That’s the title of a paper By Şebnem Kalemli-Özcan Liliana Varela that I had the opportunity to discuss at the NBER’s International Seminar on Macroeconomics (Stockholm, June 24-25).

This paper, covering both industrial country and emerging market currencies (against the dollar) investigated this object — the UIP premium from the local market perspective:

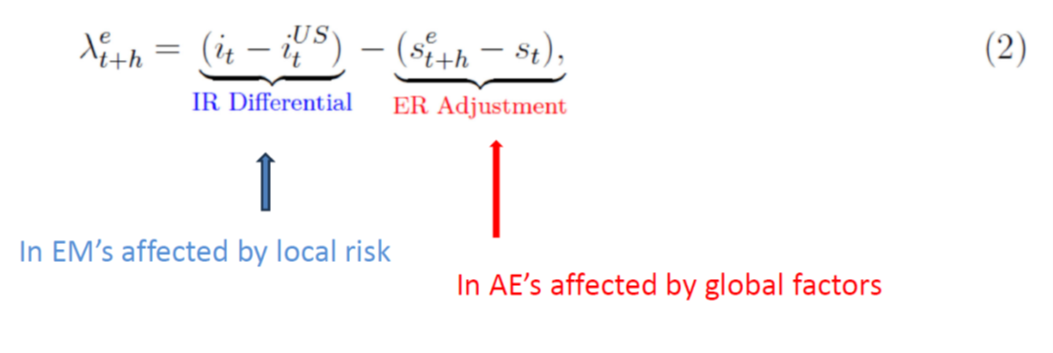

Where i is the local interest rate, iUS is the US interest rate, and s is the log exchange rate (in foreign currency unit per USD). An e superscript denotes a subjective expected value. If uncovered interest parity held, expected exchange rate changes would equal interest differentials

Using survey data — so dispensing with the rational expectations in equilibrium hypothesis which assumes expectations errors are pure innovations — the authors find for 22 EM’s, 18 AE’s, 1996-2018 (from Conssensus Economics):

- EM UIP premium > AE UIP Premium, σEM > σAM

- EM UIP premium driven by local factors

- EM Int diff more correlated with local factors

- Local & global factors affect exchange rate expectations, hence interest differentials

- Local factor predicted by country time-varying policy uncertainty

These findings are quite interesting. To sum up one of the main findings (of which there are many interesting ones in the paper):

The authors find this is the case wherein they develop Baker-Bloom-Davis types of policy uncertainty indices for countries other than the United States (as well as other risk factors).

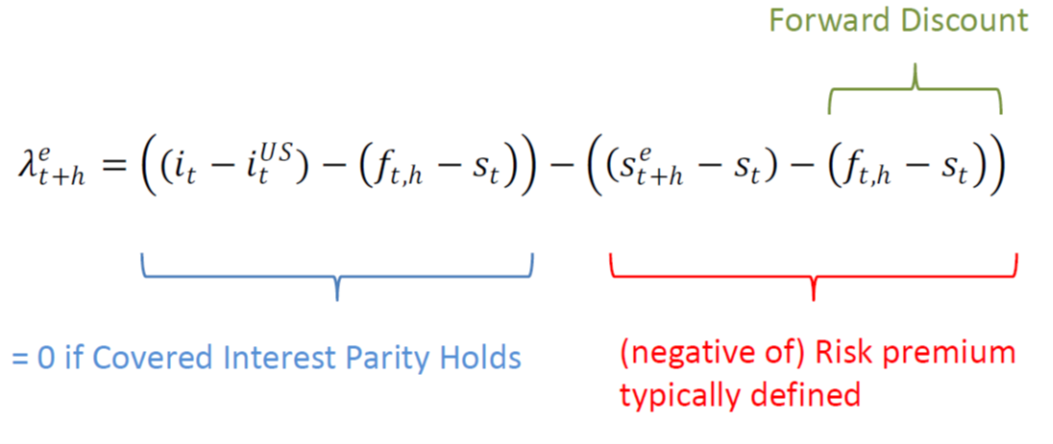

In other words, deviations from UIP can arise from the interest differential, or from the expected exchange rate change. Another, more common, decomposition is used by Chinn and Frankel (2000) as well as Chinn and Ito (2024):

Once one uses this decomposition, it makes clear that different markets would have different determinants of deviations from UIP.

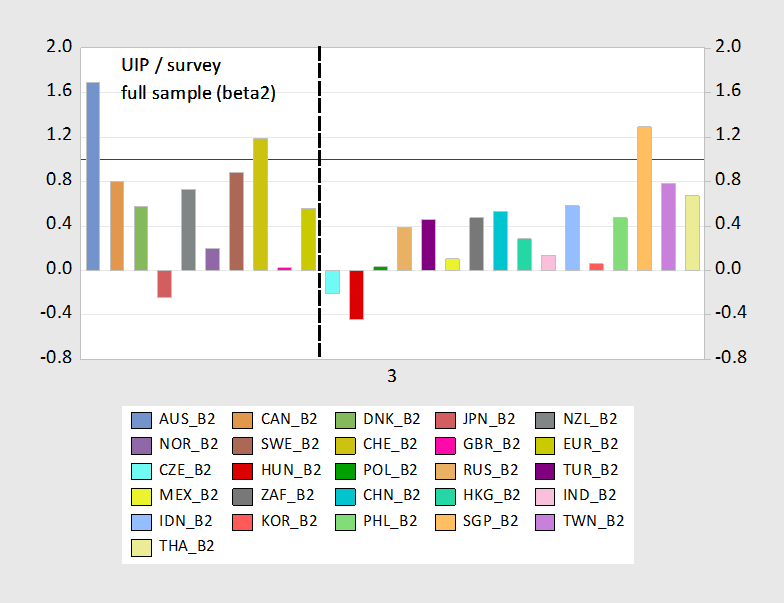

Typically, pre-2008, covered interest parity held for advanced economy currencies, so deviations from UIP had to come from exchange risk premia. Chinn and Frankel (2000), using FX4casts survey data, documented that for advanced economy currencies, UIP mostly held, so that the risk premium could not explain forward rate bias (i.e., as in the Fama regressions):

Figure 1: Regression coefficient of depreciation on forward discount. Source: Chinn and Frankel (2020).

In other words, the Kalemli-Ozcan & Varela findings were consistent with the Chinn-Frankel findings that for advanced economies, Fama regression results were primarily due to bias in survey data; while for emerging market currencies, it was much more likely to be due to risk premia.

I say consistent with, but not confirming. That’s because Chinn and Frankel did not use interest rates, so it could be that it’s a combination of exchange risk premia and covered interest differentials (due to political risk, differening default risk, or convenience yield) which explains the greater role for domestic factors in emerging markets.

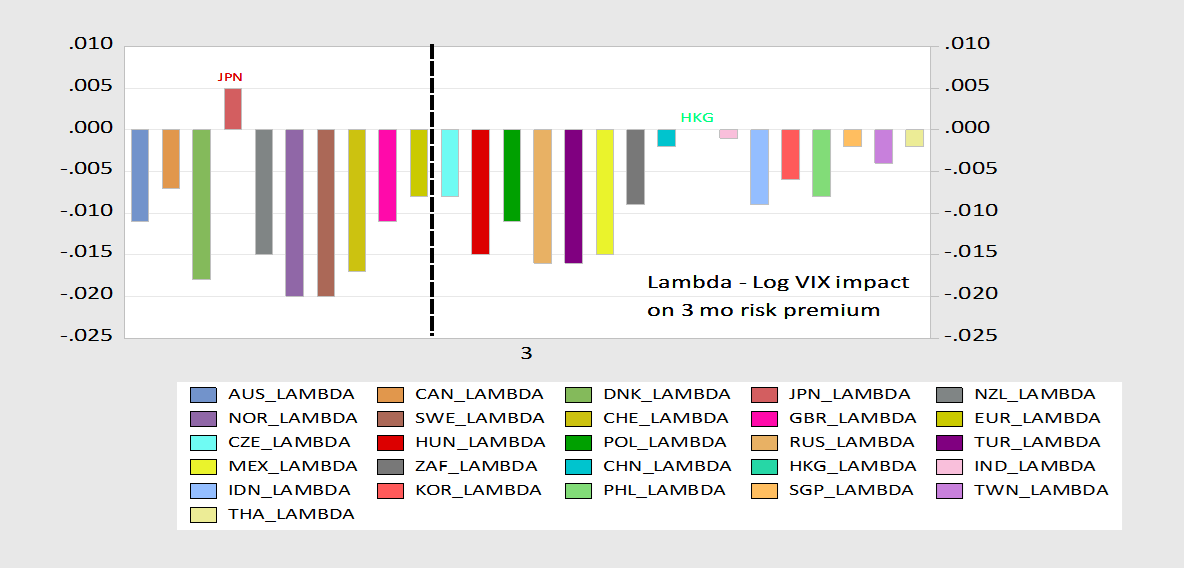

That being said, while Klaemli-Ozcan and Varela found a primary role for domestic factors on interest differentials in emerging markets, Chinn and Frankel did find a variable role for global factors (the VIX).

Figure 2: Regression coefficient of risk premium on log Vix. Source: Chinn and Frankel (2020).

The global factor has less impact for non-advanced currencies, but the impact is heterogenous. Pooling across currencies (as in Kalemli-Ozcan and Varela) might be appropriate, but these results suggest otherwise.

As of June 26, FX4casts indicate a 2.5% depreciation of the dollar against the euro over the next year (vs. forward discount of 1.7%) but 2.6% appreciation against the Korean won (-1.3% forward discount). On average, the dollar will appreciate against the euro, and depreciate against the Korean wonn under these conditions.