Jeffrey Frankel and Hélène Rey organized a great conference for the NBER’s International Seminar on Macroeconomics, hosted by the Sveriges Riksbank; topics covered were wide and diverse. The program is here:

Welcome address: Anna Seim, Deputy Governor, Sveriges Riksbank

Chair: Hélène Rey, London Business School and NBER

Discussants:

Michael McMahon, University of Oxford

Robert J. Richmond, New York University and NBER

Chair: Kenneth D. West, University of Wisconsin – Madison and NBER

Discussants:

Veronica De Falco, Imperial Business School

Stephen A. O’Connell, Swarthmore College

Chair: Ulf Söderström, Sveriges Riksbank

Discussants:

Kristin Forbes, Massachusetts Institute of Technology and NBER

Loriana Pelizzon, Goethe University Frankfurt

Discussants:

Ozge Akinci, Federal Reserve Bank of New York

Gianluca Benigno, University of Lausanne

Chair: Ricardo Reis, London School of Economics

Discussants:

Matthew Ferranti, Bitcoin Policy Institute

Fernando Broner, Center for Research on International Economics

Thursday, June 25

Chair: Jordi Gali, Center for Research in International Economics and NBER

Discussants:

Nuno Coimbra, Banque de France

Zhengyang Jiang, Northwestern University and NBER

10:30 am

Discussants:

Kenza Benhima, University of Lausanne

Menzie D. Chinn, University of Wisconsin – Madison and NBER

Chair: Jeffrey A. Frankel, Harvard University and NBER

Discussants:

Michael D. Bordo, Rutgers University and NBER

Catherine R. Schenk, University of Oxford

For me, this was a chance to catch up on a lot of open economy macro work that I’ve missed (focused as I have been on US macro policy debacles developments over the past year and half). I was a discussant for the UIP paper, on which I’ll do a separate post.

The hyperlinks to the papers allow you to read the abstracts for more details. I’ll just make a few remarks.

The first paper, presented by Anton Korineck, described how LLMs can condense IMF fiscal advice as represented in Article IV reports, and how the content has evolved over time. For those of us will little familiarity about how LLMs summarize text, this was extremely

informative.

The second paper, presented by Toni Iko, showed how exchange rate pass through into Nigerian CPI depended more on the parallel rate than the official. Anusha Chari discussed “Capital flows in risky times”, which demonstrates that passive fund behavior induces a feedback mechanism that amplifies exogenous shocks; at the same time, she and her coauthors develop a “risk-on/risk-off” index, which is now available on FRED. This is an impressive data compilation,using EPFR mutual fund data.

Gernot Muller’s coauthored paper (Dollar Trinity) delivers a model based on dollar dominance in safe assets, corss border asset trade, and trade invoicing, which explains the existence of a global business cycle, asset price cycle, and trade cycle. The discussion highlighted the fact that the dollar invoicing componnent was not central to the existence of the global business and asset price cycles, but did rationalize the trade cycle.

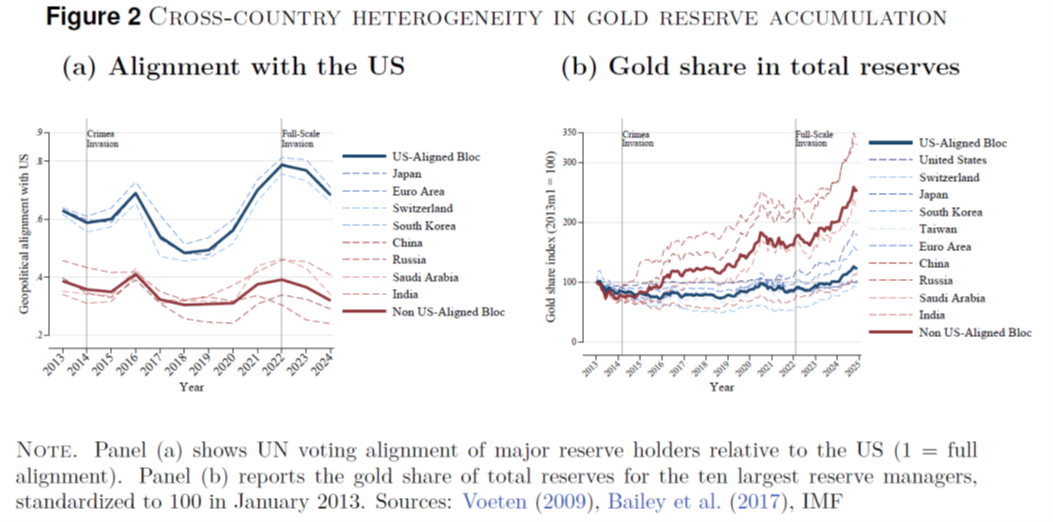

The last paper of the first day (Fool’s Gold), presented by Kai Arvai, modeled the rise of central bank gold demand as a function of greater geopolitical risk, and documented empirically the rise of such holdings. (For a slightly different perspective, see Chinn, Frankel and ito (2026), or this post).

The second day’s starting paper, “Loanly governments” documented a little known (to me!) fact that loans constitute a noticeable and persistent share of total borrowing by OECD governments. Using credit rating changes as shocks, Lucas Hack showed that loans increased as a share of total borrowing in the wake of such shocks.

Eric Monnet’s paper documented the creation of a new (Fed discount rate) measure over the period in which the (offshore) eurodollar market grew (before the breakdown of the Bretton Woods regime). Using this new measure, he and his coauthors showed that such shocks induced changes in foreign policy rates in the wake of convertability, but had on measurable impact on foreign output and prices. The discussant, Michael Bordo, commented on the fact that the discount rate is an insufficient measure of Fed policy during this period, while Catherine Schenk observed that in reality, what we typically refer to the Bretton Woods era, in some senses ended much earlier (1947, if not earlier).

All the papers were really illuminating, in terms of empirical findings, or even in describing phenomena that were not well-known. Since all papers are linked (unfortunately not the discussion slides), there’s no excuse to skip any of them. More on Sebnem Kalemli-Ozcan’s paper and my discussio next post.