I was in New York on Friday attending the U.S. Monetary Policy Forum. One of the sessions was on how central banks could better communicate their plans for using unconventional monetary policy. Federal Reserve Bank of Chicago President Charles Evans presented some very interesting ideas.

Evans argued that the most important element for effective communication was for the Fed to make very clear what it is trying to achieve. Congress has given the Federal Reserve a dual mandate to maintain stable prices and maximum employment. But what does that actually mean in practice?

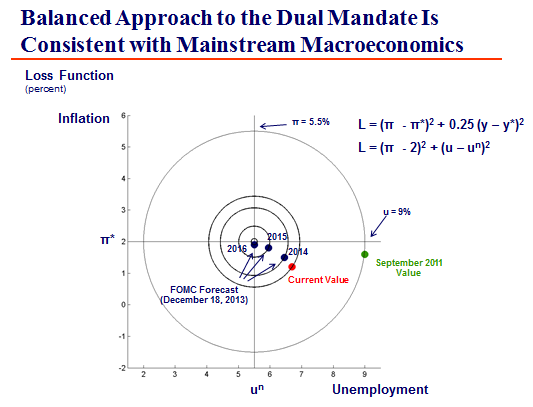

A large number of theoretical economic analyses represent this idea in terms of long-term target levels for inflation and unemployment. Suppose that our goal for monetary policy is to see an inflation rate around 2% and the unemployment rate close to 5.5%. We might then summarize how far off the Fed is from this long-term objective with a function like [math]V=(\pi-2.0)^{2}+(u-5.5)^{2}[/math] where π denotes the inflation rate as measured by the PCE deflator and u is the unemployment rate. With the inflation rate currently at 1.0% and the unemployment rate at 6.6%, that implies a value for the objective function of [math]V=(1.0-2.0)^{2}+(6.6-5.5)^{2}=2.2[/math].

If we use a function like this to summarize what we’re hoping to achieve, we’d say that if the Fed were able to get the unemployment rate down to 6.0% but at the cost of bringing inflation up to 3.4%, we’d be no better off than we are right now: [math](3.4-2.0)^{2}+(6.0-5.5)^{2}[/math]. The set of all points [math](u,\pi)[/math] for which we’d be doing about as well as we are right now will be recognized as the equation for a circle: [math]2.2=(\pi-2.0)^{2}+(u-5.5)^{2}[/math]. We’d prefer to be on one of the smaller circles, closer to the bull’s eye on a figure like this:

Source: Evans (2014).

Here’s how Evans interprets this:

This balanced approach implies strongly that our policy loss function can provide what I refer to as “bull’s-eye” accountability. This entire chart is like a simple “corporate scorecard” for our two-dimensional policy objectives in unemployment and inflation outcomes….

The most recent December 2013 Summary of Economic Projections shows that the Committee forecasts that unemployment and inflation will reach the bull’s-eye mark by the fourth quarter of 2016. This is a relatively slow attainment of our long-run goals. It also should be pointed out that these are still just projections of improvement, yet to be achieved. Nevertheless, the enhancements to our communications in recent years go a long way toward meeting our communications objectives by using this scorecard to depict progress toward our dual mandate goals….

my claim is that to be any good, monetary policy communications regarding policy actions must be consistent with the Fed expressing policy intentions clearly, so that the public can understand the Fed’s goals and its commitment to achieving these goals in a timely fashion. This should be a principle for all effective monetary policy strategies and communications: to state monetary policy intentions clearly.

I think Evans is making an excellent point. But I also agree with Federal Reserve Bank of Philadelphia President Charles Plosser, who observed as part of the same panel discussion “that dot in the middle is actually very big.” The truth is we don’t know with that much precision how low the Fed can really get the unemployment rate. Maybe 5.5% is an achievable target, as Evans’s figure above assumes. But it’s also possible that we’re not going to see an unemployment rate much below 6%, no matter how hard the Fed tries.

Nevertheless, I am very sympathetic to Evans’s suggestion. It is easy for reporters and financial analysts to get bogged down in the details of Fed operations regarding the size and pace of tapering and what will come after that. Using a figure like the above as akin to a corporate scorecard can help us all to better understand the kind of circumstances that would cause the Fed to change its operating tactics in pursuit of fixed goals, and to hold the Fed accountable for how it is doing.

How about NGDP level targeting? If the Fed simply targeted the NGDP level, they would have policy goals that were extremely easy to explain and we could stop worrying about whether 5.5% or 6% is the right unemployment target, or whether 1.8%, 2%, or 2.3% is the right inflation target.

Kenneth Duda

Menlo Park, CA

kjd@duda.org

Let’s be honest here, the Federal Reserve is a private corporation owned by member banks. Therefore, whatever the “mandates” are, their policies first and foremost are to protect their member banks. Which is another term for protecting the employees, stockholders, and large depositors and investors of those banks.

Whatever else we hear come from their mouths, and apparently yours, is propaganda.

Very nice chart.

There are (at least) two issues with it though:

1. As we have seen in the last few years, unemployment is not always a good indicator of the amount of slack in the jobs market. A lot of people have stopped looking for a job in the last couple of years (even though they’d like to have one) which has shown up as a decrease in unemployment despite a continually low labour force participation rate.

2. In Charles Evans reasoning, 1% inflation is worth as much as 1% unemployment. Having inflation go 1% above target is just as bad as unemployment 1% above target in this model. While I wouldn’t presume to know what the actual tradeoff is, I very much doubt that it’s a simple 1:1 .

Does this really address the basic rationale for why the Fed wants to clearly communicate its plans? The whole point of Fed communicating its plans is because markets are dynamic, and this means you have to be concerned about the speed of adjustment towards some goal. For example, unemployment goes up a lot faster than it goes down, but the metric proposed by Evans does not distinguish between being one percentage point above the target versus being one percentage point below the target. This is clearly wrong because an unemployment rate that is one percentage point above target will take a lot longer to achieve the target than an unemployment rate that is one percentage point below target. Does this communicate to the public that the Fed thinks their policy pace should be symmetric since the metric is symmetric? I hope not. I don’t think anyone cares about the value of the metric per se because it is just a static snapshot. And because it’s just a static snapshot it’s hard to see how it provides a forward looking public with any useful information about the pace and urgency of future Fed responses as they try to move towards the goal. What Evans has proposed looks like they are trying to solve a dynamic problem by putting out a static metric.

FWIW, a better (but still static) measure might be a weighted geometric average, with each of the weights being an exponent equal to the reciprocal of the variables coefficient of variation. Noisier variables would get less weight. The metric would be a kind of Fed Panic Index.

You make a seriously great point. Another asymmetry that is missing in this chart is deflation. A change from 0 inflation to -1% would cause far more harm than a move from 1% to 0 inflation (or, conversely, an unemployment rate 3% above full employment). Inflation stabilization should receive far more weight when inflation gets close to zero.

In addition to the above, this model asserts that a drop in the unemployment rate from 6.6% to 4.4% with no corresponding change in inflation is not an improvement. Is there anyone, really, who believes that the unemployment rate is both a meaningful measure and that a 2.2 percentage point drop in the rate with no adverse effect to inflation would not be a good thing?

Even worse, this model suggests that any reduction in employment below 5.5% is a bad thing!

I should have been more clear. While the long-term target inflation rate (in this example, 2.0%) is a choice variable for the Fed, the long-term target for the unemployment rate (in this example, 5.5%) really is not. Instead, in the theoretical framework underlying this objective function, the long-term target for the unemployment rate corresponds to the level that actually could be achieved and sustained. As a practical matter, we don’t really know what this number is, and this is the core of Plosser’s criticism which I attempted to convey. While we do not know for sure what the long-term sustainable unemployment rate is, I think there would be widespread agreement that it is a number greater than 4.4%.

For more details on the derivation of such an objective function, see Woodford (2003, Chapter 6). Another detail that I did not go into in the above post is that the more conventional motivation is in terms of the output gap rather than the unemployment rate. Evans’s derivation assumes an Okun’s Law relation between the two.

“[I]f the Fed were able to get the unemployment rate down to 6.0% . . . ”

The Fed does not “get the unemployment rate down” or up.

Also, virtually ALL of the decline in the reported U rate since 2009-10 is from the decline in labor force participation, not a net increase in employment. The labor force continues to decline. Had the participation rate remained at the secular high (demographics suggest that this is unlikely) and the persistently long-term unemployed remained as officially unemployed, the U rate would be 11%.

Flawed premises all around.

I understand why deflation is to be avoided but why is the inverse, say positive inflation of ca. 2%, a good thing in the eyes of economists?

It’s an interesting visual approach from the Fed, but I think the comments–all trenchant–point out the potential pitfalls. Slugs makes a good point on speed of adjustment, Hugo on choosing parameter values correctly.

And at the end of the day, I probably agree with Ken Duda: NGDP targeting just seems easier and simpler. But maybe I have been reading too much Scott Sumner.

Could we have an update, please, on the revised GDP numbers.

Thanks.

Unemployment rate = 5.3%, PCE price inflation = 2.1%, V= 0.05%. Perfect bull’s-eye. Superb job well done. William Tell loosed not a finer arrow. Date = July 2007. Credit bubble imploding and financial system about to collapse. Brilliant shot on target, though. Just brilliant!

From a private organization that polls real people every day for their self-reporting of their personal situations:

http://thechairmansblog.gallup.com/2014/02/the-us-economy-kidding-ourselves.html

In the meantime, most neo-feudal/neo-Medieval economists/imperial ministerial intellectuals are so well “educated” in eCONomics and in touch with the real world as to continue to debate the methods for accurately counting non-existent angels on the heads of pins.

Good grief.

There has been about 8.5 million private sector jobs added since the recession ended, 7.8 million total jobs (subtract -700,000 public sector jobs). See charts at: http://www.calculatedriskblog.com/ and http://www.calculatedriskblog.com/2014/03/schedule-for-week-of-march-2nd.html. Yes, the U3 would be higher than 6.7% if the participation rate was higher, but even U6 has fallen to 12.7% (still way to high) from 17.1% at the despond of the employment valley. http://www.portalseven.com/employment/unemployment_rate_u6.jsp. (one interesting feature of this chart is that it reveals that U6 started steadily rising beginning in December 2006, a year ahead of the official beginning of the “Great Recession, and that although the 2001 recession was suppose to short and mild, unemployment kept rising through 2002-2004, and never approached the low for U-6 in April 2000). Has Fed policy helped move these numbers? I would say that it has probably been the biggest factor, certainly counterbalancing the Fiscal austerity of the 2011-13 period while residential investment and commercial real estate investment spending continued to flat line. The sad thing is particularly from mid-2009 to mid-2011, the Fed continued to big looking for the inflation bogeyman under the bed and to “exit” and clean up its balance sheet from QEI.

Worldwide, I think disinflation/deflationary forces still dominate as globalization and the internet place OECD workers in more and more direct and indirect competition with millions of workers in China, India, SE Asia, Bangladesh, Pakistan, Latin America, South Africa, and East Africa, who are moving from countryside and subsistence agriculture to cities and factories and service centers. This has the effect of depressing wages to a common level no matter how technical or expensive the educational requirements. http://www.npr.org/2014/03/01/284178406/a-picket-line-at-the-oscars-visual-effects-artists-to-protest. Further, as the Chinese and Indian investment booms/bubbles move to the “bust” phase in the Minsky cycle, the price forces on commodities is now the opposite of what it was 10 years ago. To many people, are making to much stuff, for to little demand, while capital seeks security in cash and cash like assets (Treasuries, gold, etc.). So in a sense the Fed has been trying to inflate a tire that has a rather large leak in it. It makes some progress as long as it keeps pumping in air, but if it slows the pump, the tire starts going flat again.

I think it would be beneficial to improve communication but probably not much. The biggest gains are to be made by improving the monetary transmission channel’s effectiveness. People are quite aware of the goals of the fed and how it intends it to achieve these. The reason expectations wont budge upwards is because markets don’t expect the current channels of monetary policy to be effective. The current fed counterparties have a low marginal propensity to spend so expansion of money to these entities has little effect on spending. Asset markets are too concentrated in ownership so increases in asset prices that result from monetary policy also have too weak an effect and the credit markets are stagnant in part due to high unemployment. If the CB directly interacts with the broad public these issues can be addressed.

Why do we need “guidance” since it is perfectly obvious that the Fed’s one and only goal is to protect the interests of their fellow bankers. They’ve undershot both of their mandates simultaneously — inflation and employment — which anyone would have thought impossible just a few years ago. It is obvious from the FOMC minutes that only one mandate really counts.

It was quite shocking to read the minutes of the FOMC meetings in late 2008. Bear Stearns had gone down, Lehman had gone down, the economy was collapsing and the only thing they could talk about was raising interest rates to stop inflation. You had Ben Bernanke, who had written a paper on why you should ignore volatile commodity prices saying we might need to raise rates because of high gasoline prices. It seems you get swallowed by the Borg and everything you ever learned and said in the past is erased. You had Richard Fisher pushing for higher interest rates because, I kid you not, his favorite bakery had raised their price for doughnuts.

These aren’t the best and brightest using all of the sophisticated tools and staff at the Fed to work out the economy’s problems. They are bunch of fools operating by the seat of their pants, using personal anecdotes as data, while pushing their own personal prejudices and interests.

The Fed? I like Ripley’s prescription from Aliens: “I say we take off and nuke the entire site from orbit. It’s the only way to be sure.”

A circle and bull’s-eye is interesting but graphically it is not differet from a line with employment on one side and price stability on the other with monetary policy landing somewhere in between. What Evans is actually telling us is that the FED cannot hit two bull’s-eyes with one arrow, but we should already know that.

But the whole discussion misses the point. Can monetary policy actually correct fiscal policy. Employment is based on business activity. Burying dollar bills around the base of an apple tree does not guarantee more apples and even worse giving the money to the local banker definitely does not guarantee more apples.

The FED would do better if it stabilized the currency so the price signals for producers were not distorted. Then end the waste of assets through arbitrary redistribution and once again let market demand, consummers, distribute wealth as they see fit. Stop the government guessing (or stealing, take your pick) and let the market do its job.

What the Fed/TBTE banks have succeeded in doing is encourage and reinforce the largest global credit and financial asset and real estate bubble in world history by far, bigger as a share of GDP and wages than the 1820s, 1870s-80s, 1920s, and Japan in the 1980s.

This MASSIVE asset bubble and the coincident OBSCENE wealth and income concentration to the top 0.01-0.1% to 1% and falling labor’s share to GDP is a debilitating rentier claim against future real after-tax profits and wages, as well as gov’t receipts.

The cost of the central bank/TBTE bank-induced unprecedented global asset bubble is no growth of real GDP per capita indefinitely from 2007-08, whereas the EXTREME overvaluation of financial assets renders the financial system increasingly fragile and vulnerable to any number of “black swans” that will prick the bubble and precipitate a crash that will make 2008-09 look like a amateur dress rehearsal.

When the next debt-deflationay crash occurs, it won’t be because of China, EMs, Russia, the Fed, ECB, BOJ, or any other singular causal event or events; it will be because there is too much private debt to wages and GDP that precludes growth hereafter, resulting in a MASSIVE financial asset bubble. All bubbles burst. The biggest bubbles burst spectacularly. There has never been a global financial bubble of today’s size. The world is now facing a MASSIVE asset bubble waiting to pop.

Given the Fed/TBTE banks’ response to date, one should not be surprised that during the next crash the TBTE banks direct the Fed to buy overtly the stocks of banks, insurers, and non-bank financial firms, as well as equity index futures in a desperate end-game attempt to prevent systemic implosion. Doing so will be an unambiguous sign that the system is fatally compromised and can no longer function successfully on its own.

Historically, the elites have chosen large-scale war as the economic and political policy of other means in times of crisis to retain their legitimacy, authority, privilege, and power. Given the events in Ukraine and China’s ongoing encroachment in Africa (modern-day “race for Africa”), the western elites will have numerous rationalizations for imperial wars to respond to deteriorating financial and economic conditions and to put down domestic popular discontent or worse.

Hey BC, if it is going to happen then why not have a drink and relax dude? Only decaf coffee for you from now on.

Randall, advice taken, fellow dude.

BTW, I enjoy Earl Grey tea, perhaps too much.

Professor Hamilton wrote:

I still remember in the early 1960s economists saying that the normal unemployment rate was below 4.4% and they became concerned when the unemployment rate began to rise above 4%. The in the Johnson administration an economist (I don’t remember his name) claimed that with Keynesian stimulus (he was a Keynesian btw) the real unemployment rate should be 5.5%. Professor, it sounds like you have bought into the Keynesian demand side unemployment rate rather than the classical supply side rate.

It is interesting that during the Clinton administration unemployment fell from 7% cuased by a recession before he entered office to below 5% the last two years (starting in 1998). We see a similar situation during the Bush administration (starting in mid-2005). So it appears that unemployment is above 4.4% during economic sluggishness but below 4.4% during prosperity. So if you anticipate unemployment to remain above 4.4% you must expect a sluggish economy.

I don’t see how anyone can parse the numbers the Fed uses to calculate unemployment, inflation, etc when they are suspect to begin with: http://www.shadowstats.com/

I recall early in this last malaise seeing the opinion expressed on these boards that the Fed could surely set the money supply. Now, I get the same sense of a lack of grasp of the change that has occurred in the macroeconomic landscape. The Fed has very limited power to accomplish anything in present circumstances. What they can do is transfer scarce AD from other countries to the U.S. and, to a lesser degree, from the future to the present. In both cases, they should hope that circumstances won’t make that a short-sighted policy.