Suckers are born every minute.

Temporary shocks have temporary effects in the financial markets.

Rest assured the sellers (like Goldman Sachs) on the other side of those derivative trades will make a killing when the price falls back to it’s pre-hype level.

Same with stocks. If stocks fall tank over a debt limit stalemate, then buy the dip.

jonathan

I don’t know if that’s accurately a “perception” as a sign that the bet is not worth taking. Maybe the distinction is subtle and maybe this is what you meant, but not wanting to take a bet can mean, like in Vegas, that the cost of paying off would be too big. Houses have rules about what they’ll take as bets for that reason. It isn’t as much that there’s a bigger risk but that the cost of payout is potentially too big. In this case, you don’t know what your business will look like after a default and you can’t trust you’ll get paid if you lay off the risk so the bet becomes too big for the house to take. That doesn’t mean the risk is as high as it looks, but that the cost of payout is dominating the information.

tj: Yes, Argentina clearly pays no premium for having defaulted on its sovereign debt in the past. Just one of those temporary things.(!!!!)

tj

Menzie Yes, Argentina clearly pays no premium for having defaulted on its sovereign debt in the past.

Excuse me, I thought we were talking about the U.S. since you posted a chart of insuring against U.S. default, not an Argentinian default.

You really are revealing your ignorance on this topic if you are trying to link the current debt ceiling debate to a default by Argentina.

Here’s a little history for you –

(This is for the U.S. not Argentina.) Warning – the details of the catastrophic market meltdowns following past U.S. government shutdowns may be to graphic for some readers.

Shutdowns of more than 10 days:

— 1976 Shutdown:

From Sept 30 to Oct. 11 under President Ford. S&P 500 goes from 105.24 to 101.64.

— 1977 Shutdown:

From Sept. 30 to Oct. 13 under Carter. S&P 500 starts at 96.53 and ends at 93.46.

(Read more: Blackstone: We’re in an ‘epic credit bubble’)

— 1978 Shutdown:

From Sept. 30 to Oct. 18 under Carter. S&P starts at 102.54 and ends at 100.49.

— 1979 Shutdown:

From Sept. 30 to Oct. 12 under Carter. S&P goes from 108.56 to 104.49.

— 1995-1996 Shutdown:

From Nov. 14 to Nov. 19, 1995, under Clinton, the S&P goes from 592.30 to 600.07. And from Dec. 15 to Jan. 6, 1996, the S&P goes from 616.92 to 616.71.

—By The Associated Press. http://www.cnbc.com/id/101069585

Justafed

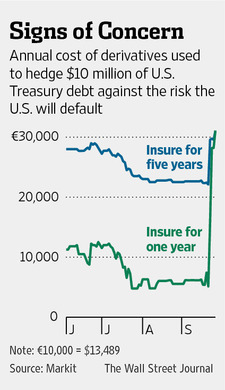

So what event triggers this insurance? Any defaulted payment or something more specific? I am assuming the payoff is $10M, otherwise the price makes no sense at all. This also appears to be thinly traded since it looks like the 5 year price is the same as one year, which also makes no sense.

tj: Are you intentionally being dense? The CDS spreads are for default “events”, not government closure. (Please see title of post, if in doubt.) If the government closes due to failure to pass a CR, payment on debt principal and interest continues…until exhaustion of funds – October 17 according to latest estimates.

With regard to US vs. Argentina — well, with that perceptive statement, we should burn all papers using cross-section/panel regression. I’m confident you’d be happy with a good book burning.

2slugbaits

I think Rick Stryker and tj have been starting their weekend football parties a little early. They both sound half-sauced and it’s only Saturday morning. I recognize that trying to argue with a drunk is hopeless, but on the oft chance that someone near and dear to him will intervene with some strong coffee, here goes.

First, Menzie was referring to default on debt payments, not a government closure due to CR roadblocks. Those are completely different issues.

Second, the failure to pass a CR has gradual and rolling effects. Going a few days without a CR will inconvenience people, but for most Americans things won’t change. It is a big hassle for government workers, but not for most people. In my case I will have any planned leave cancelled and ironically will have to report to work (I’m in the “exempt” status), but I won’t be paid for my time at work. (Incidentally, even though I had originally planned on taking personal leave a couple of those days, that leave has been cancelled and I must show up to work without pay or risk a felony conviction.) If we go a couple weeks without a CR, then things will start to affect the economy. Government workers and the military can only keep showing up a work so long without being paid before that starts to affect the larger economy.

Finally, US Treasuries are the universal benchmark for risk free assets. If the risk characteristics of those assets change due to default, then it is impossible to know the value of a portfolio. This would be orders of magnitude worse than Sep 2008 because Treasuries are ubiquitous in a way that mortgage backed securities never were.

valuethinker

Justafed

The contracts specify ‘event of default’. AFAIK that is declared by a credit rating agency (one of the big 3 at least) and usually follows an overdue payment of interest on a debt.

The payoff is $10m for the standard CDS contract, yes.

The 2 prices would converge if, for example, the market was very worried in the short term about a default (moves the 1 year CDS up) but less worried (or no more worried) in the long term (5 year). In other words, it is that the 1 year has moved, rather than what has happened to the 5 year.

Some speculators will be hoping for a default in the next year and seeking to profit from that.

Conversely someone wants a hedge on US government default and so bought the cheaper contract (although it is no longer cheaper).

dsj

This in fact strikes me as a sucker’s deal…. in the event of a true default can any of the insurance issuers actually make good on the hedge? Counter-party risk on any insurance against a US default is meaningless in the worst case scenario.

Steven Kopits

Being a born Argentine with parents who grew up there, let me assure you, the US is not Argentina–although it is certainly trying to be. Argentina, since at least the time of Peron, has tended to have terrible macro policies including high and hyper-inflation, and over-borrowing leading to external default. It has been in default since 2001 and continues to be in default today. http://www.nytimes.com/2013/08/30/business/fears-of-a-precedent-in-argentine-debt-ruling.html?pagewanted=all&_r=0

Argentina’s defaults were most certainly not caused by legislators being unwilling to borrow more money. Rather, they were caused by investors unwilling to lend more. They were caused by over-borrowing.

I am surprised that as a macro economist you would be unaware of the issues there. I might recommend Paul Blustein’s excellent book about the 2001 Argentine crisis, entitled, “And the Money Kept Rolling In (and Out): Wall Street, the IMF, and the Bankrupting of Argentina”.

Steven Kopits: Read Blustein’s book; excellent, it’s on my recommended reading list for students writing papers on emerging market crises.

The reason why investors were unwilling to roll over Argentine debt was because they saw Argentina was unwilling/unable to raise taxes/cut spending and maintain growth in order to service the debt. Here, in this case, we are unwilling to raise the debt ceiling in order to service the debt. Sure, there are differences. But do you expect there not to be a premium on US debt just because the run-up to debt default was different?

aaron

I think the key there is “unwilling to cut spending”. That was the driver if concern before our credit rating was dropped. The cash flow uncertainty from the debt ceiling debate was just a straw on the camel’s back.

Rick Stryker

Justafed’s question suggested to me that there might be a lot of readers who don’t know how to interpret the WSJ chart. For those who are interested, here is some background.

The first thing to notice is the WSJ box is wrong. CDS on US Treasuries are denominated in euros. In the WSJ box, the annual premium is stated in euros as it should be. But the notional value of the contract is stated in dollars in the WSJ box. That should be $10 million euros.

The price of 30K euros per year to insure 10 million euros means that the spread is 0.003 or 0.3% per year or 30 basis points (bps). If you buy protection you will pay 30 bps on a 10 million euro notional per year. For 1-year protection you pay for 1 year; for 5-year protection you pay annually for 5 years. But if there is a default, you will not be paid 10 million euros, but rather the post-recovery value of the 10 million euro notional. For example, if the bond recovery is 40%, you will be paid 60% of 10 million euros, or 6 million euros.

Events that can trigger a sovereign CDS depend on the contract but will typically include failure to pay, a repudiation of the debt or moratorium, and restructuring of the debt.

How do you interpret how big 30 bps is? One way to do it is to compare it to other sovereign CDS spreads. Markit has a convenient page that contains daily reports of CDS spreads over the last year. If you open the September 26 report and go to the table labeled “G7 Industrialised Countries CDS” you can see that the 5-year USD CDS spread is 31 bps, similar to Britain at 33 bps. However, Japan is at 61 bps currently. You can look at different reports on different days to see how the USD spread has changed over time. For example, on Jan 2 of this year, the USD CDS spread was 35 bps.

To understand what CDS spreads mean in terms of default risk, a useful approximation for the risk neutral probability of default is

PD(t) = 1 – exp(-s*t/(1-R))

where PD(t) = the cumulative probability of default over the time interval from now to t, s is the annual spread, t is the time horizon, and R is the recovery rate (default of 40%). exp() is the exponential function.

As an example, if the spread is 50 bps, then the risk neutral probability of default at 1 and 5 years is

PD(1) = 1 – exp(-.005*1/.6) = .0083 or 83 bps

PD(5) = 1 – exp(-.005*5/.6) = .04 = 400 bps, which is about 80 bps per year for 5 years.

These are the risk neutral default probabilities. We want however the real world default probabilities. Because we pulled these default probabilities from the spreads, they contain a risk premium to compensate for bearing risk. Risk neutral default probabilities, because they contain risk premia, are greater than real world default probabilities.

It’s difficult to estimate risk premia but just as an approximation you could cut in half the risk neutral default probabilities to estimate the real world default probabilities. So that means the real world 1-year default probability would be (1/2)83 bps or 41.5 bps in the example. And the 5-year default probability would be (1/2) 400 bps or 200 bps in the example

These calculations are just estimates of course. Hope this helps.

tj

Menzie

You are even more ignorant on this issue that I thought. 2slugs correctly explains that the government will not default on it’s interest payments. They will shuffle cashflows internally to avoid missing a principal or interest payment. Of course, it’s always possible Obama throws a tantrum and chooses to miss a payment.

It’s time to grow up Menzie, drop your Progressive bias and present all the relevant facts, like JDH does. He doesn’t get nearly as much blow-back as you do because he presents a much more balanced view of the issues.

2slugbaits

Rick Stryker I think you might be missing the larger point of the WSJ graph. The larger point is that up until very recently the spread between the 1-year and 5-year reflected risks that were uniformly distributed. In other words, the instantaneous hazard rate on day 360 was the same as the instantaneous hazard rate on day 1800. The chart is telling us that the instantaneous risks are no longer uniformly distributed; all of the risk is front loaded towards the next month.

tj: How do you know the government won’t miss an interest payment? I think I missed the presidential statement that the US government will prioritize debt payments (i.e., implement technical default).

So, exactly what was the point of you citing government closures in response to a post on CDS on debt defaults? That makes no sense, regardless. I wait explication. Until then, my thanks — that comment was good for more than a couple chuckles. I plan to share in my lecture tomorrow, in fact.

Finally, “blowback”? It’s only blowback if there is any intellectual content to the criticism. If the criticism is devoid of facts and/or intellect, then it is merely noise and fury.

2slugbaits

tj Huh? How did you interpret my comments as saying that the US would not default on interest payments if the debt ceiling is not increased??? I was saying that there is a difference between what happens under failing to pass a CR and what happens under failing to increase the debt ceiling. Over the short-run very little happens if a CR is not approved. Things get worse as time goes on, but many Americans will not notice the effects…again, at least in the short-run. Hitting the debt ceiling is a completely different matter. Daily Treasury disbursements will be limited to daily Treasury receipts. It is unclear how Treasury will prioritize claimants. Will it be first-come-first-served? Will SS retirees get a prior claim? Will bondholders get a prior claim? Will everyone just take an across-the-board haircut? No one knows. I don’t even think Jack Lew knows. Also, failing to increase the debt ceiling will furlough even those who are exempt under the CR furlough. So we’re not just talking about shutting down parks and museums.

Rick Stryker

2slugbaits,

Rather than commenting on this topic, I was just trying to give people some background and tools to come to their own conclusions.

Unfortunately, you have everything exactly backwards, which is easy to do really. However, this is a good opportunity to provide some further examples of how to use the equations.

First, it’s wrong to say that risks are uniformly distributed if the 1-year rate is lower than the 5-year rate. Using the example I gave, suppose the 5-year spread is 50 bps but the 1 year spread is 10 bps. Then, the risk neutral probability of default over 1 year is

PD(1) = 1 – exp(-.001*1/.6) = .00166 or 17 bps

and over 5 years it is

PD(5) = 1 – exp(-.005*5/.6) = .04 = 400 bps.

Conditional on no default over the first year, the probability of default over the remaining 4 years is 400 – 17 = 383 bps, which is distributed over the remaining 4 years. The risks are not uniformly distributed. Lower default probability in the first year is compensated by higher default risk in the remaining 4 years.

However, if the 1-year spread rises to be equal to the 5-year spread of 50 bps, then the risks are now uniform, since

PD(1) = 1 – exp(-.005*1/.6) = .0083 or 83 bps

PD(5) = 1 – exp(-.005*5/.6) = .04 = 400 bps,

so that default risk is about 80 bps per year for each of the 5 years.

It should be also clear that if the 1-year rate moves up to the 5 year rate, that doesn’t mean that all risk is “front-loaded towards the next month.” In this example, the risk neutral default risk is 83 bps in the first year, about 1/5 of the 5-year cumulative default probability.

It’s also incorrect to say that the hazard rates are the same when the 1-year spread is lower than the 5-year rate. Just the opposite again. In these equations, we are approximating the hazard rate to be

hazard rate = s/(1-R)

where s is the CDS spread and R is the recovery rate on the bond.

The hazard rate is directly proportional to the level of the spread, approximately. A lower 1-year spread means the hazard rate is lower. When the 1-year spread rises to equal the 5-year spread, the hazard rates are uniform across time.

Keep in mind that all the default rates in these calculations are risk neutral–they are not the true default rates.

Rick Stryker

Menzie,

What class are you teaching? Do you keep a tally of how often you have used specific commenters to illustrate fallacies (AKA conservative viewpoints) to the students? I hope I’ve won the gold.

Rick Stryker: Sad to say, I don’t think I’ve used one of your comments. Timing has to match up with what is going on and what I’m teaching (macro topics this semester). I might’ve mentioned in passing your defense of Romney’s “500,000 jobs per month is typical in a recovery” statement.

tj

Menzie

The point is that these are temporary shocks. I used the historical evidence available on the relationship between government shutdowns and stock returns to demonstrate that point.

You shriek like a scared child about the relatively minor economic impact of a failure to raise the debt ceiling or a failure to pass a CR in a timely fashion.

Your bias runs so deep you can’t even comprehend simple relationships or apply a little creativity to arguments that conflict with your Progressive babblings.

I feel sorry for your students, if you are as biased in the classroom as your are on this blog. The views of Professors can be very influential and I imagine you make no attempt to remove your political bias in the classroom. If so, you should be ashamed.

endorendil

DSJ’s question still seems relevant to me. There is an implicit assumption in these CDS that in case of a default, the damage is really very limited and the insurers can still pay out. Is this really just a financial instrument that is created to put pressure on Washington? Does the trading volume show anything that makes it look like it is a real instrument in stead?

Steven Kopits

Menzie – If you equate policies and governance in Argentina with those of the US, then we are truly doomed. But it seems to me rather than you cannot distinguish between the drunkard at the party and the host taking away the punch bowl.

Having said that, I am not sure what the Republicans are up to here. Are we voting against the debt ceiling just for the hell of it? Or is delaying Obamacare by a year a huge victory–is it worth the spilled blood? I don’t understand the narrative. Where do we want to go?

There is a case to be made. If we allow that growth will be only 1.5-2.0% per year in the future, then clearly a 3% deficit is not sustainable. Given that we’re looking at a 4.5% gap this year, there’s a case for a gradual tightening to 2% or below. And a debt ceiling policy which puts the country on a predictable glide path would be a supportable policy, in my opinion. But I haven’t really heard that.

And there’s cause to get debt under control.

Personally, I am for an incentive plan which I might call the Fiscal Accountability Act, tying incentive pay of politicians to sustainable growth. (I have written on this before.) Such a law would be worth a shutdown, but otherwise, I don’t see where we’re headed at the moment.

Steven Kopits: I don’t have to equate two countries to say the same phenomenon will have a similar impact. Consider rent control. I will bet binding rent ceilings will induce excess demand, be it in Argentina, or the U.S. Analogously, debt default in Argentina and debt default in the U.S. will have some impact on perceptions of likely repeat default. I suspect the impact is smaller in the U.S., given Argentina’s reputation as a serial defaulter. But who’s to say — perhaps exactly because Argentina is almost expected to default, the impact on the U.S. spreads is larger.

The point is not that any two countries indexed by i in a sample are the same. The idea is that after controlling for other factors, a given variable behaves the same in response to different exogenous variables. It might be the responses differ quantitatively (that’s where econometrics, as opposed to hand waving, is helpful), but the qualitative effect should be the same.

tj: So you believe a debt default would have a minor impact? I think that speaks volumes. I didn’t coin the term, but I think it useful — I’ll place you in the “debt default deniers” category.

My students complain about my lectures incorporating too much math, or being too boring, or hewing too close to the textbook, or diverging too far from the textbook, or having too hard problem sets, or too few problem sets, or the like. They don’t complain about politics. I’m sure you could file a freedom of information act request to get the evals, if you don’t believe me. (I know the handouts and notes would be gibberish to you, given the level of math capability you have demonstrated in your comments, but for your edification, here they are.)

Steven Kopits

It would be entirely possible to tighten the debt ceiling such that it would limit spending by an attainable amount, say $100 bn. That by no means implies default on US debt, but it does involve the need to reduce spending in a measured fashion as the price of approval for any ceiling increase.

But doing so would involve analysis, advance notice, communication, and consensus building, among others (on the right, at least). Republicans haven’t done that.

That’s why a Fiscal Accountability Act is so much more preferable: 0.25% * (change in GDP minus change in government debt) / 537 members of House, Senate, Pres and VP. Democrats can then spend whatever they want, but each percent of deficit will cost them $500k apiece. Then we’ll see how important the deficit really is.

tj

Menzie So you believe a debt default would have a minor impact? I think that speaks volumes. I didn’t coin the term, but I think it useful — I’ll place you in the “debt default deniers” category.

The rational folks don’t expect Obama to choose default. Not that he cares about the consequences, but a default on his record might ruin his legacy.

On the other hand, he has appeared a bit unhinged lately. Perhaps it’s the long run effects from his days as a drug user with his choom gang friends.

From Dreams of My Father, Obama admits to cocaine use and that he tried drugs- “Pot had helped, and booze; maybe a little blow when you could afford it.”…“I kept playing basketball, attended classes sparingly, drank beer heavily, and tried drugs enthusiastically. …

Come to think about it, your chicken little act regarding the likelihood of a U.S. debt default borders on lunacy as well.

Anonymous

Our debt paths are simply unsustainable. We say dumb things like “3%” deficits per year, but even those are unsustainable because if we have a recession 3% suddenly is 10%, and in the good times we are never below 3%. All this is built on an assumption of GDP growth averaging 3% which is laughable in the new global economy, painful demographics, and restrictive regulations. Republicans are a garbage party and I truly despise most of them, but Democrats are either dumb or just don’t care this we can not continue on this path for much longer. We are due for and probably will have another recession in the next 4-5 years, what does that do to our budgets?

Anonymous

Also, Menzie I appreciate your relatively free speech policy, even when criticism is directed at you. That shows good character, even if you are a communist.

tj is baffling

tj,

your comment:

You shriek like a scared child about the relatively minor economic impact of a failure to raise the debt ceiling or a failure to pass a CR in a timely fashion.

that had me rolling! you deserve all the tea baggers will bring your way. obviously you have no experience in the world of business or finance. in addition, as a partisan hack your comments are simply stupid!

failing to pay the debt is an explosive situation. now you see BOTH democracts and republicans coming out and saying so. as a debt limit denier (i like that) you are truly baffling.

if a clean bill appears in Congress to address the CR, and another appears to address the credit limit, i guarantee you both will pass in a bipartisan fashion. why are these clean bills not presented? why are they only presented tainted with partisanship?

Suckers are born every minute.

Temporary shocks have temporary effects in the financial markets.

Rest assured the sellers (like Goldman Sachs) on the other side of those derivative trades will make a killing when the price falls back to it’s pre-hype level.

Same with stocks. If stocks fall tank over a debt limit stalemate, then buy the dip.

I don’t know if that’s accurately a “perception” as a sign that the bet is not worth taking. Maybe the distinction is subtle and maybe this is what you meant, but not wanting to take a bet can mean, like in Vegas, that the cost of paying off would be too big. Houses have rules about what they’ll take as bets for that reason. It isn’t as much that there’s a bigger risk but that the cost of payout is potentially too big. In this case, you don’t know what your business will look like after a default and you can’t trust you’ll get paid if you lay off the risk so the bet becomes too big for the house to take. That doesn’t mean the risk is as high as it looks, but that the cost of payout is dominating the information.

tj: Yes, Argentina clearly pays no premium for having defaulted on its sovereign debt in the past. Just one of those temporary things.(!!!!)

Menzie

Yes, Argentina clearly pays no premium for having defaulted on its sovereign debt in the past.

Excuse me, I thought we were talking about the U.S. since you posted a chart of insuring against U.S. default, not an Argentinian default.

You really are revealing your ignorance on this topic if you are trying to link the current debt ceiling debate to a default by Argentina.

Here’s a little history for you –

(This is for the U.S. not Argentina.)

Warning – the details of the catastrophic market meltdowns following past U.S. government shutdowns may be to graphic for some readers.

Shutdowns of more than 10 days:

— 1976 Shutdown:

From Sept 30 to Oct. 11 under President Ford. S&P 500 goes from 105.24 to 101.64.

— 1977 Shutdown:

From Sept. 30 to Oct. 13 under Carter. S&P 500 starts at 96.53 and ends at 93.46.

(Read more: Blackstone: We’re in an ‘epic credit bubble’)

— 1978 Shutdown:

From Sept. 30 to Oct. 18 under Carter. S&P starts at 102.54 and ends at 100.49.

— 1979 Shutdown:

From Sept. 30 to Oct. 12 under Carter. S&P goes from 108.56 to 104.49.

— 1995-1996 Shutdown:

From Nov. 14 to Nov. 19, 1995, under Clinton, the S&P goes from 592.30 to 600.07. And from Dec. 15 to Jan. 6, 1996, the S&P goes from 616.92 to 616.71.

—By The Associated Press.

http://www.cnbc.com/id/101069585

So what event triggers this insurance? Any defaulted payment or something more specific? I am assuming the payoff is $10M, otherwise the price makes no sense at all. This also appears to be thinly traded since it looks like the 5 year price is the same as one year, which also makes no sense.

tj: Are you intentionally being dense? The CDS spreads are for default “events”, not government closure. (Please see title of post, if in doubt.) If the government closes due to failure to pass a CR, payment on debt principal and interest continues…until exhaustion of funds – October 17 according to latest estimates.

With regard to US vs. Argentina — well, with that perceptive statement, we should burn all papers using cross-section/panel regression. I’m confident you’d be happy with a good book burning.

I think Rick Stryker and tj have been starting their weekend football parties a little early. They both sound half-sauced and it’s only Saturday morning. I recognize that trying to argue with a drunk is hopeless, but on the oft chance that someone near and dear to him will intervene with some strong coffee, here goes.

First, Menzie was referring to default on debt payments, not a government closure due to CR roadblocks. Those are completely different issues.

Second, the failure to pass a CR has gradual and rolling effects. Going a few days without a CR will inconvenience people, but for most Americans things won’t change. It is a big hassle for government workers, but not for most people. In my case I will have any planned leave cancelled and ironically will have to report to work (I’m in the “exempt” status), but I won’t be paid for my time at work. (Incidentally, even though I had originally planned on taking personal leave a couple of those days, that leave has been cancelled and I must show up to work without pay or risk a felony conviction.) If we go a couple weeks without a CR, then things will start to affect the economy. Government workers and the military can only keep showing up a work so long without being paid before that starts to affect the larger economy.

Finally, US Treasuries are the universal benchmark for risk free assets. If the risk characteristics of those assets change due to default, then it is impossible to know the value of a portfolio. This would be orders of magnitude worse than Sep 2008 because Treasuries are ubiquitous in a way that mortgage backed securities never were.

Justafed

The contracts specify ‘event of default’. AFAIK that is declared by a credit rating agency (one of the big 3 at least) and usually follows an overdue payment of interest on a debt.

The payoff is $10m for the standard CDS contract, yes.

The 2 prices would converge if, for example, the market was very worried in the short term about a default (moves the 1 year CDS up) but less worried (or no more worried) in the long term (5 year). In other words, it is that the 1 year has moved, rather than what has happened to the 5 year.

Some speculators will be hoping for a default in the next year and seeking to profit from that.

Conversely someone wants a hedge on US government default and so bought the cheaper contract (although it is no longer cheaper).

This in fact strikes me as a sucker’s deal…. in the event of a true default can any of the insurance issuers actually make good on the hedge? Counter-party risk on any insurance against a US default is meaningless in the worst case scenario.

Being a born Argentine with parents who grew up there, let me assure you, the US is not Argentina–although it is certainly trying to be. Argentina, since at least the time of Peron, has tended to have terrible macro policies including high and hyper-inflation, and over-borrowing leading to external default. It has been in default since 2001 and continues to be in default today. http://www.nytimes.com/2013/08/30/business/fears-of-a-precedent-in-argentine-debt-ruling.html?pagewanted=all&_r=0

Argentina’s defaults were most certainly not caused by legislators being unwilling to borrow more money. Rather, they were caused by investors unwilling to lend more. They were caused by over-borrowing.

I am surprised that as a macro economist you would be unaware of the issues there. I might recommend Paul Blustein’s excellent book about the 2001 Argentine crisis, entitled, “And the Money Kept Rolling In (and Out): Wall Street, the IMF, and the Bankrupting of Argentina”.

Steven Kopits: Read Blustein’s book; excellent, it’s on my recommended reading list for students writing papers on emerging market crises.

The reason why investors were unwilling to roll over Argentine debt was because they saw Argentina was unwilling/unable to raise taxes/cut spending and maintain growth in order to service the debt. Here, in this case, we are unwilling to raise the debt ceiling in order to service the debt. Sure, there are differences. But do you expect there not to be a premium on US debt just because the run-up to debt default was different?

I think the key there is “unwilling to cut spending”. That was the driver if concern before our credit rating was dropped. The cash flow uncertainty from the debt ceiling debate was just a straw on the camel’s back.

Justafed’s question suggested to me that there might be a lot of readers who don’t know how to interpret the WSJ chart. For those who are interested, here is some background.

The first thing to notice is the WSJ box is wrong. CDS on US Treasuries are denominated in euros. In the WSJ box, the annual premium is stated in euros as it should be. But the notional value of the contract is stated in dollars in the WSJ box. That should be $10 million euros.

The price of 30K euros per year to insure 10 million euros means that the spread is 0.003 or 0.3% per year or 30 basis points (bps). If you buy protection you will pay 30 bps on a 10 million euro notional per year. For 1-year protection you pay for 1 year; for 5-year protection you pay annually for 5 years. But if there is a default, you will not be paid 10 million euros, but rather the post-recovery value of the 10 million euro notional. For example, if the bond recovery is 40%, you will be paid 60% of 10 million euros, or 6 million euros.

Events that can trigger a sovereign CDS depend on the contract but will typically include failure to pay, a repudiation of the debt or moratorium, and restructuring of the debt.

How do you interpret how big 30 bps is? One way to do it is to compare it to other sovereign CDS spreads. Markit has a convenient page that contains daily reports of CDS spreads over the last year. If you open the September 26 report and go to the table labeled “G7 Industrialised Countries CDS” you can see that the 5-year USD CDS spread is 31 bps, similar to Britain at 33 bps. However, Japan is at 61 bps currently. You can look at different reports on different days to see how the USD spread has changed over time. For example, on Jan 2 of this year, the USD CDS spread was 35 bps.

To understand what CDS spreads mean in terms of default risk, a useful approximation for the risk neutral probability of default is

PD(t) = 1 – exp(-s*t/(1-R))

where PD(t) = the cumulative probability of default over the time interval from now to t, s is the annual spread, t is the time horizon, and R is the recovery rate (default of 40%). exp() is the exponential function.

As an example, if the spread is 50 bps, then the risk neutral probability of default at 1 and 5 years is

PD(1) = 1 – exp(-.005*1/.6) = .0083 or 83 bps

PD(5) = 1 – exp(-.005*5/.6) = .04 = 400 bps, which is about 80 bps per year for 5 years.

These are the risk neutral default probabilities. We want however the real world default probabilities. Because we pulled these default probabilities from the spreads, they contain a risk premium to compensate for bearing risk. Risk neutral default probabilities, because they contain risk premia, are greater than real world default probabilities.

It’s difficult to estimate risk premia but just as an approximation you could cut in half the risk neutral default probabilities to estimate the real world default probabilities. So that means the real world 1-year default probability would be (1/2)83 bps or 41.5 bps in the example. And the 5-year default probability would be (1/2) 400 bps or 200 bps in the example

These calculations are just estimates of course. Hope this helps.

Menzie

You are even more ignorant on this issue that I thought. 2slugs correctly explains that the government will not default on it’s interest payments. They will shuffle cashflows internally to avoid missing a principal or interest payment. Of course, it’s always possible Obama throws a tantrum and chooses to miss a payment.

It’s time to grow up Menzie, drop your Progressive bias and present all the relevant facts, like JDH does. He doesn’t get nearly as much blow-back as you do because he presents a much more balanced view of the issues.

Rick Stryker I think you might be missing the larger point of the WSJ graph. The larger point is that up until very recently the spread between the 1-year and 5-year reflected risks that were uniformly distributed. In other words, the instantaneous hazard rate on day 360 was the same as the instantaneous hazard rate on day 1800. The chart is telling us that the instantaneous risks are no longer uniformly distributed; all of the risk is front loaded towards the next month.

tj: How do you know the government won’t miss an interest payment? I think I missed the presidential statement that the US government will prioritize debt payments (i.e., implement technical default).

So, exactly what was the point of you citing government closures in response to a post on CDS on debt defaults? That makes no sense, regardless. I wait explication. Until then, my thanks — that comment was good for more than a couple chuckles. I plan to share in my lecture tomorrow, in fact.

Finally, “blowback”? It’s only blowback if there is any intellectual content to the criticism. If the criticism is devoid of facts and/or intellect, then it is merely noise and fury.

tj Huh? How did you interpret my comments as saying that the US would not default on interest payments if the debt ceiling is not increased??? I was saying that there is a difference between what happens under failing to pass a CR and what happens under failing to increase the debt ceiling. Over the short-run very little happens if a CR is not approved. Things get worse as time goes on, but many Americans will not notice the effects…again, at least in the short-run. Hitting the debt ceiling is a completely different matter. Daily Treasury disbursements will be limited to daily Treasury receipts. It is unclear how Treasury will prioritize claimants. Will it be first-come-first-served? Will SS retirees get a prior claim? Will bondholders get a prior claim? Will everyone just take an across-the-board haircut? No one knows. I don’t even think Jack Lew knows. Also, failing to increase the debt ceiling will furlough even those who are exempt under the CR furlough. So we’re not just talking about shutting down parks and museums.

2slugbaits,

Rather than commenting on this topic, I was just trying to give people some background and tools to come to their own conclusions.

Unfortunately, you have everything exactly backwards, which is easy to do really. However, this is a good opportunity to provide some further examples of how to use the equations.

First, it’s wrong to say that risks are uniformly distributed if the 1-year rate is lower than the 5-year rate. Using the example I gave, suppose the 5-year spread is 50 bps but the 1 year spread is 10 bps. Then, the risk neutral probability of default over 1 year is

PD(1) = 1 – exp(-.001*1/.6) = .00166 or 17 bps

and over 5 years it is

PD(5) = 1 – exp(-.005*5/.6) = .04 = 400 bps.

Conditional on no default over the first year, the probability of default over the remaining 4 years is 400 – 17 = 383 bps, which is distributed over the remaining 4 years. The risks are not uniformly distributed. Lower default probability in the first year is compensated by higher default risk in the remaining 4 years.

However, if the 1-year spread rises to be equal to the 5-year spread of 50 bps, then the risks are now uniform, since

PD(1) = 1 – exp(-.005*1/.6) = .0083 or 83 bps

PD(5) = 1 – exp(-.005*5/.6) = .04 = 400 bps,

so that default risk is about 80 bps per year for each of the 5 years.

It should be also clear that if the 1-year rate moves up to the 5 year rate, that doesn’t mean that all risk is “front-loaded towards the next month.” In this example, the risk neutral default risk is 83 bps in the first year, about 1/5 of the 5-year cumulative default probability.

It’s also incorrect to say that the hazard rates are the same when the 1-year spread is lower than the 5-year rate. Just the opposite again. In these equations, we are approximating the hazard rate to be

hazard rate = s/(1-R)

where s is the CDS spread and R is the recovery rate on the bond.

The hazard rate is directly proportional to the level of the spread, approximately. A lower 1-year spread means the hazard rate is lower. When the 1-year spread rises to equal the 5-year spread, the hazard rates are uniform across time.

Keep in mind that all the default rates in these calculations are risk neutral–they are not the true default rates.

Menzie,

What class are you teaching? Do you keep a tally of how often you have used specific commenters to illustrate fallacies (AKA conservative viewpoints) to the students? I hope I’ve won the gold.

Rick Stryker: Sad to say, I don’t think I’ve used one of your comments. Timing has to match up with what is going on and what I’m teaching (macro topics this semester). I might’ve mentioned in passing your defense of Romney’s “500,000 jobs per month is typical in a recovery” statement.

Menzie

The point is that these are temporary shocks. I used the historical evidence available on the relationship between government shutdowns and stock returns to demonstrate that point.

You shriek like a scared child about the relatively minor economic impact of a failure to raise the debt ceiling or a failure to pass a CR in a timely fashion.

Your bias runs so deep you can’t even comprehend simple relationships or apply a little creativity to arguments that conflict with your Progressive babblings.

I feel sorry for your students, if you are as biased in the classroom as your are on this blog. The views of Professors can be very influential and I imagine you make no attempt to remove your political bias in the classroom. If so, you should be ashamed.

DSJ’s question still seems relevant to me. There is an implicit assumption in these CDS that in case of a default, the damage is really very limited and the insurers can still pay out. Is this really just a financial instrument that is created to put pressure on Washington? Does the trading volume show anything that makes it look like it is a real instrument in stead?

Menzie – If you equate policies and governance in Argentina with those of the US, then we are truly doomed. But it seems to me rather than you cannot distinguish between the drunkard at the party and the host taking away the punch bowl.

Having said that, I am not sure what the Republicans are up to here. Are we voting against the debt ceiling just for the hell of it? Or is delaying Obamacare by a year a huge victory–is it worth the spilled blood? I don’t understand the narrative. Where do we want to go?

There is a case to be made. If we allow that growth will be only 1.5-2.0% per year in the future, then clearly a 3% deficit is not sustainable. Given that we’re looking at a 4.5% gap this year, there’s a case for a gradual tightening to 2% or below. And a debt ceiling policy which puts the country on a predictable glide path would be a supportable policy, in my opinion. But I haven’t really heard that.

And there’s cause to get debt under control.

Personally, I am for an incentive plan which I might call the Fiscal Accountability Act, tying incentive pay of politicians to sustainable growth. (I have written on this before.) Such a law would be worth a shutdown, but otherwise, I don’t see where we’re headed at the moment.

Steven Kopits: I don’t have to equate two countries to say the same phenomenon will have a similar impact. Consider rent control. I will bet binding rent ceilings will induce excess demand, be it in Argentina, or the U.S. Analogously, debt default in Argentina and debt default in the U.S. will have some impact on perceptions of likely repeat default. I suspect the impact is smaller in the U.S., given Argentina’s reputation as a serial defaulter. But who’s to say — perhaps exactly because Argentina is almost expected to default, the impact on the U.S. spreads is larger.

The point is not that any two countries indexed by i in a sample are the same. The idea is that after controlling for other factors, a given variable behaves the same in response to different exogenous variables. It might be the responses differ quantitatively (that’s where econometrics, as opposed to hand waving, is helpful), but the qualitative effect should be the same.

tj: So you believe a debt default would have a minor impact? I think that speaks volumes. I didn’t coin the term, but I think it useful — I’ll place you in the “debt default deniers” category.

My students complain about my lectures incorporating too much math, or being too boring, or hewing too close to the textbook, or diverging too far from the textbook, or having too hard problem sets, or too few problem sets, or the like. They don’t complain about politics. I’m sure you could file a freedom of information act request to get the evals, if you don’t believe me. (I know the handouts and notes would be gibberish to you, given the level of math capability you have demonstrated in your comments, but for your edification, here they are.)

It would be entirely possible to tighten the debt ceiling such that it would limit spending by an attainable amount, say $100 bn. That by no means implies default on US debt, but it does involve the need to reduce spending in a measured fashion as the price of approval for any ceiling increase.

But doing so would involve analysis, advance notice, communication, and consensus building, among others (on the right, at least). Republicans haven’t done that.

That’s why a Fiscal Accountability Act is so much more preferable: 0.25% * (change in GDP minus change in government debt) / 537 members of House, Senate, Pres and VP. Democrats can then spend whatever they want, but each percent of deficit will cost them $500k apiece. Then we’ll see how important the deficit really is.

Menzie

So you believe a debt default would have a minor impact? I think that speaks volumes. I didn’t coin the term, but I think it useful — I’ll place you in the “debt default deniers” category.

The rational folks don’t expect Obama to choose default. Not that he cares about the consequences, but a default on his record might ruin his legacy.

On the other hand, he has appeared a bit unhinged lately. Perhaps it’s the long run effects from his days as a drug user with his choom gang friends.

From Dreams of My Father, Obama admits to cocaine use and that he tried drugs- “Pot had helped, and booze; maybe a little blow when you could afford it.”…“I kept playing basketball, attended classes sparingly, drank beer heavily, and tried drugs enthusiastically. …

Come to think about it, your chicken little act regarding the likelihood of a U.S. debt default borders on lunacy as well.

Our debt paths are simply unsustainable. We say dumb things like “3%” deficits per year, but even those are unsustainable because if we have a recession 3% suddenly is 10%, and in the good times we are never below 3%. All this is built on an assumption of GDP growth averaging 3% which is laughable in the new global economy, painful demographics, and restrictive regulations. Republicans are a garbage party and I truly despise most of them, but Democrats are either dumb or just don’t care this we can not continue on this path for much longer. We are due for and probably will have another recession in the next 4-5 years, what does that do to our budgets?

Also, Menzie I appreciate your relatively free speech policy, even when criticism is directed at you. That shows good character, even if you are a communist.

tj,

your comment:

You shriek like a scared child about the relatively minor economic impact of a failure to raise the debt ceiling or a failure to pass a CR in a timely fashion.

that had me rolling! you deserve all the tea baggers will bring your way. obviously you have no experience in the world of business or finance. in addition, as a partisan hack your comments are simply stupid!

failing to pay the debt is an explosive situation. now you see BOTH democracts and republicans coming out and saying so. as a debt limit denier (i like that) you are truly baffling.

if a clean bill appears in Congress to address the CR, and another appears to address the credit limit, i guarantee you both will pass in a bipartisan fashion. why are these clean bills not presented? why are they only presented tainted with partisanship?