Deja vu all over again – China retaliates, and again soybeans are on the list.

Also a lot of other food items.

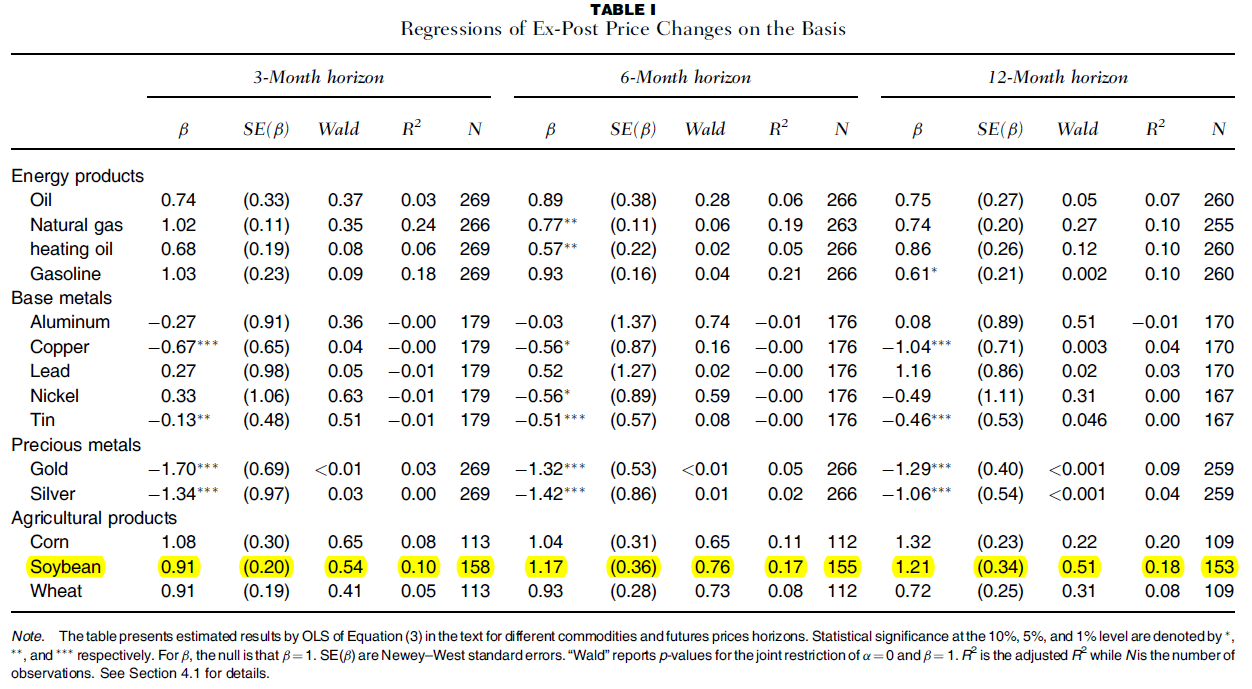

Some people (the now banned CoRev) argued against the usefulness of futures, despite Chinn and Olivier Coibion (Journal of Futures Markets, 2014), in which we evaluate — among other commodities — soybean prices. V. Fernandez (Resources Policy, 2017) conducted an update of our work, confirming our results.

To see our results, consider estimating the following equation, using OLS.

st+k – st = α + β(ft,k – st) + ut+k

Where st is the log spot rate at time t, ft,k is the log futures rate for a transaction k periods hence, and u is an error term that is under the efficient markets hypothesis null a random expectations error (an innovation).

In Table I (from Chinn and Coibion, 2014), I highlight in yellow the SOYBEAN results of this regression for soybeans, at the 3, 6 and 12 month horizons.

Table I from Chinn and Coibion, 2014.

Notice the point estimates are close to one, and statistically indistinguishable from that value, using standard errors robust to serial correlation and heteroskedasticity. Hence, the testing approach is conservative. A Wald test for the joint null α=0, β=1 is not rejected at conventional levels. That null hypothesis is consistent with the futures price being an unbiased predictor. In words, the results mean when the basis is 1%, the average change in the soybean price over the corresponding period will be…1%.

Interestingly, the R2’s are high for soybeans. In contrast, similar results are not obtained for metal commodities. In particular, the estimated β’s are often negative. Hence, we can conclude that futures are unbiased predictors of future spot soybean prices for horizons of up to a year, and have measurable predictive power. For more on prediction (warning: one needs to know at a minimum what an ARIMA is, better yet to know the characteristics of a DMW statistic, in order to understand the content), see this post.

The good news is, this comes as doubts about Brazil’s ever-expanding soy acreage were cropping up. Brazilian farmers’ assault on the rain forest can continue a while longer.

Salt in the wound:

https://www.marketplace.org/2025/03/03/soybean-innovation-lab-usaid-funding-uiuc-soy-agriculture-farming-trump/

USAID isn’t pushing soy in Africa anymore, ’cause USAID doesn’t do anything anymore.