Today, we are fortunate to present a guest contribution written by Ashoka Mody, Charles and Marie Visiting Professor in International Economic Policy, Woodrow Wilson School, Princeton University. Previously, he was Deputy Director in the International Monetary Fund’s Research and European Departments.

It seems a puzzle why, at its March 7 meeting, the European Central Bank indulged in sedate tinkering despite the mounting risk of a damaging eurozone recession. The puzzle has a simple answer. The ECB has reached both political and technical limits. It offers mainly words, in particular a recurring promise to aggressively use its “instruments” if economic weakness “persists.” Left with no options, the ECB must define the problem as lying in the future, not in the present. Hence, always behind the curve, it hemorrhages credibility.

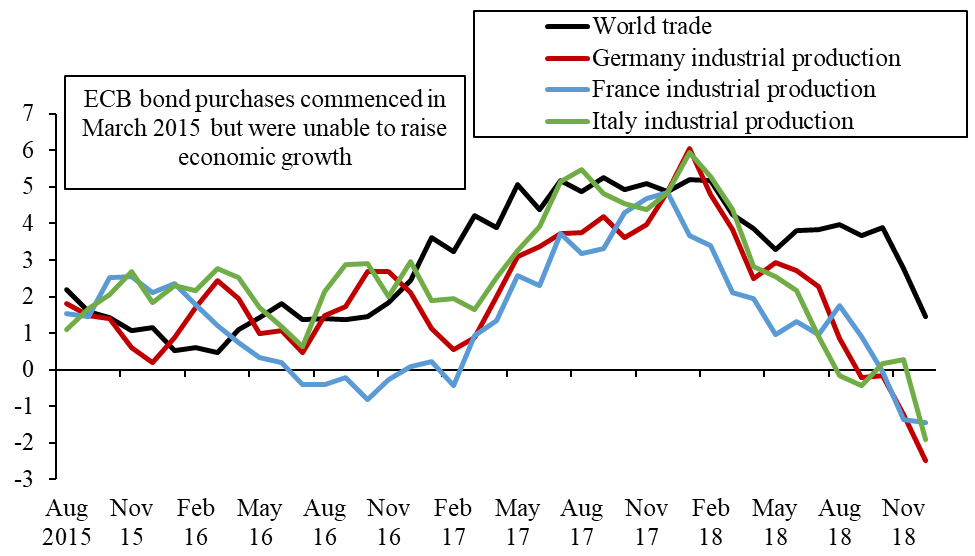

A rapid economic slowdown was already evident when the ECB’s Governing Council met on September 12-13 last year. World trade growth had slowed since the start of the year—and eurozone growth, perennially dependent on international trade, had predictably decelerated. The slowdown was sharpest in the three largest eurozone economies, but the growth momentum was petering out everywhere. The evidence was not lost on the Governing Council, which coyly noted that risks to economic growth had “tilted to the downside.”

Figure 1: Eurozone economic growth marches to the drum of global trade (3-month moving averages).

Thus began the latest cycle of kicking the can down the road. The Governing Council’s members expressed confidence that the “underlying” economy remained strong. They persuaded themselves that “broad-based expansion” was set to continue, and “inflationary pressures” would soon defeat the deflationary tendencies. Thus ignoring the “downside risks,” the Council acted on its optimistic assessment. The decision: asset purchases under the quantitative easing (QE) program, initiated to reduce long-term interest rates, would end in December.

True to that promise, the ECB ended QE in December, thus tightening monetary policy just as recession became a real threat.

The bad news kept coming. By early this year, Italy and even Germany seemed to be sinking into recession. At their January 23-24 meeting, members of the Governing Council said they were surprised. Growth indicators, they now noted, had taken a turn for the worse and “the near-term growth momentum would likely be weaker than previously anticipated.”

The poorer outlook did not justify easier monetary policy, the Council concluded. Such a change in direction was “premature.”

No, such denial and delays are not standard operating procedure for central banks.

U.S. economic growth also slowed in the second half of 2018, especially in the fourth quarter. Even so, U.S. GDP growth, at a more than 2 percent annual rate, was significantly higher than the less than 1 percent growth pace in the eurozone. And the possibility of a recession in the United States seemed remote.

Yet, the Federal Open Market Committee (FOMC), recognizing the economic deceleration, dropped its plan for “further gradual increases” in its policy interest rate. FOMC members also concluded that selling the assets acquired through QE would push interest rates up and therefore they indicated that they might stop the sale of those assets. In late February, in his testimony to the House Financial Services Committee, Fed chair Jay Powell reiterated that the drawdown of the Fed’s assets would likely end by year-end.

The Fed’s easing of monetary policy was greeted by a rise in global stock prices, reinforcing the Fed’s claim as the world’s central bank.

The Fed remains effective because it operates on the risk management principle. As Chairman Alan Greenspan famously said, the time to take action is when an elevator is in free fall, not after it has crashed. The Fed’s January decision was very much in that spirit. It chose to ease monetary policy stance from a position of relative strength. The contrast with the ECB was striking, which simultaneously tightened despite facing much bleaker economic prospects.

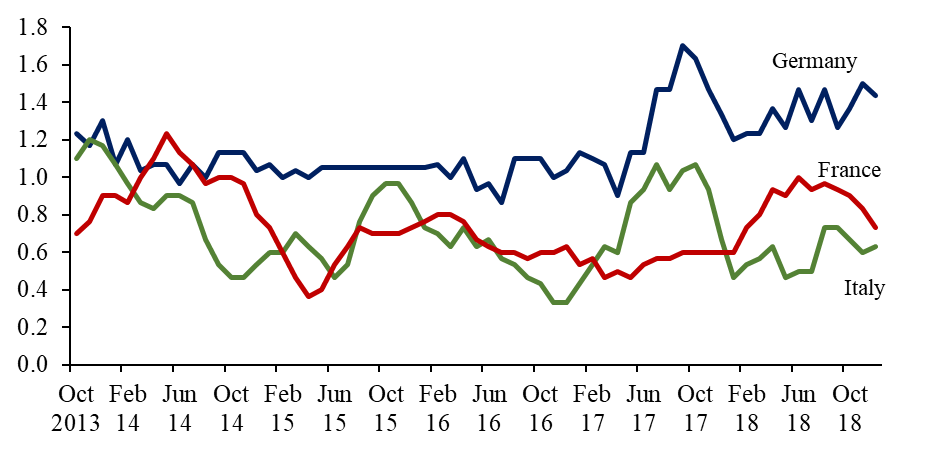

The ECB, riven by conflicting national interests, always acts late, often too late. The northern eurozone countries, with their higher inflation and growth rates, perceive less need for monetary stimulus and so oppose ECB measures to reduce interest rates. They held back eurozone QE in the crucial 2012-2014 years, when large parts of the eurozone—especially Italy and France—fell into a recession and a deflationary psychology. Italy’s “lowflation,” in particular, has kept its real (interest-adjusted) inflation over 2 percent, which is much too high for a country with zero productivity growth.

Figure 2: Italy and France in lowflation trap (Core inflation rates, 3-month moving averages) Note: For Germany, an unusual spike in inflation from June to December 2015 has been omitted.

Now, with mounting evidence of impending recession, the ECB is caught in political and technical traps. Bundesbank president and ECB Governing Council member Jens Weidmann has continued to oppose monetary stimulus. In late January, he called for monetary policy “normalization” by selling assets purchased under QE and “phasing out ultra-low interest rates.” On February 27, the same day as the Fed’s Powell repeated his call for patience in raising rates, the Bundesbank’s annual report warned that waiting to raise rates created “risks” and adverse “side effects.”

Held back by such opposition to more stimulus, the ECB has continued to offer its customary cheap talk. Yes, all policymakers rely on cheap talk. But stymied in its actions, the ECB relies particularly heavily on its words. Asked after the January monetary policy meeting how the ECB intends to fight recessionary and deflationary tendencies, ECB president Mario Draghi’s gave his standard response. Domestic economic and, especially, financial conditions, he said, remain “very favorable.” In any case, “We have lots of instruments and we stand ready to adjust them or use them.” Draghi has used these same words since November 2013, when the eurozone began to slip into deflationary psychology. This pattern of repeated denials, delays, and half-measures is the antithesis of risk management.

And because the eventual scale of actions do not match the words, the ECB has steadily lost credibility. Predictions of an imminent rise in inflation have proven false repeatedly. Italy and France are stuck in lowflation despite modest economic recovery in 2017. Businesses and households in these two countries act on the belief that inflation will not rise anytime soon, which causes them to postpone purchases, which keeps inflation low. Spanish inflation, after a brief spurt in 2016 and 2017, is sliding into lowflation territory. The ECB provides little discernible stimulus to economic growth: the timing of eurozone growth coincides with global trade growth, not with ECB monetary policy.

Having frittered away its firepower, the ECB can now do little. Restarting QE will face extraordinary political obstacles. After all, as Draghi underscored, the ECB has already purchased 25 percent of eligible eurozone government bonds. Northern countries are not anxious to buy more bonds of countries that may eventually not repay their debts.

With little choice at the Governing Council’s March 7 meeting, Draghi announced that the ECB would extend cheap liquidity to banks through its much-touted targeted long-term refinancing operations (TLTROs). In past iterations, the weakest Italian and Spanish banks have gobbled up large chunks of such liquidity. Under new regulatory requirements, these banks will require larger liquidity buffers, which will likely prove too costly to build from market sources.

Thus, in effect, the ECB will continue to subsidize banks’ lending. Not surprisingly, French central bank chief François Villeroy de Galhau and his Finnish counterpart Olli Rehn are worried. Subsidizing the lending of Italian and Spanish banks, they recently emphasized, is not monetary policy. The subsidies prop up the weak banks and their zombie borrowers. Weidmann is right that prolonged “ultra-accommodative” monetary policy can have troubling “risks and side effects.”

Moreover, TLTROs are an odd tool to deploy with the economy slowing down and banks, especially in Italy and Spain, anticipating reduced credit demand. This is especially so since the TLTROs will kick in only later this year, by when the recession will likely be deeper and the credit demand even less.

The ECB has also promised it will not raise its policy interest rates until the end of the year. That is an empty promise. Financial markets know that the ECB dare not raise interest rates in any foreseeable future.

For the rest, the Governing Council is still not persuaded that the downturn could “persist.” Members believe that the eurozone economy will hum again later in the year because Chinese growth will pick up, trade disputes will fade, and Germany’s auto industry will surely rev up again. In any case, Draghi repeated, the ECB has “lots of instruments and we stand ready to adjust them or use them according to the contingency that is produced.” What instruments?

Meanwhile, the latest Chinese economic stimulus can only modestly delay an inevitable slowdown from the country’s historically unprecedented stretch of high growth. Even Chinese authorities project slower growth next year. The eurozone’s primary driver—world trade growth—is set to slow in tandem. Poorer trade prospects will weigh down the apparently favorable domestic conditions. Consumption and investment will slide. As growth rates fall and some countries linger in recession, financial vulnerabilities will rise and, eventually, threaten to spiral out of control. Tremors will spread from the Italian fault line.

Long-time ECB analysts have welcomed the Governing Council’s March 7 decisions, but the more discerning financial markets have barely took note. Analysts have had their expectations beaten down by the ECB’s long-standing niggardly policy stance. They, therefore, are inclined to cheer any change that has a faint prospect of helping. Investors, in contrast, have their money at stake and recognize that they can expect little, if anything, from the ECB.

For the eurozone, a coordinated fiscal stimulus is the only option to prevent a long-drawn recession. Hence, not just to dodge the likely recession, which could morph into a crisis, but also to achieve more robust long-term growth, the eurozone needs a coordinated surge in spending that invests in the future. The rationale for such a policy course is reinforced by the economist Antonio Fatás’s warning: failure to counter recessions and crises causes unused resources to atrophy and, thus, weakens long-term growth potential.

But can eurozone authorities give up the encrusted identification of a good European with the practice of fiscal austerity? Make no mistake, aside from its jumble of words, the ECB has nothing else to offer going ahead. Relying on an ECB miracle and holding back a fiscal stimulus will inflict more wounds on Europe’s deeply scarred economics and politics.

This post written by Ashoka Mody.

Outstanding post by Professor Mody. Written like a true technocrat (in nothing but the best sense of that term).

Let it settle a little in my head some and then make an attempt at a comment to prove semi-worthiness of such a great blog post.

Interesting comments but a puzzle when one looks at interest rates across the major economies. Bloomberg’s reporting of 10-year government bond rates:

https://www.bloomberg.com/markets/rates-bonds

In the U.S., this rate is 2.62% while the German rate is only 0.07%. Yes I realized one can push this rate below zero (see Japan’s rate) and the long-term German government bond yield used to be zero. Just saying – maybe Europe needs to go full scale fiscal stimulus.

Never in history has there been a more inane economic policy than the ECB’s regime of negative interest rates! Europe’s goose is cooked. Mody’s post here is rock solid and quite meaty. The highlight is: For the eurozone, a coordinated fiscal stimulus is the only option to prevent a long-drawn recession. Economics students take note. No, no, no. You allow the system to purge. You will not hear this from your professors. But you can file it. And if you are amongst those who truly want to make a contribution with your advanced degree, go to the Mises.org website and research what Mises, von Hayek, Rothbard, and others of the Austrian school say about this.

There is mounting evidence that humans age mostly because natural waste elements and toxins do not get purged. They accumulate in the body and grind down the body’s marvelous life machinery thus shortening life. Mapping over to the economy, the precise term the great Austrian economists use for this is malinvestment. Malinvestment is akin to waste. Zombie firms are kept on life support by excessive credit turned to debt that monetary and fiscal policy always engender. Where’s the waste? Scarce resources locked up in the zombies, unable to move to the promising new entrepreneurial firms of the future. Classic Schumpeter, another Austrian. Hence cycle after cycle over the long-term the most important component of the economy – productivity growth – is slowly, slowly ground down. The Federal Reserve made the same mistake in this country. QE other than in the emergency months of the global financial system collapsing. No again. Certainly not QE2, QE3, Twist, and the coming QEs 4, 5, and 6.

The other necessary change (coming eventually) is to dissolve the euro. The North and the South are not culturally compatible and must go their separate ways. The longer this is put off, the more waste products will collect to hasten the end of the European half of Western Civilization. The sovereign debt of Greece is trading at yields almost identical to those in the US. Greece, a nation that will never be able to repay the principal and accumulating interest on its debt! A zombie nation on life support. Off the charts financial maldistribution. This creating real sector maldistribution not just in Greece but in the entire eurozone.

JBH: You forgot to mention “our precious bodily fluids” in your exposition.

I was trying to figure out how JBH got the idea Professor Mody was arguing for higher interest rates?? I’m also curious what he thinks central bankers are supposed to do when it’s their job to step in during a panic or immediately before a market panic when governments and U.S. legislators are really the only ones who can provide fiscal stimulus?? For example when President Obama and Democrats were trying to allow court judges the latitude to allow mortgage cramdowns and Republicans said “NO”, is Bernanke or the FOMC supposed to wave a magic wand??

Now it is a given that President Obama was extremely lazy in getting off his butt and soap-boxing, stumping, or cajoling American citizens to petition their representative lawmaker to enact the mortgage cramdowns. But as lazy as President Obama was in fighting for mortgage cramdowns, there’s not much doubt Obama would have saved up and accumulated enough energy to sign the law had it journeyed on his desk to sign.

Since JBH thinks higher rates are the answer for Europe, is JBH also arguing that the U.S. Federal Reserve should raise rates under donald trump?? Hayek, Mises and the “Austrian School” always attracts the looney tunes nutjobs doesn’t it?? I know Peter Schiff is a big Hayek guy, but he’s never explained how the federal government is supposed to balance the budget when people like his father skipped out on paying any taxes.

“Hayek, Mises and the “Austrian School” always attracts the looney tunes nutjobs doesn’t it??”

Well put – if JBH thinks Mody was arguing for higher interest rates maybe we should enroll him in a basic reading comprehension class.

@ Menzie

Not to force you to answer for all of JBH’s blatherings, but…….. Schumpeter was an Austrian (not talking nationalities here, but schools of thought)!?!?!?!?!?!?!?!

https://youtu.be/kKpU-KRYSLk?t=38

“Never in history has there been a more inane economic policy than the ECB’s regime of negative interest rates! ”

I see – raise interest rates so aggregate demand would be even weaker. Hey YEA – let’s make sure the Greek economy implodes. Sorry but I refuse the read the rest of your babble as your first sentence has won the dumbest comment of the year all by itself!

JBH Something may have been lost in the translation, or perhaps your expressed agreement with Prof. Mody was tongue-in-cheek, but it sure sounds like you badly misunderstood his argument.

humans age mostly because natural waste elements and toxins do not get purged.

Humans age because time only moves in one direction. In any event, humans are physical organisms; economies are institutional arrangements. You’re arguing from a very bad metaphor and it’s not at all convincing.

Mapping over to the economy, the precise term the great Austrian economists use for this is malinvestment. Malinvestment is akin to waste.

I’ve always wondered why a certain personality type is attracted to an economic model whose chief characteristic is a kind of inevitable thanatosian death wish in which “malinvestment” reaches its climax in economic collapse. A kind of economic version of Freud’s Civilization and Its Discontents. You probably sit around listening to Wagner’s Gotterdammerung.

Hence cycle after cycle over the long-term the most important component of the economy – productivity growth – is slowly, slowly ground down.

And in the mid-2000s those same “Austrians” used to blame “malinvestment” on the productivity growth of the 1990s. It seems that Austrians can never get their stories straight. The “Switching Theorem” debate was pretty conclusive evidence against the Austrian theory of capital. Instead they just babble magical incantations about “roundabout” and Ricardo Effects/concertina cycles, blah, blah, blah. Kaldor and Hayek agreed on an empirical way to test the concertina effect. Hayek lost the empirical argument. Get over it.

The North and the South are not culturally compatible and must go their separate ways.

You might be right that northern Europe and southern Europe should not be in the same currency union, but you’re right for the wrong reason. Cultural differences (whatever that means) have nothing to do with it.

2Slugs,

I agree that JBH’s post is simply gonzo, duly mocked by Menzie. But on Hayek and reswitching you should know that in his 1941 Pure Theory of Capital he figured out that capital theoretic paradoxes can happen and that “roundaboutness” cannot in general serve as the foundation for measuring aggregate capital. Yeah, weird.

2slugbaits: I understood the good professor’s guest contribution quite well. His recent book made clear he has an excellent grasp on what’s going on in the eurozone and why.

Humans age because time only moves in one direction.

First off, an economy is far more a network than an institutional arrangement. Secondly, as to your off the cuff quip about time. In Beat The Clock, time is an important parameter. In the aging of wine, it may well be the important causal variable. But time is a slender reed on which to hang a theory of human aging. In every moment, cosmic rays cause aging. It’s not the time that does it, it’s the effect of the rays. If you were able to ward off all proposed and still unknown causes of aging, who is to say how long a human could live? A close friend of the family is 104. Her life expectancy at birth was 57. What wisdom did she possess to achieve this precious thing? If par is 100, she’s batting 180. By analogy, I believe something similar can happen to the economy’s growth rate. By how much is an empirical question. But the only tool in your barren toolkit is monetary and fiscal policy. And you don’t even ask the question.

My purpose was to draw attention to this wholly overlooked aspect of the economy. I point to what I believe is the main cause of human aging, namely accumulated cellular waste products and ingested toxins not expelled from the organism. Therefore clogging it and playing havoc with life processes. As this line is rather astonishing when you first come upon it, and as humans are so integral to an economy – being its cells you might say – it came to me long ago that it has to be fruitful to think about clogged pipes in the economy as a source of obstruction to the economy’s rate of growth. It is face evident that there are many kinds of obstruction, not just malinvestment. Nor did I imply just malinvestment. Probably corruption is more damaging, though empirical studies of the corruption-growth connection are few and far between. And since there are no good or standard metrics for such things, economics simply turns a blind eye to blockages, impediments, and drains in its macro-modeling. In fact, as I said, mainstream economics doesn’t even entertain the question. All the reining paradigm knows how to do is throw money and fiscal stimulus at the problem. Which at some point due to the law of unintended consequences (e.g. massive debt burden) itself becomes an obstruction.

Cultural differences (whatever that means) have nothing to do with it.

If you don’t know the common sense meaning of cultural differences then you hardly have a leg to stand on in making a claim about them one way or another, do you? This is another error of logic on your part.

JBH In every moment, cosmic rays cause aging.

Right. I remember that Star Trek episode, “This Side of Paradise”. That’s the one in which the spores protected the colony on Omicron Seti III from the damaging effects of Berthold rays. I mostly remember it because a very hot Jill Ireland played Spock’s love interest. The spores restored human health and prevented aging and death.

https://en.wikipedia.org/wiki/This_Side_of_Paradise_(Star_Trek:_The_Original_Series)

mainstream economics doesn’t even entertain the question. All the reining paradigm knows how to do is throw money and fiscal stimulus at the problem.

Apparently you never took courses in microeconomics, welfare economics, labor economics, financial economics, agricultural economics, environmental economics, growth economics, international economics, etc. Economists have a lot more tools than just fiscal and monetary policies. But when dealing with the business cycle, fiscal and monetary policies are the principal tools.

If you don’t know the common sense meaning of cultural differences then you hardly have a leg to stand on

Well, I know there are regional differences in cuisine. And 500 years ago there were some differences between Reformation art and Catholic Counter-Reformation baroque art. Linguistically southern Europe speaks Latin based languages…but then again modern day Romanian is closer to ancient Latin than modern Italian, so maybe that’s not so definitive. Oh wait! I know. You don’t mean cultural differences, you really mean cultural stereotypes. Got it. Northern Europeans are hard working; southern Europeans are lazy. I am beginning to see why you like Trump so much.

Ok, sure. Enough econ. What’s more important? The 242,596 indictments that will rip the traitorous deep state to sheds. Then we’ll see who has enough bodily fluids, cosmic rays, and essential nutrients to survive. The lid is about to blown off soon. Or maybe later.

59–41 was the vote count on the blocking of the emergency declaration if anyone missed it. I forgot what was required to get the “super majority” but 59 isn’t enough. That means the measure passes, but then gets vetoed and goes to the courts—probably for a long time. I believe this cuts off donald trump from the purse strings to get the funding he is asking for on his children’s strength border partition. Anyone is welcome to correct me if I’m factually wrong here.

47 Democrats and 12 Republicans stood up for Article I of the Constitution. The 41 Senators who voted for King Donald I need to be removed from the Senate today.

Honestly, I am cynical enough at middle age to be genuinely surprised we got 12 Republicans on that. I didn’t expect any more than 1 or 2 representing moderate voting districts. Never would have guessed 12 would have some ethics there—including Rand Paul who I am generally not a fan of. Those 12 had some “backbone” and should be recognized for it, hopefully, affectionately in the history books as time wears on. It’s apt to be used against them in their next election.

But , yes, it would have been a great victory for America had they gotten the “super majority”. It speaks volumes about where we are in this country now. But in some aspect donald trump and the current situation is old news to me. I lost faith in the American electorate’s judgement when Reagan was elected, and have never really regained faith in American voters, except maybe for a few short naive moments when President Obama took the stage at Grant Park. I legitimately got a lump in my throat and became somewhat emotional, Which is extremely rare for me when not drinking liquor.

China steers US’s economy. US steers Japanese, European economies. Well actually, US steers China’s economy too — it makes monetary policy for it.

China’s CPI is the only “true” CPI worth watching which relentlessly dilates money & wealth. It was the “recipe” to re-float post-crisis. Europe would have no power over that.

Coming back to Europe, of course there’s this problem of fiscal union. Deeply it’s a political problem I believe: Northern countries vs Slavic countries. Mediterranean countries were the pawn and “had to” be sacrificed — my own read.

@ Zi Zi

Assuming you are Chinese, I keep wondering in my head what it feels like to be non-mainland Chinese and read your bull****. I think, I’m imagining it pretty accurately to as annoying as it in fact is.

Quantitatively, Europe’s CPI responds to Asian currencies, US interest rates structure, Asian current accounts — none at all to whatever Europe does.

I see that JBH and Zi Zi are in some competition for who can write the most meaningless babble here.

It would seem that the problem is not one for the ECB to solve. Europe, particularly in the north, has suffered from a stagnant to declining population while under the weight of crushingly expensive social programs. The Wall Street Journal reported today that the Finnish government collapsed because of failed social and health care reforms. Italy is a particularly sore spot for Europe. https://www.bloomberg.com/news/articles/2019-02-27/italy-failing-on-debt-reduction-is-a-risk-for-europe-eu-warns

Simply stated: Europe is not competitive with the rest of the world and its economies are suffering from their lavish lifestyles… they are consuming their future.

Still, with regard to the ECB actions, The New York Times had a good article last week. https://www.nytimes.com/2019/03/07/business/ecb-european-economy-stimulus.html

Bruce Hall Europe is not competitive with the rest of the world and its economies are suffering from their lavish lifestyles… they are consuming their future.

Hmmmm. You might want to check that claim against the OECD database. It turns out that saving as a percent of GDP is higher in Europe than it is in the US. But you should have been able to have guessed that because the US is running huge Trump deficits, which is being funded to a large extent by European savers. It’s Americans who are borrowing to fund their lavish lifestyles rather than increase national saving.

As to “failed social and health care reforms”, I think you’ll have to explain how US health care is not “failed” despite consuming twice as much of GDP and gets worse results. Good luck explaining that.

Your problem is that you wear these blinders in which you seem to think private sector consumption is less of an economic burden than public sector consumption. In terms of the economic burden it makes no difference whether “X” amount of health care consumption is paid for via taxes or insurance premiums to a private sector insurance company. You still consume “X” amount of economic resources out of GDP. It terms of the economic burden it makes no difference whether “Z” amount of retirement benefits are paid for via taxes on current workers or paid for by dissaving out of private retirement accounts. That retiree still consumes exactly “Z” amount of retirement benefits and subtracts exactly the same amount from productive capital. You’ve been hanging around various econ blogs long enough that by now you should be able to start thinking in terms of economic resources in general rather than continuing with this misguided fetish about government being the source of the benefit.

Europe, particularly in the north, has suffered from a stagnant to declining population

That’s true. Put another way, Europe is suffering from declining labor inputs. Sounds like an argument for immigration or perhaps refocusing on GNP/NNP rather than GDP/NDP. And if Trump has his way the US will be facing exactly the same demographic problem that plagues Europe and Japan…and China.

2slug, your responses are pretty good overall. You won’t get any argument from me against the notion that the U.S. is also spending its future and increasing debt over the decades would seem to to indicate.

However, I would disagree that private sector consumption is essentially the same as public sector consumption. The difference is a matter of control. You and I don’t have much, if any, say in public sector consumption, but we certainly have a say in how we consume our own resources and, for the most part, I’d argue that private sector consumption is much better controlled by each individual. Certainly, there are individuals who are poor at financial planning and debt management, but when the government does that, the whole nation is sucked in. The “mal-allocation” of resources is on a grand scale when the government is involved. I presume you are familiar with the “use it or lose it” principle of government budgeting.

Canada is a good example of a government-controlled, one-size-fits-all healthcare system: https://business.financialpost.com/opinion/william-watson-why-canadas-best-health-care-system-just-got-ranked-last-again?fbclid=IwAR0Y6hgDQ3Loq4jObxXLQscj_7YyfwWhZGNqOzrf9GL7UtZZwle3wgWNdio. Yes, that’s opinion, but not just one person’s. Having the right to something is not always the same as having access to that thing.

Europe is affected by declining population. Part of that is related to lower infant mortality rates and the emotional need to have more children. Part of that is the focus on “me” which affects the current child-bearing generation. And wouldn’t all of the eco-progressives say that is a good thing? Few people; Gaia is saved.

Bruce Hall I think you’ll find that your sense of having more control with private sector saving is illusory. One of the big problems with a privatized retirement system is that it leads to too much saving because individuals are less able to bear risk and cannot diversify risk in the same way that a government can. So if you measure economic welfare as the amount you can consume in retirement, then you will be worse off with a privatized retirement system for a given level of national saving. But my larger point was that privately funded retirements don’t make the resource consumption problem go away simply because they are privately funded rather than publicly funded. Consumption is consumption and dissaving is dissaving no matter how you slice it.

As to the article on Canada’s healthcare system, the whole thing seemed confused. The problem described in the article had to do with the delivery of healthcare services; but in that regard Canada is no different than the US. The delivery of healthcare is privatized, just as it is here. Canada is a single payer system, not a single provider system. In other words, Canada is like “Medicare for All” which is very different from Britain’s National Health System, which is single provider. The article seems to confuse health insurance with healthcare.

Regarding Europe’s low birth rate, that’s just something that comes with higher income and a stronger retirement safety net. That phenomenon is just as true in China and India as it is in Germany and Norway. As income goes up, fertility goes down. And in terms of the environment lower birth rates probably are a good thing. What’s not a good thing is the widespread slowdown in multifactor productivity (i.e., technological growth) over the last 15 years.

Some discussion on central banks, trade, and the US dollar that I thought is semi-related to this post. Seems Japan is doing well on these turbulent international seas.

https://www.youtube.com/watch?v=NrxK_G1YJAY

Hope your violin playing son is doing well Professor Mody.

As a note, on today’s Trading Economics “Major stock indexes in the Asia-Pacific region closed higher on Monday, amid renewed hopes of a US-China trade agreement…” Look at the big increases & small increases in percentage.

Actual Chg %Chg

Dow Jones 25858 11 0.04 %

S&P 500 2832 10 0.34 %

NASDAQ 100 7330 24 0.33 %

NIKKEI 225 21,602 158 0.74%

FTSE 100 7291 64 0.88 %

DAX 11670 15 -0.13 %

CAC 40 5409 4 0.08 %

FTSE MIB 21229 184 0.87 %

IBEX 35 9,402 62 0.66%

ASX 200 6,189 15 0.24%

SHANGHAI 3,096 75 2.47%

SENSEX 38,095 71 0.19%

MOEX 2484 8 0.31 %

TSX 16162 22 0.13 %

Guys, just watch all the Close-of-Day prices of major stock indices as of today 18 March. It’s not too hard to understand what it means.

https://tradingeconomics.com

Click on the “Stocks” tab.