That’s my new entry in the Oxford Research Encyclopedia of Economics and Finance.

The idea that prices and exchange rates adjust so as to equalize the common-currency price of identical bundles of goods—purchasing power parity (PPP)—is a topic of central importance in international finance. If PPP holds continuously, then nominal exchange rate changes do not influence trade flows. If PPP does not hold in the short run, but does in the long run, then monetary factors can affect the real exchange rate only temporarily. Substantial evidence has accumulated—with the advent of new statistical tests, alternative data sets, and longer spans of data—that purchasing power parity does not typically hold in the short run. One reason why PPP doesn’t hold in the short run might be due to sticky prices, in combination with other factors, such as trade barriers. The evidence is mixed for the longer run. Variations in the real exchange rate in the longer run can also be driven by shocks to demand, arising from changes in government spending, the terms of trade, as well as wealth and debt stocks. At time horizon of decades, trend movements in the real exchange rate—that is, systematically trending deviations in PPP—could be due to the presence of nontraded goods, combined with real factors such as differentials in productivity growth. The well-known positive association between the price level and income levels—also known as the “Penn Effect”—is consistent with this channel. Whether PPP holds then depends on the time period, the time horizon, and the currencies examined.

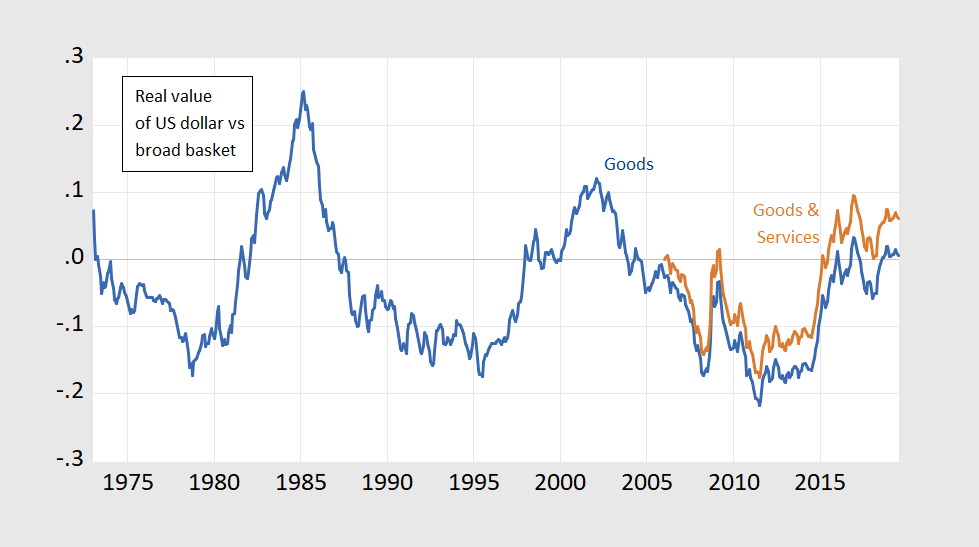

To illustrate the points made in the paper, if CPI bundles ascribed equal weights to individual goods, and the law of one price held, then the real value index for the US dollar over time would look like a flat line. It doesn’t.

Figure 1: Log value of US dollar, against a broad basket of currencies of trading partners, for goods (blue), and for goods and services (brown). Up denotes appreciation. Source: Federal Reserve Board via FRED, and author’s calculations.

Hence, purchasing power parity (PPP) does not hold over time for a given country, instantaneously. It might over longer stretches of time (i.e., in the long run), but that is an empirical question (and would show up as mean reversion in Figure 1 series; trend reversion is not PPP literally taken — and even here we are evaluating relative PPP).

Why the exchange rate moves as it does is discussed in the article, as well as this 2012 survey. For a recent horse race a la Meese and Rogoff (1983), see Cheung et al (2019).

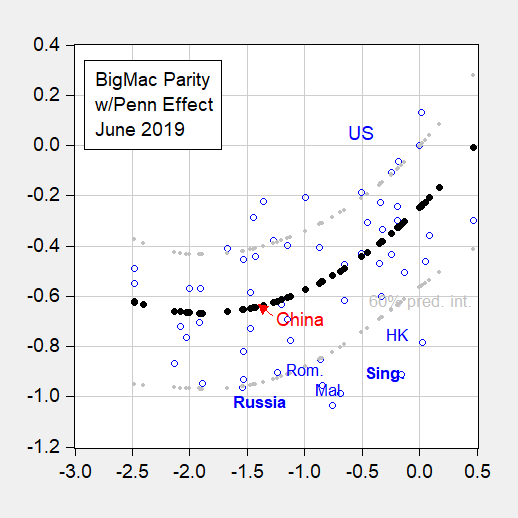

The point that price levels tend to rise as income rise, so (absolute) PPP doesn’t hold across countries, is demonstrated by the fact that at any given instant, all the observations in Big Mac Parity don’t show up on a horizontal line at “0”.

Figure 2: Log price level relative to US price level plotted against log relative per capita income, both in 2019. Penn Effect line estimated using quantile regression (black) and 60% prediction interval (gray). Source: Economist, IMF World Economic Outlook April 2019 database, author’s calculations.

Figure 2 is relevant when you hear talk about Chinese currency undervaluation. We should hear as much (or more) about Russia as we do about China (but given Mr. Trump’s allegiances, I don’t think we will).

More on the “Penn effect” in this post.

More from the Encyclopedia (free access for now):

Menzie, are you going to miss your “big chance” to be in the Palgrave Dictionary of Economics?? They have a “new edition” arriving in the future sometime—certain to be error free. [ Energy drink soda almost came out of my nose on that one ]

On a more solemn note, thanks for the links, it is gracious and kind of you.

Moses Herzog: Already in there for “real exchange rates”, as well as for “fiscal multipliers” as noted by Barkley Rosser. A useful publication – I have the original Palgrave Dictionary on my bookshelf (it’s true — it came out as hard bound books in the 80’s).

@ Menzie

Nyaaaah Nyaaaah. You know I couldn’t resist Menzie. The new editions you mean?? I sincerely hope you had that edited 3 times by academic friends if its destination was Rosser’s office.

I tell you what, I’ll do you and Barkley Junior a favor right here and now—- if YOU wanna tell me and Rosser the “admixture” of Native American DNA is “skewed” in the USA population of whites, this’ll be my last comment on the topic right here and now.

Sorry, boy, but you really have no idea now far out of it you are, and what a massive fool you are making of yourself with posts like this. Grow up.

@ Barkley Junior

Afraid one day Menzie will answer that question??

Menzie hasn’t hesitated from calling me out on other issues or mistakes I’ve made (which BTW, I never took offense to Menzie doing, I’d rather know I’m wrong, if I indeed AM, and learn something). Why you think when someone in his same profession is the one making a jackass of himself he has nothing to say?? Color me cynical when I say, I don’t think half a beat would drop for Menzie to agree with you the distribution is “skewed” if it in fact was. I’ll admit it’s a bit of a mystery to me why he chooses not to settle it. Sympathy for your age??? He can remain neutral if he likes, there is no violation in ethics in choosing to remain silent. He needn’t worry about offending me if he flat out wants to state the distribution you claim is “skewed” is indeed skewed. I’ve made it as clear as I can that it would be no offense to me as far as my attitude towards Menzie.

Moses Herzog: I’m not taking a stand on this issue as I have not invested the time to read through what you are saying. I will say that I do not think the manner in which you have conducted the debate is either appropriate or effective. Hence, do not take my failure to comment/correct as either explicit or implicit assent. However, to the extent you do not use profanity, or make explicitly racist/sexist remarks directed at an individual, I’m not going through the trouble of censoring, per the Econbrowser policy.

@ Menzie

I wanna say something here, without hopefully going down certain rabbit holes. You’ve been more than fair about it, especially as regards what I would term some of my more “borderline” comments. And I recognize that you have been equitable and fair on those grounds as on any grounds as I blog host I can think of. And I take no joy in “making things personaL’ with anyone believe it or not. But when people (specifically commenters) make personal comments towards me, which I deem largely untrue, I will point out what I view to be their personal downfalls in kind —only return something they don’t always give me—a certain amount of accuracy in their negatives I point out.

Should I use more research links?? Probably. But if someone can’t read the very paper they are quoting, I don’t know where one takes the argument from there. BTW, I have ZERO problem with you letting the more critical, even insulting comments about me through the blog’s filter—even personally insulting—IMO that is indeed PART of what makes a blog—-a blog.

Moses Herzog: My perspective is that personal insults have been flying in both directions. And that is not helpful.

Moses,

How many times must it be pointed out that the article said the disttribution was evenly distributed across rhe genome. It did not say it was evenly distributed across the population. Again for the umpteenth squared time, genome is not population. The distribution of Native American ancestry across the US white population is not remotely evenly distributed. It is much higher for whites in Oklahoma City than it is for whites in Brighton Beach in Brooklyn.

As it is, Moses, I have made several attempts to make peace with you and have even apologized to you for some of my pokes at you. As is well known, however, you owe me an apology, but have not given it, rather instead imposed a silly condition on doing so. Neither Menzie no I are your research assistant.

As it is, population genetics is yet another one of those things I happen know quite a bit about. I personally knew the late Sewall Wright, one of the main developers of it, who was in the genetics department at UW-Madison before Menzie got here. I even happen to own Wright’s personal copy of his famous 1925 USDA monograph on corn-hog correlations in which he became the first to identify the identification problem. Both Wright and R.A. Fisher were founders of population genetics who also developed important ideas of econometrics.

Again, while Menzie has chosen to stay out of it (and he is not a population geneticist, Moses), if you go back to when you first made your fuss over this matter, several others pointed out to you the point repeated above: that a genome is not a population and that a distribution on a genome implies nothing about the distribution on the population. Please do get this simple fact through your head once and for all, and indeed the distribution of Native American genetic ancestry in the US white population is skewed, not even. And the bottom line on where all this started is indeed that whites living in parts of the US where there are lots of Native Americans (like Oklahoma where Elizabeth Warren was born) are much more likely to have Native American ancestry than whites born in parts of the nation with low Native American populations.

Out of respect for Menzie and Jim and to help return this blog to its high intellectual level, I am going to do my best in the future to avoid making personalistic attacks, even when I am on the receiving end of unprovoked ones. I urge others to try to do so as well to reduce what has become an excessive amount of this sort of thing.

A followup on my last post is that in my much-cited 1991 book I quoted at length from Sewall Wright’s last paper from The American Naturalist in 1989 while developing a new transdisciplnary concept that has its own Wikipedia entry. But I am not going to bother with providing any details on that. Those really interested can dig it out. But, indeed, I knew Wright and his closest protege at UW-Madison well. Anyone trying to find in error on populsation genetics is not going to get anywhere, no matter how often they repeat points.

Your figure #1 really tempts me to forecast that the dollar is headed for a fall below the -.2 level, though perhaps with a spike in the near future if the global economy takes a sudden hit.

I would say there’s about an 80% chance they will lower rates at the next designated time to change them (mid-Sept??). I doubt if Powell learned his lesson at all from the tariffs being slapped on 24 hours after his boot-licking at the orange creature’s feet. But also it’s likely other countries will lower the rate as well. It’s an interesting question. Germany has reported some good numbers lately that I have to confess surprised me a lot. I think following Menzie’s writings and other high ranking economists can give us some idea. I agree though, from purely a visual standpoint of looking at the graph it gives the impression the U.S. dollar will lower. But that’s really a bad way to judge it, and you have to remember everyone is looking at that same graph.

Here’s the funny part, when there’s no well-structured fiscal policy to go with it, and the economy is meandering with a slight tilt to the positive side, these crap rate drops aren’t going to amount to anything, other than retired people getting nothing back on their savings deposits. Why is Powell doing them??? Because with all his “high falutin ehdguhmuhcation” all the creativity the dumb bast*rd has is doing what is expected of him to clasp onto his job.

Among the requirements of a PPP calculation are a near-identical basket of goods and services and near-identical economies.

Why oh why, I have to ask, does anyone take PPP seriously when comparing China and the US?

Taiwan vs. Korea I will accept;

Hong Kong vs. Singapore is a no-brainer;

China vs. India might qualify.

China vs. the USA ?

Really?