Irish economy as Leprechaun development; another example of such development could be Singapore. However, Leprechaun development may cloud just how successful the development of Ireland or Singapore has been. Using a combination of investment in education and preferential corporate tax policy, Ireland became the fastest growing economy in the European Union and the second highest per capita GDP economy after Luxembourg. Ireland and Singapore used preferential or competitive tax policy to gain the highest levels of per capita GDP.

https://fred.stlouisfed.org/graph/?g=HEhN

August 4, 2014

Real per capita Gross Domestic Product for Germany and Ireland, 1980-2020

(Percent change)

https://fred.stlouisfed.org/graph/?g=HEiG

August 4, 2014

Real per capita Gross Domestic Product for Germany and Ireland, 1980-2020

(Indexed to 1980)

https://www.imf.org/en/Publications/WEO/weo-database/2021/April/weo-report?c=193,122,124,156,128,172,132,134,174,532,178,436,136,158,542,137,546,138,196,142,182,576,184,144,146,112,111,&s=PPPPC,&sy=2007&ey=2021&ssm=0&scsm=1&scc=0&ssd=1&ssc=0&sic=0&sort=country&ds=.&br=1

April 15, 2021

Per capita Gross Domestic Product, 2021

Germany ( 56,956)

Ireland ( 99,239)

Singapore ( 102,742)

Switzerland ( 75,880)

United Kingdom ( 47,089)

United States ( 68,309)

* Data are expressed in US dollars adjusted for purchasing power parities (PPPs).

GDP in the presence of massive transfer pricing games is a misleading statistic. Try GNP.

https://www.macrotrends.net/countries/IRL/ireland/gnp-gross-national-product

Spend some time with this data on Ireland. Their GNP is only 80% of GDP for the reported year. FRED has a nice GNP/GDP comparison for various nations including Ireland but this series cuts off at 2010 for some reason.

Also note trade (exports + imports) seem to be more than 200% of GDP. The same is true for Hong Kong.

How is this possible. Massive reporting issues from transfer pricing games.

https://fred.stlouisfed.org/graph/?g=HEnH

August 4, 2014

Real per capita Gross Domestic Product for United Kingdom and Ireland, 1980-2020

(Percent change)

https://fred.stlouisfed.org/graph/?g=HEnN

August 4, 2014

Real per capita Gross Domestic Product for United Kingdom and Ireland, 1980-2020

(Indexed to 1980)

Taxing income of corporations is fraught with difficulties because it is easy for corporations to hide and transfer their income. But taxing corporate income is the wrong problem.

Corporations exist to earn income for their shareholders. This income is distributed to shareholders in one of three ways — dividends, share buybacks and capital gains. These three are impossible to hide without depriving shareholders of their earnings. So just tax dividends, buybacks and capital gains and forget about corporate income tax.

Yep. But really, you only need divdend and capital gains taxes. Buy-backs generate capital gains. They should be taxed as regular income in a highly progressive tax system.

You have a good point. But taxing shareholders would require us getting rid of all the little stupid loopholes we grant to dividend and capital gains income. I would tax all income as it accrues at the same rate. But then my idea is likely considered COMMUNISM in certain circles.

“But taxing shareholders would require us getting rid of all the little stupid loopholes we grant to dividend and capital gains income.”

Don’t collect the tax from the shareholders. Collect directly from the corporations for their distributions at their source before it gets to the shareholder. For one thing, about 70% of stocks are held by non-taxable entities, so taxing at the source would have a broader base and would require a lower tax rate for the same revenue.

The reason dividends and capital gains receive preferential tax treatment is to encourage investment. Do you believe investment should be encouraged?

The implication of your rhetorical question is that if those things were taxed more, the incentive wouldn’t STILL be there and be strong. The reality is that there would still be strong incentive for investment, even with an increased tax rate. We have the record of the 1950s and 1960s to point to.

“The reason dividends and capital gains receive preferential tax treatment is to encourage investment.”

I get that Donald Luskin makes this really dumb argument but anyone who actually gets financial economics realizes it is pure BS. Yea after-tax return rises with a lower rate but so does risk taking.

I would explain the simple math of this expected return to risk calculus but it would be over your head. Now take off your shoes so you can count past 10.

https://www.sciencedirect.com/science/article/abs/pii/016517659290225N

I had to go back some 29 years ago when I read this short (4 page) paper in Economic Letters entitled “Does reducing the capital gains tax rate raise or lower investment?”.

The basic finance would suggest the answer is that reducing the cap gains tax would lower investment.

Obviously sammy has never read it. He should. Then again the author appeals to the logic of the Capital Asset Pricing Model, which I doubt is something sammy would ever understand.

sammy,

People buying stocks in the stock market is not capital investment, which is building productive means of production, and it is only peripherally related to that. It is for rich people to make money, as noted by others here. If you want to tax incentivize real capital investment, then the breaks should go to companies actually carrying out real capital investments, not to shareholders of their stocks for receiving dividends or capital gains. The latter just encourages speculation.

No, the reason that dividends and capital gains get preferential treatment is because rich people write the tax laws.

Dividend and capital gains tax rates were higher in the past when the U.S. had just as high and higher growth rates. Rich people are just making up excuses for lowering their tax rates. And you believe them?

“And you believe them?”

Actually sammy does not believe their intellectual garbage. But they pay this lying troll to spread their lies here. They have the money and poor sammy needs it to pay his rent.

A simple illustration of the effect of taxes on investment:

A company is evaluating whether or not to build a new factory at a cost of $1M. Expected profits from the new factory are $1.5 million or a 50% ROI and assuming the various risks associated. Now apply an additional 20% tax rate on the profits. $1.5M x 20% =$ 300K, so now the expected profits from the new $1M factory are $1.2M, or a 20% ROI, assuming the same risks.

sammy: In addition to tax rates (cap gains, income), don’t forget about depreciation rates for tax purposes. In other words, you have cited (incompletely) the formulate for the user cost of capital. Which is hard to get to matter in empirical models of aggregate capital investment…

So, Sammy, you haven’t said what else the CEO might do with $1 million. The shareholders are going to look at the CEO and say “You have an opportunity to earn us $300,000 and you are going to turn it down and do nothing because you are in a snit about taxes? You’re useless. You’re fired.”

And you can make the opposite argument about corporate tax rates. Back in the days of 50% tax rates, AT&T Bell could give half their profit to the government in taxes or they could instead spend it on cutting edge research in their labs and keep all of it. High tax rates encouraged investment.

On top of that – we gave sammy a little homework assignment as in that 1992 Economic Letters paper on this topic. I guess he either forgot to read it or it went over his head as it invoked logic tied to the Capital Asset Pricing Model. Asking sammy to understand one of the seminal theorems in all of financial economics I guess is expecting too much.

A 50% return on investment. Yea – that must be a YUUGE premium for bearing risk. Of course you little example forgets about the risk transfer issue in that 1992 paper we asked you to read.

Until you learn a little financial economics and read the economic literature, might I suggest you stop posting comments that embarrass your entire family?

“assuming the same risks”.

That statement by itself proves you do not understand even your own example. Come on Sammy – learn a little financial economics before playing a game that is way over your head.