On the eve of the advance GDP release for Q1.

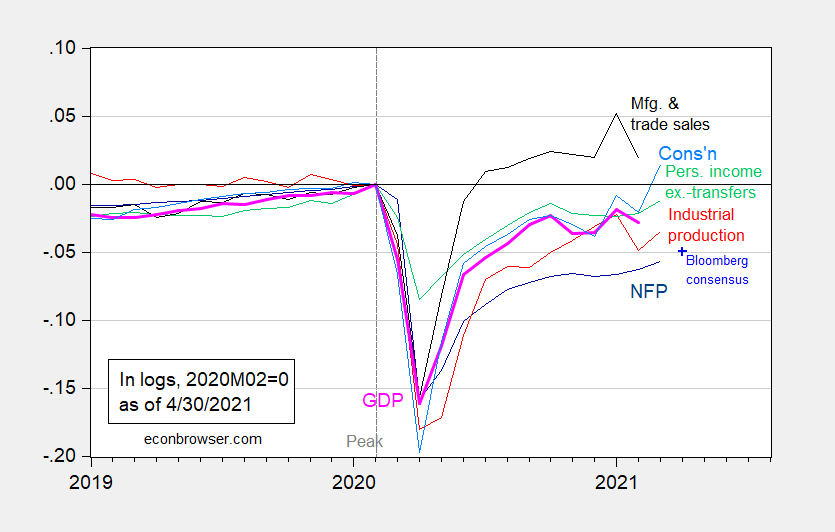

Updated Figure 3 – business cycle indicators as of 4/30:

[Updated] Figure 3: Nonfarm payroll employment from March release (dark blue), Bloomberg consensus as of 4/28 for April nonfarm payroll employment (light blue +), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), consumption in Ch.2012$ (light blue), and monthly GDP in Ch.2012$ (pink), all log normalized to 2020M02=0. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (4/1/2021 release), NBER, and author’s calculations.

Nowcasts:

Figure 1: GDP in bn. Ch.2012$ SAAR (black), Atlanta Fed 4/28 GDPNow (red), NY Fed 4/23 nowcast (blue), IHS Markit nee Macroeconomic Advisers 4/28 nowcast (green), potential GDP (gray). Source: BEA 2020Q4 3rd release, Atlanta Fed, NY Fed, IHS Markit, CBO (February 2021), author’s calculations.

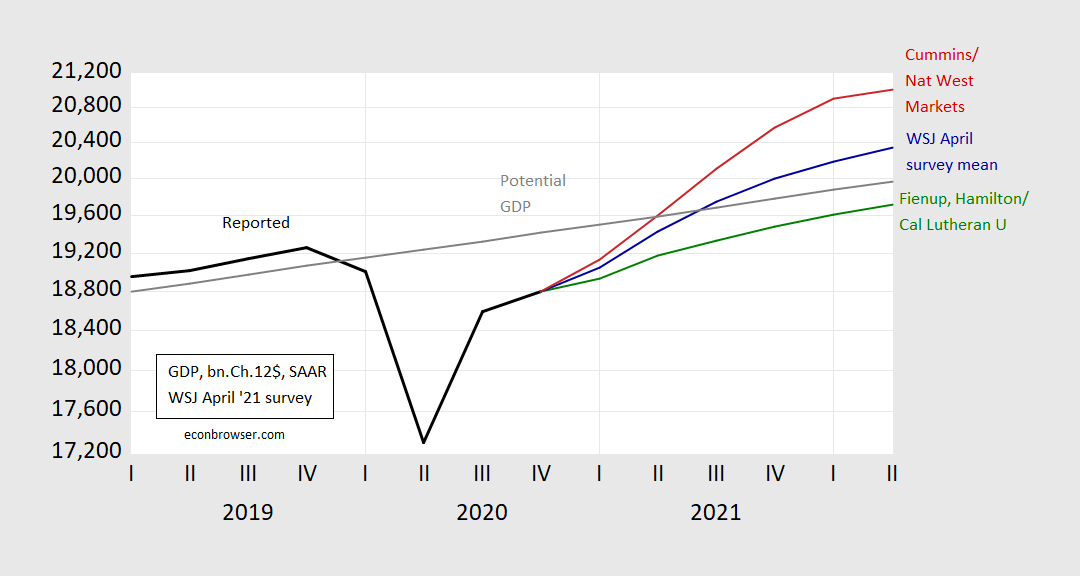

Forecasts from WSJ April survey:

Figure 2: GDP actual (bold black), WSJ April survey mean (blue), Cummins/Nat West Markets (red), Fienup, Hamilton/California Lutheran University (green), CBO estimate of potential GDP (gray), all in billions Ch.2012$, on log scale. Foreacasted levels calculated by cumulating growth rates to latest GDP level reported. Source: BEA (2020Q4 3rd release), WSJ surveys (various), CBO (February 2021), and author’s calculations.

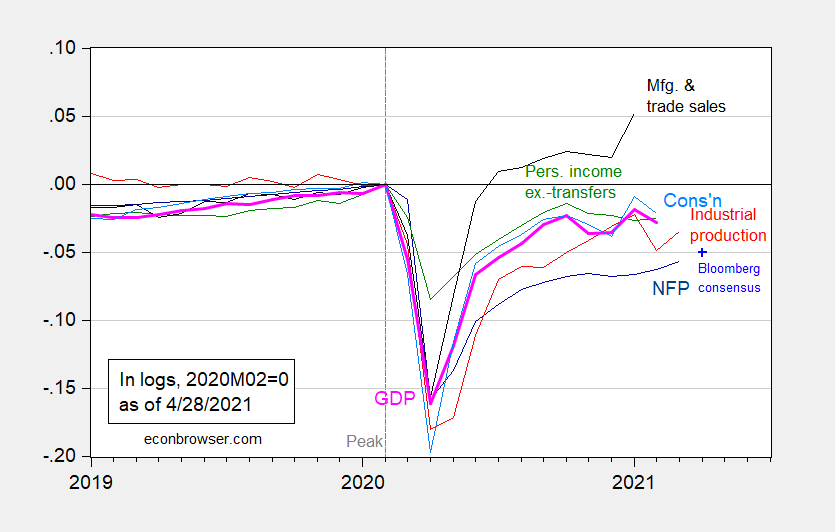

Some higher frequency indicators, tracked by the NBER BCDC:

Figure 3: Nonfarm payroll employment from March release (dark blue), Bloomberg consensus as of 4/28 for April nonfarm payroll employment (light blue +), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), consumption in Ch.2012$ (light blue), and monthly GDP in Ch.2012$ (pink), all log normalized to 2020M02=0. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (4/1/2021 release), NBER, and author’s calculations.

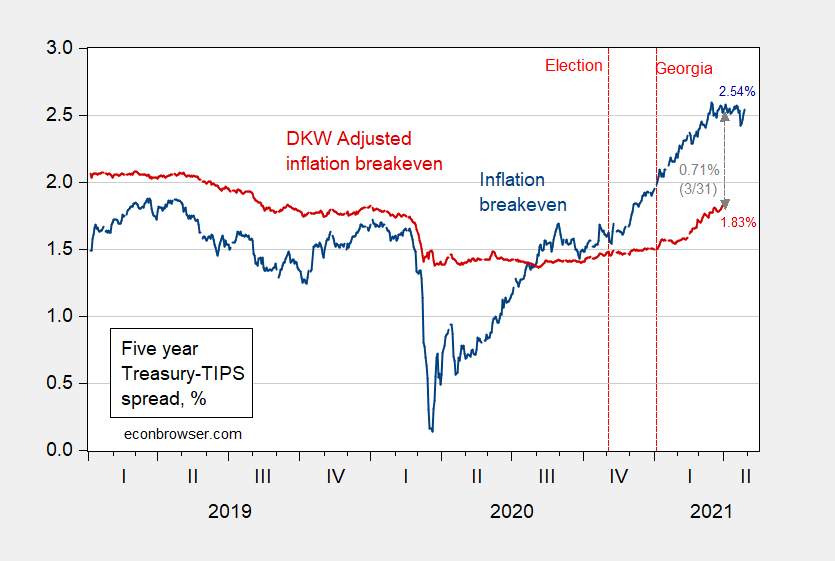

At the same time, long term inflation expectations remain anchored, at least by market based measures.

Figure 4. Five year inflation breakeven calculated as five year Treasury yield minus five year TIPS yield (blue), five year breakeven adjusted by term premium and liquidity premium per DKW, all in %. Source: FRB via FRED, KWW following D’amico, Kim and Wei (DKW) accessed 4/28, and author’s calculations.

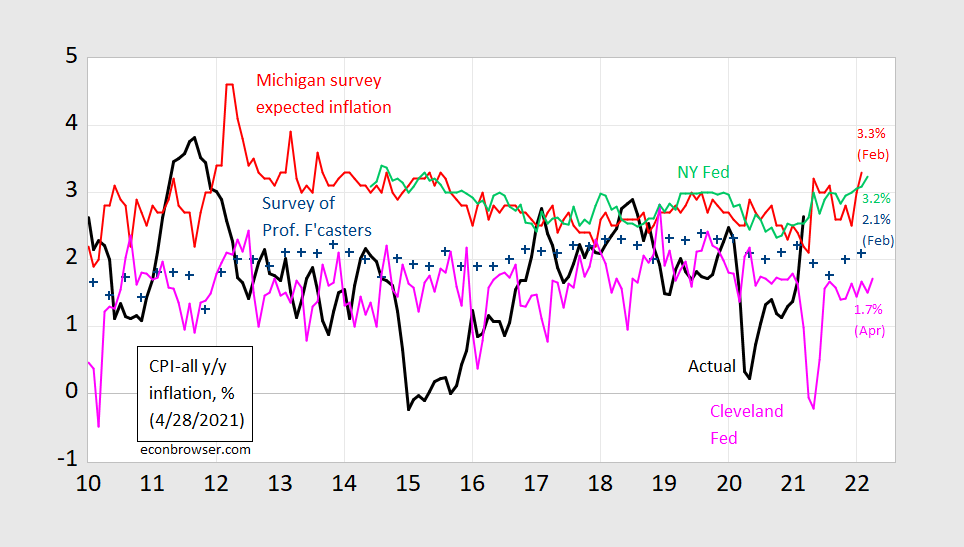

Hence, expected inflation over the next 12 months (for CPI) remains fairly low (keeping in mind household measures like Michigan and NY Fed are biased upward relative to actual outcomes):

Figure 5. CPI inflation year-on-year (black), median expected from Survey of Professional Forecasters (blue +), median expected from Michigan Survey of Consumers (red), median from NY Fed Survey of Consumer Expectations (light green), forecast from Cleveland Fed (pink). Source: BLS, University of Michigan via FRED, Philadelphia Fed Survey of Professional Forecasters, Philadelphia Fed, NY Fed, and Cleveland Fed.

Look for Jim’s post on the GDP release tomorrow!

I’m going with 5.8%. “AS”?!?!?!?! Where are you brother?? What you got for me?? I want to hear the smart model prediction. Barkley doesn’t like my Joe Six Pack Beer Gut prediction because we base our beer gut feeling on SAAR numbers and he really hates SAAR. If you teach near Virginia you just base it on whatever makes your bad prediction look better after you got busted 30% off. I need some cover from you if my 5.8% number is way wrong.

Does Menzie want me to do GDP levels er something???

https://youtu.be/48ygqP4mwxQ?t=30

@ Menzie

Menzie, how often do I suggest you follow certain accounts on Twitter?? I think maybe once with a journalist at WaPo. I strongly suggest you follow this twitter account/feed:

https://twitter.com/WomenInMacro

CBO estimate of potential GDP (gray)

I get why you draw this estimate but maybe an alternative measure that is not so conservative but be tossed in.

I generally hate references the self serving champions of corporate American at Doof and Phelps but for some reason they keep emailing me their junk. But this short statement does have a nice discussion of steel prices since 2016:

https://www.duffandphelps.com/-/media/assets/pdfs/publications/fixed-asset-management-and-insurance-solutions/cost-trend-update-bulletin-march-2021.pdf

The headline news is that steel prices have surged to $1126 per metric ton. HYPERINFLATION! Biden is a communist – the world is coming to an end. Oh wait – I’m beginning to sound a lot like Bruce Hall. Forgive me.

Back to reality – steel prices have shown a lot of volatility over the past 5 years. Stop the presses.

Then again Stephen Moore is working on a better commodity rule for monetary policy. Forget gold and use steel prices as the basis for his commodity rule. Just imagine all the incredible damage this would cause.

I’m listening to Rick Scott “criticize” Biden’s proposal with one hyperbolic lie after another. Memo to Bruce Hall – you need to up your game to keep up with Senator Scott.

It appears the BEA reported number is 6.4%. That makes me 0.6% off, which actually is pretty bad. Will be interesting to see which way the revisions/updates go. That’s what I get for having Jalapeño cheese and overly acidic lemonade flavored alcohol. That’s what I get….. It totally throws my joe six-pack gut intuition out of wack. Is that a good excuse?? Is this con working??

Kevin Drum beat this blog to announcing the BEA news? Of course Kevin is plagued with even worse right wing trolls such as this one:

‘Mitchell Young

April 29, 2021 – 9:11 am at

LOL. Real GDP ‘soared’ over 15% in Q3 of 2020 and another 4.3% in Q4, even with the recalcitrance of ‘blue’ governors to open their states and Fauci-CDC obstructionism.’

This comment went down hill from here. Mitchell seems to be unaware of what happened in Q2 of 2020.

Taking a quick look at the latest from BEA. During 2021QI, we saw strong growth in private consumption and private investment but net exports took a hit. Government purchases are up with the details being interesting. Defense purchases fell but Federal nondefense purchases were way up.