Today the Federal Reserve announced a further 50-basis-point cut in its target for the fed funds interest rate, bringing it down to 3.0% for a total reduction in January of 125 basis points. How long should it take before this has an effect on the economy?

In a recent research paper (quick summaries here and here) I sought to develop new measures of the time delays between when the Fed acts and when the effects are felt on the economy. I produced evidence that policy changes begin to affect the economy as soon as they are anticipated by markets, usually well in advance of when the Fed actually announces that its target has changed. If nothing else, the excitement this last month gives us some wonderful new evidence to illustrate this.

In December, the Fed’s target interest rate still stood at 4.25%. The graph below plots the expected average value for the fed funds rate for February or March as implied by the closing values of the February or March fed funds futures contract as of each day over the last month. At the start of January, traders were anticipating that we’d see a 25-basis-point cut by the end of the month, or an expected funds rate of 4%. There was a gradual process over the month of revising these expectations down as the month progressed. By January 13, the betting was starting to anticipate a 75-basis-point cut, and by January 22, the market was anticipating close to 3% by month’s end, as was indeed announced today.

|

My research paper presented evidence that a move like this would begin to affect mortgage rates as soon as it becomes anticipated by markets. The graph below replicates the calculations from Figure 7 of my paper (which looked at the summer of 2006) for the new numbers for January 2008. The green line indicates how the 30-year mortgage rate would have been expected to move along with changing anticipations of the February and March fed funds rates based on the parameter values that I estimated in that paper using 1988-2006 data. The blue line records the actual change. My model would have predicted a cumulative decline in mortgage rates of 66 basis points during the month of January, virtually identical to what we observed.

|

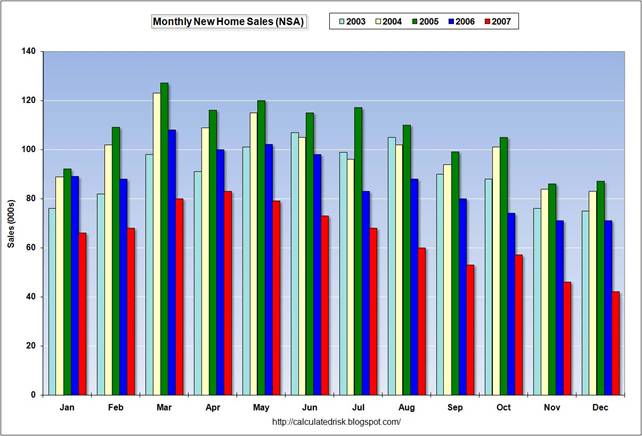

My research paper went on to demonstrate that although interest rates respond immediately to the anticipation of any change from the Fed, it takes a considerable amount of time for this to show up in something like new home sales, due to the substantial time lags involved for most people’s home-purchasing decisions. The graph below gives my estimate of the average time delay between a change in the mortgage rate and a subsequent change in the number of new home sales. According to the historical correlations, we would expect the biggest effects of the January interest rate cuts to show up in home sales this April.

But of course, this is just focusing on one determinant of home sales (the interest rate), and there are a number of other factors that have been playing a bigger role over the last year. Tightening lending standards rather than the interest rate have in my opinion been the biggest explanation for why home sales continued to deteriorate after January 2007 and for the acceleration of that trend following the credit problems in August.

|

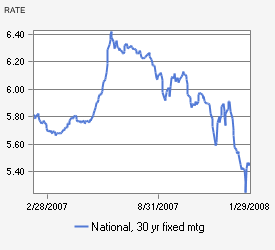

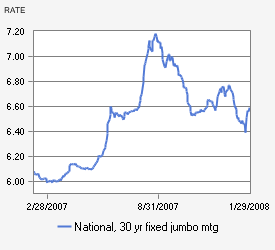

One indicator of the role of the credit crunch in the housing market is the fact that, although we have seen the interest rate on conventional 30-year mortgages decline dramatically over the last six months, the rate on jumbo loans (those too big to qualify for securitization by Fannie or Freddie) remains well above where it stood a year ago.

|

|

The effect of rising unemployment and expectations of falling house prices on housing demand is another big and potentially very important unknown.

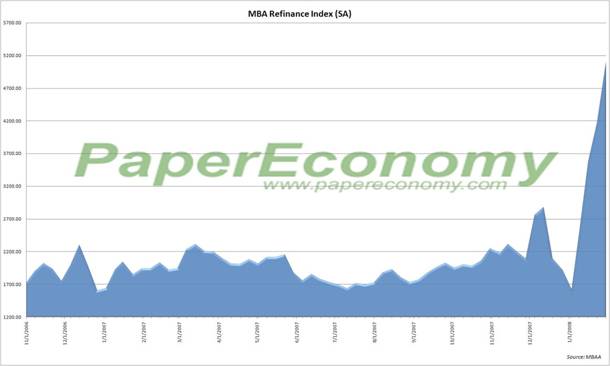

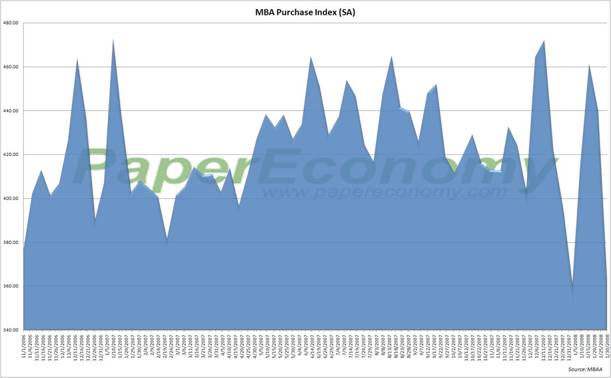

Still, it is hard to imagine that the latest actions by the Fed would fail to have a stimulatory effect. We’ve already seen a big surge in mortgage applications, though this is much more in evidence for the Mortgage Bankers Association index of refinancing applications

|

than in their Purchase Index:

|

My bottom line: the Fed’s moves this month have to help relative to where we would have been without them, but it will take some time to see by how much. If indeed a recession began in December (and I repeat that no one knows for sure whether or not it did), things are going to get worse before they get better.

Technorati Tags: macroeconomics,

economics,

Federal Reserve,

housing,

interest rates,

fed funds rate,

fed funds futures,

Bernanke,

recession

If the Fed basically does what the market expects, and the market’s expectations immediately affect e.g. mortgage rates *before* the Fed takes action, couldn’t one simplify the causality by omitting the Fed altogether?

James – “Today the Federal Reserve announced a further 50-basis-point cut in its target for the fed funds interest rate, bringing it down to 3.0% for a total reduction in January of 125 basis points. How long should it take before this has an effect on the economy?“

Late April – early May.

You asked…

>>

James, you are right. No one knows for sure if a recession began in December 2007. A fortiori no one knows if there will be a recession in 2008 or 2009. The Fed doesn’t forecast a recession for 2007 or 2008. Only a slowdown. But they engage in a, by historical standards, dramatic reduction in the federal funds rate. And Bernanke even welcomes addional fiscal policy measures (if they fullfill some standards). That looks like an overkill for a slowdown or they know something (perhaps about the U.S. and international financial system) which they cannot make public, because it will make things worse.

Mortgage rates are up a bit since the emergency Fed cut. So, conceivably at least, the Fed cuts have hurt the home builders, not helped them.

Granted, the rise in rates is a quarter of a point, but still the direction is not good.

James, what do you think about Julian Robertson’s “curve steepner” trade? If he’s correct, a “reverse conundrum” is now in play.

Groucho, I agree with Robertson that it’s risky to buy long-term Treasuries at the moment, and I’d bet on the yield curve steepening. That’s essentially what I was saying here.

Professor, I see from Table 4 of your paper that you attempted to improve your regression by using various spreads, but I can’t help wondering if the 10-year Treasury note yield (alone) is a better indicator of mortgage rates than the Fed Funds rate (alone).

If this were to be the case, then the effect of Fed Funds rate target changes on the level of housing sales would simply be indirect and therefore limited by a version of Greenspan’s Conundrum … there will be a level of FFR below which changes in the FFR will have no effect – or a negative effect – on the ten-year note yield, hence on mortgage rates, hence on housing sales, due to inflation concerns.

Of course, real assets could be perceived as being more attractive in an inflationary environment, so sales could be boosted due to hedging against the inflation predicted from the low FFR. Different mechanisms is what makes this stuff fun anyway, right?

James I. Hymas hit on an interesting point: inflationary times make it pay to hold real assets.

Is the key to overcoming the housing crisis a bout of stagflation?

I remember people making a lot of money in real estate in the 1970s in California and New York City.

I don’t want to sound alarmist or rumor mongering, but I heard “through the grapevine” that the FED believes consumption will fall to “0” the first half of 2008. Hence the reason why they and the Gmen are trying to “revive” it it the 2nd half(when the afamed “stimulus” actually will take effect).

Take it with a grain of salt.

How long should it take? It depends. Do people believe the FED will cut again? Would you borrow today at 3% if tomorrow or next week you think you could get 2.5%? Trying to put the reaction of people to interest rates in a box is like trying to make them eat hamburgers every day. People are not machines that replicate over and over. People make choices and those choices are determined by a whole lot of things.

Bernanke has been his own worst enemy by cutting then saying soon he would cut again. No one will begin to invest again until the economy finally reaches some kind of reasonable equilibrium. Bernanke has had the monetary situation in chaos since he sat in the chair. I think that his main problem is that he is an economist when what we need it a rational perceptive human being making decisions.

January 31, 2008

Econbrowser’s James Hamilton noted the Fed 50bp rate cut and pondered how long it will take for the easing to reach Main Street:

My bottom line: the Fed’s moves this month have to help relative to where we would have been without them, but …

I really don’t understand how fed cuts hasc effected mortgage rates. What is the relationsip between fed cut and recession or inflation? Please explain.