“I am going to take care of everybody. I don’t care if it costs me votes or not. Everybody’s going to be taken care of much better than they’re taken care of now.”

— Donald J. Trump, September 27, 2016

CBO has released its cost estimate. President Trump’s promise will not be fulfilled by this particular legislation.

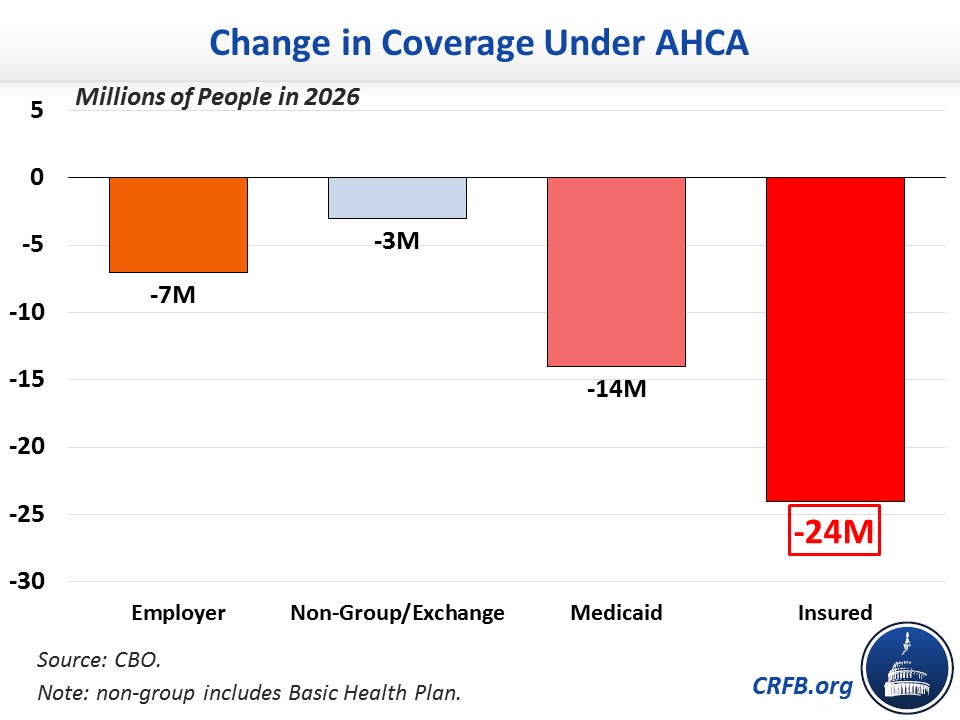

CRFB presents graphically the impact by 2026:

Source: CRFB.

If the 24 million reduction in insured relative to current law weren’t alarming enough, the 14 million reduction by 2018 (which is next year, for those of us who still mistakenly write “2016” when dating letters or checks) is pretty impressive(ly bad).

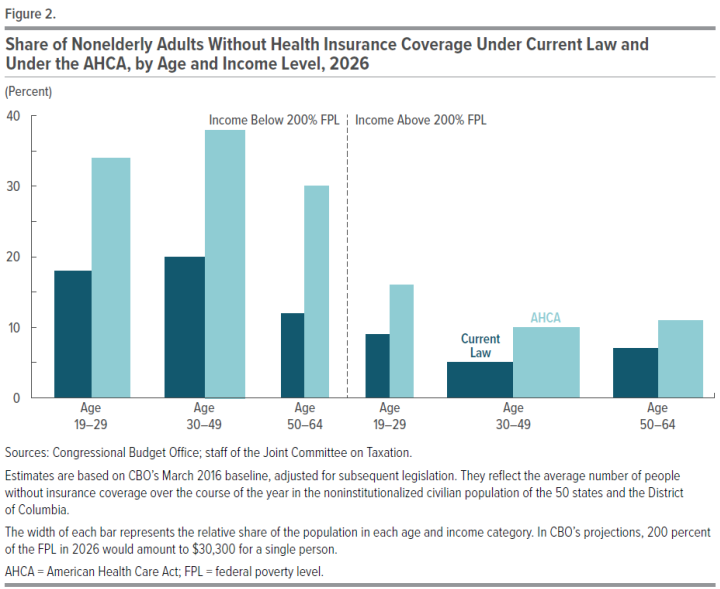

Unsurprisingly (to me), the negative impact will be most profound on the lowest income groups. From the CBO cost estimate:

Source: CBO.

As noted here, numerous critics of the CBO’s scoring and projection process have made pre-emptive attacks. However, to my knowledge, thus far no one has outlined specifically their criticisms (e.g., with respect to elasticities, etc.). For the record, CBO was not far off in their estimates (h/t TPM).

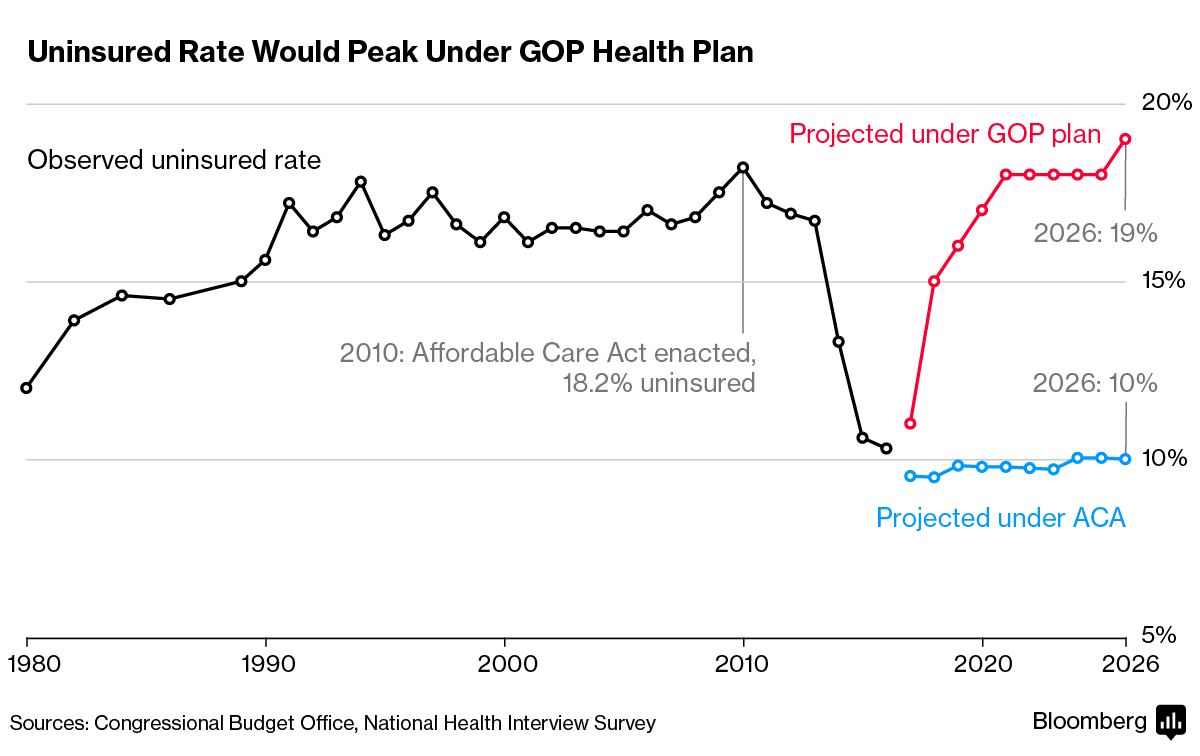

Update, 7PM Pacific: Bloomberg has another nice graphic depicting the time series under the two alternatives.

Source: Bloomberg.

Update, 7:30PM Pacific: Apparently, at the same time the White House and HHS Secretary Price are disparaging the CBO estimates of coverage loss, internal White House analyses indicate even greater losses, at 26 million, as reported here.

Dean Baker said that after freezing medicaid, within 3 years half would come off, mostly due to employment. In block granting it will the states be able to accept new entrants or does it quickly fade away over time?

Menzie,

You should read the CommonwealthFund study that you linked to more closely. They are examining the CBOs forecasts only for the year 2014, which was the CBO’s most accurate year. But 2014 was too early for most to see the perverse incentives of Obamacare that critics like me pointed out.

Both the CBO and the Administration’s CMS discounted these perverse effects. According to the CMS in 2010, by the end of 2016 the exchanges were supposed to have 25 million enrollees. In 2010, the CBO predicted 21 million enrollees by the end of 2016. The CBO revised that estimate in 2012 to 23 million by the end of 2016. Revisions in 2013 and 2014 were to 22 million and in 2015 the CBO revised the estimate to 20 million. It was only in 2016 that the CBO saw the reality, revising the estimate to 10 million.

That 2016 estimate is about right. In 2015, there were about 12 million confirmed enrollees, with about 9 million paying. In 2016, there were almost 13 million enrollees. We don’t know how many paid yet, but 10 million is probably a good estimate. But that means the CBO has been off by more than 50% for most years.

The CBO got obamacare massively wrong. Why? They didn’t properly account for the perverse incentives and the adverse selection. The CBO would have profited from reading my comments on the ACA in econbrowser, especially those in which Rick Stryker Jr. explained why he as a young person wasn’t signing up. Obamacare’s incentives for the healthy to sign up for insurance were too weak; the insurance was too expensive, considering the high deductibles and narrow doctor networks. When the relatively healthy didn’t take the insurance in the numbers actuarily necessary, the proportion of people on the exchanges who disproportionately consume medical resources was too large and premiums had to rise. But the rising premiums increased the incentive for the healthy not to sign up, resulting in a slow death spiral.

Obamacare has to be fixed as I’ve argued repeatedly in the past. It would have been fixed whether Clinton or Trump won. If the Democrats had worked with the Republicans to fix it after the 2014 elections as I had suggested then, Hillary might be President today. I’m not arguing at this point whether the CBO is right in their current analysis of the Republican plan. But I don’t think there is any doubt that the CBO’s track record on healthcare analysis hasn’t been great.

Rick Stryker: CBO overestimated those on exchanges, underestimated uptake on Medicaid, leading to overall pretty accurate estimates of coverage change:

With respect to exchanges, part of the mis-estimate is due to the fact that employee based coverage did not decline as much as CBO forecasted — so exchanges in some sense did not need to take up as much slack.

From Kaiser Family Foundation (2016):

Menzie,

You are parroting the silly defense that CBO defenders are currently pushing, i.e., since the CBO made large forecasting errors in opposite directions on the Medicaid expansion and on enrollment on the exchange, we can average those errors and say that the CBO was right on average. Sorry, no. The direction of the forecasting errors matters and the CBO got the direction wrong in both cases.

Let’s start with Medicaid expansion under the ACA. The critics of this expansion argued that it was a mistake for states to sign on. Although the Federal government would pay initially, the obligation to pay would transition to the states over time. The concern of the critics was that when you give out a free benefit, many more people would sign up than predicted, busting state budgets. The critics of the ACA medicaid expansion disagreed with the Administration and the CBO, saying that their predicted Medicaid expansion numbers were much too low. The critics were right and the CBO was wrong. Medicaid expansion numbers came in much higher than the CBO predicted.

On the exchanges question, I’ve already noted the massive forecasting error the CBO made. You have tried to mitigate the size of that mistake by referring to the Kaiser Family Foundation study that suggests that 6 million of that mistake can be explained by the CBO expectation that 6 million people would transfer from employer to exchange insurance, which didn’t happen. But if you look at the Kaiser study, you can see that they have no support for that claim. Kaiser refers to a 2015 CBO table that lists the 6 million expected to transition from employer insurance. Kaiser assumed that all of the 6 million would go to the exchanges. Kaiser should read what the CBO has actually said on the matter. For example, in 2010 the CBO said that there were 3 flows leading to its estimate of the net reduction in employer insurance: 1) increases in employer insurance resulting from ACA requirements; 2) reductions in employer insurance, primarily from small employers that would find it advantageous not to offer insurance; and 3) people who transitioned from employer insurance to exchange insurance. The CBO was clear in 2010 that category 3 was in their estimate 1-2 million people, which doesn’t do much to mitigate the size of the forecasting error.

On the crucial policy issues, the CBO got it wrong. The policy issue on the Medicaid expansion was whether the uptake would be much larger than the proponents of the ACA claimed, putting stress on state budgets. The CBO substantially underestimated the size of the expansion. On the ACA, the policy question was whether the highly regulated insurance, the relatively weak mandate, etc. would disincentivize people to sign up in sufficient numbers to avoid an adverse selection spiral, as the critics claimed would happen. The CBO got that wrong, overestimating the uptake.

To be clear, I’m not claiming that the CBO’s mistakes were some sort of partisan conspiracy. The CBO is a non-partisan agency staffed by professionals. But I am suggesting that no policy analysis or forecasting group, including the CBO, is infallible. Analysis of complex policy proposals is always hard and uncertain. We should take the CBO analysis of Trumpcare under advisement. But let’s also look at alternative analyses.

By the way, the CBO is still getting it wrong. In March of 2016, the CBO projected that of the 12.7 million people who signed up for insurance on the exchange, 12 million will on average be enrolled in any given month. Despite having consistently overestimated enrollment in the exchanges, the CBO nonetheless projected the numbers to start rising in 2017, with 15 million on average enrolled over 2017, 18 million in 2018 and 19 million in 2019. With an expectation of 15 million on average enrolled in 2017, the CBO was predicting that around 16 million would sign up for 2017.

We know now that the CBO significantly overestimated the numbers again. 12.2 million signed up for 2017, not 16 million.

that is still 12 million more people with health insurance, which is good for the country as a whole. in the proposed conservative plan, those people will not have health insurance. that is bad for the country as a whole.

Rick, the CBO also thought the employer based insurance would lose people, because companies would rather drop workers than deal with the cost of the insurance. you promoted the same idea as well. i think you were both wrong on this account, and this also resulted in fewer signups for the exchanges.

Baffles,

As I pointed out, the CBO initially thought the transition from employer-based to exchange-based insurance would be about 1-2 million. You are right that I emphasized that point and did a lot of analysis arguing that Obamacare incentives for employers to push people onto the exchanges was quite strong. My analysis was valid. But you are right that it didn’t actually happen as much as expected. Why not?

The reason it didn’t happen is that the Obama Administration, under political pressure, changed Obamacare policy mid-stream. As you may recall, there was quite an outcry when people discovered that the former President’s promise that “If you like your plan, you can keep your plan” wasn’t really true. People did not want to be forced into Obamacare plans. The Administration reacted in two ways. First, because of the criticism, the Administration allowed people to grandfather Obamacare non-compliant plans. These non-regulated plans were often much cheaper and better, and so many small employers kept them rather than moving to the exchanges. Second, and perhaps more important, the Obama Administration’s IRS promulgated new rules that barred employers from dumping workers into health exchanges. As the New York Times article I linked to confirmed, employers had come to agree with the analysis I put forth in the econbrowser comment pages showing the strong incentive to dump employees on the exchanges. The Administration, realizing this, used the IRS to stop it. Here’s a telling quote from the NYT article:

“Richard K. Lindquist, the president of Zane Benefits in Park City, Utah, a software company that helps employers reimburse workers for health insurance costs, said, ‘The I.R.S. is going out of its way to keep employers in the group insurance market and to reduce the incentives for them to drop coverage.'”

2014 was an election year, and given the unpopularity of Obamacare, the Administration did not want damaging headlines on employees being forced onto the exchanges. So, they used the regulatory power of the IRS to reverse the policy.

So, I was right about this too. The CBO was less right; they only attributed 1-2 million to this transfer from employer to exchanges. I would have thought it would have been more. But the Obama Administration, realizing belatedly that my analysis and the CBO’s (to a lesser extent) was correct after all, reversed their policy to protect themselves in the 2014 elections. (Too little, too late for the 2014 elections. I was right about that too if you recall.)

rick, what you did not anticipate correctly was that employers recognized they could and would lose quality employees by dropping the benefit of health insurance. that seems to be the view among many business owners and hr professionals. the potential losses due to employee turnover, especially of good employees, is a difficult parameter to assess quantitatively compared to direct savings from dropping the benefit. but in this case, it seems many businesses complained but found there was better value in keeping the workers on full time payrolls rather than saving on the benefit cut.

Health care inflation has skyrocketed, since the 1960s, and physicians were spending 22% of their time complying with government regulations and insurance companies, just before Obamacare, which has since worsened.

We need to increase the supply of health care (to meet the increased demand government created), to lower prices, and deregulate to deliver more patient care rather than wasting time complying with excessive regulations.

It is not an either/or proposition to get more people covered and to deregulate/trust bust the provider side of the market

Too many regulations, since the 1960s, made health care a luxury good, along with creating massive inefficiencies.

Lower standards and less waste are needed to increase the supply, and decrease the price, of health care.

Government has done a great disservice forcing consumers and taxpayers to pay way too much for health care.

Peak Trader says,

“Lower standards and less waste are needed to increase the supply, and decrease the price, of health care.”

You know, an accurate translation is “more deaths and preventable illness, less protection of medical records against identity theft, and less preventive care will save certain people money.”

Regulations are not written for the fun of it, but because people have been maimed or died. Regulations have to survive public comments and congressional scrutiny. Usually the industry has a very strong role in writing them. To the extent that regulations are bad, it is generally because large companies write them to keep out small companies. That is definitely the case in the pharmaceutical industry, where the big companies are very happy to help write the regulations, stack the drug review panels, and get ridiculous patent extensions. To the extent there’s a problem, it’s “large amounts of money used to bribe Congress,” not “regulations.”

It’s very easy to trash “regulations.” The right routinely misrepresents the facts or points to a few regulatory failures to claim that repealing “regulations” will lead to some sort of economic utopia. We’ve seen the utopia in countries that have weak regulatory regimes: Haiti, Nicaragua, Zimbabwe.

To quote the OECD:

“Modern economies and societies need effective regulations to support growth, investment, innovation, market openness and uphold the rule of law. A poor regulatory environment undermines business competitiveness and citizens’ trust in government, and it encourages corruption in public governance. ”

People who want to do away with regulation usually want to promote corruption. The current Administration being a case in point.

Charles, so, you want more people dying from unaffordable health care. Resources are not unlimited.

There are foreign physicians, who can’t practice medicine in the U.S., because of the high standards, which also prevent RNs from performing some duties.

Or, rather than treating patients, you want physicians dealing with paperwork and malpractice suits, along with discouraging people from becoming MDs.

You can have safety standards on cars where few people are killed in accidents, but then you couldn’t afford a car.

Look at the coal industry, you can pile on so many regulations that it becomes impossible to mine for coal.

Medical tourism is unfortunate:

https://www.google.com/amp/www.thefiscaltimes.com/2016/08/17/14-Million-Americans-Will-Go-Abroad-Medical-Care-Year-Should-You%3Famp

The under supply of healthcare is a big problem. The number of medical school graduates per capita is 15% lower today than it was in 1980, and the U.S. has fewer doctors per capita than most countries. Of course this means that doctors make a lot more money here than anywhere else, so the AMA prefers to restrict supply and make their members more wealthy.

Letting nurses do more, letting more doctors emigrate, and graduating more doctors would reduce prices and increase access.

mike, we already have nurses do more. when i started college, we had an actual doctor in the student health center. by the time i finished graduate school-i never saw the doctor at the health center. only the nurse practitioner. my last flu shot was given by the pharmacist. we have had quite a bit of change in the last 20 years in terms of medical care, alleviating former duties of the doctor.

but you need to address the issue of competency. graduating more doctors may put less competent doctors in the field. and you still need to train them. residency programs are expensive. you may reduce prices at the consumer level, but you have added cost at the training level which somebody needs to cover.

a lot of the cost over the past 20 years has not been driven by a lack of supply of doctors. it has been driven by the multitude of expensive diagnostics which have become available. MRI, CT, etc are not cheap. but they are plentiful. in addition, too many specialties and too few general practitioners has had an impact.

“Health care inflation has skyrocketed, since the 1960s,”

yes, lets blame obamacare for health care inflation since the 1960’s! its interesting, we have had health care inflation for 7 plus decades, but somehow its the past couple of years, during the obama years, when all the blame get applied to obamacare. look peak, health care inflation was a major problem prior to obamacare. you try to hoist that failed system onto obamacare. that is why you are a hack.

now i agree with you on increasing the supply of health care. but you will find a decrease in the quality of health care as a result. same thing happened with the law degree and law salaries. more medical doctors will change the dynamics, for good and bad. it is not a panacea. in order to produce more doctors, you need more training facilities. this costs money. training a resident is not cheap or easy.

Baffling, making things up, like saying I blame Obama for the high rate of health care inflation, since the 1960s, shows you’re the hack.

I’m sure, you want a luxury car, that was produced at a much higher cost than necessary, for little money. What you’ll get instead is either nothing or someone else subsidizing a short joy ride for you.

peak, you intentionally included obamacare in your sentence regarding health care inflation. please do not play dumb. that innuendo was intentional. which is why i called you a hack. make honest arguments, and i won’t need to call you a hack.

your “regulations” comments sound like a broken record. and with 24 million people off the insured roles, you should have no problem with supply/demand in a couple of years.

Baffling, don’t play games.

Stop re-defining what I say.

Only a hack would do that.

I am not redefining what you say. You want to play loose with words. I can do the same. Your conservative president has taught me this skill set. I will apply it as needed over the next four years. If you don’t want to be a hack, then don’t use such innuendo peak.

Now, don’t be critiquing Mr. Stryker’s point–apparently–that Obamacare created pre-2010 healthcare inflation and isn’t responsible for tamping down said inflation.

That would harsh the libertarian mellow!

And if you shouldn’t give healthcare to anyone who didn’t have it, well then, why brag about it?

Amirite?

And darn that CBO! Gosh darn them.

Really, congresscritters should just provide their own estimates of their legislation–that’ll work!

Skimming the CBO summary, I do not see any adequate accounting for the costs to states and localities, hospitals and other institutions, individuals or the economy. In other words, it might “save” the federal government $30-some billion a year, but what will the cost of this chaos be to everyone else.

I was especially perturbed by the paragraphs on hospitals.

“Other Budgetary Effects of Health Insurance Coverage Provisions. Because the

insurance coverage provisions of the legislation would increase the number of uninsured

people and decrease the number of people with Medicaid coverage relative to the numbers

under current law, CBO estimates that Medicare spending would increase by $43 billion

over the 2018-2026 period.

Medicare makes additional “disproportionate share hospital” payments to facilities that

serve a higher percentage of uninsured patients. Those payments have two components: an

increase to the payment rate for each inpatient case and a lump-sum allocation of a pool of

funds based on each qualifying hospital’s share of the days of care provided to

beneficiaries of Supplemental Security Income and Medicaid.

Under the legislation, the decreased enrollment in Medicaid would slightly reduce the

amounts paid to hospitals, CBO estimates. However, the increase in the number of

uninsured people would substantially boost the amounts distributed on a lump-sum basis.”

This sounds to me like $43+X+Y+Z = PiP, where PiP is “A Pig in a Poke”, the effects on hospitals. The hospitals themselves protested the ACA repeal, so I have the impression that PiP is a large negative number.

Any better estimates on the value of PiP?

so it seems a healthy 21 year old with a current $1700 a year premium will save 20%, and pay around $1400 per year under the new republican plan-with fewer benefits. i would assume this is enough to get rick stryker jr off his lazy butt and now buy health insurance like a responsible adult. all it took was a mere $300 subsidy, and all of rick strykers rantings about how the young will avoid buying health insurance will merely disappear with this wonderful new option. so rick, is your boy now going to buy health insurance under the new plan. or do you still advocate he remain a leach on society? and now we have 14 million newly uninsured next year, who can gain health care access affordably through their local emergency room.

I’m fascinated by the Right’s need to legislate health care as a moral obligation. Social sciences show the few people that respond to this kind of thinking and have the resources to afford health insurance already have it.

The rest of humanity will use the money in a manner they decide that does not include spending it on health care. The Right condemns this behaviour pretending they have somehow solved the average person’s fundamental scarcity of wealth problems.

In my opinion, the Swiss have the best combination of private and public health care. A Wikipedia entry on Swiss health care:

https://en.wikipedia.org/wiki/Healthcare_in_Switzerland

Jeffery J. Brown,

Perhaps, but it depends on how you define the “best”. One might have to look at the cost/effectiveness of both major and minor treatments. Having the “best” might not be attractive if it is not within one’s means. Or being the best in one area may not translate to another. Certainly, the cost, availability, and efficacy of medications are considerations. Our FDA has come under significant criticism for the cost and time to bring new drugs to market, particularly for so-called “orphan” diseases. Some doctors are advocating a “safety-only” FDA evaluation for drugs and let the internet-connected marketplace of researchers, doctors, and patients decided on efficacy.

http://www.thefiscaltimes.com/2016/08/17/14-Million-Americans-Will-Go-Abroad-Medical-Care-Year-Should-You

http://www.wbur.org/commonhealth/2016/10/31/american-british-health-care

2011 Forbes Article: Why Switzerland Has the World’s Best Health Care System

https://www.forbes.com/sites/theapothecary/2011/04/29/why-switzerland-has-the-worlds-best-health-care-system/#223cc8a57d74

“Full repeal, in particular repeal of ObamaCare’s health-insurance regulations, would cause premiums to fall for the vast majority of consumers in the individual market.”

https://www.cato.org/blog/cbo-more-lose-coverage-under-obamacare-lite-full-repeal

So, it’s possible that the Republican plan is akin to taking the broken windows out of a rotting warehouse and calling it a palace. No, delete the “it’s possible that”…. The entire remainder is an accurate simile.

Where’s that “RESET” button when you need it?

Cato is a right wing welfare org. that exists to push the agenda of the rich at the expense of everyone else.

Hey, but Cato made the wacko argument that libertarians love–namely health insurance that doesn’t cover anything will be a lot cheaper–and allow tax cuts for the 1%!

That’s if you use the Cato estimates.

“Full repeal, in particular repeal of ObamaCare’s health-insurance regulations, would cause premiums to fall for the vast majority of consumers in the individual market.”

while not a majority, that leaves a large number of people priced out of the insurance market. you are in favor of leaving them out of the insurance market, and thus out of health care? do you have a plan for these folks? or do they get to play a round of hunger games? and for the people who have a decrease in premiums, they really did not need health care to begin with, did they?

baffling

Of the 20 million or so that were insured under the ACA, about 2/3 just went on Medicaid and CHIP; and several million of those that went on Medicaid were previously eligible, but chose not to enroll. About 2-1/2 million of the 20 million were 19-25 year olds who have the lowest incidence of coverage need. And in 2016 over 80% of the newly insured went on Medicaid.

So, what it boils down to is a huge Ponzi scheme that siphons funds from all of the paying policyholders to place more people on Medicaid. It totally disrupts the healthcare system and many insurers while allowing the Democrats to avoid having to admit that all they did, effectively, was expand Medicaid without proper funding.

Time to hit the RESET button.

I’m sorry, but this just seems confused. If you want universal access to health insurance, then you must have an individual mandate in order to pay for it. And if you have an individual mandate, then you must make some kind of subsidy available for those who cannot afford the mandate. And if you have a subsidy, then you need a revenue stream. That revenue stream must come from a combination of young & healthy people (temporarily overpaying…someday they too will be old & unhealthy) and high income folks. Those are just the basic accounting requirements. There’s no escaping the arithmetic. So I don’t know what you mean when you talk about not properly funding Medicaid. The Democrats wanted to increase Medicaid funding. It was the GOP that urged the Supreme Court to strike down the Medicaid expansion, remember? I suspect that your real gripe is that you resent poor people getting any kind of aid that might cost you money. But you know what? Since Obamacare kicked-in the growth rate of health insurance premiums for those of us that already had employer based health insurance slowed down dramatically. Last year was the first significant uptick, and even that was far less than the annual increases we would see before Obamacare. Contrary to the nonsense hat PeakTrader spouts, healthcare costs have been growing at a slower rate than we saw before Obamacare. Granted, not all of that reduction is due to Obamacare alone, but some of it is. Obamacare did nothing that would actually increase the cost growth rate.

I also don’t know what you mean when you say that Obamacare “disrupts the healthcare system and many insurers…” The insurance companies did pretty well under Obamacare. True, they did have to accept a higher risk demographic, but the federal government cushioned those costs. At the same time, Obamacare lowered the costs for those already insured through group plans.

Obamacare basically needed two relatively easy fixes. The first fix should have been a stiffer penalty so folks like Rick Stryker’s worthless, freeloading son is forced to carry his share of the load. The second fix would be a public option.

2slug,

“If you want universal access to health insurance, then you must have an individual mandate in order to pay for it.”

Why? Simply expand Medicaid for those who can’t afford insurance or let them choose high-deductible catastrophic insurance for those who want a lower-cost plan… like it used to be. Then, let the representatives who support such action find a way to fund it without screwing up the whole market which is what ACA has done.

Mandating the purchase of a product to have someone else pay for it (effectively subsidizing Medicaid) is devious and wrong. Tell the people that their taxes are going to go up $1,000 to $5,000 based on their income to pay for Medicaid expansion… and see how many are clamoring for “universal access”. Presently, it’s a dishonest scheme that tries to blame the insurance companies for rising rates and less coverage.

I believe that Cato article was well-written by a man quite familiar with the shortcoming of both the ACA and the Republican “revision”. https://www.cato.org/blog/cbo-more-lose-coverage-under-obamacare-lite-full-repeal

bruce,

universal health care was brought to us by st. reagan in the 1980’s, when he forced emergency rooms to treat all patients, regardless of insurance status. so universal health care was brought to us by the compassionate conservatives. it was already an unfunded mandate, as emergency rooms costs were not picked up by the government. the current approach is to provide those services in a much more economical and efficient way. the choice has already been made years ago.

“Mandating the purchase of a product to have someone else pay for it (effectively subsidizing Medicaid) is devious and wrong. ”

that is what employer based health insurance is. in that case, the young workers subsidize the older workers. you never noticed everybody pays the same amount for premium at the workplace? subsizided. why are you not screaming about that scheme?

baffling,

Obviously, you were never involved in employer paid health care. First, it was treated as a benefit so even though it may have reduced the employee’s gross it was not taxable so it was a true benefit. Secondly, the cost was reduced by the employer’s ability to negotiate prices/coverage that were generally superior to that which individuals could obtain. Thirdly, and to your point, individuals (before Obamacare) could opt out and receive compensation from their employer (that, of course, was dependent on the employer). Naturally, under Obamacare, those individuals would have to purchase insurance or be fined (coerced).

While Reagan may have begun the process of having individuals treated at ERs, it was subsequently expanded to include 12-20 million illegals (depending on whose count you want to believe) which was never Reagan’s intention.

Prior to Obamacare, individuals were free to purchase very low cost “catastrophic” insurance. That went away when Obamacare mandated minimum levels (and the costs to individuals skyrocketed… sort of like the costs to build a new coal power plant).

“Obviously, you were never involved in employer paid health care.”

bruce, obviously you are wrong. nothing i stated is incorrect. employer based health care, especially for large self insured companies, is exactly what most conservatives rail against with obamacare. young subsidize old-no variation in price. there is basically a mandate and penalty for not insuring. i have yet to encounter a company that reimbursed me for the premium coverage (i.e. benefit) if i opt out. so if i opt out, my salary is not adjusted higher. effectively, i am forced to pay my share of the premium to receive my “benefit”. small businesses may be better at this, because they do not self insure. my first job was with a small firm, but i do not recall what options i had for opting out. and finally, you typically have little choice in the insurance policy available to you. this is chosen by your employer.

bruce, if you have issues with obamacare, you should have the same issues with employer based health insurance.

baffling,

I shouldn’t have to do simple research for you, but here is an example of the opt-out pre-Obamacare feature: https://www.thestreet.com/story/13339782/1/why-employees-are-skipping-their-company-s-health-insurance.html

“Rejecting coverage from a company used to mean extra cash for the employee. Before the Affordable Care Act was passed, some employers chose to offer employees a general “opt-out credit” which provided perhaps $250 in monthly taxable compensation to employees who were eligible for benefits and waived the medical plan, he said. The credit was often paid as taxable cash during each pay period. These reimbursement arrangements subsided over time.”

And this: http://www.teambim.com/blog/are-opt-outs-on-the-way-out/

“Opt-out payments or cash in lieu of benefits have been a staple in the employee benefits industry for many years. Employers offer individuals who are eligible to enroll in their group health plan a sum of money, typically paid monthly, to those who waive enrollment in the group health plan. Employers who offer group health plans often use opt-out payments to share the savings they receive when an employee chooses not to enroll in the benefits offered.”

As I said before, the problem now under Obamacare is that these employees must then buy their own insurance with taxable funds or pay a “tax” fine. So the marketplace is twisted inside out for the sake of 6 or 7 percent of the population.

bruce, i should not have to do this work for you

“Before the Affordable Care Act was passed, SOME employers chose to offer employees a general “opt-out credit”

you could consider this anecdotal evidence, especially from thestreet.com. i provided the same. I have worked for three large firms, my wife two, and none of them offered salary in place of my opt out benefit. None. This is probably pretty representative of the nation as a whole for the decade prior to the ACA, as it applied to several firms in large cities around the country. At least for large firms, as i stated in the previous comment. and for the firms that actually do provide an opt-out, my guess is none of the bonus was close to the firm’s share of the insurance policy. you still get a pay cut. i know you could then go out and buy your own policy, but i would imagine the net result is a worker with less total compensation and weaker insurance policy than otherwise available to them.

“the problem now under Obamacare is that these employees must then buy their own insurance with taxable funds or pay a “tax” fine.”

again, most of these folks were paying a fine prior to the aca, if they opted out. in those cases, it was simply a fine paid to their employer for not accepting a benefit they had to purchase.

PeakTrader I agree that some regulations increase costs and constrict the supply of healthcare. The requirement that all doctors must do their residency in a US hospital is a case in point…but that’s an AMA requirement that the GOP seems to think is just fine. And allowing the govt to leverage its buying power with Big Pharma is another example of low hanging fruit. But again, it’s the GOP who is standing in the way of that reform. The GOP likes to talk about health insurance competition across state lines. At first blush this sounds like a great idea. And it’s an idea that Obama wanted early on; however, healthcare economists have known for 30 years why that’s a bad idea and why it would actually increase costs, so Obama dropped it. (Aside: if you don’t know why competition across state lines will increase costs, then you probably don’t have any business posting about Obamacare and the GOP plan. It’s one of those “tests” that quickly identifies who knows their stuff and who doesn’t. And since Paul Ryan keeps blathering about it, he clearly does not know his stuff.)

No one would deliberately design a health insurance scheme like the one we have today. Employer based health insurance is a terrible idea. But we have to live with a certain amount of path dependence. We are where we are. Given where we are there are only four options available. The first option is to ditch the goal of affordable universal access to health insurance. If you don’t believe in universal access, then that’s fine. It’s an immoral position, but at least it’s coherent. The second option is single provider; i.e., the kind of health coverage we give to soldiers. My niece is a surgeon at Walter Reed…and Walter Reed is a single provider activity. The third option is single payer. Medicare is a single payer approach. This is probably the most cost effective way to go and if Obamacare 1.0 and 2.0 (or as Krugman calls it “0.5”) collapse, then the next stop will be universal Medicare. The fourth option is something that looks a lot like Obamacare; i.e., universal access funded by a mandate for the young and healthy along with a generous subsidy for those who cannot afford the mandate. The GOP plan is a house of cards. The plan wants all of the good stuff without having to pay for it. The GOP plan is incoherent and will lead to a worst-of-all-possible worlds outcome. The individual market will collapse because without a mandate insurers will have to assume anyone signing up for private insurance must be a high risk. And employer provided insurance will also get scaled back as companies realize the GOP plan actually grants all kinds of tax advantages for companies that offload insurance. And that’s just the tip of the iceberg. It’s a mess.

Deregulation and competition are needed to make health care affordable for consumers and taxpayers.

Most people can’t afford expensive luxury goods.

2slug,

Holding up Walter Reed in the VA system as an example of what should be our health care goal is a good indication that you completely fail to understand the terrible bureaucracy and system-oriented nature (as opposed to patient-oriented) of that government-run entity. My father, as a WWII veteran, trusted the VA to provide for his medical needs when he was in his 70s. The level of care was atrocious; I know because he had to come to live with us and my wife had to take him to his “appointments” where he never saw the same doctor twice and an 8:00am appointment meant he got a number like a deli with the 200 other veterans who showed up at 8:00. He ultimately died because the VA did not provide the normal follow-up treatment for his cancer which allowed it to return and spread.

No, there is a distinct difference between paying for and providing health care. Government systems have unique and often foolish regulations such as Medicare’s you can’t get an ultrasound scan and then have your doctor give you the diagnosis while you are there, even if you are getting the scan done at your doctor’s facility (my wife just went through this which required an extra round trip of 25 miles and two hours of time). It may be convenient for the bureaucracy, but it’s not for the patient.

I guess it boils down to your expectations of a medical system. Medicaid can provide coverage, but doctors can and are refusing to see Medicaid patients. The same is true for Medicare in many instances, but not as often as Medicaid. A VA government-paid, government-provided system has proven for decades that it is a train wreck.

But in the words of Star Trek’s Mr. Spock and the ACA’s mission, “The needs of the few outweigh the needs of the many.” Mission accomplished.

“Deregulation”…

the cut and paste response from peak and others of similar mindset. mindless ideology. from the set that brought us the financial crisis.

Jeffrey J. Brown: “In my opinion, the Swiss have the best combination of private and public health care.”

Interesting that you single out the Swiss system because it is precisely the same as Obamacare except that it has higher taxes allowing better subsidies and absolute compulsory insurance coverage. Every single person living in Switzerland for more than 90 days, starting at birth, must purchase an insurance plan that complies with required coverage limits. If you don’t, the government will assign you to a plan and bill your for it. If you don’t pay, they take it out of your paycheck.

So to turn Obamacare into the Swiss plan all you need to do is increase taxes, provide better subsidies and strengthen the insurance mandate. Obamacare is already most of the way there and just requires some minor improvements.

As for costs, while the Swiss system uses private insurance, government also strictly regulates provider fees for services and pharmaceuticals.

I agree that we need a stronger insurance mandate; it’s the only realistic way to have a ban on pre-existing conditions exclusions.

Note that based on 2014 data, Switzerland spent 11.7% of GDP on healthcare (and basically have universal coverage with very good health statistics), versus 17.1% for the US:

http://data.worldbank.org/indicator/SH.XPD.TOTL.ZS

Note that another interesting aspect Switzerland is that only about 30% of high school students are on an academic track. 70% are on a vocational track and graduate with basic job skills. They can then go on to higher levels of vocational training.

My premise is that the Swiss seem to have the most rational approach to a variety of societal issues, without being too burdened with Political Correctness.

Health insurance premiums have skyrocketed, since the 1960s, along with health care costs. We need to lower health care costs before mandating buying health insurance, which can be done along with buying auto insurance. Otherwise, consumers will have less discretionary income for other goods & services.

“We need to lower health care costs”

now that sounds like a socialist! free markets set the price of health care since the 1960’s.

Note that based on 2014 data, Switzerland spent 11.7% of GDP on healthcare (and basically have universal coverage with very good health statistics), versus 17.1% for the US

Switzerland has a government board that strictly controls the cost of provider fees and pharmaceuticals. The salaries of doctors are much less than the U.S. particularly for specialists, about 50% lower. There are also about one-third more doctors per 1000 people which also holds down costs.

None of these changes are likely to get past a Republican congress.

The U.S. has many specialists that created enormous value for the rest of the world. Why give that up?

but the increase in specialists has produced a lack of general practitioners. this has driven up health care costs. you want to drop costs, get more general practitioners.

So, you want to order specialists they can’t do that work and have to do something else. Typical – another mandate.

no, a reality. YOU want lower health care costs. one driver is the lack of general practitioners vs specialists. this is the result of larger salaries for the specialists. you could create more internal medicine and less specialists/fellowship training programs to correct the problem. i am not ordering specialists to do different work-that is your wording hack. i simply train fewer specialists and more general practitioners. you want lower costs, here is one solution, or part of a solution. why is this a problem?

Baffling, you said the increase in specialists produced a lack of general practitioners. Sounds like a zero sum game.

And, then you want fewer specialists trained. Sounds like a mandate. You’re hacking your own words.

Fewer specialists mean they’ll do something else.

The U.S. has the best health care in the world. Switzerland bought the second largest biotech firm in the world from the U.S., and foreign countries have benefited enormously from advancements in U.S. health care.

The U.S. would be #1 in the world in life expectancy if we didn’t define infant mortality rates much stricter than other countries, excluded the black population, and adjusted for auto accidents and murder rates.

“The U.S. has the best record for five-year survival rates for six different cancers. In some cases the differences are huge: 81.2% in the U.S. for prostate cancer vs. 41% in Denmark and 47.4% in Italy; 61.7% in the U.S. for colon cancer vs. 39.2% in Denmark; 12% in the U.S. for lung cancer vs. 5.6% in Denmark.

Also interesting is the fact that there is often a significant difference between white and black cancer survival rates in the U.S., e.g. prostate cancer – 82.7% for whites vs. 69.2% for blacks. But even in that case, the five-year survival rate for blacks (69.2%) is still higher than for all European countries except Switzerland.”

There’s enormous waste in U.S. health care:

http://www.healthaffairs.org/healthpolicybriefs/brief.php?brief_id=82

PeakTrader: “The U.S. has the best record for five-year survival rates for six different cancers. In some cases the differences are huge: 81.2% in the U.S. for prostate cancer vs. 41% in Denmark and 47.4% in Italy”

Always with the prostate cancer from the wingnuts. It’s a favorite theme. Turns out that most cases of prostate cancer are very slow progressing and typically people die of other causes before the prostate cancer becomes fatal.

The five year survival rate isn’t because of superior treatment. It’s just that in the U.S. prostate cancer is often diagnosed years earlier. Most people survive prostate cancer for longer than five years even with no treatment. So early testing provides a better “survival rate” number. The better understanding today is that prostate cancer is over-diagnosed and over-treated in the U.S., causing much health harm through side effects and much unnecessary spending.

Same with other cancer survival rates. Earlier diagnosis simply improves the five-year survival rate even if you were to do nothing.

PeakTrader: “The U.S. would be #1 in the world in life expectancy if we didn’t define infant mortality rates much stricter than other countries, excluded the black population, and adjusted for auto accidents and murder rates.”

More BS from PeakTrader. The OECD shows that life expectancy at age 65 is much higher in other developed countries than the U.S. That eliminates your BS about infant mortality, auto accidents and murder rates. Despite all the expensive technology and treatment in the U.S., elderly people live longer in other countries.

PeakTrader: “excluded the black population”

Yeah, because black people just don’t count in the U.S as real people. Typical racist BS from conservatives.

Conservatives as usual, dumber than dirt.

Joseph, over the past 20 years, cancer treatments have made substantial improvements. Anyone who invested in biotech firms would know that. Also:

“American university-affiliated hospitals lead the world in research and development. From life-saving medications developed by U.S. companies to procedures such as heart stents, many of the world’s newest drugs and technologies are developed right here.”

Adjusting life expectancy for other factors shows the U.S. is #1 in the world. It’s not BS.

And, so, citing that the black population don’t benefit as much as the non-black population in cancer results makes someone a racist? Talk about dumber than dirt.

“And, so, citing that the black population don’t benefit as much as the non-black population in cancer results makes someone a racist?”

no. but excluding 12% of the population so that you can provide evidence of greater life expectancy shows an ignorant and callous view of your fellow citizens. we are promoting policies that include african americans in the health care discussion, to improve their health metrics. your approach is simply to wish them away and not deal with the problem.

the proposed health care plan will take many people, especially the poor and african americans, off the insurance roles. and this will result in an improved life expectancy among the poor and african american? for peak trader, I guess it will be a win because we will not count those folks when we measure life expectancy. our metric will be on those that actually have health insurance-and the numbers will probably improve.

Another dumber than dirt conclusion. What it means is some European countries have small black populations and that should be controlled for an apples to apples comparison.

no peak, you want to exclude the black population because they bring down the life expectancy to a number you are not happy with. that population does exist. so from a policy perspective, we have a policy in the us that is not adequately supporting the entire population, but a specific subgroup of that population. obviously its a great situation for those in the benefit-why would you want to change it? not so great for other subgroups of the population.

You can always exclude the unwanted populations from healthcare and “decrease the surplus population” which will make Peak and Scrooge very, very happy.