That question was posed in the WSJ, and poses three possible answers:

There are three possible answers:

First, it’s too early to tell. Most of the tariffs announced haven’t been in place long. …

Which leads us to the second possibility—the tariffs thus far have just not been big enough to cause the harm economists warned us about from full-on protectionism. The U.S. is a relatively closed economy …

So third, and tantalizingly, perhaps the conventional wisdom is wrong. Or, more precisely, since no one can deny the effect of taxes are real, perhaps, in their rush to emphasize the negatives, economists have overlooked the countervailing forces at work with tariffs: The redistribution of the burden of duties between foreign exporters, U.S. importers and consumers may be reordering the balance of benefit between domestic and foreign businesses and between companies and consumers. Federal tariff revenue up to $300 billion a year will produce gains for Americans.

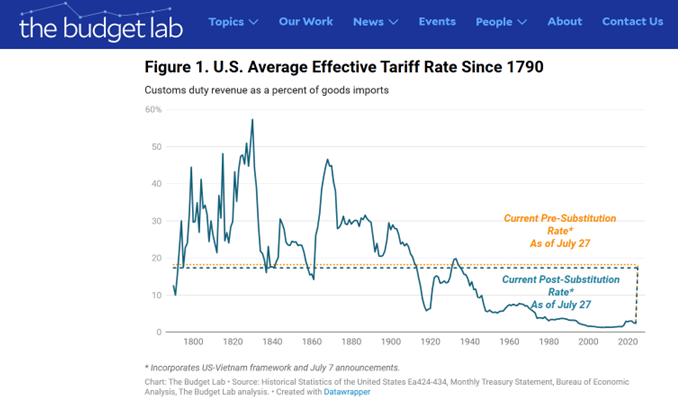

On count 1, I’d remark that most of the tariffs haven’t into play yet. See the effective tariff rate as calculated by the Budget Lab.

Source: Budget Lab, accessed 7/28/2025.

Baker also doesn’t mention the buffering effect of pre-tariff inventory accumulation, which is strange as most of the economics commentary mentions this factor.

On the second point, it’s true the US economy is relatively closed as compared to say UK, or Singapore in an extreme example. But it’s more open than it was just 50 years ago, and more of the trade is of differentiated goods, included in value chains. That magnifies the impact of tariffs. So I think when the tariffs are actually in place, we will see effects (although with USMCA exemptions still in place, we won’t have it as bad as it could be).

The third point is one where Baker is trying to channel the optimal tariff theory. There is a tariff rate that — given the elasticities — maximizes welfare for the country imposing tariffs. But in general such tariff rates are not typically 10-15%, since the US is not a large economy in the context of other countries’ exports. Moreover, empirically, in the 2018 trade war, prices did not behave in a way consistent with this thesis. Most of the burden was borne by US consumers (broadly defined as domestic households, firms, workers). See pp. 133-34 in Chinn and Irwin, International Economics (CUP, 2025).

Addendum:

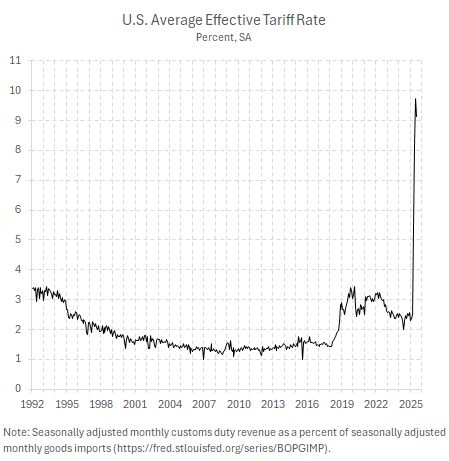

Paweł Skrzypczyński estimates July effective tariff rate at about 9.1%.

Most of the burden is borne by US consumers – no one on Fox or WSJ seems to mention this – I’m sure the Titans of Capitalism will do well regardless.

A news item I found interesting – in light of the U.S. housing market is somewhere around 15-18% of U.S. GDP is this: “US Housing Market Posts Worst Spring Selling Season in 13 Years” (also I recall that Harris had a plan for a first time home buyer credit.) https://www.bloomberg.com/news/articles/2025-07-28/us-real-estate-market-high-prices-mortgage-rates-hamper-spring-home-selling

I say we are heading into stagflation – slower growth and higher prices – rather than a recession.

From Bank of America:

https://www.yahoo.com/finance/news/not-just-cyclical-recovery-boom-195339244.html

I have not seen any evidence of the manufacturing boom that was promised. Further, trump promised me a 2% mortgage, which we are very far from. Bruce, it seems you have been too busy promoting policies that resulted in dozens of young girls drowning in texas rather than fulfilling your economic promises. And last i heard from you, you defended the gun used to kill several people in new york city. Well done comrade.

Brucie seems unwilling even to describe the article he has linked to, perhaps because he has so often been caught mischaracterizing his own links. So here’s the gist:

A Bank of America note argues that a boom is a “tail risk” for the U.S. economy, citing five factors supporting growth. Four of those five are spending plans of one sort or another – U.S. fiscal plans (twice), European fiscal plans, corporate spending plans. The fifth reason is a proprietary BofA indicator which is currently negative, but which might turn positive.

Y’all know what “tail risk ” means? Here’s part of what Investopedia has to say:

“Tail risks include events that have a small probability of occurring…”

So, what we know from the BofA article is that a Keynesian spending surge creates a small probability of a boom. Implicit in this view is that some other outcome is far more likely and that any such boom will come at the expense of a big increase in debt. What should also be noted is that in the U.S. and Europe, the type of Keynesian boost we’ll be seeing is military rather than goods and services enjoyed by the public. Thought I should mention that in case anyone is curious.

“any such boom will come at the expense of a big increase in debt.”

this is the point worth emphasizing. so bruce, are you all of a sudden ok with spending trillions in additional debt? let’s get this put in writing, boy. or are you simply going to silently hide in the corner and ignore these inconvenient items?