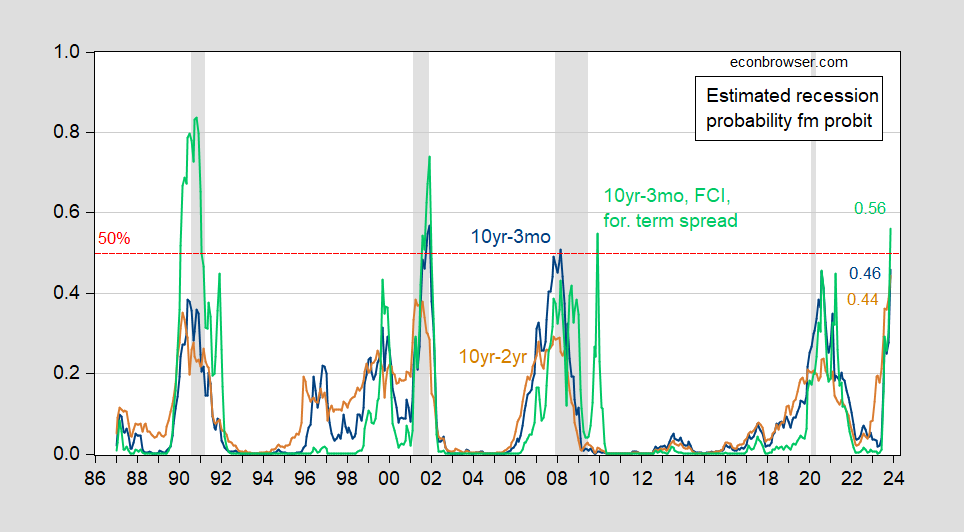

Yesterday’s Bloomberg article “Fed Staff Sees a 50-50 Chance of Recession” spurred me to examine the implications of the latest readings on term spreads. Figure 1 depicts the recession probabilities estimated using a simple probit model based on the 10yr-3mo and 10yr-2yr spreads, through November 23rd.

Figure 1: Forecasted probability of recession from 10yr-3mo term spread (blue), from 10yr-2yr term spread (tan), 10yr-3mo term spread augmented by FCI, foreign term spread (green). All models estimated over 1986M01-2022M11. NBER defined peak-to-trough recession dates shaded gray. Red dashed line at 50% probability. Source: author’s calculations, NBER.

While neither the 10yr-3mo and 10yr-2yr models breach the 50% threshold, they are sufficiently close to merit a 50-50 reading.

In work by Ahmed and Chinn (2022), it’s shown that the foreign term spreads and financial conditions index have additional predictive power for US recessions (see Table A.1). I augment the 10yr-3mo spread with the average of German-Euro Area/UK/Japan 10yr-3mo spreads, and the national financial conditions index, to obtain the estimated probabilities of recession shown in the green line in Figure 1. The reading for November 2023 is 56%.

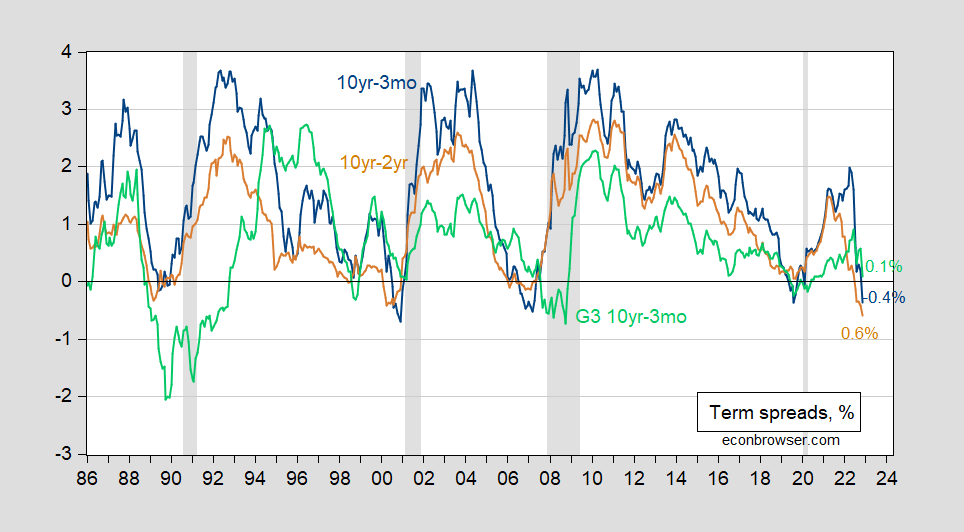

All these estimates are based upon the following term spreads:

Figure 2: US Treasury 10yr-3mo term spread (blue), 10yr-2yr (tan), and G3 Germany/UK/Japan 10yr-3mo (green), all in %. NBER defined peak-to-trough recession dates shaded gray. Source: Treasury via FRED, OECD Main Economic Indicators, NBER, and author’s calculations.

https://fred.stlouisfed.org/graph/?g=N741

January 4, 2020

Interest rates on 10-Year Treasury Bond minus 2-Year Treasury Note, 2020-2022

https://fred.stlouisfed.org/graph/?g=zSG6

January 4, 2020

Interest rates on 10-Year Treasury Bond minus 3-Month Treasury Bill, 2020-2022

The question I have is whether severely high real home prices will hold at least moderately from here. The historical work of Robert Shiller would suggest this is now a key question:

https://fred.stlouisfed.org/graph/?g=AuPM

January 15, 2020

Shares of Gross Domestic Product for Private Fixed Nonresidential & Residential Investment Spending, Government Consumption & Gross Investment and Exports of Goods & Services, 2020-2022

(Indexed to 2020)

https://fred.stlouisfed.org/graph/?g=QKkZ

January 30, 2018

Case-Shiller Real Home Price Index and 30-Year Mortgage Rate, 1992-2022

(Indexed to 1992)

“As some have since telegraphed in public, US Federal Reserve officials concluded in private earlier this month that they should soon moderate the pace of interest-rate increases, likely leaning toward a 50 basis-point hike in December. And while some economic observers have predicted a recession with near certainty for months, Fed staff told officials during a Nov. 1-2 gathering that their assessment of the risk is about 50-50.”

So they finally decided to moderate their interest rate hikes. Maybe it is time to REVERSE some of these hikes since the likelihood of a recession is getting very concerning.

BTW – data reporting query. When does the BEA tell us about 3rd quarter GDI?

November 30 the site seems to indicate.

“PGL” raised a significant question about copper pricing and a premium price that is paid to Chile by China for copper imports. China is the largest producer and consumer of copper, also China imports copper. China has a copper futures market in Shanghai and does not use the London Metal Exchange for buying imports. Rather China pays a premium for copper directly to Chile rather than paying fees to London. China saves, Chile gains:

https://www.globaltimes.cn/content/1207271.shtml

November 18, 2020

International copper futures to start trading in China

Contract helps hedge risks, increase pricing power

By Ma Jingjing

Now you may have thought Tucker Carlson and the other MAGA hate mongers are awful to the rights of

https://www.msn.com/en-us/news/world/russia-passes-answer-to-blinken-gay-propaganda-law/ar-AA14vXaq?ocid=msedgdhp&pc=U531&cvid=6b85c238a27744dcb5f929fb97dc1bfc

Russia’s lower house of parliament has unanimously voted to extend its ban on so-called “gay propaganda”. Under the latest version of the law, any promotion of homosexuality – including in books, films and online – is illegal and carries heavy penalties. It was nicknamed the “Answer to Blinken” law, after the US Secretary of State Antony Blinken criticised it as a “blow to freedom of expression”. Activists say it is a further attempt to repress Russia’s LGBT community. It was approved by 397 votes to none in the Duma – Russia’s lower house – with no abstentions. The bill still has to pass in the upper house and be signed off by President Vladimir Putin, but this is largely seen as an administrative step.

Yea – Putin is this disgusting. I would ask if Putin’s pet poodle JohnH agrees with this homophobia but he has already indicated he does by mocking the World Cup athletes who had hoped to protest state sponsorred homophobia. So yea expect JohnH to be a guest on Tucker Carlson’s show. MAGA.

Why shouldn’t I root for recession, because it means less logging?

Root for whatever you want. Your wishes don’t matter to reality. Much like reality doesn’t seem to matter to you.

Fed staff make their assessment. We need not take that assessment at face value. Recession prediction is, as Bill at CalculatedRisk once wrote, a mug’s game. Nobody does it well, as evidenced by the Fed’s own record, gleaned from FOMC minutes. Fed staff and policy-makers don’t have an impressive record and most often err by not anticipating recession.

What might one suspect when Fed staff sees a 50/50 rsk, based on this record? Given the Fed’s tendency to underestimate recession risk, perhaps the actual odds are higher than even.

The staff assessment is predicated on assumptions, including that monetary policy will proceed according to recent FOMC communication – so not necessarily according to market expectations. As of the September SEP, the median estimate for the end-2022 Funds rate was 4.4%. The current effective funds rate is 3.83%, so as of the time of the November minutes, staff was probably working with an assumption of a 60 basis point rate hike in December – realistically, 50 bps.

From the minutes –

Staff:

“With inflation remaining stubbornly high, the staff continued to view the risks to the inflation projection as skewed to the upside…The staff, therefore, continued to judge that the risks to the baseline projection for real activity were skewed to the downside and viewed the possibility that the economy would enter a recession sometime over the next year as almost as likely as the baseline.”

Participants:

“Participants generally noted that the uncertainty associated with their economic outlooks was high and that the risks to the inflation outlook remained tilted to the upside…A number of participants judged that the risks regarding the outlook for economic activity were weighted to the downside, with various global headwinds being prominently cited.”

The staff assessment is that recession and inflation are likely. Somebody is covering their backside. The policy-maker view is that risks to the economy come from abroad. So not from Fed policy?

One more quote:

“Participants generally noted that the uncertainty associated with their economic outlooks was high and that the risks to the inflation outlook remained tilted to the upside.”

Yeah, yeah – upside inflation risk. But note the bit about uncertainty. This, I think, accounts for the odd views expressed by staff and participants. They know they’re groping in the dark.

I often have to fight the temptation of attempting to read Menzie’s mind and/or put words in his mouth. But it seems like to me Menzie is saying here he believes there WILL BE a recession, even if he’s not ready to tag the timing yet.

I’m not ready to say yet myself, but if there is one, the Fed deserves 75% of the blame. Because it wasn’t necessary, and rate hikes don’t solve supply chain problems.

Moses,

As someone who actually knows Menzie, I think he is pretty straightforward. His bottom line seems to be to agree with the Fed staff that the chances are about 50-50, period.

Well, this is the number back in August along with a statement from the man’s own paper:

“For context, a reading as high as 42.5% had a false positive rate of 6.8 percent and a true positive rate of 70.4 percent between 1979-2021. Meaning, the model-implied probability of a recession occurring in the following year is likelier than not.”

Now if the true positive is 70% on a 42% reading on Menzie’s and Mr. Ahmed’s model back in August, what is the true positive rate on a 56% reading on Menzie and Mr. Ahmed’s model?? I certainly would be fascinated to know. As Menzie is all too aware, I am too lazy to (and at least in the current context lack the mathematical skill set) to do the math.

Do you “know” Menzie better than me?? I don’t think you’re particularly perceptive about people, much less have a half-decent amount of self-awareness of yourself and how you come across to people. I doubt if even meeting the man in person told you a lot. So, if your knowledge over whether Menzie chews his dinner with his mouth open or chews his dinner with his mouth closed gives you telepathic insight here, I give you the slow hand clap.

Moses,

Oh dear, have you got an upset stomach from too much food yesterday?

Have looked at the paper and admit to being a bit mystified by the statement you quote, which states numbers that do not appear in Table A.1, although I guess that table supplies the model that somehow generated those numbers. While presumably his conclusion that a 42.5% probability based on this model means “a recession in the following year is likelier than not,” I do not think it means that it is as high as 70%, but I could be wrong, and Menzie xan certainly clarify if he wishes to. I find that remark in the paper confusing, frankly.

As it is, it may be correct that he sees the probability as slightly greater than 50%, but I think not by much. He argues that the FTS is a better forecaster than USTS, apparently working through trade, with U”STS predicting investment better than the FTS. The two USTS numbers are near 50% but below it, which leads him to say that they are close enough to justify the Fed staff predicting at 50-50, and he does not outright say they are wrong. He does say FTS is better, and reports a 56% from it, which is indeed above 50%, thus perhaps justifying a claim that he is forecasting a recession, but it is not all that much above 50%, and is not 70%, and I doubt he is forecasting a probability that high or higher. If he were, I think he would have said so more clearly.

As for who knows Menzie better, well, Moses, I have met him on several occasions and had some fairly extended conversations with him, including last spring having him present a seminar at JMU I hosted to which you were invited, although that was by zoom. As it is, I have known Jim Hamilton for a longer time and had more such conversations with him than I have had with Menzie.

Happy Day After Thanksgiving.

@ Barkley

You know I don’t doubt you are sharp in some ways (you know how much it kills me to type that, right?? It might even give you a clue what I am partaking in now, to grant you that) Certainly you were sharp in your younger years. But how someone who is pretty sharp, cannot “get”, basically a binary thing~~ “false positive”, “true positive” is a mystery to me and why sometimes I don’t even read your comments, as my brain goes into a negative feedback loop, wondering what in the F— you could possibly be thinking.

“Nobody ever hears both sides of the story, except the neighbors”

—-David Lee Roth

Moses Herzog: I cannot attest to whether Dr. Rosser or you “know” me better, but I can attest to the fact that I have in fact met Dr. Rosser on two occasions IRL, and at least once virtually.

Menzie is remaining coy about just what he thinks the probability of a recession is next year, although his touting of the the better forecasting by FTS suggests he might stand on 56%. Again, FTS is seen as having the edge because it takes into account what is happening in other economies around the world, with the link between them and ours operating importantly threough trade. And as of now it indeed seems that much of the rest of the world is getting into very poor economic conditions, worse than ours. So it will not be surprising at all if their problems become our problems.

Hahahahha, Menzie, I tip my hat, you and Rosser, as colleagues you probably “relate” to each other more than you would me. Is that fair enough?? I mean hah. you greatly compliment me entertaining this conversation. I felt you were stating something about the recession, maybe if I had thought more, I would have taken your 56% as more indicating 50-50. But I cannot, BUT half entertain, you weren’t just trying to say “Yah I really just kinda agree with the FRB’s 50-50” but might have even just somewhat been indicating a faith in you and Ahmed’s own research, which seems to tilt strongly (in my personal view) to more than 50-50.

Moses Herzog,

Regarding what I was unclear about in Dr. Chinn’s remark you highlighted, it was not that I have somehow in my degenerate senility forfotten the difference between a fslse positive and a true positive. Rather it has ro do with the point of that remark at that moment in the paper. Indeed I did make what I think was a minimally correct interpretation, that it implied possibly a somewhat greater positive probability than the estimate, while not implying the full higher number you thought that it did.

As it is, I somewhat rapidly scanned the paper, looking for those numbers, which I may have missed, only finding them in the Conclusions. As it is, this smelled to me of something it probably was not, a caveat. You see, I have been and am an econ journal editor and have read thousnds of submitted papers, with many of those being revisions after reviews. The comment smelled a bit, although it may not have been, of a caveat stuck into a conclusion, which I have seen more times than I can count. As it is, the most immediate meaning of those numbers is that the model generating them is seriously not robust. This is exactly the sort of thing a reviewer might demand a report on, and in a case such as this when the model being presented is in fact t robust, one notes it briefly in the Conclusions with something to offset the problem, such as noting this asymmetic outcome might indicate a somewhat higher probability than estimated. As it was, a further lack of clarity was whether this applied to the FTS model as well as the USTS, which it looked like was the one specifically referenced. So this is what I would have liked to see clarified, while in fact viewing this as kind of a minor point, even as you emboldened it and made it into a big deal, including asserting I think without good evidence that this meant that the 56% number should also be viewed as higher.

As it is, the paper has a lot of other interesting stuff in it that Dr. Chinn did not mention. Thus while FTS seems to forecast recessions in the US better than USTS, the latter leads the former, forecasts it better than the latter. This suggests an arguably peculiar outcome Dr. Chinn did not mention: USTS forecasts FTS, but the FTS forecasts US recessions better than USTS. This is a bit odd, frantkly.

BTW, I skimmed the paper somewhat quickly because I am under a deadline to complete a paper for special issue in a somewhat mathy journal that is ranked about where the one Dr. Chinn coedits is. If you want to continue to point out my creeping senility, which some years ago you lumped mw with Pelosi and Biden as suffering from, I would say that my declining ability to remember names of people is a much bigger problem than the gradual decline of my math ability is. Not ready to shut down the shop on the latter yet.

Oh, and it occurs to me that Dr. Chinn decided to refer to me as “Dr. Rosser” because yet again someone has called him by his first name while calling his c0=blogger by his professional title, something that Dr. Chinn has openly expressed frustration here regarding.

Oh, and we have only had lunch together, not dinner, at a restaurant on State Street in Madison, iI forget which one, oh awful incipient senility! No, he did not chew in some odd way.

Barkley Rosser: (1) the specification and data are not exactly the same as in Ahmed-Chinn (I use a simplified FTS, and *exactly 12 months ahead* instead of *within 12 months* specification. (2) Casa de Lara as I recall, indeed on State Street.

Oooops! Bad proofreading. Where I said “is in fact t robust” that should have been “is in fact not robust.” Of course, Dr. Chinn can either correct or clarify on all this as necessary, although I think this matter s indeed pretty much of a sideshow of not much importance.

BTW, Moses, I have fully and openly and repeatedly accepted what you have occasionally claimed what you find most annoying about me, my egomaniacal arrogance. I am guilty guilty guilty indeed, and no amount of claims that I am senile and the taxpayers of Virginia should have me fired will cure me of it. I have also repeatedly suggested that if we actually were to meet, we would get along, seeing eye to eye on many things. I would readily admit my faults and laugh about them, doing even more so heartily after quaffing some beverages, although perhaps you would continue to bear all kinds of annoyance with me for all my giving you hard times about this and that. But, probably will not happen, so you can continue to try to reform me or at least expose me yet again for all my flaws.

Professor Menzie Chinn,

Thank you for the clarifications.

As it is, I did remember that where we ate was on the south side of State Street. Thus I knew it was not the Sunshine Kitchen on the north side, where I have lunched with Buz Brock. But it might have been Tutti Pasta where I used to lunch with the late Don Hester or the I think now defunct Afghan restaurant closer to campus where I used to lunch with the late Len Weiss. As it is, I like Casa da Lara, although have not eaten there in quite some time.

But, uh oh, there I go again dropping names when as has been made clear by a particularly astute expert on me, I am not “particularly perceptive about people,” an opinion probably held because I have criticized him so harshly at times in personal terms, obviously without any cause whatsoever.

Why not just look at the underlying forward rates to see if markets are pricing in a recession via the ZLB? Forwards right now are consistent with the FRB dot plots and soft landing.

H: What’s the track record for your approach? (I.e., how many recessions has this approach had the opportunity to predict or not.)

Today, I am thankful for too many things to innumerate. But what I would like to say here is that I am thankful in America that generally we have the free flow of information, that we still have one of the better higher education systems in the world, and that we have peoples like Menzie and Professor Hamilton who have the grace and generosity to share their knowledge and intellectual talents with us.

And also we have some smart people in the comments that are willing to give allegorical punches and receive allegorical punches, not always taking it in a personal fashion, and the disagreements will keep us still “turning things over” and changing our views hopefully closer to reality and truth, over time.

That’s all from philosophical Mr. Sponge Bob for today.

FRB economists find forward rates to have greater explanatory power than typical term spreads, per the paper below. The intuition is much stronger as well as it gets to the heart of the question of what the bond market is predicting in the near term without as much distortion from term premiums that are more pronounced at the long end of the curve. While I favor this over other term spreads, I still think it helpful to plot the entire forward curve rather than focus on a spread. For example, forward rates being lower than current rates can still be benign if the market is pricing in a soft landing. Forward fed funds and 1m SOFR rates are currently consistent with FOMC median projections where rates eventually come down with inflation to a more equilibrium rate, not the zero lower bound that a recession would suggest.

https://www.federalreserve.gov/econres/feds/the-near-term-forward-yield-spread-as-a-leading-indicator-a-less-distorted-mirror.htm

H: Agree entire yield curve is informative, at different horizons.

https://www.federalreserve.gov/econres/notes/feds-notes/there-is-no-single-best-predictor-of-recessions-20190521.html

At 12 months, I think 10yr-3mo, 10yr-2yr is pretty informative.

my tiny contribution to the yield curve reflects agreeing with bonddad/new dealdemocrat iow we upgraded our prediction from recession ‘watch’ to ‘warning’ timing for me is may – june 2023.

as yogi berra said ‘predications are hard, especially about the future’

my second favorite rule of investing