Most quick assessments of the impact of a continued US-Israel/Iran war work of reduced form responses to oil shocks. I’m not sure how equity market responses, quantitatively, fit in. However, I suspect that higher uncertainty and perceived risk may prove the catalyst for a sustained correction.

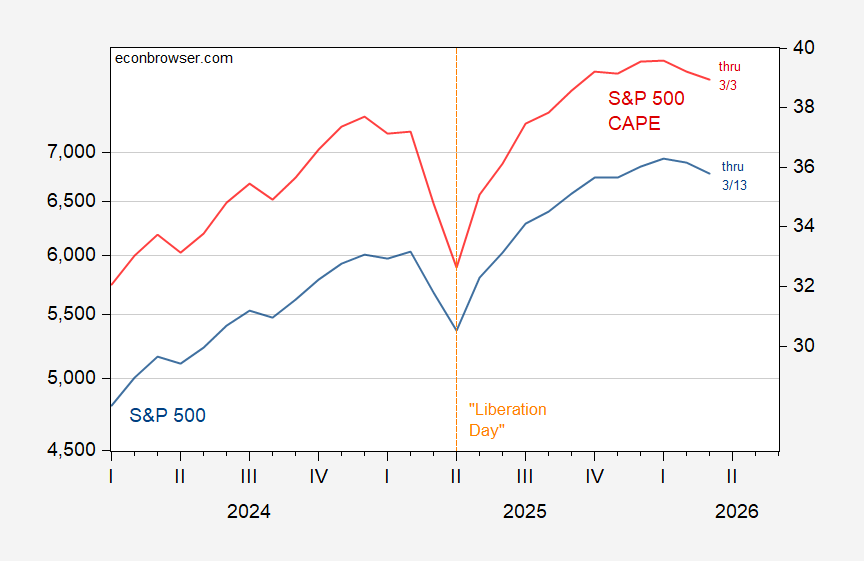

Here’s the latest available information on aggregate SP500 data:

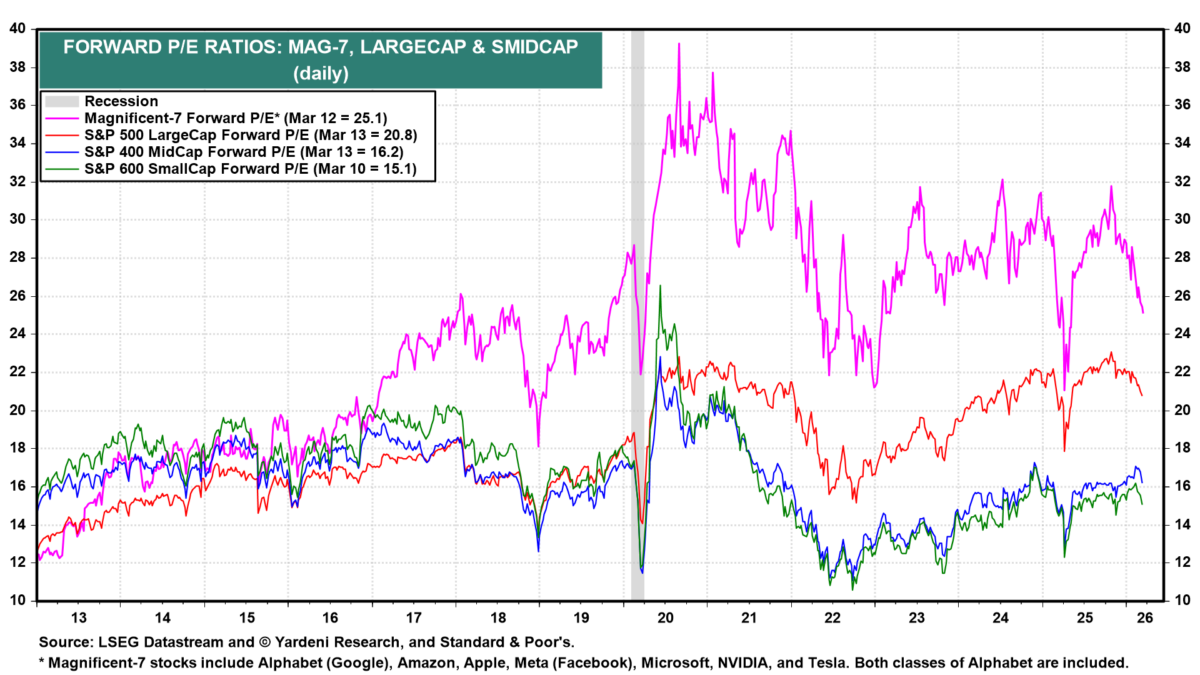

However, aggregates hide a sharp division in price-forward earnings ratios:

Source: Yardeni, accessed 3/15/2026.

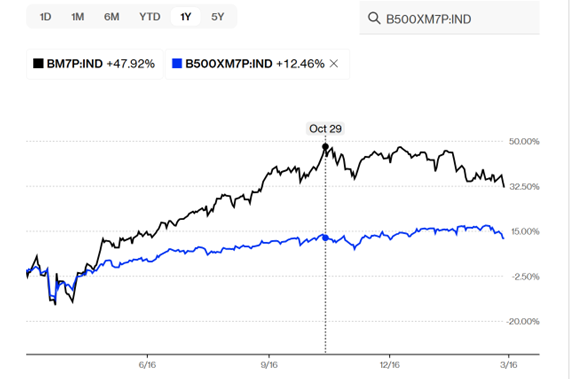

The SP500 price returns divergence is more clearly shown by comparing the two Bloomberg price returns index. The bulk of gains in SP500 over the past year has been associated with the Magnificent 7 — and yet currently the Magnificent 7 price index is down about 16% relative to last peak (log terms).

Black line is Bloomberg Magnificent 7 net return index, blue line is ex-Magnificent 7 net return index. Source: Bloomberg, accessed 3/15/2026.

Jeff Currie, commodity analyst at Goldman Sachs, told BBG TV that the flow rate out of strategic oil reserves world wide is 2 million barrels per day, against a shortage of 18 million bpd through the Strait of Hormuz. His point is that the pledge to release 400 million bbls from reserves is not a big deal relative to the size of the problem.

He went on to say that there is no policy response adequate to address the problem, and that (until the Strait is reopened) the likely direction for oil prices is upward.