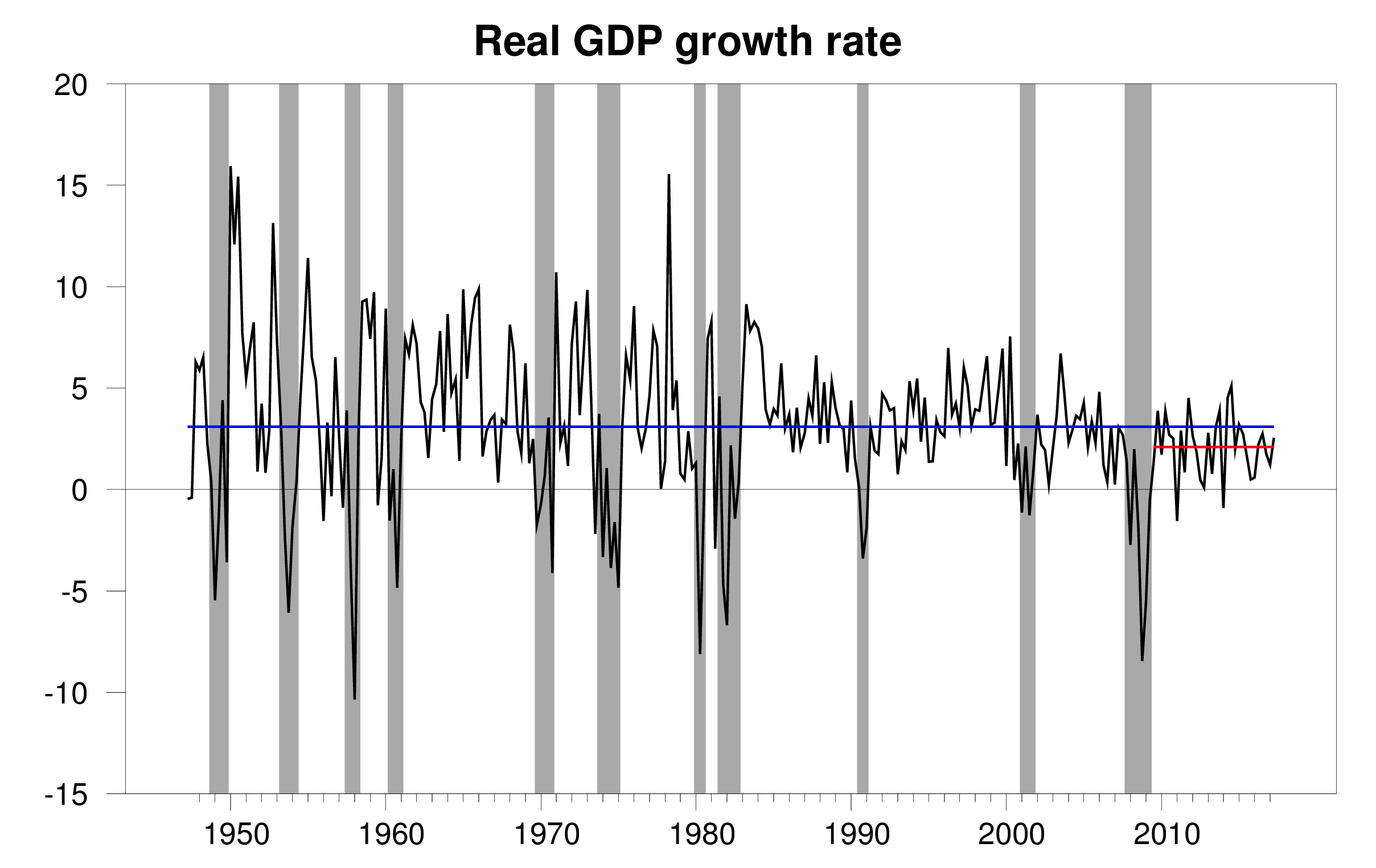

The Bureau of Economic Analysis announced today that U.S. real GDP grew at a 2.6% annual rate in the second quarter. That is below the long-term historical average of 3.1%, but better than the 2.1% we’ve seen on average since the Great Recession ended in 2009.

Real GDP growth at an annual rate, 1947:Q2-2017:Q2, with the 1947-2017 historical average (3.1%) in blue and post-Great-Recession average (2.1%) in red.

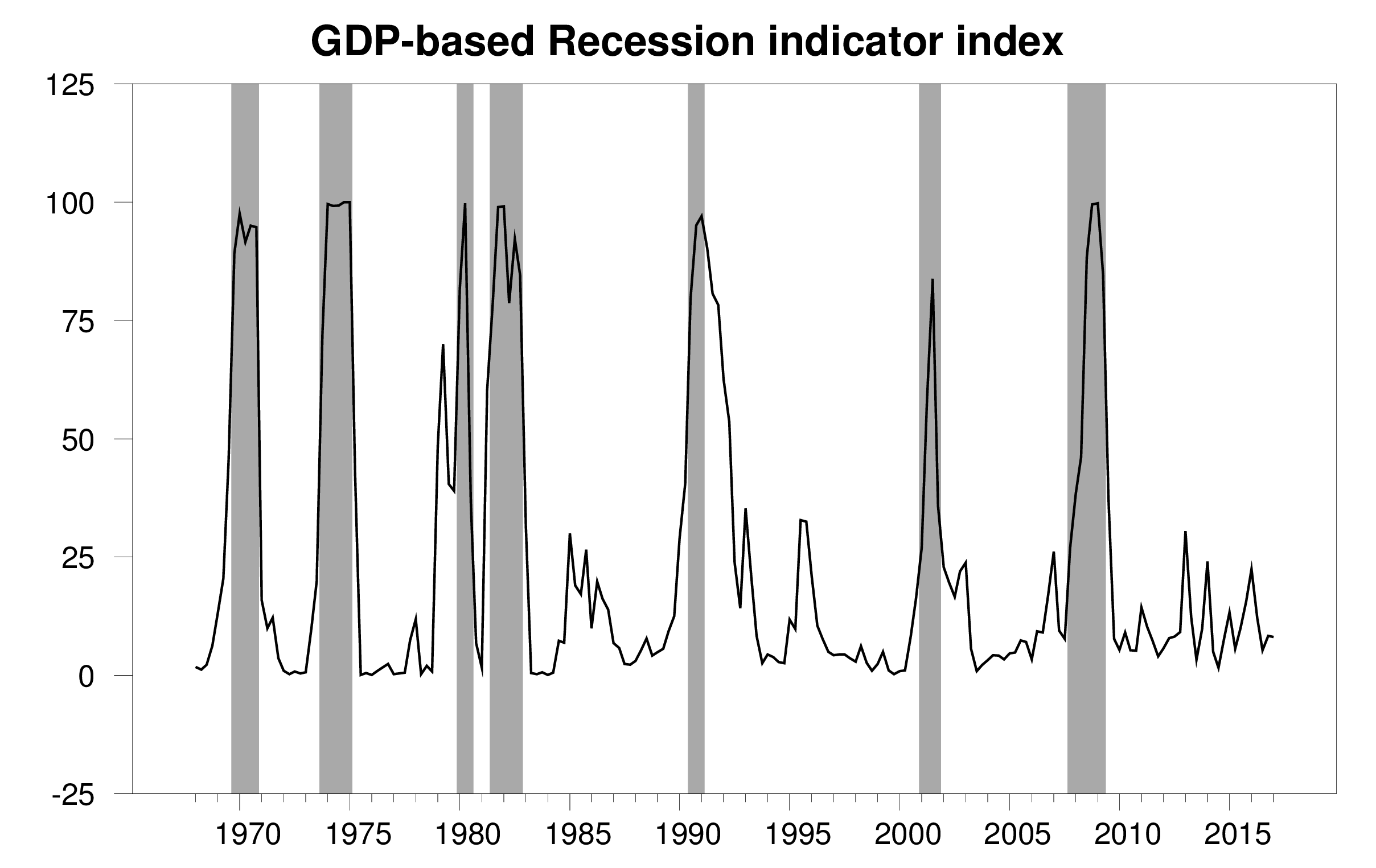

This helped our Econbrowser Recession Indicator Index to ease down to 8.2%, confirming the U.S. remains steadily in the expansion phase of the business cycle.

GDP-based recession indicator index. The plotted value for each date is based solely on information as it would have been publicly available and reported as of one quarter after the indicated date, with 2017:Q1 the last date shown on the graph. Shaded regions represent the NBER’s dates for recessions, which dates were not used in any way in constructing the index, and which were sometimes not reported until two years after the date.

Solid growth in consumption spending was the main driver, with increases in nonresidential fixed investment also making a solid contribution.

But that last number doesn’t look as robust as one might have hoped. Nominal fixed investment (at an annual rate) was up $36 billion in the second quarter over the first. Nineteen billion (more than half) of that came from mining exploration, shafts, and wells. A resurgence in U.S. oil drilling is showing up in GDP.

Nominal expenditures on private fixed nonresidential structures investment in mining exploration, shafts, and wells, in billions of dollars seasonally adjusted at an annual rate. Data source: BEA Table 5.3.5..

And that happened with many of the key players in fracking still cash-flow negative [1], [2]. Should we expect further big increases in oil-related investment from the 2017:Q2 levels? I don’t.

Professor Hamilton,

I notice that the GDP price index Q/Q change SAAR was reported at 1.0%. I also notice that on Tuesday, July 25, the WSJ reported the CPI for Mexico at an annual rate of 6.28% and core CPI at an annual rate of 4.92%.

In a future post, I wonder if you would discuss why Mexico’s inflation is above the current rates in the US and EU? Can we take a lesson from Mexico to get the US rate up to the Fed’s current desired 2.0% level?

If it wasn’t for the fracking boom, the depression would be even worse.

https://www.advisorperspectives.com/dshort/updates/2017/07/28/q2-real-gdp-per-capita-1-95-versus-the-2-57-headline-real-gdp

I can understand a slightly slower growth rate from shifting demographics. However, we should’ve rebounded much more strongly from the severe recession to close almost all of the output gap by the end of 2011. It seems, growth will slow, ceteris paribus, after the last of the Baby-Boomers, born between 1946-64, leave prime age, 35-54, in 2018. I expect a large middle class tax cut to boost consumption and reaching full employment to boost investment.

Economic depressions cause population growth rates to fall. The Great Depression cut the population growth rate more than half compared to the 1920s. The Great Recession caused the population growth rate to fall from roughly 0.95% to 0.75% per year.

http://www.multpl.com/us-population-growth-rate/table/by-year

Yes, that’s right. US population growth rates, before and after the Great Depression, were quite high, around 1.7% per annum.

During the Great Depression, 1931-1941. the US averaged 0.73% per annum. From 2009 (again, with a lag of a year after the start of the Great Recession) until 2017, the growth rate has averaged 0.75% — essentially the same as the Great Depression.

By historical precedent, the current growth rate lasts until 2019, and recovers to around 1%, perhaps a bit less, in 2020.

I would note that the growth rate recovered to over 1% in 1942, immediately after the attack on Pearl Harbor, and stayed above 1% until 1968, with an average of 1.53% in the 1942-1968 stretch.

I’d just note there was a world war in there.

World population growth:

https://ourworldindata.org/wp-content/uploads/2013/05/updated-World-Population-Growth-1750-2100.png

Looking at real government purchases and it is almost exactly where it was in 2016QI. Fiscal austerity continues – alas.

Janet Yellen:

“Increased business sales would almost certainly raise the productive capacity of the economy by encouraging additional capital spending, especially if accompanied by reduced uncertainty about future prospects. In addition, a tight labor market might draw in potential workers who would otherwise sit on the sidelines and encourage job-to-job transitions that could also lead to more-efficient–and, hence, more-productive–job matches. Finally, albeit more speculatively, strong demand could potentially yield significant productivity gains by, among other things, prompting higher levels of research and development spending and increasing the incentives to start new, innovative businesses.”

The rate of growth in the Obama years is especially poor when you consider that the economy was coming out of recession (therefore from more spare capacity).

I think stocks and investments attempt to be forward looking. The huge hand of government (both actions and the threat of actions) was something that weighed on the economy. The Trump boom (maybe even the non Hillary boom) is a contrast. It also is showing expectations.

In addition, I think the Wall Street bailout (both Democrats and centrist Republicans guilty, but far right and far left opposed) weighed on the economy because it showed a long term danger of moral hazard. Not just the event itself but what it implies about the change in free markets. We would have been MUCH better biting the bullet, letting counterparties eat their counterparty risk and moving on.

TARP was needed, because of government policies in the housing market and too-big-to-fail. Given the massive stimulus of monetary policy and targeted fiscal policy, along with TARP, why was the recovery so weak? Again, because of government policies. There were too many anti-growth policies, e.g. too little government refunding for consumers (after the huge trade deficits in the 2000s), Obamacare, Dodd-Frank, regulations reaching over $10,000 per worker, the build-up of student debt, etc., with the pro-growth policies.

Some investors appear to believe that US funds and banks will continue to throw money at oil drilling in the USA because of the apparent growth prospects despite the overall poor financial results.

That said, the newness and promise of tight oil formation technology appears to be fading. Slowly.

At some point, financiers and investors should fully grasp how a good inventory of drilled but uncompleted (DUC) wells can quickly ramp up production on modest oil price increases. At some point, the cost of capital for the sector should become noticeably more expensive. When is another question.

Near term, if benchmark oil gets close to US$60/bbl in the near future, I fully expect US oil production to ramp up relatively quickly (again). To the point of moderating oil price increases, if not reversing them. US tight oil producers have become the de facto swing producer in the global market.

Given social attitudes surrounding oil and ‘energy independence’, perhaps it is no surprise that American patriots flood the sector with capital?

Foreigners are also investing:

https://www.eia.gov/todayinenergy/detail.php?id=10711

“We would have been MUCH better biting the bullet, letting counterparties eat their counterparty risk and moving on.”

And after Lehman and AIG had defaulted during the financial crisis, would Goldman or Morgan or Citi or (name a financial institution) still have been solvent and able to cover their own risks and counterparty deals? You do understand how much risk AIG itself had put into the system? There would not have been any “moving on” from that situation. Such talk is naive or a misunderstanding of the problems of that moment.

Would rather say, Trump really needs a war right now to solve his most pressing problems. China would benefit from a US – DPRK confrontation and is in a position to facilitate the conflict.

Imagine if the DPRK, armed with nuclear weapons, subsequently had a new leader with no experience in politics, possibly from a real estate background, and a history of intemperate behavior. It’s too frightening to contemplate.

More outperformance from WI vs MN.

http://www.businessinsider.com/gdp-growth-state-map-q1-2017-2017-7

It’s to China’s advantage, along with Russia and Iran, to keep feeding North Korea, making it stronger, and eventually having it possess dozens of nuclear missiles aimed at the U.S., South Korea, Japan, etc.. We should’ve allowed General MacArthur to finish the war.

Professor Hamilton,

While trying to use a Markov Switching model to match your recession indicator model, I seem to be having some trouble getting my probabilities of recession to match yours. Looking at your chart, I assumed that you used data from 1968Q1 to 2017Q1(as you mention). I also assumed that you used the continuous quarterly growth of the real GDP and “c” for the Markov model and no AR factors. Some of my probabilities match yours and others do not match yours. For example my 2000 probability estimate of recession is only about 12% and my 2017Q1 estimate is about 4.8%.

Any suggestions would be appreciated.

Thanks

AS: Please note that this is a real-time index calculated at each data using only data for that date as it was reported at that date. The numbers reported today for GDP in 2001 are not the same as the numbers for GDP for 2001 that were reported in 2001. For any indicated date, you need to download data as it was actually reported at that date (you can get such real-time data from Alfred). For example, to get the number for 2001:Q4 you take the dataset from 1947:Q1 through 2002:Q1 as reported as of the date of the first (advance) release of the 2002:Q1 GDP.

Thank you. If I understand correctly, it seems very tedious at this point to recover all the original data points. Now that you mention the real time data, I seem to recall that you posted your original data on Econbrowser in an Excel file in a post a couple years ago.

Professor Hamilton,

I apologize. I re-read a prior blog from 2016 and see that I asked you similar questions. This time, I copied the comments and put them in a file, so I don’t ask the same questions again. Using your comments from 2016, I am able to calculate the 2017Q1 smoothed recession probability of 8.2% to agree with your calculation.

I am curious as to why an AR(1) factor is not appropriate, since the residuals appear to be autocorrelated.

Thanks again.

So here is our fearless leader talking about GDP. I kid you not. This is a direct quote from a Trump interview:

So I deal with foreign countries, and despite what you may read I have unbelievable relationships with all of the foreign leaders. They like me. I like them. You know, it’s amazing. So I’ll call, like, major – major countries, and I’ll be dealing with the prime minister or the president. And I’ll say, how are you doing? Oh, don’t know, don’t know, not well, Mr. President, not well. I said, well, what’s the problem? Oh, GDP 9 percent, not well. And I’m saying to myself, here we are at like 1 percent, dying, and they’re at 9 percent and they’re unhappy. So, you know, and these are like countries, you know, fairly large, like 300 million people. You know, a lot of people say – they say, well, but the United States is large. And then you call places like Malaysia, Indonesia, and you say, you know, how many people do you have? And it’s pretty amazing how many people they have. So China’s going to be at 7 or 8 percent, and they have a billion-five, right? So we should do really well.

It would be hilarious if it wasn’t so frightening, the ignorance of this president. He’s bragging like a six-year old about his “amazing relationships”. “Major, major countries .. you know, fairly large like 300 million people.

You know, there are exactly three countries with more than 300 million people and one of them is the U.S, so why so coy? He thinks he is fooling us? And Malaysia and Indonesia certainly aren’t among them. In fact Malaysia has only a tenth as many. And China, not a billion-five — actually less than a billion-four. What is up with Republicans (like Stephen Moore) and their propensity to always exaggerate even the most indisputable facts?

This narcissist talks like a small child. He is obviously suffering from dementia and Republicans continue to pretend not to see.

At least those who pretend not to see feel a little chagrin. Millions of Americans see him just the way he is and want him as our President.