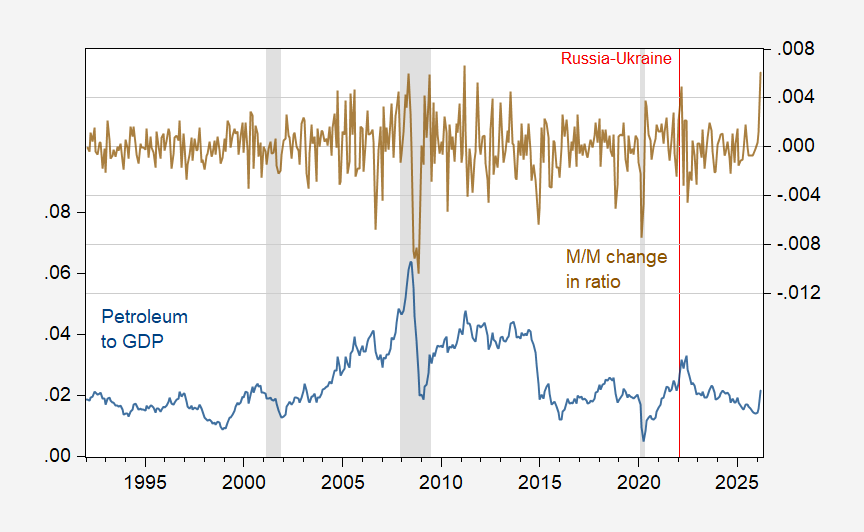

It’s true that the real price of oil is lower than in past episodes of oil price jumps. Moreover oil consumption constitutes a smaller share of US GDP than in previous episodes of oil price jumps. However, if one wants to discuss “shocks”, in part one would want the surprise or non-predictable component of oil price use. Approximately (I think for oil), that’s the change in the oil share, as shown below.

Figure 1: Oil consumption to GDP ratio (blue, left scale), and change in ratio (brown, right scale). Consumption ratio calculated by multiplying consumption in bbl by WTI price/bbl, divided by nominal GDP. NBER defined peak-to-trough recessio dates shaded gray. Source: EIA, S&P Global, NBER, and author’s calculations.

The “shock” so defined is larger than the 2022 shock associated with the expansion of the Russian invasion of Ukraine, and larger than the shock that took place early in the 2007-09 recession.

Note that the average WTI price in April was yet higher — at $100.32, and at $101.56 as of Monday.

What is true is that with a slight net export surplus in petroleum and petroleum products, we don’t suffer a terms of trade shock (as Europe and East Asia do). But that is a separate issue from a cost push shock.