CPI services, services ex-energy, core services ex-shelter, vs. core and core commodities.

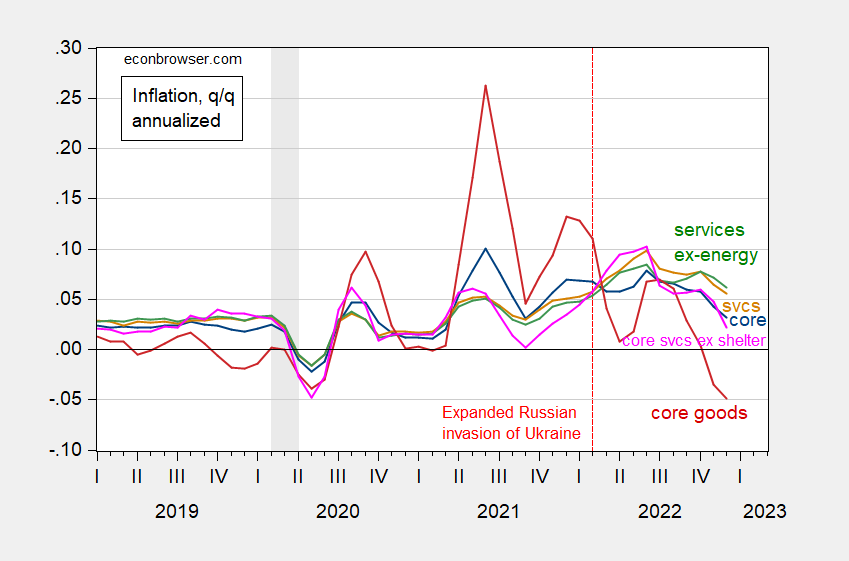

Figure 1: Core CPI inflation rate (blue), core goods (red), services (tan), services ex-energy (green), core services ex-shelter (pink), all s.a., q/q at annual rates. NBER defined peak-to-trough recession dates shaded gray. Source: BEA via FRED, Pawel Skrzypczynski, NBER, and author’s calculations.

To me, q/q inflation rates are generally declining, while core goods are experiencing deflation.

Addendum:

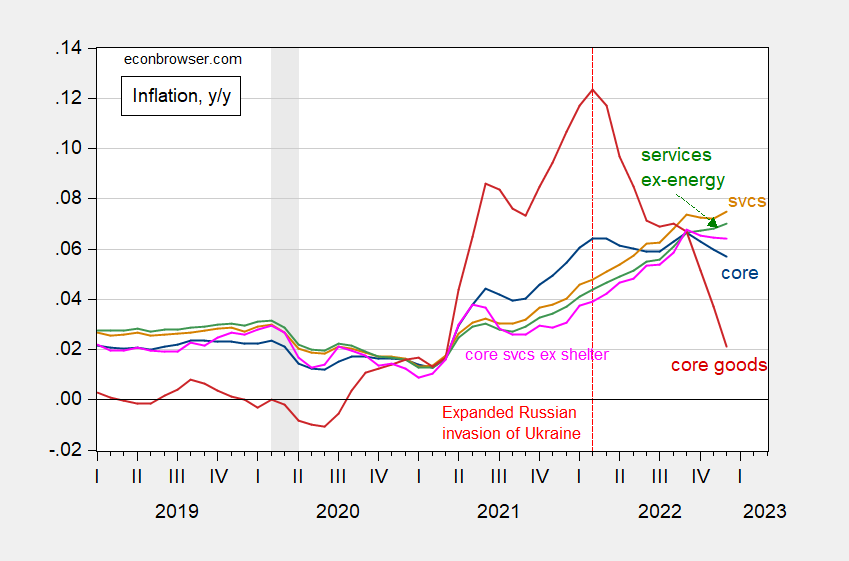

Here are year-on-year rates:

Figure 2: Core CPI inflation rate (blue), core goods (red), services (tan), services ex-energy (green), core services ex-shelter (pink), all s.a., year-on-year. NBER defined peak-to-trough recession dates shaded gray. Source: BEA via FRED, Pawel Skrzypczynski, NBER, and author’s calculations.

core services ex-shelter (pink) has gotten a lot of attention of late. The grown ups here likely remember why. But of course we were told by Jonny boy that the inflation rate for services is still over 7.5%. That does not seem to correspond to your informative graphs. And yes we are seeing good price deflation. Now I get the weight for services is lower than the weight for services, but I doubt there is any weighting scheme that would justify that 13.3% inflation claim Bruce Hall is still defending.

Hey Brucie – please mansplain for us average folks how you do your magical weighted averages!

pgl: Year-on-year services (total) inflation is 7.5% (not over 7.5%, unless going out to 4 significant digits). But looking at y/y hardly seems appropriate if you are looking at turning points. Year-on-year graph to follow.

Thanks. This is the point Alan Blinder ably made as I noted in a link to his oped. Of course Bruce Hall and JonhH refuse to read this piece!

Jonny boy tried to school me with something that said part of the reason reported service inflation was not higher was because health care costs fell. Now most of us would see that as a good thing but not Jonny boy.

More importantly – his own link had a long discussion with respect to the way shelter costs are being measured. Which is rather important as its weight was reported as being over 30%. I guess Jonny boy has not seen all those discussions that suggest the BLS measure may be overstating this issue. Yea – Jonny boy has trouble keeping up with even basic accounting issues.

Yes, pgl. It would be good if health care costs fell. But a wise man once said that, “it pays to understand the data.” In fact, healthcare costs did not in fact fall. What caused the apparent fall “a massive mega-adjustment by the Bureau of Labor Statistics in the CPI for health insurance. And it came on November 10.

Everyone knows that the costs of health insurance didn’t plunge in October from September. But because of the periodic adjustment, the CPI for health insurance plunged 4.0% in October from September, a 6.1 percentage-point swing from September (+2.1%), according to data from the Bureau of Labor Statistics today. This was by far the biggest month-to-month plunge in the BLS data going back to 2005, and far outstripped the adjustments in prior periods…

The adjustment will carry forward for the next 12 months, meaning that health insurance CPI will be negative on a month-to-month basis for the next 12 months to work down the overstatement for the past 12 months…

The CPI for health insurance accounts for 0.9% in overall CPI and for 1.1% in the Core CPI. And the plunge on November 10 pushed down the overall index, and even more the core CPI and the services CPI.”

https://seekingalpha.com/article/4556323-services-inflation-spiked-to-second-highest-in-4-decades

JohnH: What exactly is the significance of “And it came on November 10.”?

Don’t expect Jonny to know what the fellow at Seeking Alpha meant. He just cuts and pastes words he never understood. Another version of Bruce Hall disease.

us marine corps’ birthday….

November 10 was the date when the BLS released the October CPI and the health insurance adjustment first showed up.

BLS changes are explained here.

https://www.bls.gov/cpi/factsheets/medical-care.htm

JohnH: But you wrote “November 10” as if the date of release had a special significance. I really don’t understand why that is so important. Just say “the October 2022 release” then.

You’ll have to ask Richter about his choice of words. I have reviewed his numbers. As far as I can tell, they are accurate with the caveat that I can see neither his specific source data nor his work. Of course, this is also true of the graphs above.

What I can say is that Richter did over-sensationalize a fairly trivial factor. Regrettable as that may be, I can note that as behaviors go, I have seen a lot worse—unprovoked insults, smears, lies, and character assassinations, that occur pretty much on a daily basis without comment.

JohnH

January 20, 2023 at 7:38 pm

You’ll have to ask Richter about his choice of words. I have reviewed his numbers. As far as I can tell, they are accurate with the caveat that I can see neither his specific source data nor his work.

So jonny finally admits he reproduces trash without verifying the supposed data. Good to know!

BTW – BLS has had two more releases since it published its October statistic. This release was on 1/12/2023 showing Dec. 2022:

https://www.bls.gov/news.release/cpi.nr0.htm

Note Medical care services fell by another 0.7% in November and rose by only 0.1% in December. Now we all know why Jonny boy is citing some Seeking Alpha discussion that is two months on. He does not care to tell us the most up to date figures as that would just ruin his latest rant.

“Everyone knows that the costs of health insurance didn’t plunge in October from September.”

And everyone knows that CPI-services rose by less than 0.6% over the same period. Hey Jonny boy – takes for admitting you cherry pick the data.

Medical services dropped in Q4? It doesn’t pass the smell test. Never happened before. The measurement adjustment is much more plausible explanation than the silly notion that medical services costs actually fell. I mean, have you seen any doctors advertising discounts?

https://fred.stlouisfed.org/series/CUSR0000SAM2

Ladies and Gentlemen, we have comedy gold for you! You’re gonna love this. Heeeere’s Johnny!!!

“Medical services dropped in Q4? It doesn’t pass the smell test. Never happened before.”

But it did happen, just two years earlier. Medical services costs dropped in Q4 of 2020, in the very data series Johnny linked to:

https://fred.stlouisfed.org/graph/?g=Z1qE

So, Johnny lectures pgl about understanding the data, and Johnny gets the data wrong. How embarrassing. But never mind that. Johnny is lecturing pgl on understanding the data while relying on some other guy’s analysis of data that Johnny can’t find! Even more embarrassing. What doesn’t pass the smell test? Johnny doesn’t pass the smell test!

Want more laughs? Here’s a little something Richter didn’t mention, so Johnny didn’t know:

“In October 2022, the retained earnings calculation began including premium and benefit expenditures for Medicare Part D. Previously, these Medicare Part D expenditures were not included.”

Could the inclusion of Part D in the insurance index account for the drop? Dunno, but it could, and anyone who ignores the change doesn’t understand the data. This quote, by the way, is from one of Richter’s links, so Johnny could have known, but Johnny doesn’t bother to understand the data. He relies on Richter.

We’re not done yet! What else is going on? Well, 65 million Medicare beneficiaries will pay lower premia and lower deductibles in 2023. When would this show up in CPI health insurance? January would make sense, but there’s no adjustment in January. The adjustment is in October. So maybe that drop in health insurance costs is based on – ready? – a drop in health insurance costs!

Now, I haven’t called BLS to find out which month introduced the premia and deductible cuts, so I won’t claim to “understand the data”. I will, however, fearlessly assert that I understand the data better than Johnny. Johnny missed a cut in health insurance premia for 65 million people. That’s 21% of the insured population.

You can’t make this stuff up!

JohnH

January 20, 2023 at 6:42 pm

Medical services dropped in Q4? It doesn’t pass the smell test. Never happened before.

https://fred.stlouisfed.org/series/CPIMEDSL

Consumer Price Index for All Urban Consumers: Medical Care

Gee Jonny – this series dropped by a similar amount in 2020QIV. But you claimed this has never happened before?

Damn – you have this habit of saying some really stuoid things before checking the data. Your comments never pass the smell test.

Thanks Macroduck. The difference between presuming something is fishy because it “never happened before” and actually digging into and trying to understand why a number seems out of line – is why I consider you a credible source of information and insights.

It is very rare that trackable information doesn’t have a logic explanation for anything unusual. However, it requires a knowledgeable person spending some time, to find that explanation. Any lazy idiot can simply imply that there is something wrong with data if it has a variability that is not supporting their favorite narrative..

Wolf Richter says “everyone knows”? Dude – you rely on total hacks way too much. Learn to do some real research using actual data and not some Wall Street wolf’s bloviating. Damn!

Why doesn’t pgl do some research to refute Richter instead of just throwing insults left and right.

“The adjustment will carry forward for the next 12 months, meaning that health insurance CPI will be negative on a month-to-month basis for the next 12 months to work down the overstatement.”

I’m pretty sure that Richter misstated what’s actually going to happen over the next 11 (not 12) months. The health insurance index probably won’t be negative “on a month-to-month basis” over that period. It is very likely to be negative on a y/y basis in each of those months, which is a rather different thing. That’s how once-a-year adjustments work.

Do keep in mind that if the health insurance index is going to understate y/y insurance price changes for a year, it’s because the index was overstating insurance price changes in the prior year. Can’t be all fussy about one without being fussy about the other, now can we?

And yes, the PCE deflator doesn’t have this problem. So let’s all take a breath…

“Can’t be all fussy about one without being fussy about the other, now can we?”

Exactly! Isn’t it funny that it cites this Seeking Alpha clown verbatim without bothering to check the supposed data. That is our job I guess since Jonny boy does not know how.

Macroduck

January 20, 2023 at 8:53 pm

Ladies and Gentlemen, we have comedy gold for you! You’re gonna love this. Heeeere’s Johnny!!!

That was a world class take down. Thank you!

https://www.piie.com/blogs/realtime-economic-issues-watch/how-improve-measurement-housing-costs-cpi

How to improve the measurement of housing costs in the CPI

David Wilcox (PIIE)

December 20, 2021

New data could be used to improve the measurement of housing costs in the consumer price index, or CPI. Ordinarily, the housing-related components of the CPI are among the stodgiest, least-noticed elements of the index. But they constitute an astonishing 31 percent of the overall index

One of the papers revisited this issue. Note this paper was written over a year ago and yea it noted shelter costs would surge in early 2022 which is what BLS is now picking up. But wait – we are talking about inflation over the past 6 months where it is highly likely that actual shelter costs are falling relative to what BLS is reporting.

Something the grown ups here are following whereas people like Bruce Hall and JohnH either ignore or misrepresent.

Yet another unprovoked and gratuitous insult from pgl.

Personally I’m all for reducing the rate of inflation…it helps raise real wages and protects consumers’ purchasing power.

BTW I am well aware of the problems with the measurement of housing costs.

“I am well aware of the problems with the measurement of housing costs.”

And yet you cite a statistic that is heavily weighted by a questionable number? Go figure.

Yet another string of unprovoked, gratuitous insults from pgl.

Unprovoked? You’re kidding, right?

In a previous post you were positive about deflation. Have you changed your tune? Because at that time you were griping that reducing the rate of inflation still could lead to inflation, which wad bad. Now it seems acceptable to you. Which is it. You are posting contradictory preferences.

Thanks for adding core services ex shelter.

One thought on deflation of goods. This is mainly pulled by used cars and trucks. Conditional on Manheim index changes this deflation is likely to somewhat fade over Q1: https://twitter.com/p_skrzypczynski/status/1616434277305958402?s=46&t=pGXm9cJngI_-LTEptw0-pA Overall I guess we still deal with high uncertainty to inflation outlook. Ofcourse disinflatiin will continue but there might be a lot of surprises to the pace of it on both upside and downside.

Your point about higher uncertainty is widely applicable and needs frequent repetition. Policy making, business planning and governance are all harder now than prior to Covid and Russia’s war.

Based on recent price cuts by tesla, we will see similar deflation in new cars through 2023. My wife is now looking seriously at a new car. And tesla just went up the list. She is considering an EV over gas, and favored a benz until the tesla price cuts came by.

Three class people who are the better part of this blog in continuum comments. : ) this would be the “ideal” of the blog comments section. Sorry I messed it up like a newborn puppy at the last : )

Off topic, long Covid and income –

A medical researcher (Daniel Kim, Northeastern) has taken a crack at estimating the differential impact of long Covid on various population groups, and has added an estimate of the annual loss of income due to long Covid:

https://www.medrxiv.org/content/10.1101/2023.01.06.23284199v2.full.pdf+html

As a back-of-the-envelope effort, it ain’t bad. His estimate is an annual loss of $175 billion in income. What the author did not do is address the “Is that a little or a lot?” question. By my calculation (also back-of-the-envelope), that amounts to a 0.7% annual loss in household income from long Covid.

Not surprisingly, this is another area in which being non-white, poorly educated or marginally attached to the labor force compounds problems.

Your last sentence is giving the idea we should feel empathy for these people. Boy, you are a strange character. Or should I say rare character?? : )

Off topic, Biden’s foreign policy:

Foreign Affairs has asked 20 policy experts to assess the first two years of the Biden admnistration’s foreign policy:

https://foreignpolicy.com/2023/01/19/biden-2-year-report-card-foreign-policy/

Y’all can decide for yourselves whether there is more good than bad in Biden’s record so far. A few things are clear. One is that Biden is bringing profound change to U.S. foreign policy. Another is that he is achieving the intermediate goals he sets. Yet another, related to achieving stated goals, is predictability. Even when Russia initiates a substantial policy change, Biden sticks to plan and (thanks to Blinken, Yellen, Milley and others) leads democratic allies in a largely consistent set of policies. So, while one may disagree on goals, competence is clearly in evidence.

Biden is given high marks on environmental issues, which is a sad statement about the “art of the possible”. He has accomplished more than his predecessors in part because his predecessors accomplished too little.

Obama came to office in the midst of an economic and financial crisis, won a second term and enjoyed widespread approval. (Clinton, too, though the recession was smaller.) It’s early days for Biden, and it’s hard to top breaking the race barrier and massively restructuring the U.S. health insurance system, but Biden looks like he’s winning himself a place in history comparable to Obama’s, based on his foreign policy scorecard and legislative successes with very small legislative majorities.

From BOA:https://www.yahoo.com/finance/news/stock-market-flipped-upside-down-155256976.html

ProLiberalGrowth still can’t figure out how there was about 13% inflation between January 2021 and June 2022, but he can figure out how inflation was about 1% between June 2022 and December 2022… using the same approach. I guess when you have an administration to defend, you can be deliberately obtuse.

https://fred.stlouisfed.org/series/CPIAUCSL

Bruce Hall: And here I thought inflation was a “rate of change”. Wouldn’t it have been more precise to say the price level change was 12.6% going from January 2021 to June 2022; and that the annualized inflation rate over that period is 8.8%. That’s how I would discuss terms with my fellow economists. Am I daft?

Okay, we’ll speak to 12-month point in time to point in time (or one month to month x 12) change as “rate” which is expressed in % and any other point in time to point in time as “price level change” which is expressed in %. Thanks for showing the folly of my thinking. I guess that pgl’s expression of inflation from June through December should be “price level change”, eh?

btw, pgl insists on using 13.3% which is what I wrote on my initial comment regarding this “price level change” based on data not seasonally adjusted. After his “correction of my thinking” I used the Fed’s seasonally adjusted data which was 12.6% from January 2021 to June 2022. Of course, we all know that the end points of seasonally adjusted data are subject to revision as the seasonal factors are recalculated over time. So maybe after several months that number may be 12.4% or 12.8%. But the issue is not the exact percentage change but the general magnitude of that change and how that relates to subsequent (June-December) change. June appears to be the point of discontinuity which is not generally featured in the yr/yr numbers, but has to be gleaned.

WTF are you are babbling about now?

Look CPI rose by 0.9% over the last 6 months which I properly annualized to 1.8% per annum. See – this is simple except for someone like you who wastes all of our time spinning around in circles like a retarded dog.

Come on Bruce – relax and take the weekend off. You are working way too hard to prove the obvious – that you are a worthless idiot. We all knew that a long time ago.

You can annualize if you wish. It is not necessary as long as the timeframe is specified. You should be able to understand that. Even Joe Biden said inflation has been basically flat for the last six month sand he has an army of economic advisors to write his scripts. I’ve been agreeing with that, so what’s your problem? Oh, you don’t like me using inflation over 18 months because it breaks your little comfort zone. Tough. It’s still accurate. Rate of change versus price levels? Come on, man! Rate of change is calculated by dividing an end point by a starting point. You just want to insist on annualized data because it makes you comfortable and, in this case, hides the bigger impact during the Biden Administration. You’re very conservative in your thinking. Maybe even ossified.

Look at your favorite hobby topic: climate. What’s the average temperature change over the past decade? Thirty years? 100 years? Since 1880 when records are generally recognized as “official”? Different staring points. So, if the average change over 100 years is 1.5 degrees and over the past 30 years it’s 2.0 degrees can you see the value of that? Come on, man! How about from 1900-1950, 1950-1990, and 1990-2022? Different starting points, but still understandable and telling the story.

So what’s the big deal calculating inflation over 18 months and then the next 6 months when it clearly tells the story?

Bruce Hall: Well if you use NSA for the first 18 months (I count 17, but who cares), and then SA for the next six, isn’t that kinda mixing and matching?

pgl, I know what’s bothering you and Menzie. You want everything expressed as either an annual or monthly change rate. I don’t feel constrained by that arbitrary limitation. If there was 12.6% or 12.5% inflation over 18 months, that’s clearly understandable. I don’t have to take that and divide by 18 and multiply by 12 to make it an “annualized” figure. Maybe you do to feel comfortable. See my previous reply regarding temperature changes for differing timeframes. Feel free to call that change in price levels if it makes you more comfortable.

But then I’d like you to express global average temperature change as annual rates of change also.

Bruce Hall: If you look *at the graphs in this post*, you will see that those are *quarterly* inflation rates expressed at an annual rate.

Also, it is just plain nonsensical to do 17 month changes on not-seasonally-adjusted data. Each time you do it, I will flag it and/or do a post on it (do you remember this post, which did not take into account seasonality).

Menzie,

First, I initially use data that was not seasonally adjusted and then switched to seasonally adjusted data… wrote that several times.

Secondly, why is it “nonsensical” to use any timeframe other than annual, quarterly or monthly? For any other metric, one can designate a timeframe for the reason that it shows during that period a unique trend. If, during a year, inflation (CPI) is rapid for half the year and stable for the other half, citing an average for the year misses the dynamics.

That’s like saying the average death rate from COVID is 2% but it was 3% initially but now is 0.5%. The average is misleading.

“Rate of change” is, by convention, an annualized rate over whatever period is being discussed. An annualized change over 3 months, 6 months, twelve months. A 12-month percentage change in level is a special case, in that it is equal to the12- month rate of change.

While your failure to use the language correctly is a problem, the greater fault is in picking your end-points in order to show the greatest level change possible and then to note the level change rather than the annual rate of change. Both of those choices exaggerate inflation, and since that exaggeration fits your political bias, the choice to exaggerate looks intentional. Dishonest. Disingenuous. Bovine droppings.

Macroduck, I appreciate your discomfort with me breaking convention, but convention doesn’t always tell the story accurately. During the past two years, there were two distinct periods of inflation. Using yr/yr “convention” may show the rate of increase decreasing, but it doesn’t tell the story that there has been an abrupt change in the middle of last year.

The Fed is still locked into the yr/yr convention, so it is still fighting inflation that stopped 6 months ago. I’d think that economists would want to have a better feel for the problem than saying we had 6.5% inflation in December (vs. last year). We did, but we didn’t really have inflation of any import since June. So monetary policy is pushing us into an economic slowdown when the inflationary problem has abated. Why are you, pgl, and Menzie so dead set against viewing inflation from a different perspective?

You’ve locked yourselves into a very esoteric way of thinking that communicates badly the reality of what is happening. You’re telling everyone that inflation is 6.5%, but if someone says not for the past six months, you respond with “you’re not using the language correctly”. No, your language is not reflecting reality correctly. According to the CPI, there has been hardly any inflation for the past six month… even with an end value of the index that is subject to recalculation. That’s the reality. The other reality is that for the 18 months prior, average prices increase almost 13%. Cutting off six months for “convention” doesn’t tell the whole story.

Brucey is pretending to read minds again. He needs me to be uncomfortable so he doesn’t have to be. And he claims that doing the math wrong is Oh! So cutting edge!

Then, Brucey claims the Fed is “locked in” to year-over-year inflation. Really? All the Fed guys I ever dealt with were really good at this turning-points, moving-average-model stuff. The Fed research I’ve read seems a good bit more sophisticated than being “locked in” to a single measure of inflation. If one were to check some of the regional Banks’ alternative inflation measures, one would find one, three, six and twelve month measures of inflation. No 18-month measures, though.

But maybe Brucey can tell us where he gets the idea that Fed folk only care about year/year.

Brucey also keeps insisting on focusing on inflation between a half year and a year-and-a-half ago, rather than more recent months, and pretends others are being obtuse when they point out how badly he hasmessed things up.

Best of all, there’s this:

‘You’re telling everyone that inflation is 6.5%, but if someone says not for the past six months, you respond with “you’re not using the language correctly”.’

Horse Heaps! pgl has repeatedly cited inflation inthe second half of the year. I’ve man-splained very carefully to Brucey about annualizing rates over various periods. I’m pretty sure I have never written that inflation is 6.5%, at least not in this century. Menzie? Menzie is stuck in an unclear communication frame? Holey hockey pucks, Batman!

Brucey, stop digging, for goodness sake. Pretending that your lame effort to make inflation seem really, really bad is actually an attempt shining new light on the data is sooo three mistakes ago…

Bruce Hall

January 20, 2023 at 7:06 pm

Macroduck, I appreciate your discomfort with me breaking convention, but convention doesn’t always tell the story accurately.

Seriously? You never strive for accuracy or clarity. All you do is to write in a way that pleases your boss Kelly Anne Alternative Facts Conway.

Hey Brucie – Macroduck provides the best summary of what you did:

While your failure to use the language correctly is a problem, the greater fault is in picking your end-points in order to show the greatest level change possible and then to note the level change rather than the annual rate of change. Both of those choices exaggerate inflation, and since that exaggeration fits your political bias, the choice to exaggerate looks intentional. Dishonest. Disingenuous. Bovine droppings.

Keep on trying to defend your droppings here. It amuses the rest of us!

I have this strange feeling that Brucie has spin himself around so much that he does not even know how to get home. Call someone call the police and make sure Brucie does not hurt himself?

“ProLiberalGrowth still can’t figure out how there was about 13% inflation between January 2021 and June 2022”

About? Why do rounding Brucie. Oh yea – your dodgy source said 13.3% but BLS says 12.5%. The only thing I can’t figure out is why you insist on reminding us of your incessant stupidity. No we are not using the “same approach”. You are a Kelly Anne Alternative Facts type whereas I live in the real world and write clearly.

Bruce Hall: I *am* curious. How was the 13.3% number calculated? What CPI was being used?

I used the *not* seasonally adjusted CPI originally. I did change that to 12.6% using the Fed’s seasonally adjusted data which I have referenced several times.

Bruce Hall: I repeat: “Why would one ever want to compare NSA Jan 2021 to June 2022 (NSA Jan 2021 vs Jan 2022, sure…)” That does nothing but confuse people.

You FINALLY figured that out! Good boy little Brucie boy.

Brucie was proud he pulled some cite that claimed it was reproducing BLS data but provided no explanation why its data did not match the seasonally adjusted CPI data presented by BLS or FRED. I asked Bruce WTF this weird source was presenting. He had no clue. But I did match it to the NSA data BLS provides.

The Blinder oped I have been noting (Brucie had to read it) advised against using NSA data when using periods either shorter or longer than 12 months. Of course Brucie still has not got that point or any of the other points Blinder made.

Looking at the BSL CPI-U index table January 2021 is 261.582 and June 2022 is 296.311. The change is 13.3% (non-seasonally adjusted).

Joseph: Thanks. Why would one ever want to compare NSA Jan 2021 to June 2022 (NSA Jan 2021 vs Jan 2022, sure…)

This is what Bruce gets when he searches the web for weird ways of showing the data rather than relying on original sources.

I think you are presuming that “one” wants insights.

If “one” want to support a narrative of “big increase” then “one” will chose a starting point that is very low and and ending point that is very high.

It is the difference between seeking insights or seeking “support” for an already decided conclusion.

Apples to oranges to bananas. Not seasonally adjusted through November; seasonally adjusted through November; seasonally adjusted through December… but you knew that.

YOU did not know that. The high schoolers website you relied on did not know that. No old incompetent troll – I was the one who figured out what your bozo source had done. And so once again Bruce Hall wastes an incredible amount of time because he is incompetent at even the simplest of things.

Menzie, I repeat, I used the seasonally adjusted data from the Fed for the calculations.

https://fred.stlouisfed.org/series/CPIAUCSL

January 2021 = 262.2

… rapid inflation

June 2022 = 295.3 (rapid upward trend stops)

July 2022 = 295.3

… low inflation

November 2022 = 298.3

December 2022 = 298.1 (low increase since June)

I see a discontinuity of trends. Perhaps you do not. The 6.5% yr/yr for December is misleading in my mind even if it is “conventional”, especially for decision making regarding interest rates. That’s not to say that faster increases in the CPI won’t resume, but there has been low inflation for 1/2 year. If you disagree, please explain.

I seem to remember that in 2007 as the economy was grinding to a halt that the Fed was slow to recognize that with interest rates which didn’t start dropping until August 2007.

Bruce Hall: You really should read the old Burns-Mitchell papers on discerning cycles and trends. Sure, you see that trend using 18 month changes. Try 3 month changes (annualized)

‘Menzie, I repeat, I used the seasonally adjusted data from the Fed for the calculations.’

Now you are lying. Your starting comments on this thread used NSA data. Now you probably did not know that until I told you because you relied on the website of some high schooler who is rather incomplete in telling people his source data.

Damn Bruce – you started off owning your mistake but now you just flat out LIE about what you wrote? I guess since Trump lies all the time, it is OK for you too?

January 2021 = 262.2

… rapid inflation

June 2022 = 295.3

I was the one that used those SA adjusted numbers to say the increase was 12.6%. You kept telling us the increase was 13.3%.

Bruce Hall – serial liar.

No, pgl, just go back and look at the comments. You’ll find that after you pointed out the error of my ways regarding the use of NSA data, I went back and got the SA data and have used that in my comments since and have even provided the links. So, I give you credit for that. But that is no longer the issue. The issue is the appropriateness of using other than yr/yr or mo/mo data which is the “conventional” way of examining inflation. My point was and remains that using the yr/yr number of 6.5% inflation is misleading when the data from 6/22 through 12/22 is essentially very slow increase. You and I agree on that whether or not you want to recognize it. Even the POTUS agrees on that. But you are trying so hard to find a point of disagreement that you can’t get to the real point.

Whether or not the 1/21 through 6/22 increase was 13.3% or 12.6% only matters if you can’t get to the point that was the period during which inflation hit the hardest and after that inflation has subsided. Your technicalities work wonders for your ego, but get you trapped into not understand what is being offered as the bigger picture. That bigger picture is that the “conventional” way of reporting inflation is not a good tool for identifying a discontinuity in the momentum of inflation and certainly is not what the Fed should have been looking at since October which led to rate hikes of 0.75 and 0.50 pp. and may push the US unnecessarily into a recession.

The inflation damage was done when the Fed acted belatedly to try to tame it in 2021 and it looks like another mistake currently.

Perhaps in answer to one of my own questions, here’s a picture of retaile sales, total and ex-vehicle, alongside industrial production:

https://fred.stlouisfed.org/graph/?g=Z13n

Goods demand is soft; IP is soft. Service consumption, which would over-complicate the picture, is still rising.

Core PCE inflation, FRED series, PCEPILFE will be reported on Friday, January 27. So far, Bloomberg shows a m/m consensus forecast of 0.3%. Using FRED series, CPILFESL and PPIFES as regressors, I am finding a m/m % change of 0.22%, close to Bloomberg. At an annualized rate of about 2.6%, Core PCE is getting close to the Fed’s target.

As I understand, the FED favors the Core PCE inflation index, so maybe the next rate increase will be at 0.5% as forecasted on the CME Fed Watch site.

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

JohnH used to pretend he is the champion for the working class. He is not. He is more the gold bug fiscal austerity Rand Paul type. But that is an old story. Lately JohnH has been all upset the cost of services might be rising in nominal terms.

But wait – what are services. Since I just got a haircut at the best barber shop in NYC (since the pandemic I only go twice a year so this is a small weight in my CPI). Gee the price went up 4% since 6 months ago. Now I did not complain as these are hard working professionals who do a great job.

But my point is simple – that increase represented an increase in the wages of a working person. That is often what we mean by the cost of services. And JohnH must now either hate hard working people or this troll has no clue what he is talking about (as usual).

Now Macroduck recently told us that the cost of nursing services has been held down by hospital monopsony power. Then again Macroduck gets basic economics. JohnH does not.

meanwhile in wonderland:

“Alice quipped, “This sure seems like a strange non-recession.”

“Oh,” said Humpty. “In Wonderland, when you hint there may be a recession, you automatically agree to a debate”.

“Wonderland loves nothing more than a debate on recession,” said Humpty, adding “I will moderate and keep score.” ”

https://mishtalk.com/economics/alice-debates-the-mad-hatter-and-the-red-queen-on-timing-the-recession

Are you presenting this link because you want us to join you in ridiculing Shedlock?

It is odd that Mish writes about debate without engaging in one himself. He makes up a cast of characters, attaches real names to them, writes a script for them which misrepresents the views of the actual people named, all without inviting a capable opponent to present the other side.

Shedlock has a decent understanding of credit markets, nothing much to offer regarding economics and a big chip on his shoulder when it comes to politics and policy. No wonder you set him up for ridicule.

seriously?

I thought the cartoon was funny.

I skim Mish occasionally on twitter.

everyone has a point to make.

different ways of seeing

What concerns me about Core CPI as mentioned on a prior post is that over the past few months, the Core Commodities index has declined in percent about the same as the Core Services has increased in percent. My FWIW forecast for January is for Core Commodities to show a m/m increase of about 0.08% and Core Services to increase by about 0.58% m/m. Using data from the past several months and using Microsoft Solver, I calculated the optimized weight for Core Commodities at about 24%(rounded) and for Core Services at 76%(rounded). The weights were to optimize the % change fit of Core Commodities and Core Services to FRED series, CPILFESL% change. If my calculations are not totally off, then Core CPI would increase about 0.45% m/m for January 2023. I previously reported the January m/m change as 0.48% on January 12. The weights were tweaked a bit.

https://fred.stlouisfed.org/graph/fredgraph.png?g=Z16O

https://fred.stlouisfed.org/graph/fredgraph.png?g=Z17u

Looking at homeowners’ equivalent rent (OER), Core Services inflation could show a decline as home prices decline. Although home prices may not be the major factor in OER. Penn Mutual Asset Management cites a Cleveland Fed research study, “Research by the Cleveland Federal Reserve suggests the best predictor for OER inflation is recent OER inflation. In other words, OER momentum is a more useful predictor for future OER measures than home price appreciation, vacancy rates, interest rates or unemployment.” I was unaware of how equivalent rent is estimated. Per the linked item from Penn Mutual Asset Management, “OER is determined by a monthly survey of consumers who own a primary residence. The survey asks how much consumers would pay to rent instead of own their home. OER represents approximately 25% of the Consumer Price Index and 12% of personal consumption expenditures (PCE) [as of2021].”

https://www.pennmutualam.com/market-insights-news/blogs/chart-of-the-week/2021-02-25-owners-equivalent-rent-and-price-stability#:~:text=OER%20is%20determined%20by%20a,personal%20consumption%20expenditures%20(PCE).

Recent momentum has been on the side fairly large monthly increases, with the December 2022 m/m percent change of about 0.8%. A second log difference MA(1) model forecasts an increase of about 0.7% for January 2023. As expected, recessions decrease the OER rate of inflation as shown on the FRED chart.

https://fred.stlouisfed.org/graph/fredgraph.png?g=Z26v

A very important point about OER (=25% of CPI). It is not about about actual cost of rent or even actual cost of ownership. It is about answers to a subjective question about a theoretical situation. It also comes from people who have little to no information about actual rents and changes in rents.

Core PCE deflator, quarterly and semi-annual averages:

https://fred.stlouisfed.org/graph/?g=Z2zG

FRED doesn’t do 3 and 6-month averages, but I assume the point is clear; the quarterly average running below the semi-annual average means core inflation is slowing.

Here’s a similar treatment of owners equivalent rent:

https://fred.stlouisfed.org/graph/?g=Z2A8

Crud… Short-term average running above the longer average – trend still upward. A handy conformation of the point AS made.

While OER is problematic in some ways, the momentum in the series that AS told us about makes good sense. Actual home prices trend pretty strongly. Mortgages tend to induce downward flexibility in home prices. Information about changing market conditions accumulates slowly, as Ivan noted. It’s a formula for inertia.

Oh, and see Ivan’s comment below about y/y vs q/q. Same point I’ve tried to make with pictures.

Memo to Princeton Steve, Econned, and CoRev:

Just gander on these embarrassments reaped on both Bruce Hall and JohnH and realize they are far, far, ahead of the rest of you for dumbest troll of the year 2023 edition. Maybe the rest of you will have to settle for going for the bronze medal.

If you want to know where we are heading y/y is obviously less informative than q/q. That is simple math. Some people who’s agenda is not truth and insights may chose y/y to “make their point” – but who would be fooled by that.

You can sometimes get even better clues from m/m, although there is always a risk of being fooled by outliers. An informed analyst should be able to spot when something is an outlier, even though it usually takes a few months to get the “mathematical” proof that a datapoint is indeed an outlier.

Sometimes data can be so noisy with random fluctuations that you need to do averages over multiple datapoint to see a trend.

One of my favorite sites for following the Covid pandemic early on was “worldometers” https://www.worldometers.info/coronavirus/country/us/ They have a great way of showing the case numbers. The daily numbers are bar graphed and then you can select to show line graphs for 3 day and 7 day averages. Those are absolutely perfect for demonstrating the advantages of curve fitting and how it deals the peak signals. I hope this approach will become much more common. Give people a visual of datapoint for the shortest time interval that it is collected, with options to add a curve for self selected averages.

AS: “What concerns me about Core CPI as mentioned on a prior post is that over the past few months, the Core Commodities index has declined in percent about the same as the Core Services has increased in percent.”

Keep in mind that 40% of Core CPI is shelter and we know that shelter has a big lag. Spot prices are already in decline but won’t show up in CPI for several months.

And Core Services, well, that is even a higher percentage shelter (60% maybe?). Shelter is dominating Core CPI and especially Core Services. I see no justification for a 0.25% increase let alone 0.50%.

Ivan: “A very important point about OER (=25% of CPI). It is not about about actual cost of rent or even actual cost of ownership. It is about answers to a subjective question about a theoretical situation. It also comes from people who have little to no information about actual rents and changes in rents.”

Sorry, but this is a myth and a very common misunderstanding. Owner’s Equivalent Rent is computed each month by sampling actual rents paid for single family homes. There are some 16 million rented single family homes so plenty to sample from. It is not a subjective question. It is actual rental payments, the same way they sample apartment rents.

Where the confusion comes from is in the construction of the CPI market basket. The market basket and its weighting for each item is reconstructed every two years based on the Consumer Expenditure Surveys of over 24,000 consumers. In that survey they do ask home owners questions about equivalent rent, but that only affects the weighting in the CPI index. Those questions do not affect actual sampling of home rental costs tabulated each month for the CPI or the changes in rents each month in the CPI. These are real numbers, not subjective.