Last semester, teaching the Financial System, I laid out three things that worried me: Crypto & stablecoins, private credit, and the AI boom. How’re things looking for the latter?

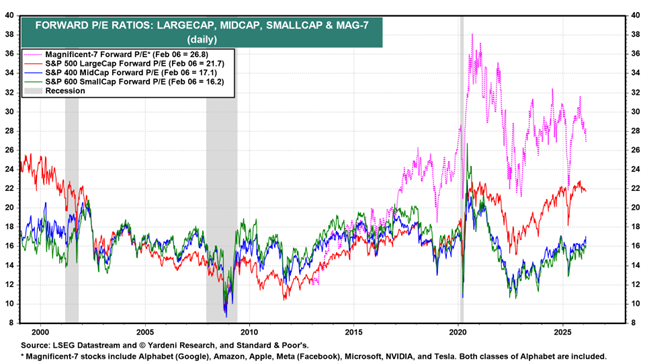

Despite recent movements in Magnificent 7 prices, forward price earning ratios remain elevated.

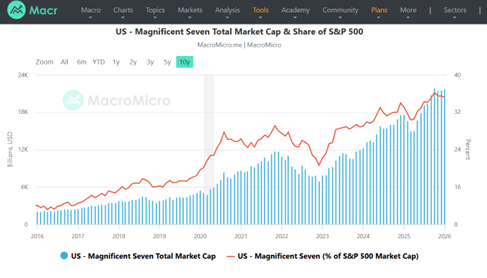

Through January, Magnificent 7 accounts for 35.7% of the SP500 capitalization. Or $21.7 trillion.

At the end of Q3, household net worth was $172.9 trillion, so the Magnificent 7 capitalization accounted for about 12.1% of household net worth at that time.

A big correction of the dot.com bust nature (about 20%) decline would have a substantial impact, given the greater holding of stock market assets now. I provide a back -of-the-envelope calculation of first round effects on consumption, here.

A large correction would finance-constrain AI-related firms aside from the Magnificent 7. The Magnificent 7 up to now have largely relied on internal funding (and even Amazon has indicated that going forward, that’s less true); that’s not true for many other firms that have relied on debt.

Recent reports put capital investment plans for 2026 at about $665 bn. 2025q3 nonresidential fixed investment as about $4300 bn (SAAR). Assuming the same rate for all of 2026, one gets a share of about 15.5%. Should there be a big drop in AI-related spending, that will also hit aggregate demand.

Sharp declines in asset prices usually leads to greater losses in risky assets, almost no matter which assets fall first. If AI shares – or debt – crumble, then portfolio risk reduction will lead to knock-on selling of riskier assets. Emerging markets are always a favorite, as are growth stocks and anything heavily leveraged.

There’s reason to question whether Treasuries would be a big winner in a flight to safety. Domestically, that’s still a pretty likely choice. Internationally, not so obvious right now.

I would prefer to invest in Japan’s national debt instead of US national debt if rates are the same. There is only $9 trillion of Japan treasuries vs. $38 trillion of US. But the market for Japan’s bonds are at least big enough that they can drag US rates up – especially since Trump has declared a weak $ policy.