Both strongly beat consensus. From the Fed’s G.17 Release today:

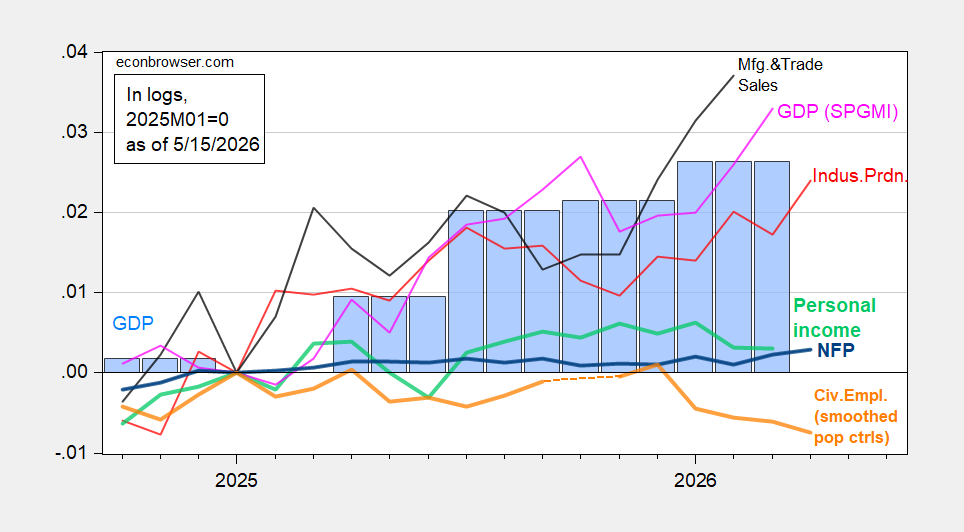

Figure 1: NFP employment (bold blue), civilian employment with smoothed population controls (bold orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold light green), manufacturing and trade sales in Ch.2017$ (black), and monthly GDP in Ch.2017$ (pink), GDP (blue bars), all log normalized to 2025M01=0. Source: BLS via FRED, BLS, Federal Reserve, BEA 2026Q1 Advance release, S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (5/13/2026 release), and author’s calculations.

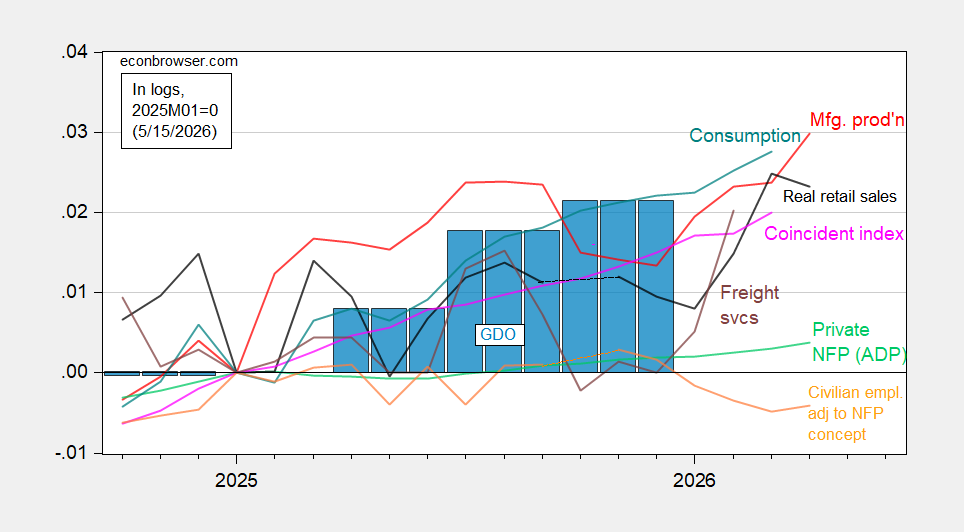

Figure 2: Civilian employment adjusted to NFP concept smoothed population controls (bold orange), manufacturing production (red), ADP private nonfarm payroll employment (light green), real retail sales, CPI deflated (black), freight services indexes (brown), and coincident index in Ch.2017$ (pink), GDO (blue bars), all log normalized to 2025M01=0. Source: BLS, ADP,via FRED, Philadelphia Fed [1], Philadelphia Fed [2], Bureau of Transportation Statistics, Federal Reserve via FRED, BEA 2026Q4 3rd release, and author’s calculations.

Off topic – change of plans?:

‘After countless comments about the importance of addressing Iran’s nuclear program, when asked about the country’s enriched uranium, he told Reuters, “That’s so far underground, I don’t care about that.” He went on to say Iran was “incapable” of developing a nuclear weapon in light of the damage it has suffered…’

https://www.ms.now/rachel-maddow-show/maddowblog/i-dont-care-about-that-trump-moves-the-goal-posts-on-irans-uranium-stockpile

Off topic – Treasuries getting skittish.

The three components of market interest rates – expected cost of funds, expected inflation and term premium – are all at new highs for the Iran-war period. I won’t bore you with the details, but futures are now pricing in no chance of a Fed ease this year, some chance of a hike. A month ago, futures still priced in some chance of a cut. CPI and PPI data clearly had an effect.

Also, I think, the pricing of oil futures is having a big impact. This week, futures into mid-2029 rose above their 2022 prices. By October 2029, this week’s high just about matches the 2022 high. Some boost to future oil prices, relative to last week, is reflected well into 2030s contracts. Higher oil prices => higher input and transportation costs => higher inflation. Not transient if it persists into the 2030s.

The war-criminal-in-chief has said today he doesn’t care about Iran’s nuclear stuff, but the front-month price remains over 4% higher on the day. Headlines reflect a continued buildup of U.S. weaponry near Iran, and that seems to be driving inflation and rate expectation.

So blast ’em again just for good measure, but with no real strategic goal? That’s what you do when the China trip ends in humiliation? Maybe that’s what a malignant narcissist does. We’ll see.