Analysis of current economic conditions and policy

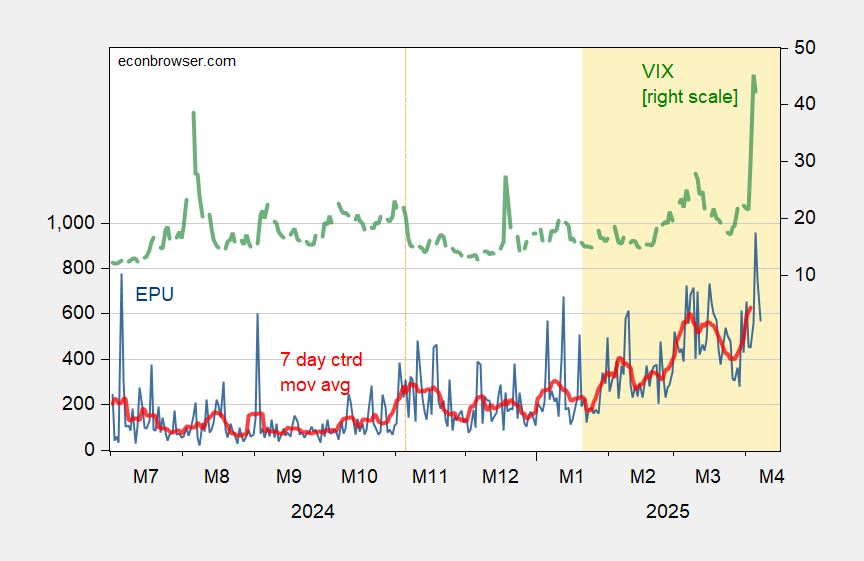

Policy Uncertainty and VIX Down (from Pretty High Levels…)

Data available as of 11am CT today:

7 thoughts on “Policy Uncertainty and VIX Down (from Pretty High Levels…)”

baffling

10 year yields are back to where we started from last week. I just think that is strange. while the vix dropped, it is still elevated at is highest levels outside of the covid period. and yet the 10 year yield is flat from a week ago. I am worried about something, but I don’t know what. yet.

Macroduck

I’m just speculating – I haven’t done the math…the weather has cleared, so math has to wait. The little math I have done agrees with you – it’s odd.

Menzie has pointed out the increased inversion of the curve in the 2-to-3-year range. So if tens are absorbing more of the “flation” part of stagflation, while shorted-dated Treasuries benefit more from recessionary and Fed rate expectations, that might explain why tens didn’t rally like crazy. If higher inflation due to tariffs is persistent, then the inflation premium for longer-dated Treasuries is going to increase a bunch. However…

Here’s a picture of 5-year/5-year inflation expectations:

That big dip on Thursday and Friday (4/3-4) doesn’t fit my explanation; it says inflation expectations fell in response to the Orange Crisis ™. I can’t find any daily 2-year inflation expectations measures on Fred, so I haven’t compare short to long, but the inflation premium on tens doesn’t look, at first glance, like it has blown out.

I’ll fiddle with this further once the sun goes down, but I can’t promise anything useful.

Macroduck

The White House keeps babbling about how many countries have “been in touch” about tariffs. That’s what grown-up countries do when threatened. They know that diplomacy might help avoid a recession, so they engage in diplomacy.

The felon wants a line of foreign leaders outside his door that he can point to – “Look at those important people, dancing to my tune.” Ridiculous. A line outside his door doesn’t do this country any good, just his ego.

Sharon

I cant believe the crazyness. I found your article on http://www.google.com

when I was searcing for better news… oh man.

Macroduck

The good Professor is a little weak when it comes to sugar-coating. We’re trying to help him with his bedside manner, but it doesn’t seem to take..

Macroduck

I recently ranted that the felon-in-chief is doing something very much like Liz Truss and Kwasi Kwarteng’s “mini-budget” in terms of arrogance and stupidity. Brad DeLong argues instead for Brexit as the apt comparison:

Pretending that one’s pinhead dogma should be made into actual policy has cost the UK massively. Per capita income is still 4% lower today than it was eight years ago when the Brexit vote was held. EU per capita income, meanwhile, has risen 15%. The felon isn’t just withdrawing from a regional trade group, though he does seem set on destroying NAFTA. Rather, he is trying to withdraw from the world. The felon has the example of Brexit, and Liz Truss, but examples don’t help if you don’t crack a book once in a while. So he plowed ahead with the same sort of mistakes as the Tories made.

Economic quackery comes in a variety of shapes. The trade deficit at the heart of the felon’s looney tariff idea is the result of decades of tax-cut quackery. Piling a withdrawal from the world on top of giant budget and trade deficits answers one type of quackery with another.

Anonymous

Yves Smith goes through this at Naked Capitalism

I think there is a run to pull cash out of risk, and a view to inflation lowering demand in the long bonds.

10 year yields are back to where we started from last week. I just think that is strange. while the vix dropped, it is still elevated at is highest levels outside of the covid period. and yet the 10 year yield is flat from a week ago. I am worried about something, but I don’t know what. yet.

I’m just speculating – I haven’t done the math…the weather has cleared, so math has to wait. The little math I have done agrees with you – it’s odd.

Menzie has pointed out the increased inversion of the curve in the 2-to-3-year range. So if tens are absorbing more of the “flation” part of stagflation, while shorted-dated Treasuries benefit more from recessionary and Fed rate expectations, that might explain why tens didn’t rally like crazy. If higher inflation due to tariffs is persistent, then the inflation premium for longer-dated Treasuries is going to increase a bunch. However…

Here’s a picture of 5-year/5-year inflation expectations:

https://fred.stlouisfed.org/graph/?g=1HWgI

That big dip on Thursday and Friday (4/3-4) doesn’t fit my explanation; it says inflation expectations fell in response to the Orange Crisis ™. I can’t find any daily 2-year inflation expectations measures on Fred, so I haven’t compare short to long, but the inflation premium on tens doesn’t look, at first glance, like it has blown out.

I’ll fiddle with this further once the sun goes down, but I can’t promise anything useful.

The White House keeps babbling about how many countries have “been in touch” about tariffs. That’s what grown-up countries do when threatened. They know that diplomacy might help avoid a recession, so they engage in diplomacy.

The felon wants a line of foreign leaders outside his door that he can point to – “Look at those important people, dancing to my tune.” Ridiculous. A line outside his door doesn’t do this country any good, just his ego.

I cant believe the crazyness. I found your article on http://www.google.com

when I was searcing for better news… oh man.

The good Professor is a little weak when it comes to sugar-coating. We’re trying to help him with his bedside manner, but it doesn’t seem to take..

I recently ranted that the felon-in-chief is doing something very much like Liz Truss and Kwasi Kwarteng’s “mini-budget” in terms of arrogance and stupidity. Brad DeLong argues instead for Brexit as the apt comparison:

https://braddelong.substack.com/

I’m fine with that.

Pretending that one’s pinhead dogma should be made into actual policy has cost the UK massively. Per capita income is still 4% lower today than it was eight years ago when the Brexit vote was held. EU per capita income, meanwhile, has risen 15%. The felon isn’t just withdrawing from a regional trade group, though he does seem set on destroying NAFTA. Rather, he is trying to withdraw from the world. The felon has the example of Brexit, and Liz Truss, but examples don’t help if you don’t crack a book once in a while. So he plowed ahead with the same sort of mistakes as the Tories made.

Economic quackery comes in a variety of shapes. The trade deficit at the heart of the felon’s looney tariff idea is the result of decades of tax-cut quackery. Piling a withdrawal from the world on top of giant budget and trade deficits answers one type of quackery with another.

Yves Smith goes through this at Naked Capitalism

I think there is a run to pull cash out of risk, and a view to inflation lowering demand in the long bonds.

Maybe margin calls, and hedge funds going cash.