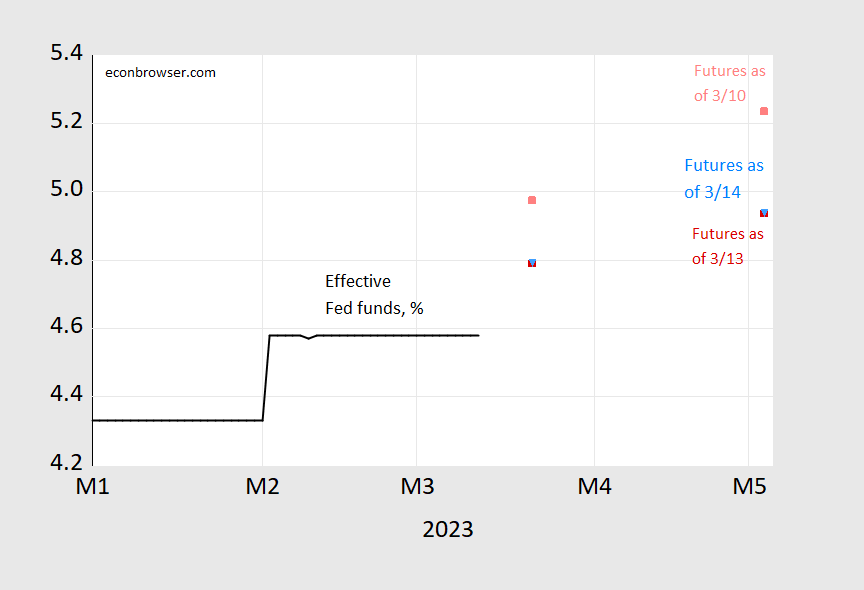

M/M core CPI inflation surprised on the upside (0.5 ppts vs. 0.4 ppts Bloomberg consensus) while m/m headline at consensus. The path of the Fed funds as indicated by futures barely budged.

Figure 1: Effective Fed funds (black), CME futures implied as of 3/13 12:20CT (red square), as of 3/10 (pink square), as of 3/14 (inverted sky blue triangle) 1:20CT. Source: CME Fedwatch, accessed 3/13, 3/14.

It’s pretty hard to see the increase, but it’s there; for the May 3rd meeting, the implied rate rose from 4.936% to 4.940%.

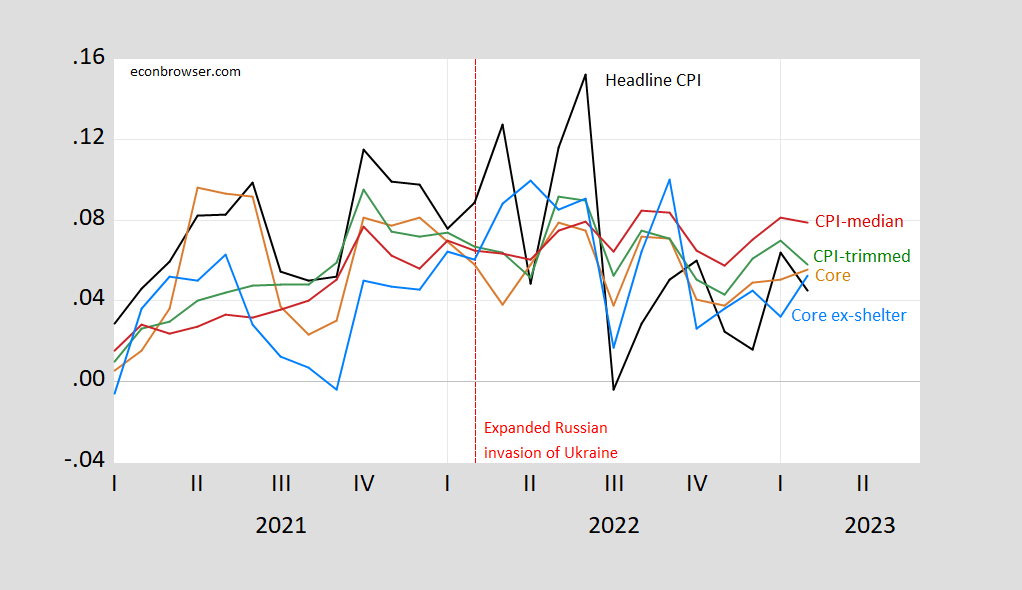

Here’s the picture of inflation measures month-on-month, annualized: headline, core, core ex-shelter, trimmed mean, and median.

Figure 2: Month-on-month annualized inflation of headline CPI (black), core (tan), core ex-shelter (sky blue), 16% trimmed CPI inflation (green), median CPI (red), all in decimal form (i.e., 0.05 means 5%). Source: BLS, BEA, Cleveland Fed via FRED, Paweł Skrzypczyński, and author’s calculations.

Shelter driven mirage. Core CPI ex shelter deflated significantly.

Kevin Drum has a post nothing what you said.

I saw a claim that the Fed Chair is actually paying attention to “CPI ex shelter”. If that is the case then he may understand that inflation is under control and they should not raise rates at all at the next meeting.

Measuring Price Change in the CPI: Rent and Rental Equivalence

Is the shelter CPI contribution a “mirage” or is it “real”? Could the rent equivalent also be seen as an approximation to depreciation?

Questions for those more enlightened than I.

As the BLS says, “The shelter service that a housing unit provides to its occupants is the relevant consumption item for the CPI. Most of the cost of shelter for renter-occupied housing is rent. For an owner-occupied unit, most of the cost of shelter is the implicit rent that owner occupants would have to pay if they were renting their homes, without furnishings or utilities.”

“Owned housing units themselves are not priced in the CPI Housing Survey.

“Spending to purchase and improve houses and other housing units is treated as investment and not consumption in the CPI. Interest costs (such as mortgage interest), property taxes, real estate fees, most maintenance, and all improvement costs are part of the cost of the capital good and are also not treated as consumption items. These non-consumption costs of owned housing are out of scope for the CPI under the cost-of-living framework that guides the index.”

“The data used as inputs in the construction of the index for shelter, as well as the indexes for rent and OER, are collected in two surveys. The Consumer Expenditure (CE) Survey asks households the share of their budget which goes towards different categories of goods and services and is subsequently used by the CPI program to create weights for index estimation. The Housing Survey collects price observations of rental housing units across the United States.”

https://www.bls.gov/cpi/factsheets/owners-equivalent-rent-and-rent.htm

A lot of the concern around the SVB mess had to do with First Republican Bank:

https://www.foxbusiness.com/markets/first-republic-shares-rebound-fears-broader-financial-crisis-ease

First Republic Bank shares rebounded sharply on Tuesday after suffering a record drop following the collapse of Silicon Valley Bank. The San Francisco-based First Republic saw its shares climb 57% as of Tuesday afternoon, the largest percent increase since 2010. It was among the best-performing stocks in the S&P 500. Shares of other regional banks also jumped: PacWest Bancorp increased 70%, Customers Bancorp was up 12% and Zions Bancorporation climbed 10%.

This bank’s equity was more than 10% of the value of its assets before the mini-crisis but the value of its assets quickly fell by 7%. So its equity to value ratio for a while was only 3%. Yea they survived the crisis and now has an equity to asset ratio closer to 7%.

The market works …. as long as the bank does not endure another major hit. I just hope its management does not go wild and ignore the lessons of prudent management. Of course a renewed Dodd-Franks might help here

Ole Bar bark can’t even get the fundamentals correct: “Of course a renewed Dodd-Franks might help here” Adding more regulation/regulators doesn’t help INFLATION nor THE FED’S INTEREST INCREASES. He even quoted/cited one of their effects: “…the value of its assets quickly fell by 7%. So its equity to value ratio for a while was only 3%. Yea they survived the crisis and now has an equity to asset ratio closer to 7%.”

Please quit showing your stupidly ignorant bias and denial of the fundamental causes of the current potentially catastrophic banking crisis (his term). Even your mother must cringe at your commenting.

CoRev: If you increase regulation, so as to reduce the amount of contingent liabilities that the government has to take on during crises, then the federal debt would be smaller than otherwise, and the need to monetize that debt would be reduced. Hence, inflationary pressures would be reduced relative to the counterfactual. Read a book (if you can). Say “Lost Decades”.

I love that book actually, LOVE Its “anti Reaganism slant”. Love that book SO MUCH, did you want me to search through this house for that book WHILE I’m drunk??? YOU are cold man, you’re so cold to motivate me to look for that book WHILE I’m drunk dude. : )

I guess he had to write INFLATION as the buttons on his keyboard could no long bang out WEATHER, WEATHER, WEATHER.

Menzie – if, if , if … contingent liabilities.? How does that work in real life when there is a ~40% run on a bank’s assets? How does “Hence, inflationary pressures would be reduced relative to the counterfactual. ” work in such an instance? How does the lie: ZERO taxpayers $s will be used?

The pervasiveness of this current problem is evident even in the FDIC insurance fund:

“The DIF’s comprehensive income totaled $5.2 billion for 2021 compared to comprehensive income of $7.5 billion during 2020. The year-over-year decrease in comprehensive income of $2.3 billion was primarily driven by a decrease in interest and market value adjustments on U.S.Treasury securities of $2.4 billion.” https://www.fdic.gov/about/financial-reports/corporate/cfo-report-4thqtr-21/balance.html

Even the FDIC has ~80% of its assets losing money.

Keep ignoring the basic causes for this issueBiden’s inflation and Biden’s FED attempt to lower inflation, and keep hoping with time it will get better.

Yep! It’s all transitory. You folks crack me up.

Thanks once again for proving you have no clue what the SVB matter was about. Then again money and banking was never your forte. No more than ag econ or climate science.

Restoring the original Dodd-Franks would be a good start. We definitely also need to redefine the “to big to fail” concept and rules. Any bank with over $100 billion should go through a tough annual stress test that evaluate all possible stress scenarios. The final reports should not be a “all clear call” – but a “this is what it would take for this bank to get in trouble” (e.g., house prices cut in half, treasury rates raised to x % in the next 2 years, Z % of deposits withdrawn a year, etc.). Maybe a spreadsheet showing what happens to the banks profits and solvency in case of a mild, medium and high adverse event in each category. The fact that we had to do all this emergency intervention would suggest that it doesn’t take a trillion dollar bank failure to destabilize the whole system.

As a matter of fact I think the shareholders should demand such a test of any bank they invest in. Maybe the hit that shareholders took this time will make them wake up and demand that they actually know what they are investing in, and its risk.

Again, I have to say – if you are a bank, where would you park assets? Treasuries? No. Commercial real estate? Hell no. Mortgages? No. Equities? No. Cash? No- not while there is high inflation. We are in a world now where probably every bank has underwater assets; it’s just a question of what percent of their total is underwater. So at this point confidence is absolutely everything. The Fed cannot take actions which everybody now knows are undercutting bank assets… at some point they will break more banks than they can afford to bail out. (I see Credit Suisse is the bank de jour)

I’m gonna say this the kindest way I can.

You’re dumb

It’s NOT a systemic problem. Thanks for playing the board game.

Oh, grow up.

If you have a point to make, explain it.

W says: “We are in a world now where probably every bank has underwater assets; it’s just a question of what percent of their total is underwater.” and so is their FDIC insurance fund.

Still some of the stupidest here don’t think the problem is systemic.