After adjustment for premia, constant over the last three months:

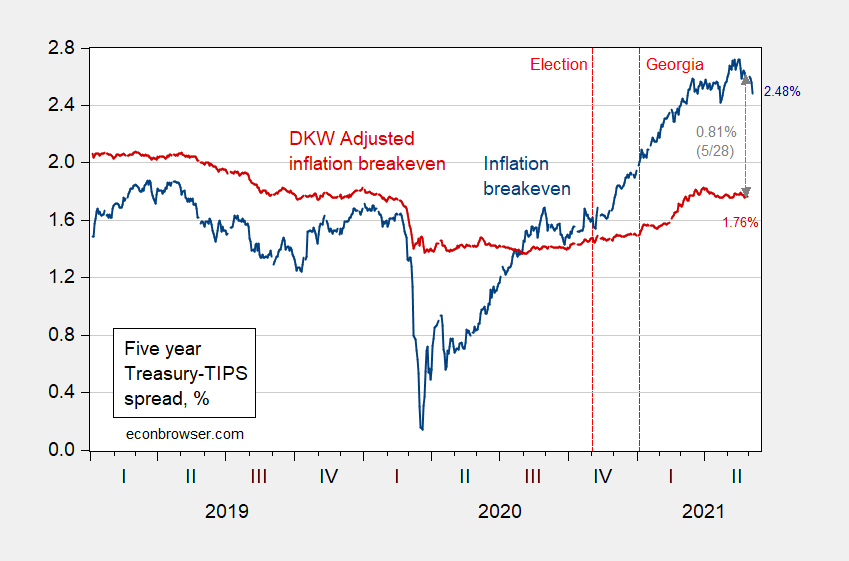

Figure 1: Five year inflation breakeven calculated as five year Treasury yield minus five year TIPS yield (blue), five year breakeven adjusted by term premium and liquidity premium per DKW, all in %. Source: FRB via FRED, KWW following D’amico, Kim and Wei (DKW) accessed 6/4, and author’s calculations.

https://www.nytimes.com/2021/06/05/us/politics/g7-global-tax-deal.html

June 5, 2021

Finance Leaders Reach Global Tax Deal Aimed at Ending Profit Shifting

The Group of 7 nations reached an agreement over a global minimum tax that companies would pay regardless of where they are based.

By Alan Rappeport

LONDON — The top economic officials from the world’s advanced economies reached a breakthrough on Saturday in their yearslong efforts to overhaul international tax laws, unveiling a broad agreement that aims to stop large multinational companies from seeking out tax havens and force them to pay more of their income to their governments.

Finance leaders from the Group of 7 countries agreed to back a new global minimum tax rate of at least 15 percent that companies would have to pay regardless of where they locate their headquarters.

The agreement would also impose an additional tax on some of the largest multinational companies, forcing technology giants like Amazon, Facebook and Google as well as other big global firms to pay taxes to countries based on where goods or services are sold, regardless of whether they have a physical presence in that nation.

Officials described the pact as a historic agreement that could reshape global commerce and solidify public finances that have been eroded after more than a year of combating the coronavirus pandemic. The deal comes after several years of fraught negotiations and, if enacted, would reverse a race to the bottom on international tax rates. It would also put to rest a fight between the United States and Europe over how to tax big technology companies….

[ The point so far as I can understand is that this agreement has nothing to do with minimal tax locations such as the Netherlands or Ireland or Switzerland or Singapore… The G7 is not even the European Union. What is needed is a significantly broader negotiation base. ]

International tax law is overly complicated. This may be a step in the right direction but something tells me this is not the end of profit shifting.

“the largest global firms with profit margins of at least 10% will be in scope – with 20% of any profit above the 10% margin reallocated and then subjected to tax in the countries where they make sales.”

I copied the only coherent and relevant part of some LinkedIn post from the UK representative who is patting himself on the back for what he is calling a “historic” change in international tax. I literally fell out of my chair laughing at the blow hard’s rant. And one wonders how multinationals continue to beat tax authorities at this game of tax evasion.

ltr,

Well, given the importance of the G-7 nations, larger economies than all but the PRC, this looks like a good place to start. Heck, I did not think they would even get as far as getting those all on board.

Lorraine Eden – the goddess of transfer pricing – has written papers on this which note if the US, China, and the EU are all in, this idea is going to hold together.

http://www.xinhuanet.com/english/2021-06/05/c_139990693.htm

June 5, 2021

Over 744 mln COVID-19 vaccine doses administered across China

BEIJING — Over 744 million doses of COVID-19 vaccines had been administered across China as of Friday, the National Health Commission said Saturday.

[ Vaccination is proceeding at a rate of 20 million doses daily, with 5 Chinese vaccines being used. Distribution of Chinese vaccines as public goods now includes dozens of countries. ]

“five year breakeven adjusted by term premium and liquidity premium per DKW”

I’m a bit confused by the terminology. Term premium generally refers to the risk of changes in the real rate as you go to longer terms. Since 5-year TIPS and 5-year nominal bonds have the same term, they should have approximately the same term risk so that term risk does not show up in the breakeven rate.

The breakeven rate is expected inflation plus the inflation risk premium for nominal bonds minus the TIPS liquidity premium. So in the quoted statement above, it would seem to be more accurate to say “adjusted by the inflation risk premium and the liquidity premium”. Inflation risk and liquidity risk have opposite signs.

Or another way of looking at it is that the inflation risk premium increasing nominal rates is exactly equivalent to an inflation insurance premium decreasing TIPS rates. The relative difference is what matters.

joseph: Sure, see KWW article linked to for that terminology.

https://www.nytimes.com/2021/06/05/upshot/jobs-rising-wages.html

June 5, 2021

Workers Are Gaining Leverage Over Employers Right Before Our Eyes

“Employers are becoming much more cognizant that yes, it’s about money, but also about quality of life.”

By Neil Irwin

The relationship between American businesses and their employees is undergoing a profound shift: For the first time in a generation, workers are gaining the upper hand.

The change is broader than the pandemic-related signing bonuses at fast-food places. Up and down the wage scale, companies are becoming more willing to pay a little more, to train workers, to take chances on people without traditional qualifications, and to show greater flexibility in where and how people work.

The erosion of employer power began during the low-unemployment years leading up to the pandemic and, given demographic trends, could persist for years.

March had a record number of open positions, according to federal data that goes back to 2000, and workers were voluntarily leaving their jobs at a rate that matches its historical high. Burning Glass Technologies, a firm that analyzes millions of job listings a day, found that the share of postings that say “no experience necessary” is up two-thirds over 2019 levels, while the share of those promising a starting bonus has doubled.

People are demanding more money to take a new job. The “reservation wage,” as economists call the minimum compensation workers would require, was 19 percent higher for those without a college degree in March than in November 2019, a jump of nearly $10,000 a year, according to a survey by the Federal Reserve Bank of New York.

Employers are feeling it: A survey of human resources executives from large companies conducted in April by the Conference Board, a research group, found that 49 percent of organizations with a mostly blue-collar work force found it hard to retain workers, up from 30 percent before the pandemic….

https://www.bloomberg.com/news/articles/2021-06-01/the-teacher-rocking-markets-by-taking-on-peru-s-elite-for-the-presidency?sref=IHf7eRWL

June 1, 2021

Elites Tremble as Peru Leftist Taps Anger Over Rising Inequality

Pedro Castillo was a little-known schoolteacher from the hinterland. Now he’s made it to the runoff, striking fear into Lima’s elite.

By Ana Maria Cervantes and Jim Wyss – Bloomberg

At a recent rally in Lima, hundreds jostled to catch a glimpse of Pedro Castillo, the school teacher and union organizer who pulled off an upset to make it to the runoff for Peru’s presidency.

Supporters chanted “No more poor people in a rich country,” as they waved an image of Tupac Amaru II, the indigenous leader who fought against Spanish domination almost 250 years ago and who has inspired revolutionary movements across the region ever since.

Castillo’s jubilant backers can barely believe that the son of illiterate Andean peasants has reached the June 6 second-round vote on a platform that amounts to taking up the historic struggle to liberate the oppressed. Investors are shocked for different reasons, recoiling at the prospect that Castillo and his Free Peru party — founded by a Marxist — seem prepared to tear up decades of market-friendly consensus.

“He came from nothing and now he’s on the verge of being president,” said Miguel del Castillo, a friend and adviser who’s not related to the candidate. “The Peruvian miracle exists.”

In reality, Castillo’s rise is a consequence of the political upheaval sweeping Latin America as it’s battered by one of the world’s deadliest waves of Covid-19 and an economic crisis that has exposed and exacerbated long-standing inequalities. On Monday, Peru’s official death toll almost tripled after a government review of data, giving it the highest per-capita mortality rate in the world, according to Johns Hopkins University Coronavirus Resource Center.

The seeds of Peru’s revolt were sown during 20 consecutive years of economic growth that pulled millions out of poverty and established the country as a relative safe haven in a turbulent region, at least until the pandemic hit. An economic slump of 11% last year focused attention on the fact those gains haven’t been evenly distributed. Perversely, some of the country’s most mineral-wealthy provinces — rich with copper, gold, silver and zinc — are also its poorest.

The result has been to accentuate the divide between a wealthier, Spanish-speaking capital and the impoverished countryside, where much of the population speaks the indigenous Quechua language. As classes moved online, for example, many students in rural areas didn’t have internet access. It is that latter constituency where Castillo has built his base. Wearing a straw hat and carrying an over-sized pencil to stress his focus on education, Castillo, 51, promises to forge a country that works for everyone, not just the capital elite.

“People see that all the natural resources are in the countryside but all the benefits are concentrated in Lima,” said Maritza Paredes, a sociology professor at the Pontifical Catholic University of Peru. “Castillo has been able to capitalize on it.”

Castillo’s program is as ambitious as his lack of government experience is daunting. At the center of his strategy are plans to force multinational corporations, particularly the mining companies that are the backbone of the economy, to leave more of their profits in Peru. He wants to promote rural development, plow 20% of economic output into education and health care and shut down private pension funds. His flagship proposal is to rewrite the constitution crafted under President Alberto Fujimori, a document he says prioritizes business interests over “human rights” like public housing and organized labor.

Castillo’s rival in the run-off, Keiko Fujimori, is at the other extreme of the political spectrum. The former president’s daughter, she is one of Peru’s best-known politicians and one of the most controversial: Her father is in jail and she’s running her campaign while out on bail facing money-laundering charges….

https://fred.stlouisfed.org/graph/?g=Eusg

August 4, 2014

Real per capita Gross Domestic Product for Brazil, Argentina, Chile, Colombia and Peru, 1971-2019

(Percent change)

https://fred.stlouisfed.org/graph/?g=Eusm

August 4, 2014

Real per capita Gross Domestic Product for Brazil, Argentina, Chile, Colombia and Peru, 1971-2019

(Indexed to 1971)

https://www.worldometers.info/coronavirus/country/us/

Over the past 5 months, daily new deaths and new cases have dramatically declined in the US. It is interesting that listening to scientists while ignoring Trump and people like Bruce Hall can change things for the better. Get your vaccine and please do not drink bleach.

One of the funnier things going on now is that after Trump bragged about his role in moving the development and adoption of the vaccines forward, for which he does deserve some credit (and I saw Fauci on MSNBC doing so), so many of this followers are now totally against getting vaccinated. So Trump was wonderful for helping to achieve this awful thing they want nothing to do with.

And, of course, Fauci is somehow now responsible for the pandemic, with Donald Trump, Jr. last night saying he is looking forward to “celebrating” Fauci being murdered. One cannot make this stuff up.

ItalyGate! It seems for the last 5 months the insane right wing nutcases have been telling us that an Italian security firm tampered with the Nov. 2020 votes switching votes from Trump to Biden. Satellites and military technology was involved:

https://www.reuters.com/article/uk-fact-check-debunking-italy-gate-idUSKBN29K2N8

Of course none of this happened but in Trump world Biden is the puppet of some Italian socialist regime. MAGA!

Well, since nobody so far is commenting on Menzie’s post, let me ask Menzie, so what has been responsible for the recent decline in the breakeven rate of inflation expectation, declining nominal 5-year rate, rising 5-yeat TIPS rate, or some of both?

Define recent. Since April 1, TIPS rate has declined but nominal rate has declined more.

Oh wait – the breakeven peaked on May 18 and is lower now. So it does seem TIPs rates have shown no net change but nominal rates have become slightly less negative. My apologies as I needed to pull out my microscope on this one!

https://fred.stlouisfed.org/graph/?g=r5VT

January 15, 2020

Interest Rates on 5-Year Treasury Inflation-Indexed Bonds, 2021

https://fred.stlouisfed.org/graph/?g=r5Wn

January 15, 2020

5-Year, 5-Year Forward Inflation Expectation Rate, 2021

https://fred.stlouisfed.org/graph/?g=r5VO

January 15, 2020

TIPS 5-year spread, * 2021

* Breakeven inflation rate (difference between rate on nominal Treasury Notes and on Treasury Inflation-Protected Securities)

So the blue line in the graph is the mechanical subtraction of the nominal rate from the TIPS rate, the so-called breakeven rate.

According to DKW this breakeven rate is composed of three parts — the expected inflation rate, the inflation risk premium, and the liquidity premium.

Through some econometric modeling magic DKW claim to be able to be able to tease these invisible pieces apart. Once you subtract out the inflation risk premium and the liquidity premium you are left with the actual expected inflation rate which is shown by the red line in their model.

What is interesting is the difference between the blue line and the red line. This difference is the combination of the inflation risk premium and the liquidity premium. Further, DKW show that the liquidity premium is close to zero except for crisis conditions like 2008-2009 when liquidity is in high demand.

So that leaves the difference between the blue line and the red line representing only the inflation risk premium.

DKW interpret the inflation risk premium as the uncertainty in expected inflation, a fudge factor for yield that bond traders demand because of their lack of confidence in the consensus expected inflation.

What is interesting is that this inflation risk premium can be both positive and negative. For example in early 2020, the premium was decidedly negative, with the blue line below the red line, implying that bond traders perceived a risk that inflation would be much lower than expected (due to the pandemic).

Recently the inflation risk premium has opened up decidedly positive, the blue line above the red line, implying that bond traders think there is a strong risk that inflation could be somewhat higher than the 1.76% expected inflation rate.

What this means to me is that the bond market is saying to take the 1.76% DKW estimate of expected inflation with a grain of salt. Inflation could very well break higher. There is currently a lot of upside uncertainty implied by the inflation risk premium.

joseph,

I stand to be corrected if wrong, but it is my understanding that it is the adjusted rate that adds in (subtracts right now) the effect of the term and liquidity premia to the breakeven rate, which is simply the nominal 5-year rate minus the 5-year TIPS rate, with the recent changes seeming to mostly to the breakeven rate itself.

According to DKW, the breakeven rate (the blue line) consists of three parts — the expected inflation rate, the inflation risk premium and the liquidity premium.

DKW then use their magic to subtract out the inflation risk premium and the liquidity premiums. What you are left with is their estimate of expected inflation, the red line.

The difference between the blue line and the red line is what they subtracted out — the inflation risk premium and the liquidity premium. Since the liquidity premium is near zero in normal times, the difference between the blue line and the red line is just the inflation risk premium.

DKW interpret the inflation risk premium as market uncertainty about their red line number, a safety factor for yield that the market demands in case the red line is wrong about inflation. That degree of uncertainty about inflation can vary with time as the blue and red lines move relative to each other and can even go negative, as it did in early 2020.

I would again recommend against using the phrase “term premium” as it is misleading in this context. Both DKW and KWW use “inflation risk premium” as it represents a measure of the uncertainty of the inflation forecast of the red line. Term premium generally refers to the rate difference between two bonds of different term, for example the 5-year vs the 10-year. The term premium is the risk that the real rate will change over time. Here we are talking about two bonds of the same 5-year term, the TIPS and the nominal bond. They both have the same assumed real rate so both have the same term risk. Term risk should not appear in the difference between the blue line and the red line, only inflation risk.

@ joseph

There’s a lot of KWW and DKW I haven’t digested/absorbed yet. I’m not going to pretend that I fully grasp it. I am hoping to grasp it more fully as the time wears on.

But here is one thing I think the data is telling us~~we have two choices in the current context, either the forecasts (or “market expectations”) on inflation are ungodly high, or bond traders (generally regarded as a pretty intelligent group) are demanding way too low of an interest rate for the usage of their money. Which do you think it is?? To me it implies two things. If the Fed keeps its policy nose out of things, bond rates will rise over the next 6 months–1 year time frame. Inflation projections will lower. Those two things can occur simultaneously. So then, if we look at these two things as a kind of “meeting in the middle”, which will make the more drastic move?? Will 10 year treasury rates rise in a major fashion, or will inflation expectations lower in a larger fashion?? To me, I think the inflation (or what I view as reflation) expectations make a bigger move down than the interests rates will move up.

That’s my version of Greenspan lingo for today. But in all seriousness we can use the 10-year yield as a gauge. It’s 1.56% at the moment. If we go back and check the 10-year treasury number at the end of 2021, if my prediction is correct, it should be higher than 1.56%. Now if we check the number for Inflation (using Atlanta Fed Sticky Price CPI annualized number) then around December of 2021, then if I am right that number should be lower than the most recent number of 5.5%. Maybe Barkley Junior will bring this up later around December or January and hold a donkey sign over my head if I am wrong on those two predictions.

This prediction excludes “major event” factors such as a war, major terrorist event, similar virus to SARS, Covid-19 striking, etc etc.

What I would like to understand better is how DKW’s model works to distinguish expected inflation from the inflation risk premium. Both are contained in the breakeven rate (the blue line), but how you reliably separate the two is difficult. Some analysts use inflation swaps as a proxy for expected inflation but DKW do not. From the best I can tell they are using the structure of the yield curve over time to tease out expected inflation from the inflation risk premium but I can’t pretend to understand their method, let alone evaluate its validity.

Towards the end of the Fed note they as much as admit these things aren’t written in stone, there is some grey area and even warn they may “fine-tune” some of the calculations. Basically admitting there’s too many real life variables involved. The CSV file (though it’s pretty damned humongous to my eyes) may add some insight with the headings of the columns near to the top.