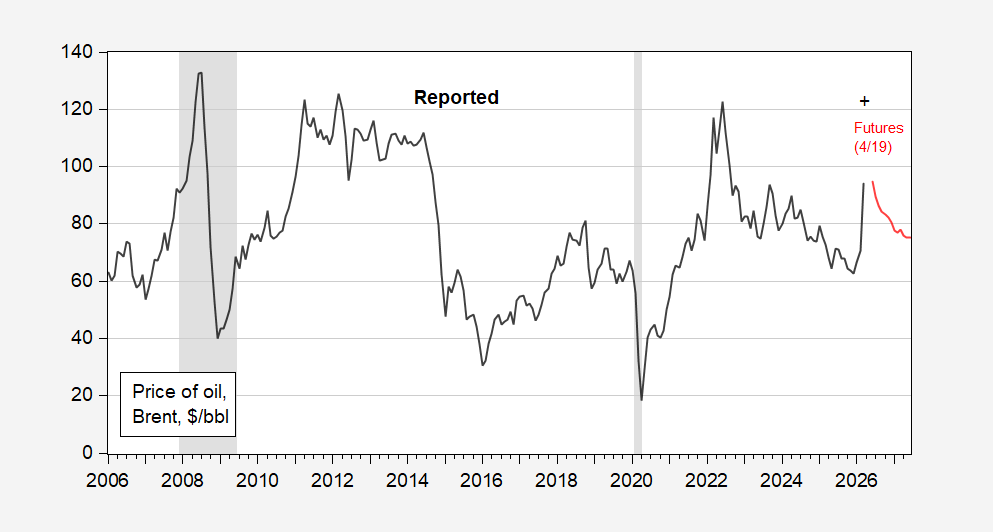

Front month Brent futures (for June) jumped tonight. Where are gasoline prices going, conditional on those futures being predictive.

Figure 1: Brent oil price (black), NYMEX futures as of 4/19 (red), all in $/bbl. April observation for data through 4/10. NBER defined peak-to-trough recession dates shaded gray. Source: EIA via FRED, NBER, barchart.com.

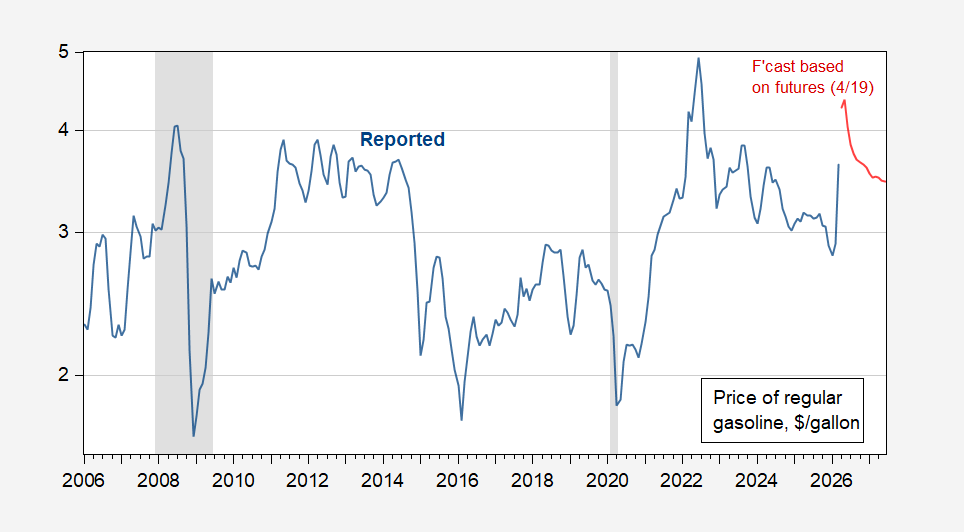

Using a regression in log first differences of gasoline price on current and lagged oil price of 1990M10-2026M03 (adj-R2 = 0.56), this is the conditional forecast of gasoline prices:

Figure 2: Price of regular gasoline (blue), and forecast based on Brent futures (red), both $/gallon. NBER defined peak-to-trough recession dates shaded gray, barchart.com, NBER, and author’s calculations.

Oil futures are pretty much the most accurate predictors on average, as discussed in Chinn and Coibion (2014). However, these assessments usually focus mostly on peacetime sample periods. Futures were not particularly accurate during the 1990-91 Iraq war, nor the 2003 war, as noted in this post.

In the context of the current conflict, Norland (2026) observes:

…If the conflict ends soon and supply disruptions resolve quickly, crude prices could fall across the curve leading to losses for anyone who is long. That said, the fact that the returns of holding long positions during periods of contango have tended to be negative, while the returns on holding long positions during periods of backwardation tend to be positive tells us two two things:

Traders tend to underestimate how long periods of oversupply last. Hence markets in contango tend to remain at depressed prices for longer than investors initially imagine.

Likewise, traders had historically tended to underestimate how long periods of undersupply last. This can be true for demand shocks, such as the rapid increase in demand from Chinese and other emerging markets between 2003 and 2011, and can also be true during periods of supply disruption, such as following the U.S. invasion of Iraq.

and:

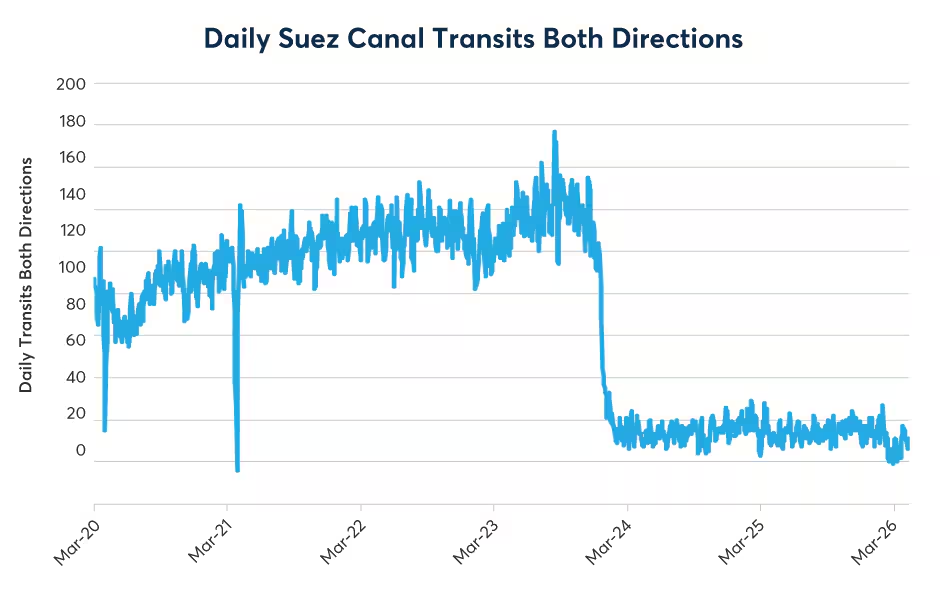

One key indicator to watch is shipping traffic through the Strait of Hormuz (Figure 7). Also, what happened to shipping traffic through the Red Sea and the Suez Canal offers a warning about how supply disruptions can carry on for longer than initially expected. After Suez traffic dropped off in late 2023, it never recovered in part because insurance companies withdrew from the market (Figure 8).

…

In other words, even with a nominal “re-opening” of the Strait, actual realized oil prices may very well exceed futures-implied prices.

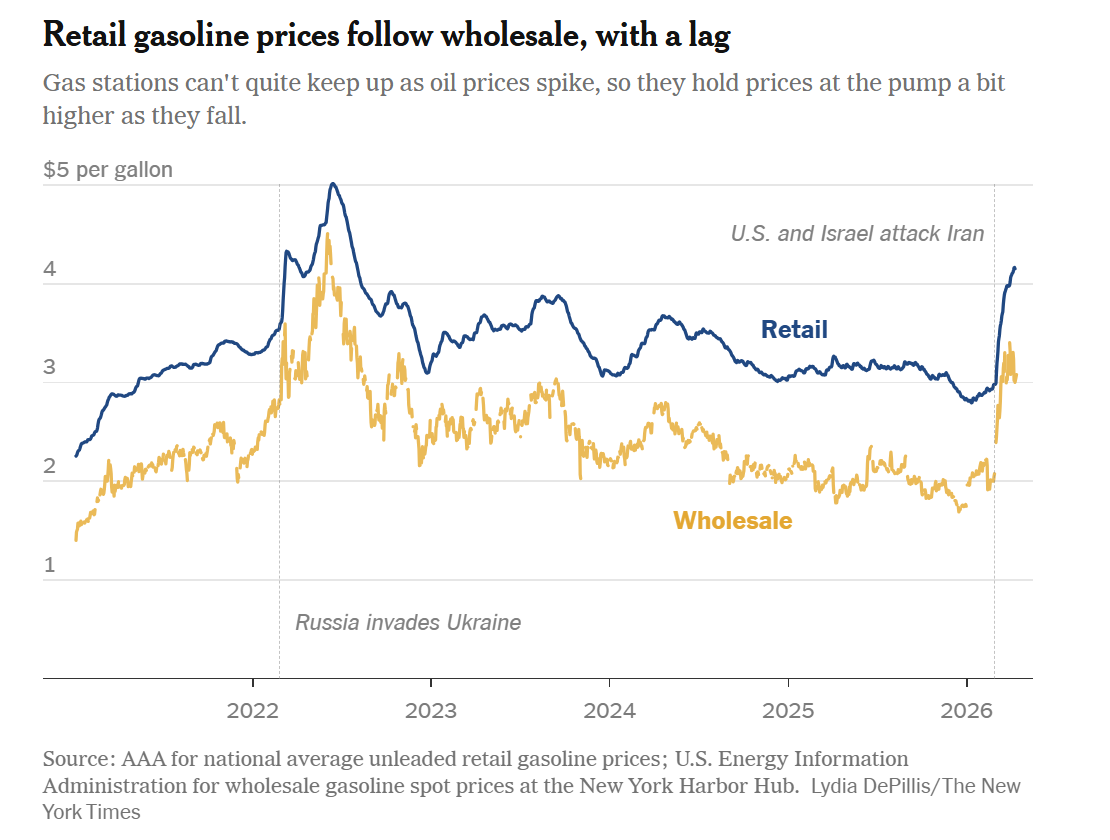

A final reason for expecting elevated gasoline prices in the future, even if spot oil prices decline: the asymmetric response of gasoline prices to oil prices. Gasoline prices rise quickly with an oil price increase, and decline more slowly in response to an oil price decrease. This asymmetric response is termed the “rocket and feather” thesis. For an examination, see Wen et al. (2025). I ignored this effect in my regression specification above.

* Unless there’s a global recession, which induces a big decline in demand…

Addendum:

DePillis/NYT, as if on cue, notes today the asymmetric price response of gasoline prices. Graphic:

Dr. Chinn, you may have to rethink your pessimism about gas prices.

I have it on good authority (Kevin Hassett, AKA Baghdad Bob) that “Gulf energy production has been depressed over time because of the huge risk premium associated with Iranian behavior. Once this is done, think about the explosion in new energy production that could happen in the Middle East.”

So there, take that.

(Rather careless of Hassett to use the words “explosion” and “energy production” in the same sentence under the circumstances.)

Remarkable.

An obvious lesson from this war is that low-cost rocketry can shut down Hormuz AND impose serious damage on oil infrastructure throughout the Gulf. Hassett seens to assume either that Iran, and everyone who shares Iran’s interests, will be neutralized by this war, or that Iran’s neighbors will simply forget this lesson. The guy is true a student of the “rosy scenario” school of economics.

Further to the point about the lessons of the war, Iran, along with Ukraine, has already changed the face of warfare by producing cheap, highly capable drones. Aerial and naval drones have pushed Russia’s navy out of much of the Black Sea. The land war in Ukraine is now drone war, with echoes of WWI trench warfare. The U.S. did not dare put naval vessels in the Persian Gulf until a ceasefire was in place, because of Iran’s drones.

And here’s a kick in the pants – China may have developed a cheap hypersonic missile:

https://techstartups.com/2026/03/24/private-chinese-startup-mass-produces-mach-7-hypersonic-missiles-for-99000/

You, too, can afford a hypersonic missile! At just $99,000, how can you afford not to have one? For a million dollars, you can own a whole set.

Of course, the new Chinese geegaw only does mach 7, whereas the U.S. prototype is rumored to top out at mach 17. I’m no expert, but I suspect top speed is beside the point until defensive systems are in place that can readily intercept swarms of slow poke hypersonic missiles.

The Tech Startups article focuses on the implications of China’s missile for the Iran war. That’s just small-minded “hot topic” journalism, since Iran is already doing scary things to Israel and keeping the U.S. at bay with cheapo $15,000 drones. At $99,000 a pop, and concealable anyplace where shipping containers are common, these missiles could make China’s own newly-purchased navy obsolete, not to mention the war-ctiminsl-in-chief’s dream of a supership named after himself. It could mean the Iran/Iraq “War of the Cities” could be replayed over and over, around the world.

Cheap, capable range weapons seem to humble little me to be a Kalashnikov sort of development. Every tin pot warlord and dictator can now afford to threaten massive harm, and do it from a distance.

Assuming, of course, the $99,000 hypersonic missile actually exists. China, after all.

Would China sell, or perhaps give, hypersonic missiles to Iran? Depends on whether they want to joint the U.S., Russia, Iran, France and the UK in the weapons business, ’cause it could be very effective advertising.

Cheap-but-effective drones and hypersonic missiles seem to call much of U.S. military doctrine into question. The war-criminal-in-chief’s massive, budget busting military spending request may be mostly a waste of money. And a gift to defense industry fat cats – mustn’t forget that part.

… and, if they become popular enough, they will be covered by the 2nd Amendment, at least according to the current DOJ! Effective home defense for every upper-middle-class and wealthy family in America! Let’s see those Iranians invade now!

Last one – the oil services industry sees the Iran war as bad for business:

https://www.bloomberg.com/news/articles/2026-04-20/oil-contractors-facing-profit-hits-from-mideast-war-fallout

Unless I’m missing something, that’s the opposite of what Hassett said.