Analysis of current economic conditions and policy

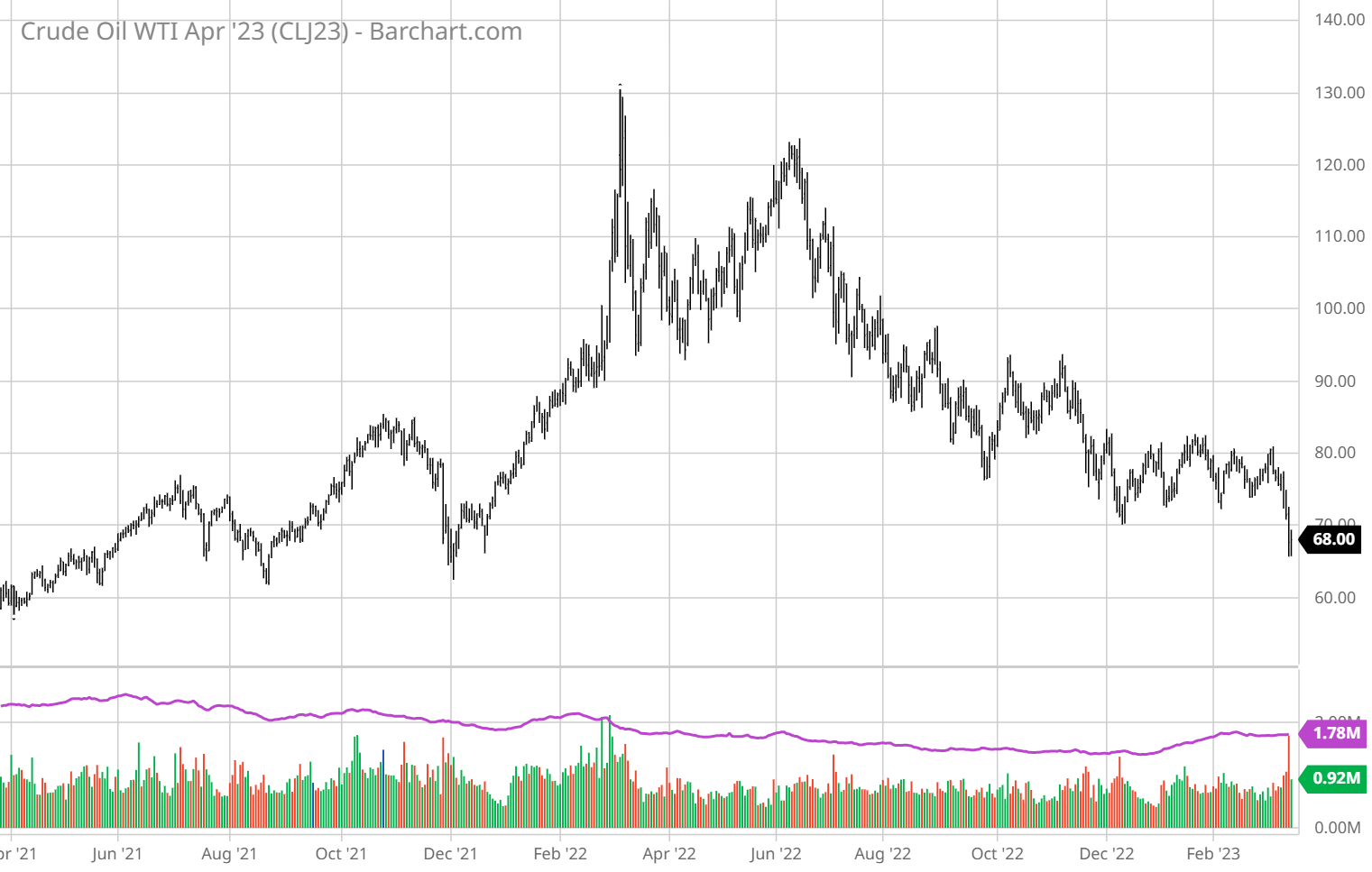

Oil Futures

Near month, over past two years:

Source: barchart.com, accessed 3/16/2023.

33 thoughts on “Oil Futures”

Bruce Hall

US is producing about 800,000 bpd less than the peak of 2019 and Russia announced it was cutting 500,000 bpd from its production. However, it’s expected that China will increase its demand this year and be about 1/2 of the global increase in demand for 2023. So, if production increase in the US is being offset by Russian decreases and China is expected to increase its demand by 700,000 bpd, it looks as if there’s some chance that oil prices increase as we go through 2023.

But EIA is also optimistic that US oil production daily rates will surpass 2019 and be enough to roughly balance supply with demand keep oil prices more stable and low. https://www.eia.gov/outlooks/steo/report/us_oil.php

Seems like a lot of maybes.

Pgl

Maybe you finally understand what market prices signal. Maybe you will finally read that graph.

Macroduck

Testing

Anonymous

From the recent data, the supply side of China’s economics is recovering very quickly, while the demand ( consume ) is below the expectation. The market looks forwards to more policies to stimulate the consumption, but little effect yet. It is more likely that the recovery of China’s economics this year is weak and fragile. The oil demand is possible lower than the expected.

Anonymous

I think the recent drop is probably demand (or demand worries) driven. But I love this memetic take on encouraging supply, to make up for Russia:

p.s. There is also an argument that Russia is still producing a fair amount, but just sending it to different markets. Kind of a deadweight loss in terms of higher transport costs. But still, not the drastic loss of supply.

Ivan

The recent dip under $70 is almost certainly connected to the fear that the banks could pull us into a recession. Biden also gave us a surprise with his willingness to permit drilling in Alaska. That indicates the potential for more oil from US even as fracking appears dead in the water at prices of $70-80. This dip is way to sudden to reflect any underlying changes in supply/demand, and the economic trends for China and the west have been known for a while and already baked into prices.

Russia is likely selling all they can, and with India and China willing buyers (at a discount) Russias official announcement of a small 500K bpd cut, may not even have been implemented. Putin asked his oil companies to set up and fund private military – so there must be money there.

The Saudi king has demonstrated that he will defend prices with cuts in production. Last time prices began moving down he cut supply by 2 million bpd, clearly showing that he can set those prices as he wants. Any increases in US production will have minimal and temporary effects on the world balance of supply/demand. It seems to me that almost everybody is happy with oil at $70-80 so I would be surprised if it doesn’t get back there rather quickly.

GREGORY BOTT

No, it’s the China, KSA deal. There is no real problem in the main banking system outside crypto heavy banks right now. Fake runs are fake.

The term structure of oil futures is unchanged, that is, oil prices have fallen across the curve. This implies a demand-side (wrt to securities), risk-off move. Either the bank thing gets better, or it doesn’t. But people are beginning to pull exposures and husband cash.

Steven Kopits

Meanwhile, pressures persist despite a couple of bank bailouts.

This is as expected. We have here not a balance sheet crisis, but an income statement crisis. You can’t solve it with more capital. Revenues and expenses have to be realigned. The 3 mo treasury is at 4.55% today. That has to come down 2% (pp), in my opinion, to stabilize the banking sector.

Fed and Treasury are still dead at the switch.

Pgl

An income statement crisis? Why do you just make up gibberish? Maybe you think SVBwas insolvent. If so use the right terminology. Oh wait you do not get basic monetary economics. Never mind

Pgl: If he can’t understand a balance sheet, how do you expect him to understand anything?

Ivan

One of my credit unions is giving 3% on large deposits in checking accounts. With 3 month treasuries at 4.5% they have a 150bp spread and are making money with a very minimal risk. Any bank can do that.

By allowing banks to get loans at par on “locked up” long treasuries, the Fed has solved the solvency issue, but not the profit issue, for the more careless banks (currently trapped). Those banks will have to restructure their assets and business models, before they are told to sink or swim a year from now. The Fed will not allow an over-the-cliff event, but they may allow a slow culling of the herd.

Steven Kopits

But Ivan, why are you getting 3% when you could buy treasuries at near 5%? Any professional treasurer would have already moved their money. And that’s the point. That’s how you get a structural run on deposits.

Macroduck

You missed the lecture about liquidity preference?

Macroduck

On the point of missing the lecture about liquidity preference…

Discussion of finance is often separate from discussion of productive business, so that one minute, we discuss liquidity as if it’s a purely financial issue, the next we discuss the impact of bank runs on businesses, and don’t make the connection. The connection is in the lecture on liquidity preference.

Our highly financialized economy has apparently led some to an over-financialized way of thinking about money; the first purpose of money is maturity transformation in pursuit of profit. Paying the bills is an afterthought. That’s exactly NOT what business management with deposits at SVB were thinking last weekend.

And by the way, those managers had NOT done what Kopits assured Ivan they had done. They maintained deposits large enough to pay their bills, and those deposits were at risk.

Moses Herzog

I think it’s great and I applaud if Menzie wants to use Kopits’ nonfactual statements, intentional errors, and right-wing propaganda to guide his students on their learning adventures and teach his public readership some of the worst minefields of economics. But I hope neither him or his more intelligent readers think any corrections will adjust Kopits’ love of being wrong whenever being wrong suits his self-marketing goals.

Baffling

Depends upon how likely you are to need the money today. One month treasuries are not the same as checks. You get access every 28 days. You pay for flexibility. Most businesses will take 3% and flexibility rather than the restrictions on the 4.5%. There is a cost to selling before maturity.

Ivan

No – a run doesn’t develop from a slowly increasing spread. The professional treasurers will each have a different point of spread and preferences; that is determined by their specific needs for liquidity, profits and risk tolerance. Each have their own answer to how many bp difference it takes to compensate for the lost liquidity. So as a group they slowly move from one to another asset type.

A run comes from a chock that suddenly make a large proportion of the “professional treasurers” switch their preferences in the same direction.

Pgl

BTW Stevie. Loan margins can be positive if loan rates rise with deposit rates. If you bothered to take a simple money and banking course you realize how utterly stupid your comments are

Macroduck

Off topic – I find it interesting that the “safe” asset class is showing much increased volatility right now, as represented in the MOVE index, while stock market volatility, as represented by the Vix, is behaving as it often does.

Banking is at the center of the current mess, so interbank lending should be tight, yes? Well, yes and no. FRA-OIS spreads, a measure of dollar liquidity, is showing clear signs of stress:

And by the way, that FRA-OIS spread is pretty closely related to monetary liquidity. The Fed is getting tighter monetary conditions without hiking rates. Seriously, Fed guys, don’t do it. Wait to see whether financial conditions ease and WHETHER INFLATION IS COMING DOWN!!!. Lags, children. Lags.

GREGORY BOTT

Dollar liquidity is down structurally. It’s not new. It’s been that way since late 2021. That is not tightening, it’s just a more historical in context. Dollar is leaving the global financial system as a currency.

Macroduck

Everything that happens happens inside your fantasy financial gizmo? The spike in the FRA-OIS spread indicates nothing that matters to the economy? Fed liquidity measures have no effect on the economy?

And, by the way, how could the dollar leaving the global economy as anything other than a currency? The dollar is a currency, not a lollipop or a pickup truck.

Read a book. Take a class. Do something to pull your head out of this all-knowing fantasy you built for yourself.

GREGORY BOTT

A lot of talk of the Saudi’s being pissed at Russia. Bet the China backed deal with KSA/Iran was about removing Putin. The Ukrainian care packages from KSA and Iran reducing military support. My guess is KSA starts pumping more oil into China replacing Russia. Will create a global oil glut 2 until Putin is overthrown.

The U.S. is pretty much divorcing itself from the middle east. We are Nat gas supported by wind/solar/EV. The dollar standard has ended. The wind down has been clean so far. Back to 1984 we go. Oceania(America’s), Eurasia/Northern Africa, East Asia(minor). China replaces the Soviets. Will baltoslavic Russia join their brothers in the EU(west asia)???

Anonymous: I’m guessing you mean SPR, but who knows. Maybe you’re right and NPR does have a stash of crude…

Moses Herzog

Anonymous has unknowingly brought up an interesting topic. Biden had said something similar to this during the release of a large part of the SPR oil reserve release (“opening up”, whatever your preferred nomenclature) that they would later buy back or “build back up” the reserves after the price went below a certain price point, I want to say it was $70, it may have been $65.

Do we know how far the U.S. government is on making those purchases to the oil SPR, and is this about the correct time to be doing them??

US is producing about 800,000 bpd less than the peak of 2019 and Russia announced it was cutting 500,000 bpd from its production. However, it’s expected that China will increase its demand this year and be about 1/2 of the global increase in demand for 2023. So, if production increase in the US is being offset by Russian decreases and China is expected to increase its demand by 700,000 bpd, it looks as if there’s some chance that oil prices increase as we go through 2023.

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=pet&s=mcrfpus2&f=m

https://www.eia.gov/outlooks/steo/report/global_oil.php

But EIA is also optimistic that US oil production daily rates will surpass 2019 and be enough to roughly balance supply with demand keep oil prices more stable and low.

https://www.eia.gov/outlooks/steo/report/us_oil.php

Seems like a lot of maybes.

Maybe you finally understand what market prices signal. Maybe you will finally read that graph.

Testing

From the recent data, the supply side of China’s economics is recovering very quickly, while the demand ( consume ) is below the expectation. The market looks forwards to more policies to stimulate the consumption, but little effect yet. It is more likely that the recovery of China’s economics this year is weak and fragile. The oil demand is possible lower than the expected.

I think the recent drop is probably demand (or demand worries) driven. But I love this memetic take on encouraging supply, to make up for Russia:

https://twitter.com/MOAR_Drilling/status/1501762759209504769?cxt=HHwWgsC–brRqtcpAAAA

p.s. There is also an argument that Russia is still producing a fair amount, but just sending it to different markets. Kind of a deadweight loss in terms of higher transport costs. But still, not the drastic loss of supply.

The recent dip under $70 is almost certainly connected to the fear that the banks could pull us into a recession. Biden also gave us a surprise with his willingness to permit drilling in Alaska. That indicates the potential for more oil from US even as fracking appears dead in the water at prices of $70-80. This dip is way to sudden to reflect any underlying changes in supply/demand, and the economic trends for China and the west have been known for a while and already baked into prices.

Russia is likely selling all they can, and with India and China willing buyers (at a discount) Russias official announcement of a small 500K bpd cut, may not even have been implemented. Putin asked his oil companies to set up and fund private military – so there must be money there.

The Saudi king has demonstrated that he will defend prices with cuts in production. Last time prices began moving down he cut supply by 2 million bpd, clearly showing that he can set those prices as he wants. Any increases in US production will have minimal and temporary effects on the world balance of supply/demand. It seems to me that almost everybody is happy with oil at $70-80 so I would be surprised if it doesn’t get back there rather quickly.

No, it’s the China, KSA deal. There is no real problem in the main banking system outside crypto heavy banks right now. Fake runs are fake.

And speaking of Yahoo Finance…

https://finance.yahoo.com/news/did-eia-finally-realistic-u-160000056.html

The term structure of oil futures is unchanged, that is, oil prices have fallen across the curve. This implies a demand-side (wrt to securities), risk-off move. Either the bank thing gets better, or it doesn’t. But people are beginning to pull exposures and husband cash.

Meanwhile, pressures persist despite a couple of bank bailouts.

This is as expected. We have here not a balance sheet crisis, but an income statement crisis. You can’t solve it with more capital. Revenues and expenses have to be realigned. The 3 mo treasury is at 4.55% today. That has to come down 2% (pp), in my opinion, to stabilize the banking sector.

Fed and Treasury are still dead at the switch.

An income statement crisis? Why do you just make up gibberish? Maybe you think SVBwas insolvent. If so use the right terminology. Oh wait you do not get basic monetary economics. Never mind

https://www.bloomberg.com/opinion/articles/2023-03-17/first-republic-svb-credit-suisse-crisis-signals-growing-recession-odds?leadSource=uverify%20wall

This is how you addressed my critique. Ok Stevie … it is clear you have no clue what any of this is about

Pgl: If he can’t understand a balance sheet, how do you expect him to understand anything?

One of my credit unions is giving 3% on large deposits in checking accounts. With 3 month treasuries at 4.5% they have a 150bp spread and are making money with a very minimal risk. Any bank can do that.

By allowing banks to get loans at par on “locked up” long treasuries, the Fed has solved the solvency issue, but not the profit issue, for the more careless banks (currently trapped). Those banks will have to restructure their assets and business models, before they are told to sink or swim a year from now. The Fed will not allow an over-the-cliff event, but they may allow a slow culling of the herd.

But Ivan, why are you getting 3% when you could buy treasuries at near 5%? Any professional treasurer would have already moved their money. And that’s the point. That’s how you get a structural run on deposits.

You missed the lecture about liquidity preference?

On the point of missing the lecture about liquidity preference…

Discussion of finance is often separate from discussion of productive business, so that one minute, we discuss liquidity as if it’s a purely financial issue, the next we discuss the impact of bank runs on businesses, and don’t make the connection. The connection is in the lecture on liquidity preference.

Our highly financialized economy has apparently led some to an over-financialized way of thinking about money; the first purpose of money is maturity transformation in pursuit of profit. Paying the bills is an afterthought. That’s exactly NOT what business management with deposits at SVB were thinking last weekend.

And by the way, those managers had NOT done what Kopits assured Ivan they had done. They maintained deposits large enough to pay their bills, and those deposits were at risk.

I think it’s great and I applaud if Menzie wants to use Kopits’ nonfactual statements, intentional errors, and right-wing propaganda to guide his students on their learning adventures and teach his public readership some of the worst minefields of economics. But I hope neither him or his more intelligent readers think any corrections will adjust Kopits’ love of being wrong whenever being wrong suits his self-marketing goals.

Depends upon how likely you are to need the money today. One month treasuries are not the same as checks. You get access every 28 days. You pay for flexibility. Most businesses will take 3% and flexibility rather than the restrictions on the 4.5%. There is a cost to selling before maturity.

No – a run doesn’t develop from a slowly increasing spread. The professional treasurers will each have a different point of spread and preferences; that is determined by their specific needs for liquidity, profits and risk tolerance. Each have their own answer to how many bp difference it takes to compensate for the lost liquidity. So as a group they slowly move from one to another asset type.

A run comes from a chock that suddenly make a large proportion of the “professional treasurers” switch their preferences in the same direction.

BTW Stevie. Loan margins can be positive if loan rates rise with deposit rates. If you bothered to take a simple money and banking course you realize how utterly stupid your comments are

Off topic – I find it interesting that the “safe” asset class is showing much increased volatility right now, as represented in the MOVE index, while stock market volatility, as represented by the Vix, is behaving as it often does.

https://www.tradingview.com/symbols/TVC-MOVE/

https://fred.stlouisfed.org/series/VIXCLS

Banking is at the center of the current mess, so interbank lending should be tight, yes? Well, yes and no. FRA-OIS spreads, a measure of dollar liquidity, is showing clear signs of stress:

https://en.macromicro.me/charts/45928/us-fra-ois-spread

Not so much for TED and Libor spreads:

https://en.macromicro.me/collections/34/us-stock-relative/3775/ted-spread

Libor has moved with 3-month yields, so is reflecting volatility in bills more than increased risk in the interbank market.

Credit default swaps for U.S. Treasury debt are elevated, but we have a debt ceiling thingie around the corner:

http://www.worldgovernmentbonds.com/cds-historical-data/united-states/5-years/

And by the way, is this really the time to put small-minded political budget stunts ahead of prudence?

Bank CDS rates in general are up:

https://www.reuters.com/business/finance/us-bank-cds-prices-surge-contagion-concern-widens-2023-03-15/

Which makes me wonder why the TED and Libor are tame. Maybe I’m misreading them.

Those are all measures of volatility/risk across entire markets. If one looks at individual banks, the story is just nuts:

https://www.bloomberg.com/news/articles/2023-03-15/credit-suisse-one-year-default-swaps-near-1-000-basis-points

And by the way, that FRA-OIS spread is pretty closely related to monetary liquidity. The Fed is getting tighter monetary conditions without hiking rates. Seriously, Fed guys, don’t do it. Wait to see whether financial conditions ease and WHETHER INFLATION IS COMING DOWN!!!. Lags, children. Lags.

Dollar liquidity is down structurally. It’s not new. It’s been that way since late 2021. That is not tightening, it’s just a more historical in context. Dollar is leaving the global financial system as a currency.

Everything that happens happens inside your fantasy financial gizmo? The spike in the FRA-OIS spread indicates nothing that matters to the economy? Fed liquidity measures have no effect on the economy?

And, by the way, how could the dollar leaving the global economy as anything other than a currency? The dollar is a currency, not a lollipop or a pickup truck.

Read a book. Take a class. Do something to pull your head out of this all-knowing fantasy you built for yourself.

A lot of talk of the Saudi’s being pissed at Russia. Bet the China backed deal with KSA/Iran was about removing Putin. The Ukrainian care packages from KSA and Iran reducing military support. My guess is KSA starts pumping more oil into China replacing Russia. Will create a global oil glut 2 until Putin is overthrown.

The U.S. is pretty much divorcing itself from the middle east. We are Nat gas supported by wind/solar/EV. The dollar standard has ended. The wind down has been clean so far. Back to 1984 we go. Oceania(America’s), Eurasia/Northern Africa, East Asia(minor). China replaces the Soviets. Will baltoslavic Russia join their brothers in the EU(west asia)???

Oh for heaven sake…

https://www.bis.org/publ/qtrpdf/r_qt2212x.htm

https://econbrowser.com/archives/2022/06/the-demise-of-dollar-dominance

https://econbrowser.com/archives/2022/06/first-annual-frb-nyfed-conference-on-the-international-roles-of-the-u-s-dollar

Read something. For once.

jim cramer advised ‘buy dip when oil hits $65. dec 13 2022

maybe one time not 2b opposite cramer

several weeks of comm’l crude built and no release from npr…..

Anonymous: I’m guessing you mean SPR, but who knows. Maybe you’re right and NPR does have a stash of crude…

Anonymous has unknowingly brought up an interesting topic. Biden had said something similar to this during the release of a large part of the SPR oil reserve release (“opening up”, whatever your preferred nomenclature) that they would later buy back or “build back up” the reserves after the price went below a certain price point, I want to say it was $70, it may have been $65.

Do we know how far the U.S. government is on making those purchases to the oil SPR, and is this about the correct time to be doing them??

moses:

https://www.cnbc.com/2022/12/16/us-begins-buying-back-oil-for-strategic-petroleum-reserve.html

may answer your question,

yes spr!

Rule #1: Return of Principal over return on principal

Rule #2 See Rule #1