Friday’s jump in 10 year Treasury yields (10 bps), and the 30 year yield nearing 5% alarmed markets. But why?

Debt and the debt trajectory are up. Fed Chair Designate Warsh wants to shrink the Fed balance sheet, even as Trump continues his assault on Fed independence. And don’t expect the foreign sector to rush in to help…

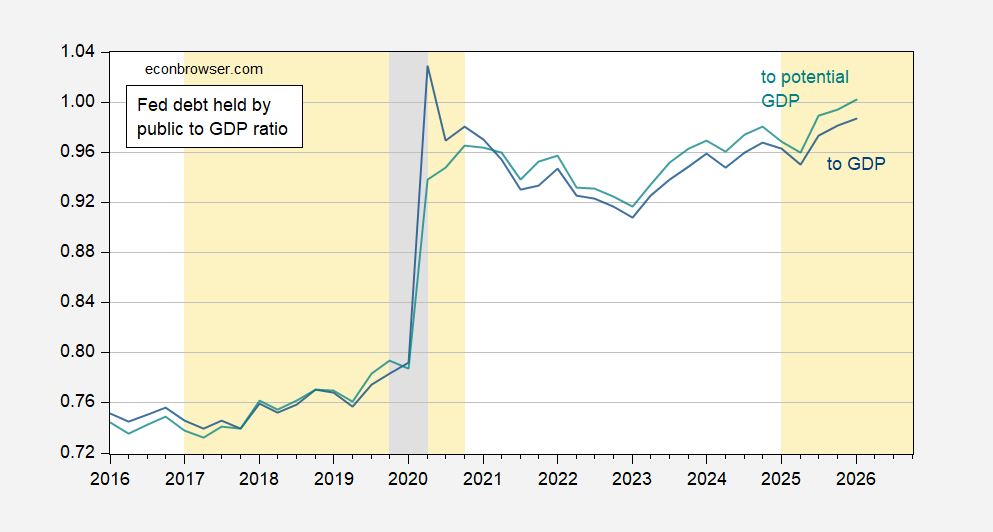

First, debt held by the public as a share of GDP:

Figure 1: Federal debt held by the public to GDP (blue), to potential GDP (teal). NBER defined peak-to-trough recession dates shaded gray. Source: Treasury, BEA via FRED; CBO (February 2026), NBER and author’s calculations.

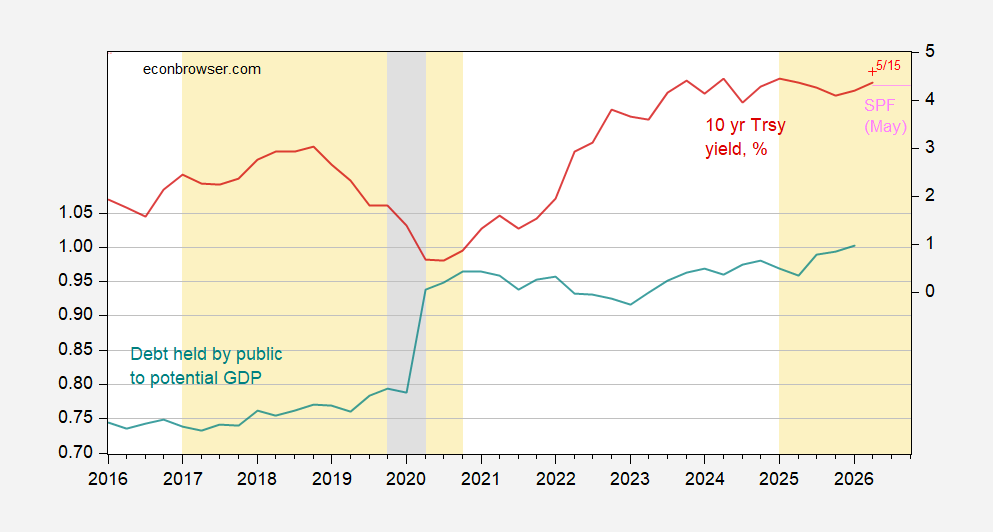

Second, debt and rates.

My work with Jeffrey Frankel (2005) indicates the debt to GDP ratio, expected changes in debt-to-GDP, expected inflation and output gap affect Treasury yields. This correlation is shown below.

Figure 2: Federal debt held by the public to potential GDP (teal, left scale), and 10 year Treasury yield (red, right scale), 5/15 COB observation (red +, right scale), SPF May mean forecast (pink, right scale), all in %. Q2 observation for 10 year yield is for data through May 15th. NBER defined peak-to-trough recession dates shaded gray. Source: Treasury, BEA via FRED; CBO (February 2026), Philadelphia Fed (May 2026), NBER, and author’s calculations.

Note that the 5/15 10 year yield has already jumped above the SPF forecast for Q2.

Subsequent work (Kitchen and Chinn, 2011) indicates that foreign holdings of Treasurys and Fed credit easing also play sigificant roles for rates. With newly confirmed Chair Warsh’s antipathy toward credit easing well-known, perhaps the timing of the rate rise might not be so surprising.

The U.S. has one of the lower ratios of central bank assets to GDP:

https://en.macromicro.me/charts/55993/cbs-total-assets-gdp-ratio

Globally, central bank assets have been falling since 2022, generally a period of tighter monetary policy:

https://en.macromicro.me/series/19275/major-cbs-total-assets

Warsh is apparently arguing to end the Fed’s policy of “ample reserves”. Here’s a description of how that policy works:

https://www.stlouisfed.org/publications/page-one-economics/2026/feb/fed-balance-sheet-and-ample-reserves

For us commoners, the implication of such a policy change is reduced liquidity in overnight funds, resulting in greater interest-rate volatility. Volatility in the cost of overnight funds means price volatility and reduced liquidity for financial assets in general. The Fed has operated in a lower reserve regime in the past and knows how to do it. The transition is still likely to be rocky if it occurs.

Seen from a great altitude, the question here is whether technocratic experts can, and should, craft policy interventions to improve welfare. Same old conservative/progressive squabble, with Warsh taking the conservative side.

Yeah, but nope. The dying dollar standard is why rates are rising. The Fed’s balance sheet is small already to totall assets which is 300 trillion. Reduce reserves , but it iis rrelevant. Problem is banks need higher rates to fund Trump’s deficits. They don’t have the dollars anymore and that situation has been building since 2012. Lower rates were just a phony debt bubble. Didn’t help a thing.

I believe I just pointed out that the Fed’s reserve holdings are small, relative to other countries. If you intend to correct my position, you need to:

1) Know what it is,

2) Disagree with it.

On the point of Fed holdings, you don’t, and you don’t.

The rest of your argument is mostly wrong, too. I don’t know what you mean by “the dying dollar standard”, and I don’t see any evidence that you do, either, in sufficient detail to make your point. The dollar is overwhelmingly the currency of choice for international transactions, and international transactions swamp reserve holdings, an order of magnitude larger. It is mostly private demand for dollar assets and dollar transactions which determine U.S. interest rates. Reserve demand, to the extent it changes, is an increment of total demand.

“To the extent it changes” is what our host is discussing here. Changes and levels matter, but in the short run, changes dominate. If Warsh gets his way, there will be a change in demand for Treasury assets. That change will effect interest rates. Your position seems to be that the change Warsh contemplates is not sufficient to drive this week’s rate rise, about 11 basis points. Are you sure you want to defend that position?

Happy to read any evidence, empirical or theoretical, that you’d care to offer in support of a “dying dollar standard”. Editorial hand-wringung, not so much.